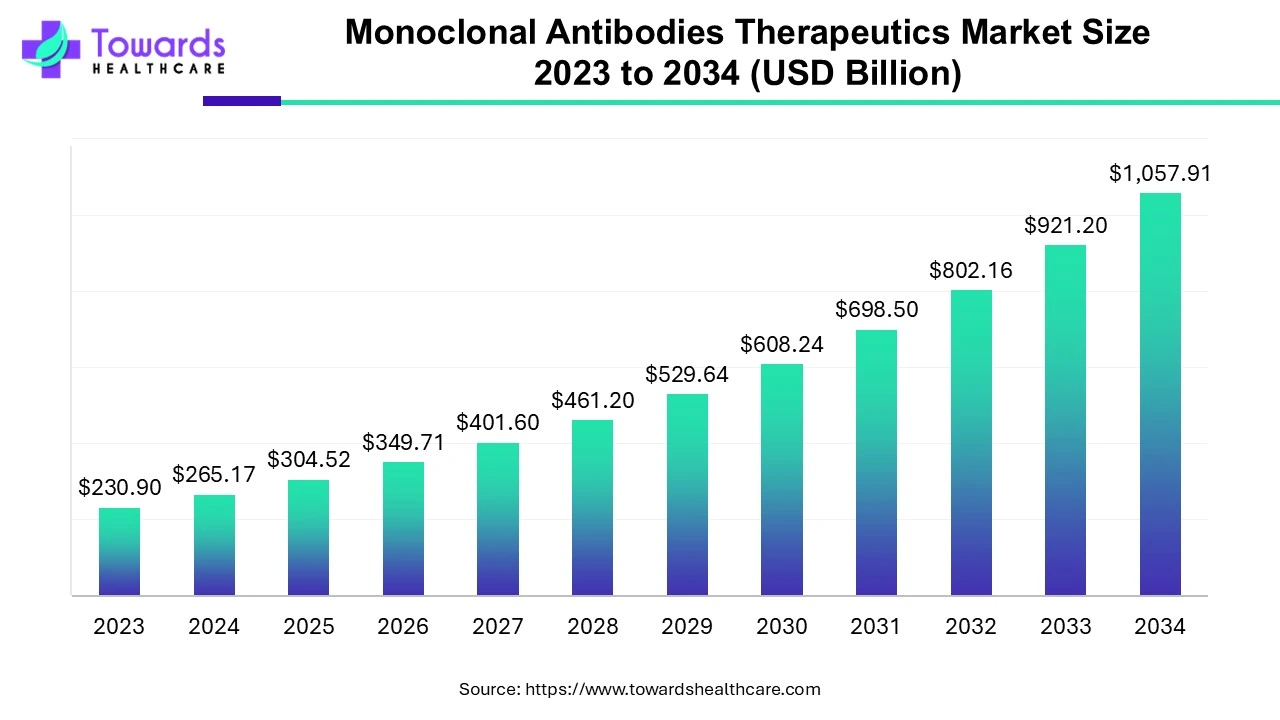

The global monoclonal antibodies therapeutics market was valued at USD 265.17 billion in 2024, grew to USD 304.52 billion in 2025, and is projected to reach USD 1,057.91 billion by 2034, expanding at a CAGR of 14.84% (2025–2034), driven by oncology, autoimmune, and infectious disease applications.

Download the free sample and get the complete insights and forecasts report on this market @ https://www.towardshealthcare.com/download-sample/5490

Market Size

2023 Baseline

➣Market stood slightly below USD 265 billion.

➣Growth trajectory accelerated due to approvals in oncology and autoimmune diseases.

2024 (USD 265.17 Billion)

➣North America dominated the market due to advanced R&D, high adoption of immunotherapies, and large cancer patient pool.

2025 (USD 304.52 Billion)

➣Growth fueled by rapid expansion of humanized and human mAbs in immunotherapy.

➣Increased use of mAbs in diagnostics + therapeutics.

2030 Milestone (≈USD 630 Billion, projected)

➣Doubling of the market within 5 years, largely through new cancer immunotherapies and biosimilars entry.

2034 Forecast (USD 1,057.91 Billion)

➣Market expected to quadruple from 2024 levels.

➣Oncology remains dominant, while autoimmune diseases + online pharmacies rise fastest.

Market Trends

Shift from Small Molecules → mAbs

➣Traditional pharmaceuticals relied on small molecules.

➣mAbs are now a core therapy class due to target selectivity and lower toxicity.

Cancer Immunotherapy Growth

➣In 2024, cancer held the largest application share.

➣Expected to continue as a backbone therapy along with chemo, radiation, and surgery.

Rise of Autoimmune Indications

➣Fastest CAGR application segment.

➣Over 250 mAbs currently in trials for RA, lupus, MS, and other autoimmune conditions.

Hospital Pharmacy Dominance

➣Hospital pharmacies led in 2024 due to mAbs’ complex administration and storage needs.

Online Pharmacy Surge

➣Expected fastest CAGR in distribution, driven by accessibility, privacy, and convenience.

Pipeline Expansion

➣Dozens of companies are expanding clinical programs across oncology, immunology, and rare diseases.

FDA Regulatory Reform (2025)

➣Announced phase-out of animal testing for mAbs, reducing R&D cost and accelerating drug approvals.

Funding Momentum

➣Example: Timberlyne Therapeutics closed $180M Series A (2025) for autoimmune therapies.

➣Arxx & Oxitope raised €75M (2024) for immune disorder pipeline.

Regional Research Boom

➣North America leads with cancer R&D funding (925 grants worth $583M in 2024).

➣Asia Pacific accelerates due to clinical trials in China and India.

Biotech Consolidation

➣Mergers & acquisitions (e.g., Novartis acquiring Anthos Therapeutics) expanding antibody portfolios.

AI Impact / Role in Monoclonal Antibodies Market

1 Computational Antibody Design

Role: AI enables in-silico modeling of antibody–antigen interactions, predicting binding affinities before lab testing.

Impact:

➣Reduces dependency on trial-and-error wet lab experiments.

➣Speeds up early discovery from years to a few months.

Example: AI platforms (e.g., DeepMind’s AlphaFold, Insilico Medicine) predict 3D protein folding, accelerating hit-to-lead processes.

Future: AI-driven de novo antibody design will dominate early-stage R&D by 2030.

2. Optimization of Antibody Specificity

Role: ML algorithms analyze massive antibody sequence libraries to optimize specificity and minimize cross-reactivity.

Impact:

➣Lowers off-target toxicity → safer therapeutics.

➣Enables next-gen bispecific and trispecific antibodies targeting multiple epitopes with high precision.

Future: Could become a quality-by-design (QbD) standard, enforced by regulators like FDA and EMA.

3. Predictive Developability Assessment

Role: AI predicts biophysical properties such as solubility, stability, and aggregation propensity.

Impact:

➣Reduces late-stage clinical trial failures (~30% of biologics fail due to poor developability).

➣Improves manufacturability by selecting the most stable candidates early.

Example: Companies like Schrödinger use AI-powered simulations to screen molecules before scale-up.

4. Accelerated Clinical Trial Design

Role: AI-driven models simulate patient stratification, biomarker-based inclusion, and virtual trial arms.

Impact:

➣Shortens trial timelines by up to 30–40%.

➣Improves recruitment by predicting best-fit patient subgroups.

Example: Novartis & Microsoft collaboration uses AI for adaptive clinical trials.

Future: Virtual control arms could replace costly comparator groups in oncology trials.

5. Target Discovery

Role: Deep learning scans genomic, proteomic, and clinical datasets to identify novel disease-associated antigens.

Impact:

➣Expands therapeutic scope beyond oncology and autoimmunity to rare and infectious diseases.

➣Enables precision mAbs tailored to underexplored targets.

Example: AI platforms like BenevolentAI and Exscientia are pioneering new target discoveries.

6. Manufacturing Automation

Role: AI-powered bioprocessing integrates with bioreactor monitoring, cell culture optimization, and predictive maintenance.

Impact:

➣Boosts yields by 10–15%.

➣Cuts batch failures, ensuring consistent product quality.

Example: AI-enabled “digital twins” of manufacturing plants (Siemens, GE Healthcare) are being adopted by biologics manufacturers.

Future: Autonomous “lights-out” biologics factories by 2035.

7. Personalized mAb Therapy

Role: AI integrates biomarker, genomic, and proteomic data to design patient-specific antibody regimens.

Impact:

➣Especially powerful in oncology, where tumor mutational burden and PD-L1 expression vary across patients.

➣Enables precision dosing and adaptive treatment monitoring.

Example: Roche & Flatiron Health using AI to personalize checkpoint inhibitor treatments.

Future: Could integrate with AI-powered digital twins of patients for fully personalized therapy.

8. Drug Repurposing

Role: AI scans existing drug/mAb databases to identify new therapeutic indications.

Impact:

➣Speeds up development since repurposed drugs already have safety data.

➣Expands market lifecycle of blockbuster mAbs (e.g., Rituximab, initially for lymphoma → now in autoimmune diseases).

Example: AI identified Tocilizumab (IL-6 mAb) as a COVID-19 therapy in 2020.

Future: Routine repurposing pipelines will extend drug lifespans by 5–10 years.

9. Cost Reduction in R&D

Role: AI eliminates inefficient experimental iterations and streamlines candidate selection.

Impact:

➣Cuts drug discovery costs by 30–40%.

➣Shortens design cycle from 5–7 years to 12–24 months.

Example: Insilico Medicine discovered a novel fibrosis drug in under 18 months using AI.

Future: AI-first discovery could save the industry tens of billions annually.

10. AI-Enhanced Diagnostics

Role: AI combines with antibody-based diagnostics (e.g., ELISA, lateral flow tests) for early disease detection.

Impact:

➣Boosts sensitivity and specificity, allowing earlier therapeutic intervention.

➣Expands companion diagnostics → ensuring right mAb for right patient.

Example: AI-powered pathology integrated with PD-L1 IHC tests for checkpoint inhibitors.

Future: AI-mAb integrated diagnostics will become standard-of-care in oncology and autoimmune therapy selection.

Regional Insights

North America (Leading Region)

Strengths:

➣Advanced healthcare ecosystem with integrated hospital networks and specialized cancer centers (e.g., MD Anderson, Mayo Clinic).

➣FDA’s evolving regulatory flexibility for accelerated approvals of oncology and autoimmune mAbs, including breakthrough therapy and fast-track designations.

➣Strong biotech ecosystem in hubs like Boston, San Francisco, and San Diego, driving innovation.

➣Large cancer burden: ~2 million new cases and 611,000 cancer-related deaths projected in the US for 2024.

Key Drivers:

➣Government Funding: NIH awarded 925 oncology and autoimmune-related grants worth $583M in 2024, with additional allocations under the Cancer Moonshot program.

➣Pharma Leadership: Pfizer, Amgen, and Merck dominate oncology and immunotherapy R&D.

➣Adoption of mAbs in Diagnostics: Widespread use in companion diagnostics, imaging, and early cancer detection.

Outlook:

➣North America will retain its dominance due to sustained oncology R&D pipelines, increasing autoimmune trials, and growing adoption of biosimilars.

➣By 2034, the region could capture >40% of global revenues, driven by payer reimbursement support and high patient access.

Europe (Second-Largest Market)

Strengths:

➣Strong laboratory infrastructure, anchored by EuroMAbNet, enabling collaborative antibody R&D.

➣High rare disease prevalence – ~30 million EU patients rely on targeted biologics.

➣Cross-border healthcare frameworks supporting patient access to mAb therapies.

Country Highlights:

➣Germany: 4M rare disease patients, >30 dedicated rare illness centers, heavy investment in precision oncology.

➣UK: £118M allocated in 2024 for cancer research & development, with strong academic–industry collaborations (Oxford, Cambridge hubs).

➣France: Expanding immunology research, particularly in allergy and autoimmune disorders.

Outlook:

➣Europe is an innovation hub for recombinant and engineered antibodies, with a focus on bispecifics, trispecifics, and ADCs (antibody–drug conjugates).

➣EMA’s evolving regulatory flexibility may speed approval of biosimilars and next-gen immunotherapies, widening patient access.

Asia Pacific (Fastest-Growing Market)

Strengths:

➣Large and diverse patient pool, particularly in oncology and autoimmune disorders.

➣Growing middle-class population and disposable income driving demand for advanced biologics.

➣Rising government funding for biotechnology research and clinical trials.

Country Highlights:

➣China: 31.5–35.5M people with autoimmune disorders, high prevalence of rheumatoid arthritis and thyroid diseases. Strong pipeline supported by domestic players like Innovent Biologics.

➣India: ~80M rare disease cases, backed by the National Fund for Rare Diseases (₹974 crore for 2024–26) to improve patient access.

Japan & South Korea: Leaders in biosimilars and precision oncology therapies.

Outlook:

➣Asia Pacific is emerging as the preferred hub for clinical trials and global R&D collaborations due to cost advantages, diverse patient genetics, and rapid regulatory evolution.

➣Expected to register the fastest CAGR (~10–12%) through 2034, outpacing Europe and North America.

Middle East & Africa

Strengths:

➣Expanding biotech infrastructure in GCC countries.

➣Rising adoption of advanced therapies in UAE, Saudi Arabia, and South Africa.

Country Highlights:

➣UAE: Approved LEQEMBI (lecanemab) for Alzheimer’s in 2024, signaling openness to innovative biologics.

➣South Africa: Hosting 26 ongoing mAb trials in 2025, making it a clinical hub for Sub-Saharan Africa.

Outlook:

➣Gradual shift toward personalized medicines and oncology-focused trials, supported by government initiatives and international partnerships.

Latin America

Strengths:

➣Expanding oncology demand in Brazil, Mexico, and Argentina.

➣Increasing government spending on universal healthcare and biologics adoption.

Outlook:

➣Market growth is moderate but steady, with biosimilars serving as an affordable entry point.

➣Rising partnerships with multinational pharma for distribution and co-development.

Market Dynamics

Drivers

➣Targeted Therapy Demand: mAbs dominate oncology and autoimmune treatments due to precision and reduced side effects.

➣Diagnostics Expansion: Growing use of mAbs in imaging, biomarker assays, and personalized medicine.

➣Government Incentives: FDA reforms, EU rare disease frameworks, and China’s fast-track approvals boost innovation.

Restraints

➣High Development Cost: Complex clinical trials and manufacturing require billions in investment.

➣Entry Barriers: Smaller biotech firms face funding, IP, and regulatory hurdles.

➣Cold Chain Challenges: High dependency on specialized storage and logistics.

Opportunities

➣Expanding Pipeline: >250 ongoing clinical trials globally, including bispecific and trispecific mAbs.

➣Biosimilars Boom: Expiry of patents (e.g., Humira, Avastin) is fueling biosimilar entry.

➣AI-Driven Discovery: Machine learning accelerates drug discovery and target validation, reducing R&D timelines.

Top 10 Companies

Pfizer Inc.

➣Key Products: Rituximab biosimilars, oncology pipeline (breast, lung, hematology).

➣Strengths: Strong global oncology presence across the US, EU, and APAC; vast R&D budget exceeding $11B annually.

➣Strategic Focus: Actively pursuing next-gen bispecific antibodies and ADC (antibody–drug conjugates) partnerships.

➣Pipeline Highlights: Expanding biosimilar portfolio targeting blockbuster biologics (Herceptin, Avastin).

2. Novartis AG

➣Key Products: Cosentyx (IL-17 mAb, autoimmune), Beovu, oncology-focused antibodies.

➣Strengths: One of the largest autoimmune-focused portfolios, with dominance in dermatology and rheumatology.

➣Strategic Move: Acquisition of Anthos Therapeutics (Feb 2025) for abelacimab pipeline (thrombosis, cancer), valued at $925M upfront + milestones.

➣Outlook: Diversifying into cardio-immunology and rare clotting disorders, strengthening leadership in immune-mediated conditions.

3. Roche Holding AG (F. Hoffmann-La Roche Ltd.)

➣Key Products: Herceptin, Avastin, Rituxan, Tecentriq.

➣Strengths: Pioneer in oncology mAbs; maintains largest global biologics market share.

➣Strategic Focus: Expanding into ophthalmology with Vabysmo (launched 2024 in India).

➣Outlook: Continued innovation in bispecific antibodies and ADCs, leveraging diagnostics expertise (Roche Diagnostics).

4. AbbVie Inc.

➣Key Products: Humira (adalimumab), Skyrizi, Rinvoq.

➣Strengths: Historically largest autoimmune revenues globally (>$21B Humira sales pre-biosimilars).

➣Strategic Challenge: Humira biosimilar erosion; shifting focus to Skyrizi and Rinvoq.

➣Outlook: Heavy pipeline in immunology and oncology to sustain revenue growth.

5. Bristol-Myers Squibb (BMS)

➣Key Products: Opdivo (nivolumab), Yervoy (ipilimumab), Abecma (CAR-T).

➣Strengths: Global leader in immuno-oncology checkpoint inhibitors.

➣Strategic Focus: Combination therapies (Opdivo + Yervoy), expansion into hematologic malignancies.

➣Outlook: Long-term dominance in solid tumors and rare cancers expected.

6. Regeneron Pharmaceuticals Inc.

➣Key Products: Dupixent (dupilumab – co-developed with Sanofi), Eylea, oncology assets.

➣Strengths: Fastest-growing immunology portfolio, driven by Dupixent approvals in asthma, dermatitis, and chronic rhinosinusitis.

➣Strategic Focus: Partnering with Sanofi while expanding into oncology (bispecific antibodies).

➣Outlook: Positioned for double-digit growth in autoimmune and ophthalmology segments.

7. AstraZeneca plc

➣Key Products: Imfinzi (durvalumab), Enhertu (ADC in collaboration with Daiichi Sankyo).

➣Strengths: Expanding oncology immunotherapy pipeline, with focus on lung and breast cancers.

➣Strategic Focus: Investing in next-gen ADCs and bispecifics; strong APAC market penetration.

➣Outlook: Expected to outperform in oncology immunotherapy segment through 2034.

8. Sanofi

➣Key Products: Dupilumab (with Regeneron), Sarclisa (multiple myeloma).

➣Strengths: Strong immunology base, growing oncology footprint.

➣Strategic Focus: Diversification into oncology and rare diseases, with multiple partnerships.

➣Outlook: Strengthening immunology pipeline while positioning itself in oncology leadership tier.

9. Eli Lilly and Company

➣Key Products: Mirikizumab (ulcerative colitis), Taltz (psoriasis), oncology mAbs in development.

➣Strengths: Expanding autoimmune research portfolio; strong market penetration in dermatology.

➣Strategic Focus: Investment in neuro-immunology and GI-focused antibodies.

➣Outlook: Long-term growth from autoimmune and rare disease therapy expansion.

10. Merck & Co. (MSD)

➣Key Products: Keytruda (pembrolizumab), one of the best-selling biologics globally (>$24B annual sales 2023–2024).

➣Strengths: Market leader in checkpoint inhibitors, with broad label expansions across cancers.

➣Strategic Focus: Exploring combination immunotherapy regimens and investing in novel modalities.

➣Outlook: Keytruda expected to remain global oncology blockbuster through 2030, despite biosimilar risk post-patent expiry.

Latest Announcements

➣Novartis (Feb 2025): Acquired Anthos Therapeutics (abelacimab pipeline, $925M upfront + milestones).

➣Roche India (Mar 2024): Launched Vabysmo for retinal diseases – debut in ophthalmology.

Recent Developments

➣Sun Pharma (Mar 2025): Acquired Checkpoint Therapeutics for oncology immunotherapies.

➣REGiMMUNE & Kiji (Oct 2024): Merger → regulatory T-cell therapies.

➣Aerovate & Jade Biosciences (Oct 2024): Merger for autoimmune therapies.

➣KBI Biopharma (Sep 2023): Launched SUREmAb platform for efficient mAb R&D.

Segments Covered

By Type

1. Human mAb (Leading, 2024)

➣Market Share: Dominates global mAb sales due to superior safety and efficacy.

➣Therapeutic Areas: Oncology, autoimmune diseases, ophthalmology.

➣Examples: Keytruda (Merck), Dupixent (Regeneron/Sanofi).

Drivers:

➣Low immunogenicity → improved patient tolerance.

➣Broad FDA/EMA approvals across multiple cancers and autoimmune disorders.

➣Increasing payer support due to proven outcomes and survival benefits.

➣Outlook: Expected to remain largest sub-segment through 2034, capturing >60% of market share.

2. Humanized mAb (Fastest Growth)

➣Applications: Rare diseases, immunology, infectious diseases.

➣Examples: Trastuzumab (Herceptin), Bevacizumab (Avastin).

Drivers:

➣Reduced side effects vs. chimeric/murine mAbs.

➣Expanding R&D pipeline (over 120+ ongoing trials).

➣Strong fit for rare and chronic conditions requiring long-term therapy.

Outlook: Projected to grow at CAGR 9–11% (2024–2034); will likely replace chimeric antibodies in standard of care.

3. Chimeric mAb

➣Applications: Early oncology and autoimmune therapies.

➣Examples: Rituximab, Infliximab.

Challenges:

➣Higher immunogenicity → risk of adverse immune reactions.

➣Facing competition from humanized and fully human antibodies.

➣Outlook: Gradual decline in usage; mainly restricted to biosimilars and developing markets where affordability outweighs risk.

4. Murine mAb

➣Applications: Historically important but now limited to research and niche areas.

➣Limitations: High immunogenicity, short half-life, not suitable for chronic therapies.

➣Outlook: Almost entirely phased out in mainstream clinical use; remains relevant for preclinical studies and diagnostics.

By Application

1. Cancer (Dominant, 2024)

➣Market Share: Largest segment, accounts for >60% of global mAb revenues.

➣Therapies: Checkpoint inhibitors (Keytruda, Opdivo), HER2-targeted drugs (Herceptin), bispecifics, ADCs.

Drivers:

➣Rising cancer incidence (20M+ new cases globally in 2024).

➣Integration of immunotherapy in first-line cancer treatment.

➣Expanding companion diagnostics → more personalized therapy approvals.

➣Outlook: Will remain largest market through 2034, with continuous expansion into solid tumors and hematological malignancies.

2. Autoimmune (Fastest CAGR)

➣Therapies: Dupixent, Cosentyx, Skyrizi, Humira (biosimilars).

Drivers:

➣Over 250+ ongoing clinical trials targeting rheumatoid arthritis, psoriasis, ulcerative colitis, and thyroid disorders.

➣Increasing prevalence of autoimmune diseases (400M+ globally).

➣Patient preference for biologics due to long-term symptom relief and reduced hospitalizations.

➣Outlook: Fastest-growing segment (CAGR ~10–12%) driven by new drug launches and wider label expansions.

3. Others (Emerging Applications)

➣Infectious Diseases: COVID-19 mAbs, RSV therapies, HIV research.

➣Ophthalmology: Anti-VEGF mAbs (Vabysmo, Eylea) for retinal disorders.

➣Rare Illnesses: Orphan drug designations boosting niche therapies.

➣Outlook: While smaller, this segment is expanding rapidly due to increased rare disease funding and ophthalmology-focused launches.

By Distribution Channel

1. Hospital Pharmacy (Leading)

➣Market Share: Handles 70% of global mAb volume.

Why Leading?

➣Most mAbs require infusion or cold-chain storage.

➣Specialist monitoring and adverse-event management available only in hospitals.

➣Outlook: Will remain dominant, but growth will slow as self-administered subcutaneous formulations expand.

2. Online Pharmacy (Fastest Growth)

Drivers:

➣Expansion of telemedicine & e-health platforms.

➣Growing adoption of chronic therapy refills online (e.g., Dupixent, Cosentyx).

➣Pandemic-driven consumer shift toward digital healthcare.

➣Outlook: Expected CAGR ~12–14% (2024–2034). Will play a transformative role in patient convenience and long-term therapy adherence.

3. Retail Pharmacy

➣Current Role: Secondary distribution channel.

➣Trend: Increasingly relevant for self-injectable biologics that patients can administer at home.

➣Outlook: Growth expected, but limited compared to online & hospital channels; role will expand in chronic autoimmune therapy refills.

By Region

1. North America (Largest Market)

➣Strengths: Advanced R&D, FDA fast-track approvals, largest cancer patient pool.

➣Outlook: Will remain innovation hub, capturing >40% of revenues by 2034.

2. Asia Pacific (Fastest Growth)

➣Strengths: Huge patient pool, strong government R&D incentives, rapid biosimilar adoption.

Country Highlights:

➣China: Expanding domestic biologics manufacturing.

➣India: National rare disease fund (₹974 crore, 2024–26).

➣Outlook: Fastest CAGR (10–12%), becoming clinical trial hotspot and cost-efficient manufacturing hub.

3. Europe

➣Strengths: EMA rare disease frameworks, strong university-industry collaborations, high orphan drug approvals.

➣Outlook: Strong growth in engineered antibodies, bispecifics, and recombinant formats.

4. Latin America & Middle East & Africa

➣Strengths: Expanding oncology & immunology demand in Brazil, Mexico, UAE, and South Africa.

➣Challenges: Limited access, pricing barriers, reliance on biosimilars.

➣Outlook: Gradual but steady adoption; biosimilars will be key growth driver.

Top 5 FAQs

Q1. What is the projected size of the monoclonal antibodies therapeutics market by 2034?

A1. The market is projected to reach USD 1,057.91 billion by 2034, growing at 14.84% CAGR.

Q2. Which region dominates the market today?

A2. North America held the largest share in 2024, driven by advanced cancer research and R&D investments.

Q3. Which type of mAb is growing the fastest?

A3. Humanized monoclonal antibodies, due to reduced immunogenicity and better efficacy.

Q4. What are the main drivers of this market?

A4. Rising demand for targeted therapies, growing prevalence of cancer and autoimmune diseases, and AI integration in antibody design.

Q5. Who are the leading players in the market?

A5. Major companies include Pfizer, Novartis, Roche, AbbVie, Bristol-Myers Squibb, Regeneron, AstraZeneca, Sanofi, Eli Lilly, and Merck.

Access our exclusive, data-rich dashboard dedicated to the therapeutic area sector – built specifically for decision-makers, strategists, and industry leaders. The dashboard features comprehensive statistical data, segment-wise market breakdowns, regional performance shares, detailed company profiles, annual updates, and much more. From market sizing to competitive intelligence, this powerful tool is one-stop solution to your gateway.

Access the Dashboard: https://www.towardshealthcare.com/access-dashboard

Immediate Delivery Available | Buy This Premium Research @ https://www.towardshealthcare.com/price/5490

Become a valued research partner with us – https://www.towardshealthcare.com/schedule-meeting

You can place an order or ask any questions, please feel free to contact us at [email protected]

Powering Healthcare Leaders with Real-Time Insights: https://www.towardshealthcare.com/healthcare-intelligence-platform

Europe Region – +44 778 256 0738

North America Region – +1 8044 4193 44

APAC Region: +91 9356 9282 04

Web: https://www.towardshealthcare.com

Find us on social platforms: LinkedIn | Twitter | Instagram | Medium | Pinterest