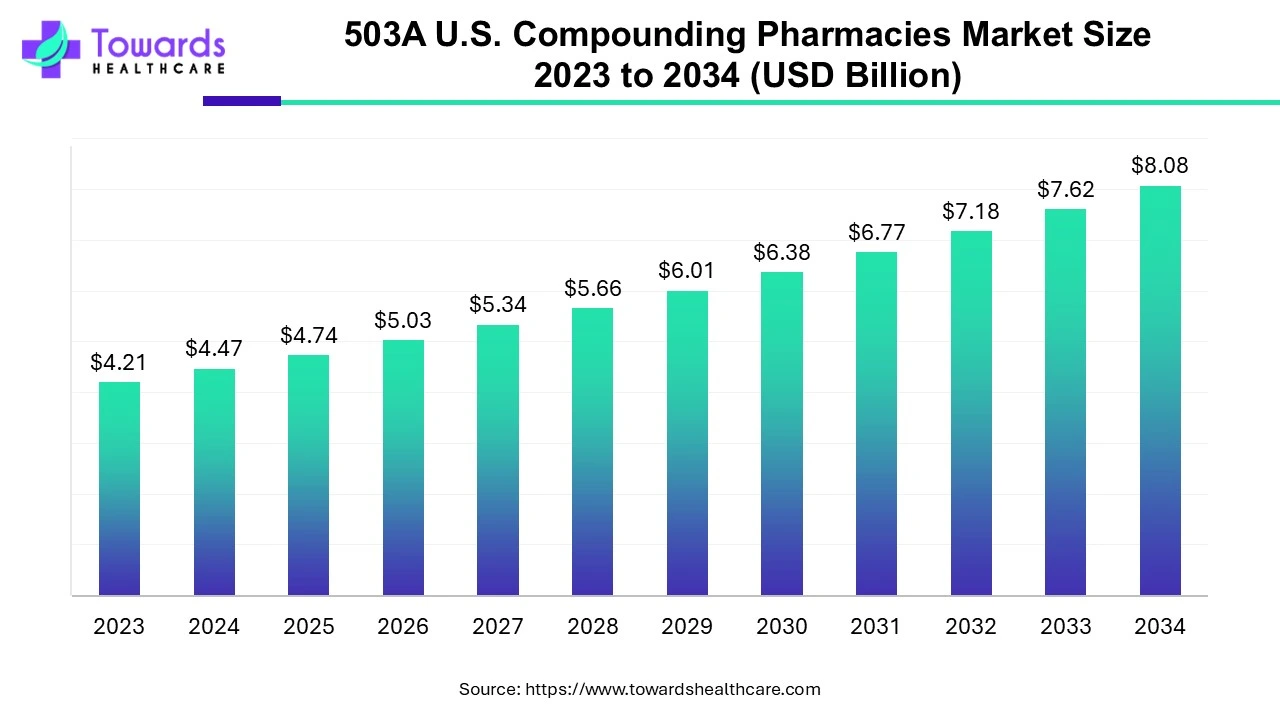

The 503A U.S. compounding pharmacies market is growing from USD 4.74 billion (2025) to an estimated USD 8.08 billion by 2034 (CAGR 6.11%), driven by demand for personalized, convenient, and accessible care for chronic and specialty conditions.

Market size

Current baseline & projection

• 2025 market size: USD 4.74B (base used in projection).

• 2034 projected size: USD 8.08B — implies steady growth at 6.11% CAGR across 2025–2034.

Market expansion components

• Volume growth — increasing prescriptions for personalized formulations (topicals, oral thin-films, rectal forms).

• Price / mix uplift — higher ASPs for specialty, patient-tailored, allergen-free, or complex compounded products.

• Service expansion — growth of veterinary compounding and niche therapy areas (HRT, pain management).

Addressable patient population

• Chronic disease prevalence (cardiovascular disease, cancer, diabetes) expands the potential user base. The report cites 859,000 annual CVD deaths, 1.7M cancer diagnoses, and 37.3M Americans with diabetes — all signals of a large, recurring medication need pool.

Revenue drivers

• Repeat prescriptions for chronic conditions.

• High-value customized products (hormone replacement pellets/creams, topical pain cocktails, sterile injectables when patient-specific).

• Cross-sector demand (human + veterinary compounding).

Cost drivers affecting market size

• Capital investments for compliance (controlled environments for USP <797>/<800>), automation for sterile compounding, and robust QA systems.

• Labor: licensed pharmacists and trained compounding technicians.

• Raw material sourcing for niche APIs and excipients.

Margins & unit economics

• Higher gross margins on bespoke products (limited competition, premium pricing) but offset by compliance costs and specialized staff—net margin varies widely by firm size and service mix.

Serviceable Available Market (SAM) vs. Total Addressable Market (TAM)

• TAM: All patients needing customized medications (human + veterinary).

• SAM: Patients in jurisdictions/states served by compliant 503A pharmacies and willing/able to pay or with reimbursement. Growth in wholesale platforms and partnerships expands SAM.

Capital intensity & scale effects

• Small 503A pharmacies face steep fixed costs (infrastructure, documentation). Larger networks/partners (or hybrid 503A–503B relationships) achieve scale advantages—reflected in consolidation and acquisitions.

Forecast sensitivity

• Market projection is sensitive to regulatory shifts (e.g., stricter USP updates), reimbursement/payer decisions, and adoption of automation/AI (which can compress costs and increase capacity).

Takeaway

• The market’s growth to USD 8.08B is a blend of increasing patient demand (chronic diseases + aging), higher value per prescription via personalization, and operational scaling by larger providers—tempered by regulatory and compliance costs.

Market trends

Consolidation & strategic M&A activity

• Revelation Pharma’s acquisition of Cascade Specialty Pharmacy (Jan 2025) demonstrates vertical expansion into ENT and animal health compounding—a deliberate strategy to broaden therapeutic and veterinary portfolios.

Brand unification & multi-channel operations

• Empower’s rebrand (Feb 2025) and unification of 503A and 503B operations indicate a trend: firms are integrating 503A/503B capabilities for service breadth and brand clarity.

Capacity expansion of sterile compounding

• Empower’s new 503B facility in Houston (Mar 2025) increased sterile production capacity by >150% using automation/robots — signaling major investment to serve hospital/clinic sterile needs via outsourcing partners.

Technology & software tailored to compounding

• Fagron’s platform (Feb 2025) for workflow + patient-outcome tracking shows software is shifting from dispensing support to clinical outcomes and QA integration—improving compliance and demonstrating value to prescribers.

Wholesale & distribution innovations

• Sept 2024 coalition launched a national wholesale platform to streamline procurement for providers—reducing friction for order fulfillment and expanding compounding product reach.

Veterinary compounding growth

• Wedgewood adding molnupiravir and veterinary-focused mergers (2023 onward) highlight a rising veterinary compounding demand and cross-application of human antivirals to animal health.

Regulatory pressure shaping business models

• USP <795>/<797>/<800> updates and the 503A/503B distinction force capital investments, push for partnerships with 503B partners for sterile/hazardous compounding, and act as a barrier for small entrants.

Product mix evolution

• Oral remains dominant (2024), but rectal formulations forecast fastest growth — driven by targeted treatments for GI disorders and formulations tailored to patients who cannot use oral routes.

Clinical focus shifts

• Pain management holds significant share (2024) due to demand for topical multi-ingredient formulations; hormone replacement projected for highest CAGR due to aging population and demand for tailored HRT.

Patient centricity & personalization

• Personalized formulations (dose, carrier, allergen-free) and patient-preferred delivery forms (thin films, topicals) are central to market growth, improving adherence and perceived value.

AI roles & impacts for 503A compounding pharmacies

Automated formulation design & optimization

• ML models analyze physicochemical properties and suggest excipient combinations and concentrations that maximize stability and bioavailability for patient-specific doses.

Allergy & contraindication screening from EHR/Rx

• NLP extracts patient data and cross-checks allergies, drug interactions, and prior adverse events to flag unsafe excipients or combinations before compounding.

Predictive demand & inventory optimization

• Time-series models forecast prescription volumes (by molecule/formulation) reducing stockouts of niche APIs and minimizing costly overstock of short-shelf APIs.

Robotic compounding orchestration & quality control

• AI controls robotic dispensing and mixing sequences, monitors in-process sensors (weight, viscosity, particulate counts), and halts runs if anomalies appear—improving precision and reducing cross-contamination risk.

Stability & beyond-use date prediction

• Models predict chemical/physical stability under specific excipients and storage conditions, enabling more accurate beyond-use dates and reducing waste or unsafe compounding.

Sterile environment monitoring & anomaly detection

• Computer vision and sensor fusion continuously monitor cleanroom parameters (particle counts, airflow, gowning compliance), with alerts and automated corrective suggestions.

Personalized dosing algorithms

• Using patient age, weight, comorbidities, and PK/PD models, AI proposes individualized dose ranges and compounding instructions for prescriber review—helpful for pediatrics or HRT titration.

Regulatory compliance automation & audit trails

• Intelligent documentation systems auto-generate batch records, chain-of-custody logs, and evidence for USP/FDA compliance—streamlining inspections and reducing manual error.

Clinical outcome tracking & feedback loops

• Platforms collect patient outcomes (pain scores, side effects) and feed models that correlate formulation variables with efficacy, guiding iterative improvement of formulations.

Prescription intake & prior authorization automation

• NLP intake systems parse physician notes, verify patient-specific prescription validity, and populate forms for payers when needed—reducing turnaround time and administrative burden.

Net effect: AI can raise throughput, accuracy, and clinical value while lowering per-unit costs and compliance risk — but requires investment, validation, and careful regulatory alignment.

Regional insights

Florida

• Demographics & demand: Large aging population and retirement communities → elevated HRT and chronic pain management demand.

• Veterinary opportunity: High pet ownership and veterinary practices increase demand for veterinary compounding (e.g., Wedgewood’s veterinary interest).

• Regulatory landscape: State board practices and local compounding standards can vary, necessitating localized QA practices.

California

• Scale & innovation hub: Large population plus proximity to biotech and digital health companies → earlier adoption of tech platforms (e.g., workflow/patient outcome software).

• High regulatory scrutiny & cost: Stricter enforcement and high operating costs push smaller pharmacies toward partnerships or niche differentiation.

• Telehealth forwarding: High telemedicine adoption supports remote prescribing for compounded products.

Chicago (Illinois metropolitan area)

• Hospital and clinic concentration: Strong hospital networks increase demand for sterile, patient-specific injectable formulations via 503B partners when volumes are needed.

• Distribution node: Major logistics hubs ease supply chain for APIs and specialty packaging.

New Jersey

• Pharma cluster influence: Proximity to pharma manufacturing drives API sourcing and workforce with specialized skills (sterile compounding, QC).

• Regulatory & compliance expertise: Access to legal and regulatory consultants helps firms navigate USP/FDA expectations.

Pennsylvania

• Aging rural/urban mix: Both community pharmacy needs and specialty clinics; potential for niche outpatient compounding and pain management solutions.

• Institutional purchasers: Hospitals and specialty clinics in PA may favor 503B for bulk sterile needs—opportunity for 503A–503B partnerships.

Rest of the U.S.

• Fragmentation & opportunity: Many states have underserved rural populations; local 503A pharmacies provide access to tailored medicines where commercial products are unavailable.

• Growth corridors: States with growing elderly populations and rising chronic disease burdens will be demand hotspots.

Regional execution considerations

• State board variability: Differences in enforcement and guidance for 503A compounding require region-specific compliance playbooks.

• Distribution & logistics: Cold chain or controlled temperature distribution needs (e.g., for biologics or fragile APIs) vary regionally and affect unit economics.

• Partnership models: Where sterile or bulk needs exist, 503A players increasingly partner with 503B regional facilities to serve institutional customers.

Market dynamics

Growth drivers

• Personalization demand for chronic disease management (CVD, cancer, diabetes) and aging population.

• Novel delivery forms (oral thin-films, topical multi-ingredient blends) and increased acceptance by prescribers.

Regulatory & compliance forces (key barrier)

• USP <795>/<797>/<800> and state board rules require facilities, environmental controls, and documentation; significant capital and operational costs create high entry barriers.

Supply-side constraints

• API availability for niche compounds, specialized excipients, and the need for validated suppliers drive procurement complexity.

• Skilled workforce shortage for sterile compounding and QA roles limits rapid scale-up.

Technology adoption

• Automation (robotics) and software platforms (e.g., compounding workflow + outcomes) increase capacity, reduce errors, and become competitive differentiators.

Competitive structure & consolidation

• Mix of small community 503A pharmacies and larger vertically integrated companies (that may also operate 503B). Acquisitions (e.g., Cascade by Revelation) and network formation (national wholesale platform) are consolidation trends.

Price & reimbursement dynamics

• Many compounded products are paid out-of-pocket or reimbursed variably—reimbursement uncertainty affects demand elasticity.

• Direct-to-consumer pricing tools (like Optum’s PriceEdge for conventional meds) suggest payers and PBMs could increasingly influence compounded product uptake.

Demand heterogeneity

• Therapeutic concentration in pain management and rising CAGR in hormone replacement make certain segments more attractive for focused investment.

Risk factors

• Regulatory crackdowns or adverse safety events could suppress demand and increase compliance costs.

• Supply chain disruptions for APIs or packaging materials.

Opportunity spaces

• Veterinary compounding, specialty niche formulations (rectal for GI conditions), HRT, and outcome-driven software services present high growth and margin opportunities.

Strategic implications

• Successful players combine regulatory proficiency, clinical outcome evidence, tech-enabled workflows, and selective scale (or partner models) to compete profitably.

Top 10 companies

Triangle Compounding

• Product/Overview: Traditional compounding pharmacy offering customized human medications (oral, topical).

• Strengths: Localized patient focus, clinician relationships, agility to produce niche formulations quickly.

Fagron

• Product/Overview: Global compounding supplier and software/platform provider (recently introduced a 503A-tailored platform).

• Strengths: Technology integration for workflow + outcomes, supply chain breadth for excipients/APIs, scale in compounding support services.

B. Braun SE

• Product/Overview: Large medical device/pharmaceutical company with compounding/sterile solutions and equipment.

• Strengths: Manufacturing experience, sterile systems expertise, global QA standards, ability to supply institutional customers.

Pencol Specialty Pharmacy

• Product/Overview: Niche specialty and compounding services, likely catering to specialty therapeutic areas.

• Strengths: Specialty pharmacy capabilities, patient support programs, clinical services around complex therapies.

Vertisis Custom Pharmacy

• Product/Overview: Custom compounding pharmacy focusing on personalized human formulations.

• Strengths: Customization, clinician partnerships, possible regional expertise.

Optum Inc

• Product/Overview: Large health services company; provides tools like PriceEdge for pricing transparency and has pharmacy services.

• Strengths: Data & payer reach, pricing tools, integration with pharmacy benefit management and wide distribution channels.

Pavilion Compounding Pharmacy, LLC.

• Product/Overview: Compounding pharmacy serving human patients with custom formulations.

• Strengths: Clinical focus, potential regional network, patient service models.

Village Compounding Pharmacy

• Product/Overview: Community-oriented compounding provider with human and possibly veterinary lines.

• Strengths: Local clinician ties, rapid turnaround for patient-specific prescriptions.

McGuff Compounding Pharmacy

• Product/Overview: Compounding and specialty pharmacy operation.

• Strengths: Experience in complex formulations and possibly lab/sterile capabilities.

Wedgewood Pharmacy

• Product/Overview: Strong presence in veterinary compounding and human compounding; formulary additions such as molnupiravir for veterinary use noted.

• Strengths: Veterinary expertise, formulary development, mergers that expanded service capability and speed.

Overall note: Strengths split across these firms include technology platforms (Fagron, Optum), institutional scale and sterile capability (B. Braun, Empower from trends), clinical/veterinary specialization (Wedgewood), and agility/local service (Triangle, Village, Pavilion).

Latest announcements

Empower corporate rebrand & unification (Feb 2025)

• What happened: Empower introduced a new corporate logo and unified its 503A compounding pharmacy and 503B outsourcing facilities under one brand.

• Strategic implications: Improves market clarity, facilitates cross-selling between retail/patient-specific and larger outsourcing services, and signals strategic intention to be a full-spectrum compounding provider.

Revelation Pharma acquires Cascade Specialty Pharmacy (Jan 2025)

• What happened: Acquisition to integrate ENT and Animal Health compounding into Revelation’s portfolio.

• Strategic implications: Expands therapeutic reach (ENT), adds veterinary capabilities, and strengthens Revelation’s compounding network—illustrative of consolidation and diversification.

LRockRx opens new 503A facility in Little Rock (Dec 2024)

• What happened: New facility expected to create ~100 jobs, average salary ~$100,000.

• Strategic implications: Regional investment increases local access, creates high-skilled jobs, and signals confidence in market growth.

Empower opens second 503B in Houston (Mar 2025)

• What happened: New 503B facility expanded sterile manufacturing capacity by >150%, using automation and robotics.

• Strategic implications: Enhances sterile outsourcing capacity for hospitals/clinics, and shows the interplay between 503A retail compounding and 503B bulk sterile supply.

Fagron launches a 503A compounding software platform (Feb 2025)

• What happened: Platform pairs compounding workflow management with patient outcome tracking.

• Strategic implications: Increased emphasis on measurable clinical outcomes and QA; can be a competitive differentiator for pharmacies showing real-world effectiveness.

Industry educational pieces & guidance (Nov 2024)

• What happened: PharmD candidates and pharmacists published guidance distinguishing 503A vs 503B and advising collaboration strategies amid USP updates.

• Strategic implications: Knowledge sharing encourages partnerships and risk mitigation strategies for sterile/hazardous compounding.

Recent developments

National wholesale platform launched (Sept 2024)

• Detail: Coalition of 503A/503B pharmacies created a national wholesale ordering platform to simplify procurement for providers—improves ordering reliability and reach for smaller clinics.

Wedgewood formulary additions & veterinary focus (Sept 2024 onward)

• Detail: Wedgewood added molnupiravir to its formulary; merged with veterinary prescription management to speed service—shows rising veterinary and infectious-disease related compounding.

Mergers & partnerships to widen service scope (2023–2025)

• Detail: Several small/medium players have merged or been acquired (e.g., Cascade by Revelation), indicating consolidation and network building.

Technology & automation investments

• Detail: Empower’s robotic sterile capacity expansion and Fagron’s software point to a dual trend: physical automation + digital workflow/clinical data.

Clinical/therapeutic shifts

• Detail: Pain management dominated share (2024); hormone replacement sees fastest projected growth due to aging demographics.

Segments covered

By product

• Oral (Dominant, 2024): High patient acceptance — includes liquids, capsules, thin films. Advantages: portability, taste/appearance customization, high compliance. Compounding focus: allergens removal, dose adjustments (pediatrics/elderly), flavored suspensions.

• Liquid Preparations: Useful for pediatric and geriatric patients; stability and preservative issues require tight QA.

• Topical: Widely used in pain management (multi-ingredient creams); benefits: targeted delivery, reduced systemic exposure. Challenges: absorption variability, homogeneity of active distribution.

• Rectal (Fastest growth forecast): Indicated for local GI therapy (IBD) and for patients unable to use oral route. Compounding benefits include precise local dosing and combinations of anti-inflammatories. Manufacturing challenge: patient acceptability and formulation stability.

• Ophthalmic / Nasal / Otic: Specialized sterile or preservative-free formulations needed; high regulatory scrutiny for sterility. Nasal delivery increasingly used for systemic rapid onset or local therapies.

By sterility

• Sterile: Higher capital and compliance demands (cleanrooms, laminar flow, validated aseptic processes). Sterile compounding is often routed through 503B partners for higher volumes.

• Non-Sterile: Lower infrastructure needs; commonly used for topicals, many oral formulations.

By therapeutic area

• Hormone replacement: Fastest projected CAGR; requires titration and tailored dosing for individual hormonal needs. Market driven by aging population and tailored HRT regimens.

• Pain management: Significant share (2024); multi-ingredient topical creams and bespoke oral pain regimens popular due to cost-effectiveness and avoidance of systemic opioid side effects.

• Dermatology / Pediatrics / Urology / Others: Each area leverages compounding for formulations not commercially available, allergy avoidance, or pediatric dosing.

By end-user

• Oral (Patients): Direct patient prescriptions dominate 503A.

• Hospitals & Clinics / Specialty Clinics: More sterile and higher-complexity demands; often satisfied via 503B outsourcing for volume/sterility.

• Other: Veterinary clinics and specialty care providers.

By geography

• Florida / California / Chicago / New Jersey / Pennsylvania / Rest of U.S.: Regional demand drivers discussed in Regional Insights section.

Top 5 FAQs

-

Q: What is the projected size of the U.S. 503A compounding pharmacies market?

A: The market is projected to grow from USD 4.74 billion (2025) to USD 8.08 billion by 2034, at a 6.11% CAGR for 2025–2034. -

Q: Which product type currently dominates the market and which will grow fastest?

A: Oral products held a dominant presence in 2024. Rectal products are projected to expand the fastest over the forecast period due to needs in GI and local therapies. -

Q: What therapeutic areas are most important in this market?

A: Pain management was a significant market shareholder in 2024; hormone replacement therapy (HRT) is expected to grow with the highest CAGR due to an aging population demand. -

Q: How do 503A pharmacies differ from 503B outsourcing facilities?

A: 503A pharmacies compound patient-specific prescriptions for individual patients and generally do not produce large batches or office-use stock; 503B facilities can produce larger batches for office use and are subject to outsourcing facility regulations—leading many 503A pharmacies to partner with 503B providers for sterile/hazardous or bulk needs. -

Q: What are the main barriers to entering the 503A compounding market?

A: Regulatory compliance (USP standards, state board rules), capital investments in controlled environments, staffing and quality systems, and validated supplier channels—these make entry expensive and complex for newcomers.

Access the Dashboard: https://www.towardshealthcare.com/access-dashboard

Immediate Delivery Available | Buy This Premium Research @ https://www.towardshealthcare.com/price/5070

Become a valued research partner with us – https://www.towardshealthcare.com/schedule-meeting

You can place an order or ask any questions, please feel free to contact us at sales@towardshealthcare.com

Powering Healthcare Leaders with Real-Time Insights: https://www.towardshealthcare.com/healthcare-intelligence-platform

Europe Region – +44 778 256 0738

North America Region – +1 8044 4193 44

APAC Region: +91 9356 9282 04

Web: https://www.towardshealthcare.com

Find us on social platforms: LinkedIn | Twitter | Instagram | Medium | Pinterest