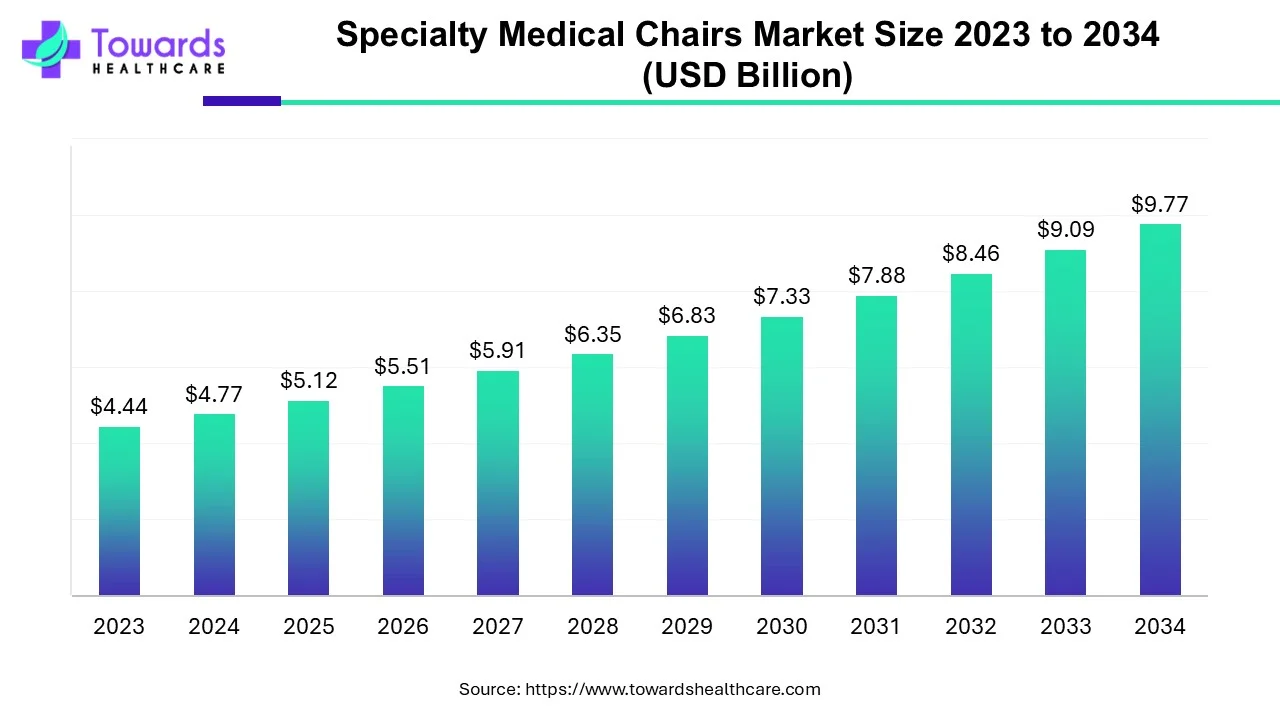

The global specialty medical chairs market was valued at USD 5.12 billion in 2025 (USD 4.77B in 2024) and is projected to reach USD 9.77 billion by 2034 at a CAGR of 7.43% (2025–2034), driven by an aging population, rising chronic disease burden, adoption of advanced/automated chair solutions, and expanding use across hospitals, clinics and rehabilitation facilities.

Download this Free Sample Now and Get the Complete Report and Insights of this Market Easily @ https://www.towardshealthcare.com/download-sample/5480

Market size

Historical base and near-term level (2024–2025):

●2024 market size: USD 4.77 billion (reported).

●2025 market size: USD 5.12 billion — ~7.3% year-over-year increase implied by those two data points.

Forecast horizon and terminal value:

●Projected 2034 market size: USD 9.77 billion.

Compound growth:

●CAGR 2025–2034 = 7.43% — implies the market roughly doubles over the decade (5.12 → 9.77).

Value growth drivers (monetary lens):

●Increased per-unit ASPs (average selling prices) for advanced/automated chairs (high-end models priced in the EUR 4,000–8,000 band).

●Expansion of addressable volume due to aging population and greater adoption in clinics and home care.

Addressable market dynamics:

●Large hospitals and clinic procurements dominate current spend (hospitals largest share in 2024), but faster growth in clinics and outpatient/ambulatory settings increases future addressable spend.

Price vs. volume tradeoff:

●High-end automated chairs drive revenue per unit; affordability/awareness remain constraints in many emerging markets, moderating unit growth but supporting value growth via premium products.

Capital expenditure / funding impact:

●Government health capital increases (e.g., India’s Union Budget allocation, UK capital spending, Newfoundland investments) expand procurement budgets and positively affect market value.

Replacement and aftermarket revenue:

●Maintenance, service contracts and retrofits for high-technology chairs contribute recurring revenue streams (serviceable market beyond new unit sales).

Market concentration (by revenue):

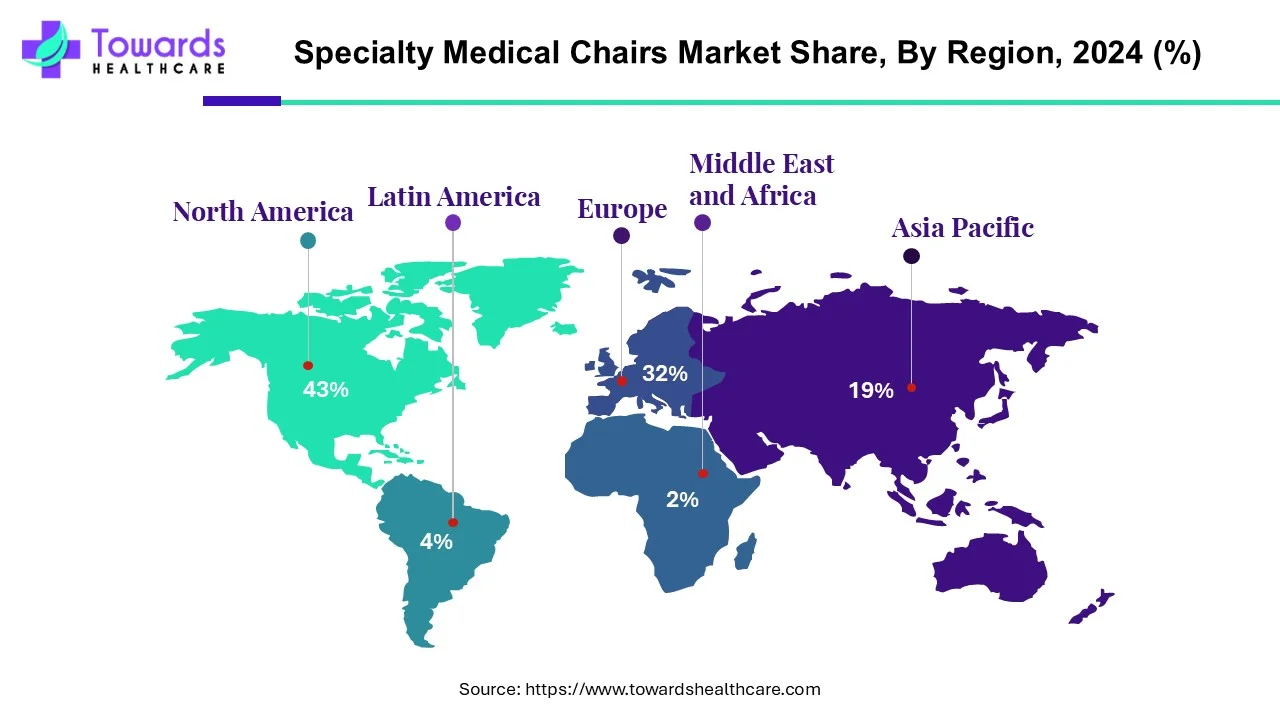

●North America accounted for ~43% share in 2024 — large single-region concentration that influences global revenue distribution.

Long-term upside / downside sensitivity:

●Upside: faster adoption of AI/automation, home care adoption, and medical tourism growth.

●Downside: price resistance, reimbursement limits, and substitution by lower-cost alternatives (stretchers, standard exam chairs).

Market Trends

Aging population as a structural tailwind

●Global seniors are expanding (WHO projections cited): rising need for geriatric, bariatric and rehabilitation chairs; drives both volume and specialized product launches.

Rising chronic disease burden

●Higher prevalence of chronic conditions (cardiovascular, diabetes, cancer) increases long-term demand for dialysis chairs, cardiac chairs, blood-drawing chairs and rehab seating.

Shift toward outpatient & clinic care

●Growth of clinics and ambulatory care centers is shifting procurement away from hospitals only; clinics projected to be fastest-growing end-use segment.

Technological sophistication and digitization

●Integration of digital delivery systems (e.g., A-dec 500 Pro / 300 Pro dental systems) and development of digitally integrated chairs increases product differentiation.

AI/automation & smart chair features

●Movement toward automated positioning, sensors for pressure-care, and predictive maintenance (detailed AI impacts later).

Product specialization and niche chairs

●Expansion of chairs designed for specific specialties: ophthalmic, ENT, mammography, birthing — creating narrower product lines with higher ASPs.

Government funding and healthcare capital programs

●Increased capital expenditure (India Rupees 99,858 crore; UK health capital £13.6B; Newfoundland $40M) frees hospital/clinic budgets to buy advanced chairs.

Consolidation and strategic partnerships

●M&A and distribution deals (e.g., Nakanishi acquiring DCI International; Infinium Medical teaming with Lemi MD) strengthen company footprints and product availability.

Focus on patient comfort and recovery metrics

●New products (Vivid. Care HiBack bedside chair) designed to improve pressure care and reduce recovery/discharge times — procurement tied to clinical outcomes.

Regional growth divergence

●North America leads (43% share), Asia-Pacific shows fastest regional expansion prospects due to rising healthcare spend and large populations.

Investment into distribution & education

●Investments by private equity/strategic investors (Foresight → DP Medical Systems) to expand product lines and market reach.

Price pressure vs. premiumization

●Tension between cost-sensitive procurement (esp. in emerging markets) and demand for premium, feature-rich chairs in developed markets.

AI impact

Automated posture & positioning control

●AI uses sensor inputs (load, body contours) to auto-adjust chair geometry for optimal procedural access and patient comfort.

●Benefits: reduces manual handling tasks, shortens setup time, improves procedure ergonomics.

Personalized patient profiles & presets

●ML models learn patient preferences/clinical needs and recall saved presets (e.g., recline angles, footrest position) per patient or procedure type.

●Benefits: consistent positioning for repeat treatments, faster turnarounds, improved patient experience.

Real-time pressure ulcer / tissue-viability prevention

●Integrated pressure sensors + AI infer high-risk zones and implement micro-adjustments or alerts to nursing staff.

●Benefits: reduces pressure injuries, shorter inpatient stays, measurable clinical outcomes for procurement justification.

Predictive maintenance & uptime optimization

●Telemetry data (actuator cycles, motor current draw) fed to ML models predicts part failures before they occur.

●Benefits: schedule preventive maintenance, reduce downtime, lower lifecycle cost.

Smart infection-control workflows

●AI monitors usage patterns and suggests optimal cleaning cycles; can notify cleaning staff after high-risk procedures.

●Benefits: improves hygiene compliance, helps infection control teams quantify risk.

Adaptive assistance for transfers and handling

●AI coordinates motorized tilt/slide and integrates with lifting devices to assist safe transfers for bariatric/disabled patients.

●Benefits: reduces caregiver injuries and need for additional staff during transfers.

Clinical decision support & integration

●Chair sensors (position, vitals if present) send context to EHR / perioperative systems — AI recommends positioning based on procedure type or clinician preferences.

●Benefits: tighter EHR integration and audit trails for compliance and billing.

Procedure analytics and workflow optimization

●Aggregated chair usage data analyzed to identify bottlenecks (setup time, idle time) and suggest staffing or layout changes.

●Benefits: increases throughput, supports ROI case for new chairs.

Assistive robotics & haptic feedback

●AI coordinates small robotic actuators for fine micro-positioning during delicate eye/dental procedures; provides haptic cues to operators.

●Benefits: enhances precision for ophthalmic/dental interventions.

Manufacturing optimization & customization at scale

●AI optimizes production lines for configurable chairs, enabling mass customization (color, module, pressure ratings) without prohibitive cost.

●Benefits: faster time-to-market of new models, improved margins on bespoke chairs.

Regional Insights

A. North America — (Market leader; 43% share in 2024)

Drivers

●Aging population and favorable reimbursement for durable medical equipment.

●High hospital capital budgets and large network of outpatient centers.

Market characteristics

●Premiumization: high acceptance of advanced automated chairs and digital delivery systems.

●Strong distribution channels and after-sales service networks.

Challenges

●Intense competition on features and quality; regulatory compliance (medical device standards) raises development cost.

Opportunities

●Integration with EHRs, AI feature adoption, and retrofits for existing fleets.

B. Asia-Pacific — (High growth potential)

Drivers

●Large, aging populations coupled with rising healthcare spending.

●Growth of private hospitals, medical tourism, and home health services.

Market characteristics

●Price sensitivity in many markets but increasing appetite for mid- and high-tier solutions in China, India, Korea.

Challenges

●Fragmented distribution, variable reimbursement and limited service infrastructure in rural areas.

Opportunities

●Affordable automation and financing models; localized manufacturing to reduce costs.

C. Europe

Drivers

●Well-established healthcare systems, high outpatient procedure volumes, emphasis on patient safety and ergonomics.

Market characteristics

●Strong regulation and standards; R&D focus on clinical outcomes (pressure care, infection control).

Opportunities

●Government funding for hospital upgrades and strong adoption of advanced chairs in developed markets (Germany, France, UK).

D. Latin America

Drivers

●Growing geriatric cohorts, expanding private healthcare and medical tourism.

Challenges

●Price sensitivity and uneven distribution of advanced facilities.

Opportunities

●Local partnerships and selective deployment in major urban hospitals and private chains.

E. Middle East & Africa (MEA)

Drivers

●Investments in healthcare infrastructure by governments and private investors.

Challenges

●Variability in regulatory environments and service networks.

Opportunities

●High-end installations in GCC nations and targeted rollouts with strong service contracts.

Market dynamics

Driver — Demographic tailwinds

●Aging population and rising chronic disease prevalence increase long-term demand for rehabilitation, geriatric and bariatric chairs.

Driver — Technological advancement

●Development of AI-enabled, ergonomically advanced and digitally integrated chairs supports premiumization and clinical benefits.

Driver — Shift to outpatient care

●Rise in clinics and ambulatory surgery centers expands the addressable market outside hospitals.

Restraint — High product cost

●Advanced chairs often range EUR 4,000–8,000, limiting adoption in cost-sensitive regions and smaller clinics.

Restraint — Awareness & training

●Limited clinician/purchaser awareness of clinical value and the need for staff training impede adoption.

Restraint — Maintenance & service burden

●Ongoing maintenance costs and need for skilled service networks increase total cost of ownership and deter some buyers.

Opportunity — Home healthcare and electric mobility integration

●Growing acceptance of electric wheelchairs and home care devices opens adjacent markets and bundled solutions.

Opportunity — AI & IoT as differentiators

●AI features and predictive maintenance reduce lifecycle cost and create recurring software/service revenue streams.

Opportunity — Government funding

●Increased health capital spending in countries such as India, UK and regional infrastructure investments unlock procurement budgets for advanced chairs.

Competitive dynamic

●Market features both established OEMs (dental and clinical incumbents) and specialist seating companies; partnerships and distribution deals (Infinium/Lemi MD; investment in DP Medical Systems) accelerate market entry for niche players.

Top 10 companies

A-dec, Inc.

Product highlights: Dental chairs and digitally integrated delivery systems (A-dec 500 Pro, A-dec 300 Pro).

Overview: Longstanding dental equipment OEM with significant North American presence.

Strengths: Strong dental focus, integrated digital delivery platforms, proven clinical adoption and brand recognition.

ActiveAid, Inc.

Product highlights: (Specialist seating / aids) — products aimed at mobility and patient handling.

Overview: Specialist in assistive devices and seating solutions.

Strengths: Niche expertise in patient aids, targeted product portfolio for mobility & comfort.

DentalEZ, Inc.

Product highlights: Dental chairs, treatment units and dental delivery systems.

Overview: Dental equipment manufacturer serving clinics and dental chains.

Strengths: Focused dental solutions, established service and distribution channels to dental practices.

Fresenius Medical Care AG & Co. KGaA

Product highlights: Dialysis chairs and related renal care seating solutions (company known for dialysis equipment).

Overview: Global leader in renal care with broad healthcare device presence.

Strengths: Strong clinical relationships in dialysis centers, scale in manufacturing and service provision.

Topcon Corp.

Product highlights: Ophthalmic chairs and diagnostic integration (Topcon is a leader in ophthalmic equipment).

Overview: Established ophthalmic and diagnostic instrument maker.

Strengths: Clinical integration in eye care workflows, global distribution to ophthalmic clinics.

Midmark Corp.

Product highlights: Exam chairs, procedure chairs and integrated treatment equipment.

Overview: Healthcare equipment and medical furniture OEM with training/education initiatives (e.g., WCOMP collaboration).

Strengths: Manufacturing expertise, partnerships with education programs, reputation for durable clinic equipment.

Danaher (KaVo Dental GmbH)

Product highlights: Dental chairs and instruments via KaVo dental unit.

Overview: Large diversified medtech conglomerate with dental equipment capabilities.

Strengths: R&D capacity, broad service network and cross-selling opportunities across Danaher portfolio.

Dentsply Sirona

Product highlights: Dental chairs, dental units and integrated treatment systems.

Overview: Major dental OEM with wide product range and global market penetration.

Strengths: Leading brand in dentistry, strong aftermarket services and digital dentistry roadmap.

Planmeca Oy

Product highlights: Dental units and ergonomic treatment chairs (Planmeca is a premium dental OEM).

Overview: Finland-based dental technology leader known for equipment innovation.

Strengths: High-end product design, strong R&D and integration in dental CAD/CAM workflows.

Rahab Seating Systems Inc. / Hill Laboratories Company

Product highlights: Specialty seating solutions (bariatric, geriatric, rehab).

Overview: Specialist seating manufacturers focusing on comfort, pressure care and bespoke solutions.

Strengths: Deep domain expertise in ergonomics, customization capabilities and niche clinical focus.

Latest announcement

Vivid. Care — HiBack Bedside Chair (Feb 2025)

What: Launch of the HiBack Bedside Chair designed to solve endemic issues with hospital ward seating (effortless height adjustment, superior pressure care, patient ergonomics).

Why it matters: Addresses a clinically measurable problem (pressure issues delaying recovery/discharge); direct feedback-driven development (ward managers, moving & handling experts, Tissue Viability Nurses).

Implication for buyers: Potential to reduce pressure-related complications and shorten length-of-stay metrics — strengthens procurement case beyond comfort alone.

Strategic angle: Demonstrates how clinician engagement in R&D can yield product features that influence adoption in acute care.

RNZAF delivery to Samoa (March 2025) — five specialized chairs delivered for chemotherapy/dialysis: demonstrates humanitarian / regional access role of logistics and partnerships for distributing bulky specialty chairs.

Infinium Medical & Lemi MD (March 4, 2025) — exclusive U.S. distribution for Lemi MD-Series surgical chairs (Dreamed Procedure Chair, Monza Mobile Surgery Chair, Lemi 4 Procedure Table) — strengthens availability of surgical chair choices in U.S. clinical market.

Recent developments

Infinium Medical — exclusive U.S. distribution with Lemi MD (Mar 4, 2025)

Details: Partnership expands surgical chair portfolio in U.S. distribution channels; adds mobile and procedure-specific chairs to market.

Impact: Improves choice for surgical centers, supports adoption of procedure chairs that maximize OR efficiency.

Vivid. Care — HiBack Chair launch (Feb 2025)

Discussed above — outcome: product addresses pressure care and ergonomics in acute wards.

Foresight investment into DP Medical Systems (Aug 2024)

Details: £4.45M investment to expand product launches and growth plans.

Impact: Capital infusion strengthens distribution, enabling new product introductions and market coverage.

Nakanishi Inc. acquisition of DCI International (Aug 2023)

Details: Strengthens Nakanishi’s U.S. presence for dental chair units and instruments.

Impact: Consolidation trend in dental seating and instruments reinforces incumbent strength in dental markets.

A-dec new digital delivery systems (June 2023)

Details: A-dec 500 Pro and 300 Pro for North America — digitally integrated dental chairs/delivery units.

Impact: Example of digital integration trend in dental specialty seating that increases ASP and clinician productivity.

Midmark / WCOMP / Ohio STEM partnership (Mar 4, 2024)

Details: Educational partnership to promote manufacturing careers and highlight healthcare innovation.

Impact: Long-term talent pipeline for manufacturing and R&D; supports local production capabilities.

RNZAF humanitarian delivery (Mar 2025)

Details: Logistics/donation of bulky chairs for Samoa dialysis/chemo patients.

Impact: Highlights role of logistics and cross-sector partnerships in improving access in remote regions.

Segments covered

By Product (major groups + explanation)

Examination chairs

●Use: general diagnostic exams across clinics/hospitals.

●Considerations: adjustability, ease of cleaning, compact footprint.

Birthing chairs

●Use: obstetrics and labor support.

●Considerations: modularity, perineal access, patient comfort and positioning support.

Cardiac chairs

●Use: cardiac diagnostics, recovery, cath labs.

●Considerations: reclining mechanics, integrated monitoring compatibility.

Blood drawing chairs (phlebotomy)

●Use: collection centers, clinics.

●Considerations: patient arm support, stability and infection control surfaces.

Dialysis chairs

●Use: dialysis centers, renal units.

●Considerations: long-duration comfort, recline for vascular access, ease of disinfection.

Mammography chairs

●Use: breast imaging centers.

●Considerations: positioning precision, radiolucent materials where required.

Rehabilitation chairs

●Subtypes: pediatric, bariatric, geriatric.

●Use: therapy, mobility, positioning.

●Considerations: pressure care, weight capacity, transfer assistance.

Treatment chairs (procedure chairs)

●Subtypes: ophthalmic, ENT, dental, other procedure-specific chairs.

●Use: surgeries, outpatient procedures.

●Considerations: specialty attachments, integration with instruments and lighting.

Pediatric chairs

●Use: pediatric therapy and treatment.

●Considerations: size ranges, safety restraints, child-friendly ergonomics.

Bariatric chairs

●Use: patients with higher weight needs; rehab & surgical prep.

●Considerations: reinforced frames, higher weight capacity, safe transfers.

By End-use

●Hospitals — largest share: tend to buy full-featured, durable chairs for inpatient, OR and specialty departments.

●Clinics — fastest growth: demand for compact, cost-effective, specialty chairs for ambulatory procedures.

●Others — includes home care, long-term care facilities, mobile units, and diagnostic centers.

By Region

North America, Asia-Pacific, Europe, Latin America, MEA — each with the drivers and opportunities previously described.

Top 5 FAQs

-

Q: What is the current size and expected growth of the specialty medical chairs market?

A: Valued at USD 5.12 billion in 2025 (USD 4.77B in 2024), projected to reach USD 9.77 billion by 2034 at a CAGR of 7.43% (2025–2034). -

Q: Which region currently dominates the market?

A: North America dominated with approximately 43% share in 2024, led by an aging population, high disposable incomes and advanced healthcare infrastructure. -

Q: Which product and end-use segments are most significant?

A: By product, rehabilitation chairs held a dominant presence in 2024; treatment chairs are expected to grow fastest. By end-use, hospitals held the largest share, while clinics are the fastest-growing end-use segment. -

Q: What are the key drivers and restraints in the market?

A: Drivers: aging population, chronic disease prevalence, tech innovation and government health capital spending. Restraint: high cost of advanced chairs, maintenance burden and limited awareness in some markets. -

Q: How is AI expected to affect this market?

A: AI is set to transform the market across positioning automation, pressure-care prevention, predictive maintenance, personalized presets, infection-control workflows, integration with EHRs, and manufacturing optimization — creating product differentiation and recurring software/service revenue streams.

Access our exclusive, data-rich dashboard dedicated to the healthcare market – built specifically for decision-makers, strategists, and industry leaders. The dashboard features comprehensive statistical data, segment-wise market breakdowns, regional performance shares, detailed company profiles, annual updates, and much more. From market sizing to competitive intelligence, this powerful tool is one-stop solution to your gateway.

Access the Dashboard: https://www.towardshealthcare.com/access-dashboard

Immediate Delivery Available | Buy This Premium Research @ https://www.towardshealthcare.com/price/5480

Become a valued research partner with us – https://www.towardshealthcare.com/schedule-meeting

You can place an order or ask any questions, please feel free to contact us at sales@towardshealthcare.com

Powering Healthcare Leaders with Real-Time Insights: https://www.towardshealthcare.com/healthcare-intelligence-platform

Europe Region – +44 778 256 0738

North America Region – +1 8044 4193 44

APAC Region: +91 9356 9282 04

Web: https://www.towardshealthcare.com

Find us on social platforms: LinkedIn | Twitter | Instagram | Medium | Pinterest