The global endoscopy devices market was valued at USD 61.1 billion in 2024, increased to USD 63.44 billion in 2025, and is projected to reach USD 88.55 billion by 2034, growing at a CAGR of 3.82% (2025–2034). North America dominated in 2024, while Asia-Pacific is expected to grow the fastest. By product, endoscopes led the market, and by end-use, outpatient facilities held the largest share in 2024.

Download the free sample and get the complete insights and forecasts report on this market @ https://www.towardshealthcare.com/download-sample/5425

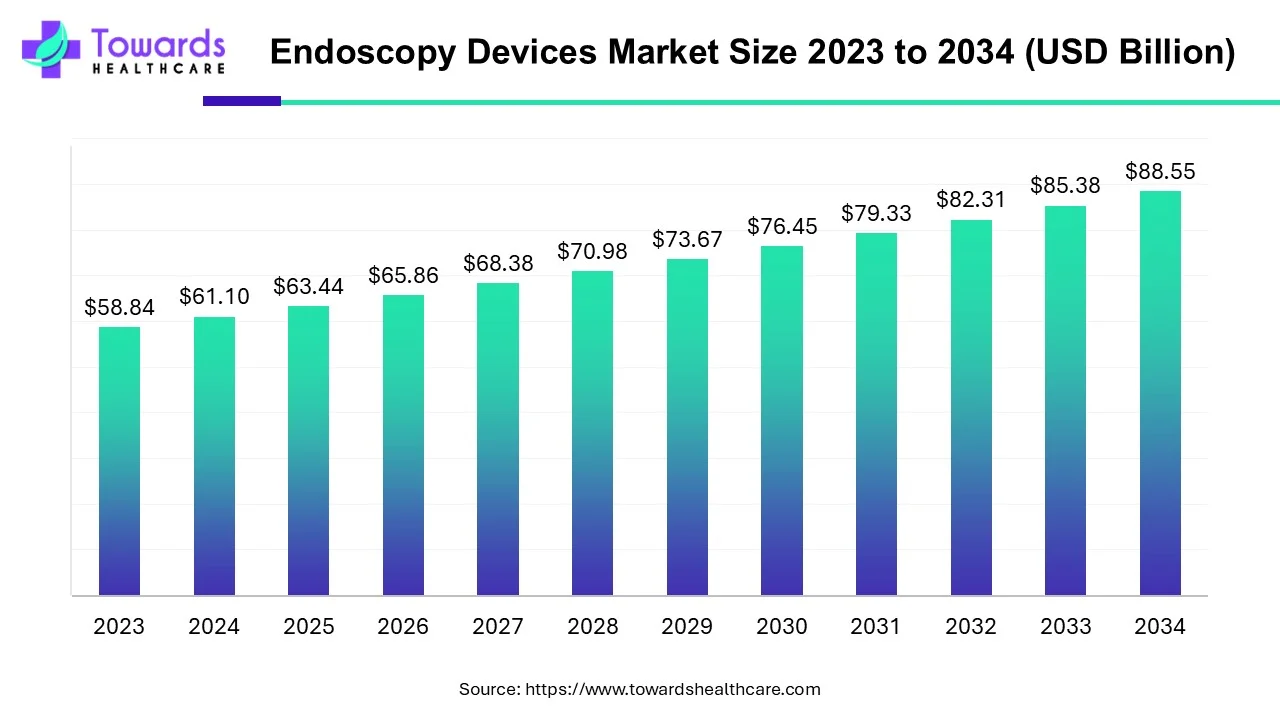

Market Size

◉2023: USD 59.5 billion (pre-2024 growth baseline).

◉2024: USD 61.1 billion (driven by chronic disorders, surgeries, tech adoption).

◉2025: USD 63.44 billion.

◉2034: USD 88.55 billion (CAGR 3.82%).

◉North America (2024): Largest share due to chronic disorders prevalence, advanced infrastructure, and major players.

◉Asia-Pacific (2025–2034): Fastest-growing region with strong government support (e.g., “Made in China,” “Make in India”).

◉By product (2024): Endoscopes dominated, visualization systems poised for highest growth.

◉By end-use (2024): Outpatient facilities led, hospitals expected to rise.

Market Trends

1 Capsule & robotic capsules transition from pilot to diffusion

◉AIG Hospitals (India) launched PillBot (2024); FDA trial review expected 2025, with global market entry targeted 2026 → non-invasive GI screening, remote navigation, and AI-assisted triage.

◉UHealth Miami (2024) deployed capsule endoscopy for small bowel mucosa → convenience and access gains.

◉Capital flows into endoscopy R&D

◉Sotelix Endoscopy ($1.7M seed, Dec 2024) to develop minimally-invasive GI devices → accelerates niche indications and disposables.

◉Imaging leap: 4K/HD + 3D + molecular probes + cloud

◉4K visualization systems and HD camera heads are standardizing; targeted molecular probes and cloud data management improve lesion detection and longitudinal care.

2 Front-line innovation in Europe

◉NEUROGATE holographic endoscope (Feb 2025) funded €2.5M → higher-dimensional visualization for neuroscience and research use-cases.

3 Commercial momentum from majors

◉Boston Scientific 2024 full-year revenue $16.747B (↑17.6% YoY) — strong minimally invasive portfolio.

◉Stryker 2024 net sales $22.6B (↑10.2%); guides 8–9% organic growth.

◉Smith+Nephew 2024 revenue $5.81B; margin improvement.

◉Hologic Q4 CY2024 revenue ~$1.02B; operating margin ↑ to 22.5%.

4 Single-use endoscopy expands

◉Ambu leadership message (2024): single-use supports infection control and sustainability priorities → faster turnover; reduced reprocessing logistics.

5 Regional launches catalyze adoption

◉Olympus EVIS X1 showcased in Mexico (2024) → physician training, education, and demand seeding in LatAm.

6 Institutional volume growth

◉UAE EHS: 425 advanced procedures in Q1-2025 at Kuwait Hospital, Sharjah; 782 procedures in H1-2024 → sustained utilization and capacity build-out.

◉Saudi MOH: 177,744 surgeries in H1-2023 → large base for endoscopic integration.

AI in Endoscopy

1 Pre-procedure decision support

◉Risk stratification for GI screening cohorts; prioritization lists optimize suite utilization and reduce wait times.

2 Intra-procedure computer vision

◉Real-time polyp/lesion detection on live video (frame-level inference with CNN/transformer hybrids).

◉Invasion depth estimation and tissue characterization to triage for resection vs biopsy vs surveillance.

3 Biopsy minimization & precision therapeutics

◉AI-enabled optical biopsies reduce unnecessary tissue sampling; parameterized energy delivery and robot-assisted targeting for precise resection.

4 Adaptive visualization pipelines

◉Auto-tuning exposure, denoising, stabilization, and 3D reconstruction; multi-spectral overlays for margins and perfusion cues.

5 Capsule autonomy and tele-endoscopy

◉Robotic capsules with path-planning; remote steering; AI triage flags for escalation to conventional endoscopy.

6 Post-procedure analytics & surveillance

◉Structured reporting, outcomes prediction, and recurrence surveillance reminders integrated with EHR.

7 Operational AI

◉Case-mix forecasting, consumables planning, reprocessing cycle optimization; downtime reduction via predictive maintenance.

8 Quality & equity guardrails

◉Dataset curation (diverse anatomies, pathologies), bias checks, video ground-truthing; audit trails meet SaMD expectations.

9 Deployment architecture

◉Edge inference (on-scope processors) for latency-critical alerts; cloud for fleet learning and updates; privacy by design.

10 Commercial impact

◉Higher diagnostic yield, fewer repeat procedures, lower total cost of care → stronger value-based purchasing arguments for providers and payers.

Regional Insights

1 North America (2024 leader)

◉Burden of chronic disease and high procedure volumes drive utilization; favorable reimbursement and capital availability sustain upgrades to 4K/HD and AI add-ons.

◉Presence of majors (Boston Scientific, Stryker, Hologic) shortens innovation diffusion cycles.

◉Canada (Ontario, 2024): +60,000 publicly-funded GI endoscopies at community centers → shift from hospitals to outpatient settings.

2 Asia–Pacific (fastest growth)

◉Industrial policy (“Make in India,” “Made in China”) + local manufacturing lowers device costs and expands access.

◉India: strong government initiatives, rising awareness, and capsule/robotic pilots (e.g., PillBot launch in India in 2024).

◉China: accelerated uptake in minimally invasive procedures; AI/HD imaging diffusion; favorable infrastructure build-out.

◉Japan, South Korea, Thailand: mature provider networks become early adopters of 3D/AI visualization.

3 Europe

◉Technology leadership in HD/AI; research funding (e.g., NEUROGATE) drives next-gen visualization.

◉Germany & UK: robust demand from aging populations; high procedural quality standards push adoption of advanced scopes and visualization stacks.

4 Latin America

◉Mexico (2024): EVIS X1 launch catalyzes physician education; medical tourism supports demand for minimally-invasive GI.

◉Urban private hospitals move first; public systems follow with cost-effectiveness evidence.

5 Middle East & Africa

◉UAE: documented growth in advanced endoscopy procedures; focus on AI adoption and specialized units.

◉Saudi Arabia: high surgical throughput, significant share in general/OB-GYN/ophthalmic, underpinning endoscopy utilization.

◉Regional governments deploy incentives for high-tech equipment to modernize care.

Market Dynamics

1 Drivers

Rising surgery volumes

◉313M surgeries annually (from your data). Endoscopy is integral to diagnosis and therapy across GI, pulmonary, urology, gynecology, neuro, and ortho.

Aging populations & chronic disease prevalence

◉Higher incidence of GI cancers, IBD, GERD, COPD → more diagnostic and interventional endoscopy.

Technology upgrades

◉4K/HD, 3D, molecular probes, robotics, AI raise detection rates and workflow efficiency, justifying capital spend.

Outpatient shift

◉Payers and providers prefer ambulatory settings for minor/intermediate procedures → higher turnover and device utilization.

2 Restraints

High acquisition & lifecycle cost

◉Average $3,600 cited for endoscopic devices in the U.S. (from your data) plus maintenance and reprocessing logistics → budget constraints for LMICs.

Reprocessing complexity

◉Sterilization workflow, staff training, and compliance → operational friction and infection-control risk if mishandled.

3 Opportunities

Capsule & single-use expansion

◉Lower infection risk, faster turnover, access to remote/low-infrastructure settings; strong fit for screening programs.

AI augmentation

◉Better detection, fewer biopsies, shorter procedure times; compelling ROI under value-based care.

Localization of manufacturing

◉APAC incentives reduce COGS, improve supply assurance, and tailor devices to local needs.

4 Challenges

Regulatory throughput

◉Evidence generation for AI features and novel capsules; validation and post-market surveillance burdens.

Workforce & training

◉Learning curves for 3D/AI systems; need for simulation and credentialing.

Data governance

◉Privacy, cybersecurity, and cross-border data transfer for cloud-connected systems.

Top Companies in the Endoscopy Devices Market

1 Boston Scientific Corporation

◉Products: Minimally invasive GI & pulmonary endoscopy systems and accessories.

◉Overview: Global leader in less-invasive endoscopy for diagnosis/treatment.

◉Strengths: 2024 revenue $16.747B (↑17.6% YoY); scale, R&D cadence, and procedure-focused ecosystems.

2 Olympus Corporation

◉Products: Flexible endoscopes; EVIS X1 platform; visualization components.

◉Overview: Flagship imaging brand in GI endoscopy.

◉Strengths: Large installed base; training networks; LatAm expansion (Mexico 2024) via EVIS X1 demos.

3 Stryker Corporation

◉Products: Surgical visualization stacks, scopes, operative tools.

◉Overview: Broad med-surg and neurotechnology footprint.

◉Strengths: 2024 net sales $22.6B; strong MedSurg integration and capital placement model.

4 Smith & Nephew

◉Products: Arthroscopes, laparoscopy solutions, operative devices.

◉Overview: Procedural focus in sports medicine and general surgery.

◉Strengths: $5.81B (2024) with margin improvement; outpatient-friendly portfolio.

5 Hologic

◉Products: Imaging and minimally invasive diagnostic technologies.

◉Overview: Disciplined execution and margin profile.

◉Strengths: Q4 CY2024 revenue ~$1.02B; operating margin 22.5%.

6 Medtronic plc

◉Products: Endoscopy devices spanning GI and surgical visualization.

◉Overview: Scale in surgical and chronic therapy ecosystems.

◉Strengths: Hospital relationships and multi-category bundling.

7 Karl Storz

◉Products: Rigid/flexible scopes; visualization components.

◉Overview: Strong in surgical specialties (urology, ENT, general surgery).

◉Strengths: Engineering depth and broad catalog coverage.

8 Fujifilm Holdings

◉Products: GI endoscopes, processors, and accessories.

◉Overview: Imaging heritage applied to endoscopy.

◉Strengths: Advanced image processing and visualization.

9 Pentax Medical

◉Products: GI scopes and visualization systems.

◉Overview: Focused GI portfolio.

◉Strengths: Clinical relationships and service models in GI.

10 Conmed

◉Products: Operative devices, energy systems, hand instruments.

◉Overview: Complements endoscopic interventions.

◉Strengths: Breadth in disposables supports recurring revenue.

◉Aesculap (B. Braun), C.R. Bard, Activ Surgical, Auris Health, Hologic, Smith & Nephew

◉Collective strengths: Specialty breadth, hospital access, and/or enabling AI/robotics features depending on sub-segment.

Government Healthcare Spending & Policies

◉Public funding to clear backlogs (Canada/Ontario, 2024): +60,000 GI endoscopies in community centers → shifts case volume to lower-cost outpatient settings; raises demand for visualization stacks and single-use accessories.

◉Industrial policy (India/China): “Make in India/Made in China” encourage local device manufacturing, joint ventures, and supplier clustering → lower COGS, faster service, and pricing flexibility for public tenders.

◉Provider modernization (UAE, Saudi): Incentives for cutting-edge technologies (AI modules, capsule pilots) plus high baseline surgical volumes → higher penetration of advanced endoscopy.

◉Reimbursement dynamics (developed markets): Coverage for screening and minimally invasive procedures underpins utilization; hospitals can justify capital upgrades through quality metrics and throughput.

Global Healthcare Production Insights

◉APAC as production hub: Policy support + labor/optics/supply-chain clusters → competitive manufacturing for scopes, processors, and disposable sets.

◉R&D in US/EU; scaling in APAC: High-end modules (processors, imaging algorithms) conceived in US/EU; volume scaling in APAC for cost efficiency.

◉Shift to single-use: Reduces sterilization burden; increases recurring demand for consumables; needs supply-chain reliability and waste management strategies.

◉Quality & compliance: ISO 13485-aligned QMS, validation of reprocessing (for reusables), and post-market surveillance especially for AI-enabled features.

Segments Covered

1 By Product — Endoscopes

Reusable (Rigid/Flexible):

◉Rigid: Laparoscopes, arthroscopes, urology/ENT scopes → durable optics; high image stability.

◉Flexible: GI, bronchoscopes, cystoscopes, hysteroscopes → navigation in tortuous anatomy; require careful reprocessing.

Capsule Endoscopes:

◉Swallowed devices with miniature cameras; ideal for small bowel; remote monitoring; expanding to robotic/remote-◉controlled use (e.g., PillBot trajectory).

Robot-Assisted Endoscopes:

◉Enhanced dexterity, precise targeting; supports complex resections with steady imaging.

Disposable Endoscopes:

◉Infection-control advantage; lower reprocessing overhead; growing in high-throughput and community settings.

2 Endoscopy Visualization Systems

SD/HD/4K; 2D/3D:

◉HD/4K: Higher detection fidelity; margin assessment.

◉3D: Depth perception for suturing/dissection; shorter learning curves.

Visualization Components (Reusable & Disposable):

◉Camera heads, light sources, insufflators, processors, monitors, suction pumps, printers → integrated stacks; cloud-connectivity for storage/analytics.

3 Operative Devices

◉Energy Systems: Controlled resection/coagulation with minimal collateral damage.

◉Access Devices & Hand Instruments: Trocar systems, graspers, scissors, snares → procedural efficiency.

◉Suction/Irrigation & Wound Retractors: Field clarity; reduced complications.

◉Disposable counterparts: Standardized kits reduce setup time and cross-contamination risk.

By End-Use

Outpatient Facilities:

◉Dominant in 2024; ideal for minor/intermediate GI/ENT/ortho scopes; shorter LOS; payer alignment.

Hospitals:

◉Lucrative growth outlook with complex cases, ICU/ER adjacencies, robotics programs, and comprehensive reprocessing infrastructure.

By Region

◉North America, Europe, Asia–Pacific, Latin America, MEA: distinct adoption curves shaped by policy, reimbursement, and manufacturing presence (detail above).

Latest Announcements

◉Ambu CEO (2024): Advocated broader single-use endoscope development with sustainability as a strategic pillar → steers product roadmaps toward recyclable materials and efficient supply.

◉AIG Hospitals (India, Nov 2024): Public launch of PillBot (remote-controlled, robotic, disposable capsule) → indicates readiness for AI+robotics in mainstream GI pathways; aligns with affordability goals.

◉Olympus (Mexico, Jan 2024): EVIS X1 hands-on demos for clinicians and biomeds → accelerates training and downstream procurement in Latin America.

Recent Developments

◉NEUROGATE (Feb 2025): €2.5M grant to build a holographic endoscope for neuronal visualization → fertilizes cross-over into complex surgical guidance once validated.

◉Sotelix Endoscopy (Dec 2024): $1.7M seed for minimally invasive GI devices → strengthens early-stage pipeline for niche indications.

◉UHealth Miami (Dec 2024): Deployed capsule endoscopy for small bowel → reinforces patient-centric access models.

◉LOMO plc (Sep 2024): New video bronchoscope prototypes slated in the 2025 R&D plan → respiratory endoscopy innovation cadence.

◉UAE EHS (Q1-2025): 425 advanced endoscopy procedures; H1-2024: 782 procedures → sustained capacity growth and procedural mix complexity.

◉Saudi MOH (H1-2023): 177,744 surgeries total with sizable general/OB-GYN/ophthalmic shares → fertile ground for broader endoscopic uptake.

◉Corporate momentum (2024–2025):

◉Boston Scientific: $16.747B revenue (↑17.6% YoY).

◉Stryker: $22.6B net sales (↑10.2%); EPS growth; 8–9% organic outlook.

◉Smith+Nephew: $5.81B with margin gains.

◉Hologic: Q4 CY2024 ~$1.02B revenue; operating margin 22.5%.

Top 5 FAQs

1) What is the market size and growth outlook?

A: USD 61.1B (2024) → USD 63.44B (2025) → USD 88.55B (2034) at a stated CAGR of 3.82% (2025–2034).

2) Which region leads and which grows fastest?

A: North America led in 2024; Asia–Pacific is the fastest growing on policy support, manufacturing, and rising surgical volumes.

3) Which products are winning?

A: Endoscopes dominated 2024; visualization systems (HD/4K, 2D/3D, processors) show the strongest forward growth.

4) What’s the role of AI?

A: AI enhances detection, invasion depth assessment, workflow efficiency, and capsule autonomy, cutting biopsies and re-procedure rates.

5) What recent moves matter most?

A: PillBot launch (India, 2024), capsule deployments (Miami, 2024), NEUROGATE (€2.5M, 2025), Sotelix seed ($1.7M, 2024), and strong 2024 revenues from Boston Scientific, Stryker, Smith+Nephew, Hologic.

Access our exclusive, data-rich dashboard dedicated to the healthcare market – built specifically for decision-makers, strategists, and industry leaders. The dashboard features comprehensive statistical data, segment-wise market breakdowns, regional performance shares, detailed company profiles, annual updates, and much more. From market sizing to competitive intelligence, this powerful tool is one-stop solution to your gateway.

Access the Dashboard: https://www.towardshealthcare.com/access-dashboard

Immediate Delivery Available | Buy This Premium Research @ https://www.towardshealthcare.com/price/5425

Become a valued research partner with us – https://www.towardshealthcare.com/schedule-meeting

You can place an order or ask any questions, please feel free to contact us at [email protected]

Europe Region – +44 778 256 0738

North America Region – +1 8044 4193 44

Web: https://www.towardshealthcare.com

Find us on social platforms: LinkedIn | Twitter | Instagram | Medium | Pinterest