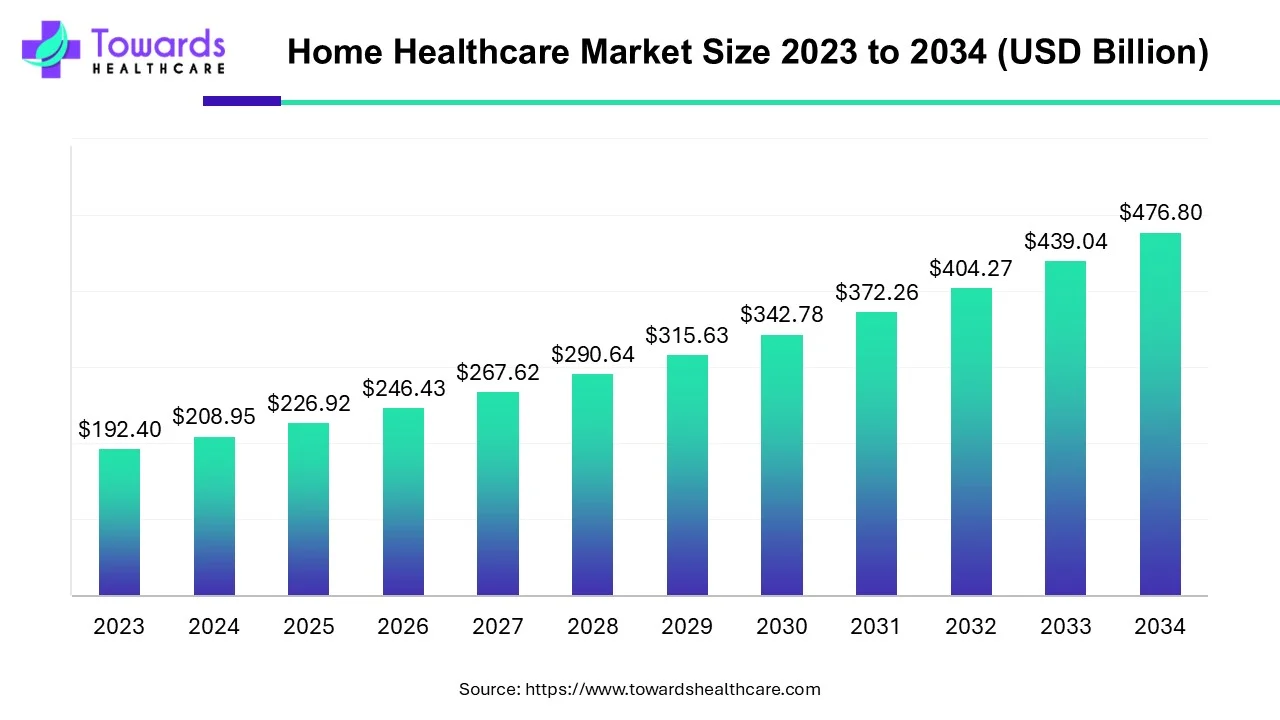

The global home healthcare market, valued at USD 208.95 billion in 2024, is projected to reach USD 476.80 billion by 2034, expanding at a CAGR of 8.6% (2025–2034), driven by aging populations, rising chronic diseases, and rapid adoption of remote monitoring & telehealth technologies.

Download the free sample and get the complete insights and forecasts report on this market @ https://www.towardshealthcare.com/download-sample/5110

Market Size

◉2023 – USD 192.82 billion (baseline year).

◉2024 – USD 208.95 billion, with strong demand in monitoring devices.

◉2025 – USD 226.92 billion, marking the start of CAGR trajectory (8.6%).

◉2026–2030 – Market steadily expands with diabetes & mobility disorders driving uptake; diagnostics & monitoring devices alone exceed USD 109.35 billion by 2030.

◉2034 – Market doubles from 2025 to USD 476.80 billion, supported by home-based chronic care (diabetes 32% share in 2023) and North America’s leadership (44% regional share in 2023).

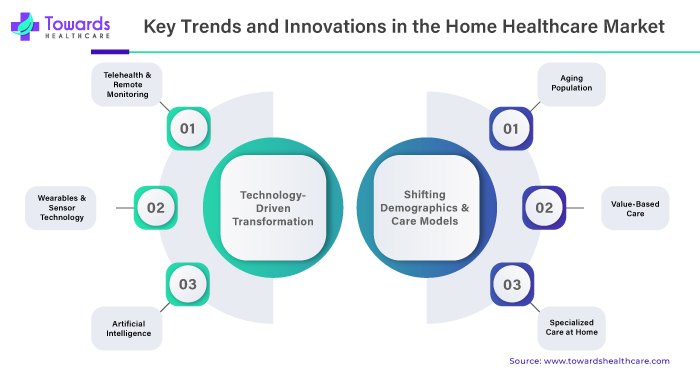

Market Trends

Aging Population Surge

◉By 2045, 783M people globally will have diabetes (IDF).

◉28.7% of U.S. adults aged 65+ had diabetes in 2021, boosting need for in-home management.

◉Cancer & mobility disorders rise with age, fueling physiotherapy & assistive device demand.

Technology Advancements

◉Telehealth & remote monitoring becoming mainstream.

◉FDA-cleared CardioTag wearable (2025) captures ECG, SCG, and PPG simultaneously.

◉AI-driven predictive monitoring—BD hemodynamic platform (2025) prevents complications.

Rise of At-home Diagnostics

◉Geneoscopy ColoSense (2025)—FDA-supported at-home colorectal screening.

◉Ayati Devices (India, 2025)—portable tools for early diabetic neuropathy detection.

Funding & Partnerships

◉Geneoscopy secured USD 105M Series C (2025).

◉NEC X investment in GPx (2024)—chronic disease monitoring startup.

Caregiver & Patient Education Gap

◉Limited awareness of home-based services hampers adoption.

◉Expansion in caregiver training & tele-education platforms expected.

Role & Impact of AI in Home Healthcare

Predictive Analytics & Early Intervention

◉AI models (e.g., Verily, CarePredict) anticipate risk of falls, glucose spikes, or cardiac stress.

◉Enables preventive treatment, reducing ER visits.

Smart Monitoring Devices

◉AI-integrated wearables track multiple vitals (ECG, SpO2, BP).

◉Enables real-time alerting for chronic disease patients.

Personalized Care Planning

◉AI analyzes lifestyle & health history to tailor rehab or diabetes management plans.

Telehealth Enhancement

◉AI chatbots & diagnostic assistants bridge gaps in rural/underserved areas.

◉Reduces physician workload, enabling scalable home care.

Data-Driven Resource Allocation

◉Predicts which patients need intensive vs. light care, optimizing caregiver deployment.

Drug Adherence Monitoring

◉AI-powered smart pillboxes track and alert medication compliance.