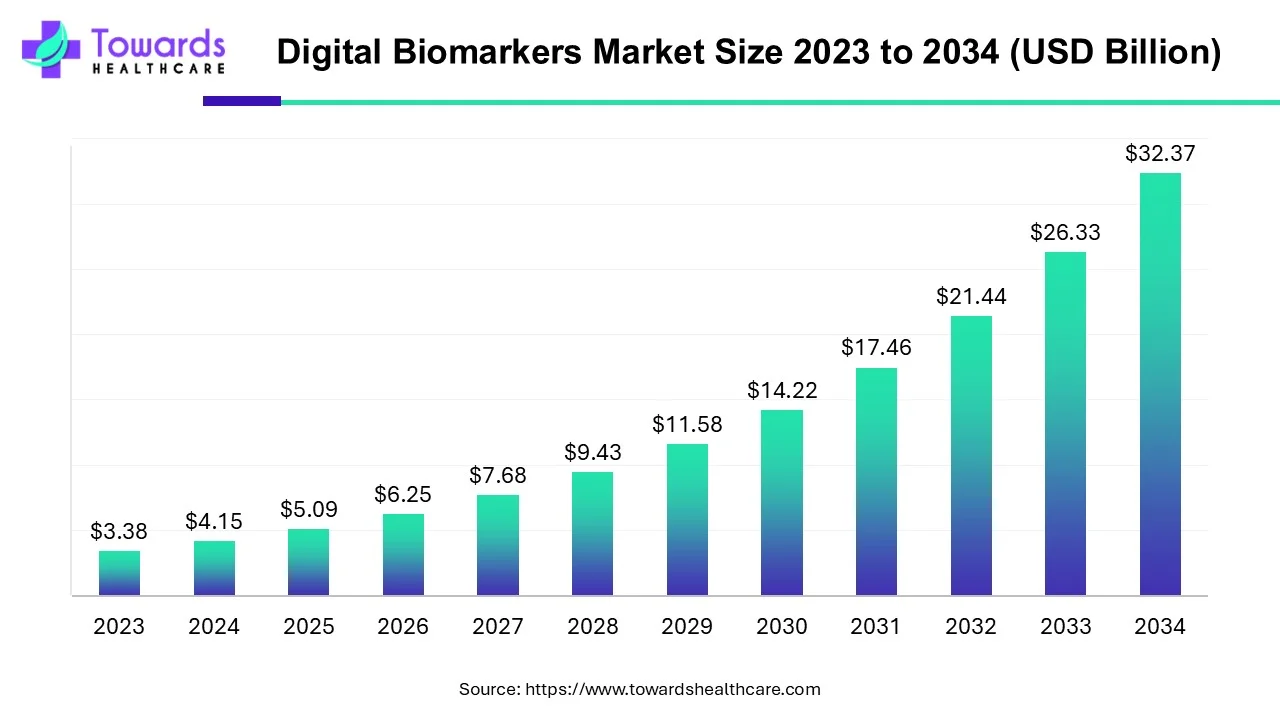

The global digital biomarkers market was valued at USD 5.09 billion in 2025 and is projected to reach USD 32.37 billion by 2034, growing at a CAGR of 22.74% (2025–2034).

Download the free sample and get the complete insights and forecasts report on this market @ https://www.towardshealthcare.com/download-sample/5434

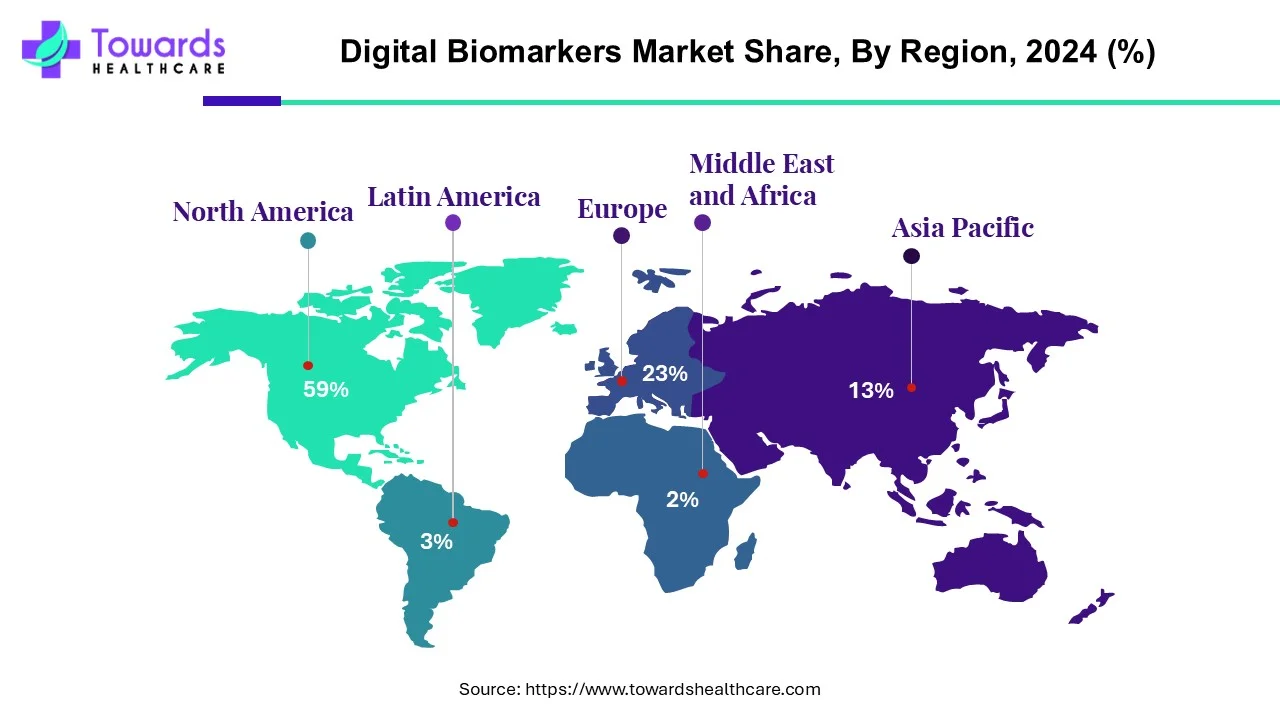

In 2024, North America led with 59% share, while Asia-Pacific is expected to expand fastest. Data collection tools dominated in 2024, while data integration systems are forecasted to grow rapidly. By end-use, healthcare companies held the largest share, and payers are projected to grow fastest.

Market Size

◉2024: USD 4.15 Billion

◉2025: USD 5.09 Billion

◉2034: USD 32.37 Billion

◉CAGR (2025–2034): 22.74%

◉Leading Region (2024): North America (59% market share)

◉Fastest Growing Region: Asia-Pacific (driven by NCDs, aging population, chronic diseases)

Market Trends

Investment Growth

◉Nov 2024: Glasswing Ventures + LDV Capital raised $2.6M for DANNCE.AI (neurological phenotyping platform).

◉Nov 2024: Quibim secured $50M Series A to expand AI-powered imaging biomarkers.

AI-Driven Innovations

◉Companies like AliveCor, Quibim, Biogen, and Empatica advancing AI-enabled monitoring.

Segmental Trends

◉Data Collection Tools (wearables, mobile apps) dominated 2024.

◉Data Integration Systems set to grow fastest due to interoperability needs.

Disease Focus

◉Cardiovascular diseases largest share (32% of global deaths per WHO).

◉Respiratory diseases fastest growing (asthma, COPD cases rising).

End-Use Trends

◉Healthcare companies largest users (R&D, clinical trials).

◉Payers (insurance) fastest-growing due to treatment personalization.

AI’s Role & Impact

Signal Engineering & Feature Discovery

◉Transform raw streams (PPG, ECG, accelerometry, voice, gait video) into validated features (variability, morphology, micro-movements).

◉Self-supervised and representation learning reduce labeling burden; discover latent disease signatures.

Disease Detection & Stratification

◉Early detection for neurological, mental health, and cardiovascular conditions via multi-modal fusion (wearable + phone usage + speech + imaging).

◉Risk stratification with calibrated probabilities to guide triage and care escalation.

Continuous Monitoring & Relapse Prediction

◉Drift-aware models update risk scores in near real-time; detect exacerbations (e.g., respiratory) days in advance; enable just-in-time interventions.

Drug Development Acceleration

◉Biomarker discovery for target engagement and endpoint sensitivity → shorter trials, smaller cohorts.

◉Virtual/hybrid DCTs (decentralized clinical trials): device-agnostic ingestion, anomaly checks, and near real-time safety/efficacy signals.

◉Adaptive designs informed by accumulating digital endpoints.

Clinical Validation & QA Automation

◉Automated artifact detection (motion/noise), outlier filtering, sensor QC, and audit trails for submission-grade data integrity.

Interoperability & Cohort Linkage

◉Entity resolution: harmonize EHR + claims + device with privacy-preserving linkage; federated learning reduces data movement risk.

Personalized Care Pathways

◉Therapy optimization engines: dose titration, behavioral nudges, and scheduling aligned to patient-level biomarker response.

Equity & Access

◉Lightweight models on commodity phones expand reach to rural/underserved areas; offline inference with store-and-forward sync.

Payer & Policy Analytics

◉AI converts continuous biomarkers into economic signals: expected avoidance of acute events, LOS reduction, and adherence prediction for value-based design.

Governance & Safety

◉Model lifecycle: bias testing, calibration, performance monitoring, and versioning; human-in-the-loop review for high-stakes alerts.

Regional Insights

North America (59% share, 2024)

Adoption Drivers

◉Mature digital health infrastructure; widespread wearables/CGMs and app ecosystems.

◉Regulatory enablement (SaMD, PreCert) supports iterative releases and post-market learning.

Use-Case Depth

◉Diabetes & CVD programs (CGMs, smartphone-based tracking), enterprise clinical trial integration.

Execution Enablers

◉Dense biopharma and CRO footprint; strong data engineering talent; reimbursement pilots.

Asia-Pacific (fastest growth)

Demand Fundamentals

◉Aging demographics + rising NCDs (55% of deaths in SE Asia, 2023).

◉Large populations create scale for low-cost, phone-centric biomarkers.

Adoption Vectors

◉Government digital health pushes; provider systems leapfrog to remote monitoring.

Constraints/Focus

◉Device affordability, language/localization, connectivity variance; huge upside via smartphone-native biomarkers.

Europe (notable growth)

Clinical Burden

◉CVD, stroke, cancer, diabetes → sustained demand for real-time diagnostics and monitoring.

System Levers

◉mHealth adoption + public system incentives; strong privacy governance favors privacy-preserving analytics.

Market Angle

◉High emphasis on precision medicine and interoperability standards in multi-country networks.

Latin America

Emergence Factors

◉Modernizing health IT; Brazil/Argentina lead pilots; preference for cost-effective mobile/wearable measures.

Operational Notes

◉Public-private partnerships; training and service models key to scale.

Middle East & Africa (MEA)

◉Growth Spots

◉UAE, Saudi: telehealth scale-ups; hospital digitization.

Challenges

◉Patchy infrastructure in parts of Sub-Saharan Africa → prioritize edge AI, offline workflows, low-power sensors.

Market Dynamics

Drivers

◉Regulatory advancement (SaMD updates, PreCert program concept).

◉Government initiatives: Funding + grants for telehealth and digital programs.

◉Wearables & sensors: Higher fidelity, lower cost, better battery → richer biomarker capture.

◉Enterprise adoption: Healthcare companies integrating biomarkers into drug development and clinical trials.

Restraints

◉Cybersecurity & privacy: High-value PHI targets; cross-border data flows raise risk.

◉Data & sample challenges: Motion artifacts, heterogeneous devices, adherence variance; need robust QA/validation.

Opportunities

◉Integration systems: Fastest-growing layer—interoperability, consent, identity, harmonization.

◉Payers: Rapidly rising demand for personalized authorization and outcomes-based programs.

◉Respiratory acceleration: Fastest growth area (from your data); monitoring and early intervention opportunities.

Structural Challenges (manage-to-win)

◉Clinical validation at scale; generalization across devices/populations.

◉Reimbursement playbooks for digital endpoints; health-economic evidence.

Top Companies (product/overview/strengths)

Roche Holding AG

Overview: Global leader in diagnostics & pharma integrating biomarker-driven precision medicine.

Products/Focus: Diagnostics platforms; digital pathology tie-ins.

Strengths: Scale, regulatory experience, oncology leadership, collaboration with Lunit (navify Digital Pathology).

Bio-Rad Laboratories

Overview: Major diagnostics & life science tools provider.

Products/Focus: Assay and analytics infrastructure relevant to biomarker validation.

Strengths: Installed lab base, quality systems, global distribution.

AliveCor

Overview: Digital cardiology pioneer.

Products/Focus: Mobile ECG-centric cardiac biomarkers.

Strengths: Clinical-grade cardiac signals, consumer-to-clinic bridge.

Biogen

Overview: Neuroscience-focused biopharma.

Products/Focus: Konectom™ smartphone digital biomarkers for neurological function (licensed to Indivi).

Strengths: CNS expertise; partnerships for wider disease coverage.

IXICO

Overview: Neuroimaging analytics company.

Products/Focus: Imaging biomarkers for neurodegeneration (fit for digital imaging pipelines).

Strengths: Trial analytics, disease-specific know-how.

Koneksa

Overview: Digital biomarker platform for clinical research.

Products/Focus: Device-agnostic endpoints, study data integration.

Strengths: Validation in trials; sponsor relationships.

Thermo Fisher Scientific

Overview: Global life sciences leader.

Products/Focus: Tools and platforms enabling data generation and analysis.

Strengths: Scale, compliance, enterprise reach.

Agilent Technologies

Overview: Analytical instrumentation and informatics.

Products/Focus: Measurement science and data environments relevant to biomarkers.

Strengths: Quality, lab informatics, regulatory posture.

Epigenomics AG

Overview: Biomarker discovery/diagnostics.

Products/Focus: Molecular biomarker platforms aligned to digital readouts.

Strengths: IP and assay expertise.

Fitbit Inc

Overview: Wearable device maker (now widely used for activity/physiological signals).

Products/Focus: Continuous data streams for digital biomarkers.

Strengths: Large installed base, consumer engagement.

Akili Interactive Labs

Overview: Digital therapeutic approaches.

Products/Focus: Software-based interventions with measurable biomarkers.

Strengths: Evidence-generating digital endpoints.

ALTODA AG

Overview: (As listed) European innovator in data/analytics for biomarkers.

Products/Focus: Digital analytics layers.

Strengths: Agility, niche expertise.

Kinsa

Overview: Connected thermometry and population signals.

Products/Focus: Symptom/temperature networks → community-level biomarkers.

Strengths: Real-time surveillance at scale.

Merck KGaA

Overview: Science & technology company.

Products/Focus: Oncology development paired with Quibim imaging biomarkers.

Strengths: R&D breadth; precision medicine collaborations.

Siemens Healthineers

Overview: Imaging/diagnostics giant.

Products/Focus: Imaging biomarkers and data integration across modalities.

Strengths: Hospital footprint; enterprise integration.

Huma

Overview: Digital health platform.

Products/Focus: Remote patient monitoring and biomarker capture.

Strengths: Configurable platform; multi-condition support.

Latest Announcements

Biofourmis (Sep 2024)

What: Four oncology collaborations; digital biomarkers + safety algorithms for CRS detection in trials.

Why it matters: Elevates digital biomarkers from supportive to primary safety infrastructure in high-risk oncology; strengthens device-agnostic DCT position.

Lunit × Roche (Sep 2024)

What: Lunit SCOPE PD-L1 22C3 TPS integrated into navify Digital Pathology.

Why: Brings AI pathology into a leading diagnostics workflow; accelerates biomarker testing and improves pathologist productivity—key to precision oncology.

Quibim × Merck KGaA (Jan 2024)

What: Imaging biomarker collaboration for oncology clinical development.

Why: Validates imaging biomarkers as core precision endpoints across multiple phases; boosts evidence generation for regulatory & payer acceptance.

Indivi × Biogen (Mar 2024)

What: Konectom™ smartphone platform licensed to Indivi for neurological assessment.

Why: Scales remote neuro biomarker monitoring; expands beyond MS into additional CNS diseases.

Recent Developments

electronRx — purpleDx (CES 2025)

What: Medical device-compliant cardiac evaluation app with digital indicators of lung function for CRD patients; clinician dashboards for real-time data.

Impact: Blends cardiopulmonary monitoring for comorbidity management; enables home-based assessment and therapy tailoring.

Roche × Lunit (2024)

Development Focus: AI-assisted pathology; improving biomarker testing speed and accuracy.

Impact: Standardizes tumor marker quantification; supports precision medicine workflows.

Biogen × Indivi (2024)

Focus: Multi-year expansion of digital neuro biomarkers; remote progression tracking.

Impact: Enriches longitudinal CNS data, reduces clinic burden, and supports adaptive trial designs.

Segments Covered

By System Component

◉Data Collection Tools (2024 leader)

◉Mobile Apps: Patient-facing capture (symptoms, PROs, phone sensors).

◉Wearables: Continuous physiology (activity, HR/HRV, sleep, rhythm).

◉Biosensors: Targeted measures (glucose, respiratory markers).

◉Desktop Software: Clinic-grade acquisition/processing; study portals.

◉Digital Platforms: Device-agnostic orchestration, enrollment, consent.

◉Data Integration Systems (fastest growth)

◉Interoperability: Normalization across device types and EHR schemas.

◉Identity/Consent: Governance, privacy controls, auditability.

◉Analytics Pipelines: Feature stores, model serving, monitoring, drift handling.

◉Clinician Interfaces: Alerting, summaries, and shared decision support.

By Clinical Practice

◉Diagnostic (2024 leader): Front-door use for detection/triage; accelerates specialist referral.

◉Monitoring (fastest-growing): Continuous, remote disease status; exacerbation prediction.

◉Predictive & Prognostic: Risk scoring for outcomes/events; therapy planning.

◉Other (Safety/PK-PD/Response/Susceptibility): On-treatment safety (e.g., CRS), exposure-response mappings, and population susceptibility signals.

By End-Use

◉Healthcare Companies (largest): Drug development, endpoint strategy, decentralized trials.

◉Healthcare Providers: RPM programs, virtual wards, perioperative/rehab tracking.

◉Payers (fastest growth): Prior authorization optimization, outcome-based reimbursement.

◉Others (Patients, Caregivers): Self-management insights, caregiver dashboards.

By Region

◉North America / Europe / Asia-Pacific / Latin America / MEA (deep drivers detailed above).

Top 5 FAQs

1) What’s the market size and growth outlook?

• USD 5.09B (2025) → USD 32.37B (2034) at 22.74% CAGR; 2024 size USD 4.15B.

2) Which regions lead and which grow fastest?

• North America led with 59% share (2024); Asia-Pacific is the fastest-growing.

3) Which components are most important?

• Data collection tools dominated in 2024; data integration systems show fastest future growth.

4) Who are the primary end-users and who’s accelerating?

• Healthcare companies (largest share, 2024). Payers growing fastest.

5) What trends and investments validate momentum?

• DANNCE.AI $2.6M (Nov 2024), Quibim $50M Series A (Nov 2024), Biofourmis oncology deals (Sep 2024), Roche-Lunit integration (Sep 2024), electronRx purpleDx (Jan 2025).

Access our exclusive, data-rich dashboard dedicated to the healthcare market – built specifically for decision-makers, strategists, and industry leaders. The dashboard features comprehensive statistical data, segment-wise market breakdowns, regional performance shares, detailed company profiles, annual updates, and much more. From market sizing to competitive intelligence, this powerful tool is one-stop solution to your gateway.

Access the Dashboard: https://www.towardshealthcare.com/access-dashboard

Immediate Delivery Available | Buy This Premium Research @ https://www.towardshealthcare.com/price/5434

Become a valued research partner with us – https://www.towardshealthcare.com/schedule-meeting

You can place an order or ask any questions, please feel free to contact us at [email protected]

Europe Region – +44 778 256 0738

North America Region – +1 8044 4193 44

Web: https://www.towardshealthcare.com

Find us on social platforms: LinkedIn | Twitter | Instagram | Medium | Pinterest