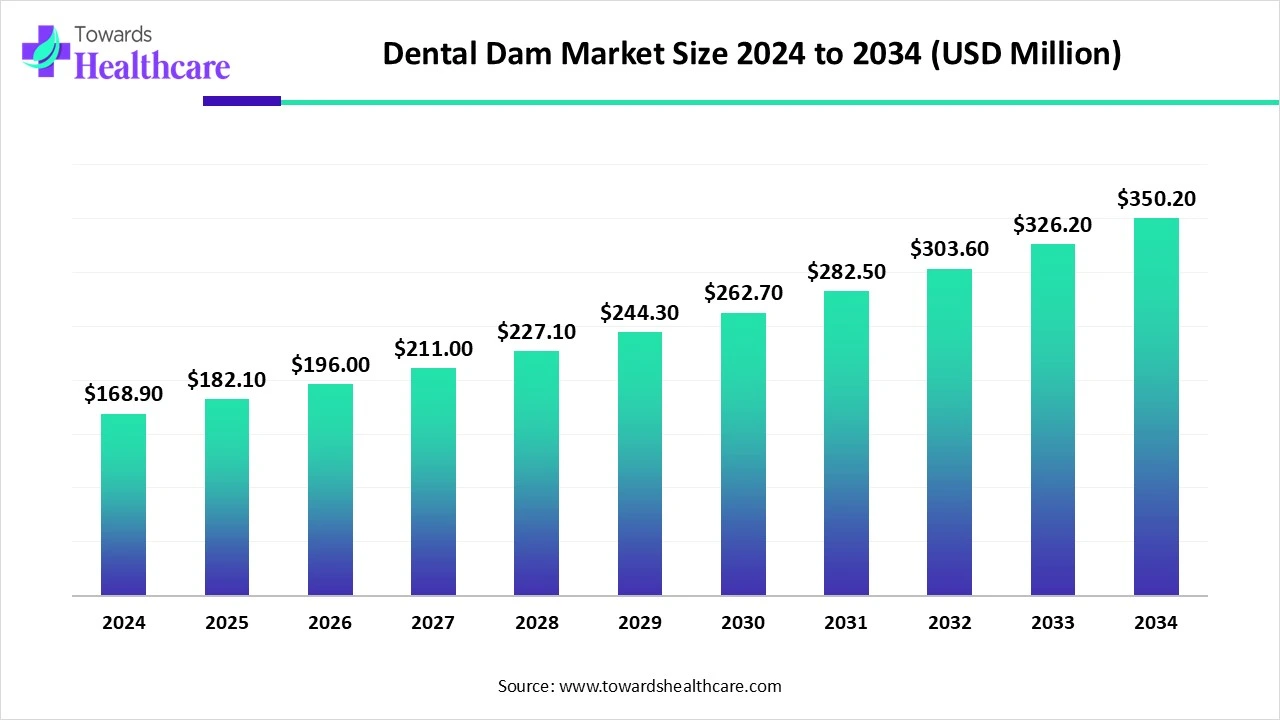

The global dental dam market was valued at USD 168.9 million in 2024, grew to USD 182.1 million in 2025, and is forecast to reach USD 350.2 million by 2034 (CAGR 7.74% for 2025–2034), driven by infection-control demand, material innovation (non-latex, nitrile, eco-friendly) and expanding e-commerce adoption.

Download the free sample and get the complete insights and forecasts report on this market @ https://www.towardshealthcare.com/download-sample/6143

Market size

Base & near-term numbers: Market size reached USD 168.9M (2024) and USD 182.1M (2025) — a year-on-year increase reflecting higher clinical uptake and early retail/e-commerce traction.

Long-term projection: The market is projected to be USD 350.2M by 2034, implying the market will roughly double over the next decade.

Growth rate: Forecast CAGR = 7.74% (2025–2034) — indicates steady, above-average growth for a dental consumables niche driven by both clinical and consumer (sexual-health/retail) demand.

Volume vs. value dynamics: Value growth is supported by premiumization (pre-framed kits, nitrile/non-latex options, flavoured/comfort variants) even as per-unit volumes rise in emerging markets.

Channel influence on size: E-commerce and retail are accelerating market reach — increasing smaller, higher-margin consumer pack purchases while distributors continue to serve bulk clinic procurement.

Product mix impact: Shift from low-cost sheet/flat dams to pre-framed kits and specialty materials inflates average selling prices and market value.

Regional contributions: North America contributes the largest revenue share today; Asia-Pacific expected to contribute an increasing share, helping reach the 2034 projection.

Regulatory/standards effect: Class II device regulatory routes (e.g., FDA 510(k), MDR in EU) raise barriers but also support higher price points and trust, affecting market valuation.

Innovation premium: New materials (nitrile, breathable membranes) and comfort features increase willingness to pay among clinics and consumers.

Market concentration & runway: Presence of large dental suppliers and distributors (Henry Schein, Patterson, Dentsply Sirona, 3M) concentrates demand, but product commoditization and new entrants keep growth opportunities open.

Market trends

Material innovation and diversification: Movement from natural rubber latex dominance toward nitrile and other non-latex materials due to allergy concerns and patient preference.

Pre-framed / pre-mounted adoption: Rising preference for pre-framed/pre-mounted dams (fastest CAGR among product forms) because of chairside time savings and standardization in multi-clinic settings.

Sheet/flat dams remain foundational: Flat sheets still dominate the market (2024) due to versatility and cost-effectiveness, especially in training institutions.

Pediatric & comfort-focused products: Increasing availability of flavoured, colourful, and more flexible dams targeting pediatric compliance and behavior management.

Retail & sexual-health overlap: Growth in the retail/consumer segment (fastest CAGR for end-users) as dental dam awareness expands into sexual-health and at-home barrier product markets.

E-commerce expansion: E-commerce/online marketplaces are the fastest-growing distribution channel, enabling discreet consumer purchases and bulk clinic orders.

Corporate dentistry standardization: Dental chains / DSOs standardizing procurement — driving bulk orders and adoption of pre-framed kits and branded consumables.

Regulatory and guidance reinforcement: Standards (FDA, EU MDR, ADA living guidelines) elevate product quality and clinical uptake; non-latex products often classified as Class II devices.

Sustainability & eco-friendly demand: Emerging interest in eco-friendly materials and packaging, appealing to clinics and consumers seeking greener options.

Integration with digital workflows: Dental dams adapted to be compatible with intraoral scanners and digital treatment planning, improving integration in contemporary digital dentistry.

AI impacts / roles for the dental dam market

Material design optimization: AI-driven materials modelling can predict tear strength, elasticity, and allergenicity — speeding development of stronger, hypoallergenic, thinner dental dams.

Personalized fit & comfort: Machine learning models using intraoral scan data can suggest customised pre-cut or pre-framed shapes for better patient comfort and reduced gagging.

Predictive demand forecasting: AI algorithms for distributors and manufacturers can forecast regional demand spikes (e.g., by procedure volume or dental tourism seasons), optimizing inventory and reducing stockouts.

Quality control automation: Computer vision systems inspect production lines to detect micro-tears, thickness variance, or contamination — lowering recalls and improving batch quality.

Supply-chain optimization: Reinforcement-learning models optimize logistics (warehouse allocation, route planning) to reduce lead times for clinics and e-commerce deliveries.

Clinical decision support: AI integrated with dental imaging can flag cases where isolation is critical (e.g., complex endodontics), nudging clinicians to use dental dams when evidence supports better outcomes.

Patient education & behavior models: Conversational AI and adaptive tutorials can guide anxious patients through dam use (demonstrations, breathing techniques), reducing resistance and improving compliance.

Customized product recommendations: E-commerce platforms using recommender systems can match dentists/consumers with the best dam type (nitrile vs latex, pre-framed vs sheet) based on practice profile and past purchases.

R&D acceleration via simulated trials: AI-powered in-silico testing of new materials reduces bench testing time; virtual trials simulate performance under varied conditions, lowering R&D costs.

Post-market surveillance & signal detection: Natural language processing on complaint logs, social media, and customer service tickets helps detect adverse trends early (comfort issues, allergy reports), enabling rapid product improvements and regulatory reporting.

Regional insights

1. North America — market leader (explanation & drivers)

Advanced clinical infrastructure: High density of dental clinics, dental schools, and endodontic specialists increases routine dental dam use.

Regulatory environment & payer support: FDA device classifications and favourable insurance/reimbursement for higher-quality infection-control items increase clinic willingness to buy premium products.

Professional guidance: ADA and AAE recommendations reinforce dental dam use, especially in endodontics — institutionalizing demand.

Innovation demand: Early adoption of nitrile, flavouring, pre-framed kits and integration into continuing education.

2. Europe — regulated, quality-focused market

MDR impact: CE marking under MDR raises compliance costs but increases clinician confidence and allows premium pricing.

Sustainability focus: Higher demand for eco-friendly materials and recyclable packaging.

Diverse payor landscapes: Mixed public/private payment systems influence adoption across countries.

3. Asia-Pacific — fastest growth (subpoints & drivers)

Expanding dental infrastructure: Rising number of clinics and dental professionals in China, India, SE Asia.

Oral health campaigns & public policy: National programs (e.g., China’s Oral Health Action Plan) boost preventive care and use of barrier products.

Dental tourism & cosmetic dentistry: Growth in cosmetic/restorative procedures raises procedural volumes and dam demand.

Price sensitivity & localisation: Demand for cost-effective flat sheets remains, but premium segments (pre-framed, nitrile) grow in urban centers.

4. Latin America — emerging opportunity

Growing private sector clinics: Urban middle classes increase restorative treatment rates.

Distribution challenges: Logistics and fragmented distribution networks create opportunities for local distributors and e-commerce solutions.

5. Middle East & Africa (MEA) — niche & institutional demand

Institutional procurement: Hospitals and NGOs drive demand for infection-control supplies in urban centers.

Education gap: Lower routine adoption in some regions due to limited awareness and training; targeted education can expand use.

6. Country-level notes (U.S. & Canada)

U.S.: Principal driver of North America’s revenue — strong education programs and reimbursement pathways.

Canada: High professional standards but lower utilization in underinsured populations due to cost/access barriers.

Market dynamics

Driver — Rising infection-control emphasis & supportive regulations: Strict device classifications (e.g., FDA Class II for non-latex dams), ADA guidance, and clinical standards elevate usage in restorative and endodontic procedures.

Driver — Growing prevalence of dental disorders: WHO/CDC data cited in the report (billions affected globally; high caries prevalence) increases procedural volumes requiring isolation, fueling demand.

Restraint — Patient discomfort & lack of awareness/training: Gag reflex, breathing concerns, and clinician time pressure reduce routine use; lack of patient education restricts consumer segment growth.

Restraint — Cost sensitivity in emerging markets: While premium products grow, many clinics still prefer low-cost sheets, slowing faster value growth in price-sensitive regions.

Opportunity — Product innovation & premiumization: Pre-framed kits, nitrile, breathable membranes (e.g., ComfiDam), flavoured options increase acceptance and willingness to pay.

Opportunity — Retail & sexual-health crossover: Expansion into consumer retail (home barrier products) and discreet e-commerce sales opens a parallel growth channel.

Opportunity — E-commerce and digital sales models: Online marketplaces enable broader reach for both clinics and consumers; subscription and bulk ordering tools support recurring revenue.

Threat — Regulatory burden & compliance costs: 510(k), MDR, and ISO13485 requirements increase time-to-market and cost for new entrants.

Threat — Commoditization & margin pressure: Large distributors and private label products could compress margins if suppliers compete primarily on price.

Enabler — Corporate dentistry / DSOs: Standard procurement by DSOs increases predictable bulk demand and adoption of standardized, higher-quality consumables.

Top companies

Dentsply Sirona

➣Products: Broad dental consumables & devices; dental dam offerings and barrier products within wider portfolio.

➣Overview: Global dental technology leader with integrated product lines and distribution.

➣Strength: Strong R&D, global distribution, and ability to bundle consumables with larger equipment sales; strategic acquisitions to deepen barrier-materials IP.

3M Oral Care

➣Products: Dental isolation products, barrier films and related consumables.

➣Overview: Diversified healthcare conglomerate with dental specialty segment.

➣Strength: Innovation capability, materials science expertise, and global manufacturing scale.

Henry Schein

➣Products: Distributor and private-label dental consumables including dental dams and kits.

➣Overview: Major distributor serving clinics with B2B procurement solutions.

➣Strength: Vast distribution network, clinician relationships, and logistics expertise.

Patterson Dental

➣Products: Dental supplies distribution including dams, frames, kits.

➣Overview: North American distributor focused on practice supply chain.

➣Strength: Strong regional presence, customer service, and bundled supply contracts with clinics.

Coltene (HySolate / ROEKO Flexi Dam)

➣Products: ROEKO/HySolate Flexi Dam rebranded — sheet and specialised barrier solutions.

➣Overview: Specialist dental materials manufacturer.

➣Strength: Brand recognition in dental isolation products and focused product innovation (recent rebranding shows portfolio strategy).

Ultradent Products

➣Products: Dental materials and accessories, including dam systems.

➣Overview: Specialty dental manufacturer known for clinical-grade consumables.

➣Strength: Clinician-driven product design and strong endodontics reputation.

Envista Holdings / Kerr

➣Products: Dental materials, isolation accessories, and restorative supplies.

➣Overview: Large dental products conglomerate with multiple brands.

➣Strength: Broad portfolio, channel reach, and cross-selling to labs/clinics.

Premier Dental

➣Products: Isolation products, dental adhesives, and supplies.

➣Overview: Focused dental products supplier to professional market.

➣Strength: Niche product focus and strong relationships with specialty practices.

VOCO GmbH

➣Products: Dental materials and accessories, including isolation solutions.

➣Overview: European dental materials specialist.

➣Strength: Strong product development and acceptance in restorative dentistry markets.

Medline Industries / TIDI Products

➣Products: Medical/dental barrier products, kits and PPE-adjacent supplies.

➣Overview: Large medical supplier with dental channel presence.

➣Strength: Scale in medical distribution, cross-market selling into dental clinics and hospitals.

Latest announcements

Dentsply Sirona — February 2025 strategic review of Wellspect Healthcare

➣What happened: CEO Simon Campion announced the company had started assessing strategic options for its Wellspect Healthcare division as part of a transformation strategy.

➣Why it matters: Strategic review signals potential divestitures, spinoffs, or re-investment — moves that could reallocate capital towards core dental product innovation (including barrier materials) or change competitive dynamics in related product areas.

➣Potential market effect: If Dentsply Sirona repositions Wellspect, it could free resources for dental dam R&D or alter supply relationships for clinics that source multiple consumables from Dentsply.

Coltene — December 2024 rebrand of ROEKO Flexi Dam to HySolate Flexi Dam

➣What happened: Product name and packaging change to align the dental dam into the HySolate family.

➣Why it matters: Rebranding can increase product visibility, support cross-selling within a product family, and signal renewed marketing emphasis on isolation solutions.

ConfiDental Labs / ComfiDam (April 2025) — student startup innovation

➣What happened: University of Toronto student Arshia Sabet introduced ComfiDam, an air-permeable membrane dental dam to improve patient breathing comfort.

➣Why it matters: Early-stage innovations addressing comfort can tackle one of the market’s core restraints (patient discomfort), accelerating clinician adoption and pediatric use. Startups signal continued niche R&D outside large manufacturers.

Recent developments

Rebranding & portfolio consolidation (Coltene → HySolate): Aligns dental dam product under unified family to strengthen marketing and cross-product integration.

Large manufacturer strategic moves (Dentsply Sirona): Corporate restructuring and asset reviews may shift investment toward barrier material IP or reshape supply chains.

Startup innovation (ComfiDam): Demonstrates targeted solutions for patient comfort (air-permeable membranes) — directly addressing gagging/breathing complaints and opening pediatric/longer-procedure use cases.

Acquisitions and inorganic growth: Dentsply Sirona’s strategic acquisitions expand dental dam product lines and IP in barrier materials — consolidates supplier base and brings new tech to market faster.

Consumer market expansion: Retail/consumer segment growth driven by e-commerce, flavoured and non-latex variants, and sexual-health positioning.

Regulatory & guideline reinforcement: ADA Living Guidelines and device classification spur adoption through clearer clinical recommendations.

Digital dentistry congruence: Vendors adapting dam products for compatibility with digital impressioning and treatment-planning workflows.

Supply chain & distribution shifts: E-commerce and direct-to-clinic models begin to compete with traditional distributor/wholesaler channels.

Material shift trends: Increased R&D into nitrile and specialty elastomers for allergy mitigation and comfort.

Education & university partnerships: Collaborations (e.g., education partnerships noted with manufacturers) help train new dentists in consistent dam use — institutionalizing demand.

Segments covered

By Product Form

➣Sheet / flat dental dams (unpunched): Versatile, low-cost; preferred in training and where customs require tailoring. Dominant in 2024 due to adaptability.

➣Pre-punched dental dams: Provide faster placement for standard procedures (e.g., single-tooth treatments).

➣Pre-framed / pre-mounted dams: Fastest-growing — reduce chairside setup time, improve consistency in high-volume practices and DSOs.

➣Dental dam kits: Bundled solutions (sheet + clamp + punch + frame) attractive for new practitioners and clinics wanting ready sets.

➣Accessories: Frames, clamps, punchers — complementary revenue and durability segment (reusable frames increase lifecycle value).

By Material / Composition

➣Natural rubber latex: 2024 largest revenue share — elasticity, seal quality, and cost-effectiveness.

➣Nitrile (synthetic): Fastest growth — hypoallergenic, strong, chemical resistant; preferred in allergy-sensitive markets.

➣Polyurethane (PU) & Vinyl (PVC): Alternatives balancing cost and comfort; used in specific use-cases or regions.

➣Silicone / specialty elastomers: Niche use for reusable frame systems and premium comfort products.

By End-user / Buyer

➣Dental clinics & solo practitioners: Largest revenue share (routine restorative/endodontic work).

➣Dental hospitals & academic institutions: Source of bulk purchases and training demand.

➣Dental chains & group practices (DSOs): Standardized procurement — driving pre-framed/kits adoption.

➣Retail/consumer (sexual-health market): Fastest-growing — flavoured, non-latex options sold via e-commerce.

By Distribution Channel

➣Dental distributors / wholesalers: Traditional dominant channel for clinics — bulk, credit terms, product range.

➣Direct sales (B2B): For large DSOs and hospitals preferring direct supplier relationships.

➣E-commerce / online marketplaces: Rapid expansion for both clinic replenishment and consumer sales; enables subscriptions and discreet retail.

➣Pharmacies & sexual-health retailers: Growing for consumer access and at-home products.

➣Institutional procurement: Hospitals/government tenders for public dental programs.

By Region

➣North America (dominant): Advanced infrastructure and strong clinical protocols.

➣Asia-Pacific (fastest growth): Rapid clinic expansion and public oral health programs.

➣Europe, Latin America, MEA: Varying adoption tied to regulation, access, and private vs public care mix.

Top 5 FAQs

-

Q: What was the global dental dam market size in 2024 and 2025?

A: USD 168.9 million in 2024 and USD 182.1 million in 2025. -

Q: What is the projected market size and growth rate through 2034?

A: Projected to reach USD 350.2 million by 2034, with a CAGR of 7.74% between 2025 and 2034. -

Q: Which product forms dominate and which are growing fastest?

A: Sheet/flat dental dams dominated in 2024 due to versatility; pre-framed/pre-mounted dams are expected to grow at the highest CAGR because of ease-of-use and time savings. -

Q: Which materials lead the market and which will grow fastest?

A: Natural rubber latex held the largest revenue share in 2024 for its elasticity and cost; nitrile is expected to grow fastest due to allergy concerns and improved comfort. -

Q: Which regions and end-user segments are most important?

A: North America held major revenue share in 2024 (advanced infrastructure, regulatory support). Asia-Pacific is expected to witness the fastest growth. Dental clinics & solo practitioners contributed the biggest revenue share in 2024; retail/consumer is the fastest-growing end-user segment.

Access our exclusive, data-rich dashboard dedicated to the dental sector – built specifically for decision-makers, strategists, and industry leaders. The dashboard features comprehensive statistical data, segment-wise market breakdowns, regional performance shares, detailed company profiles, annual updates, and much more. From market sizing to competitive intelligence, this powerful tool is one-stop solution to your gateway.

Access the Dashboard: https://www.towardshealthcare.com/access-dashboard

Immediate Delivery Available | Buy This Premium Research @ https://www.towardshealthcare.com/price/6143

Become a valued research partner with us – https://www.towardshealthcare.com/schedule-meeting

You can place an order or ask any questions, please feel free to contact us at [email protected]

Powering Healthcare Leaders with Real-Time Insights: https://www.towardshealthcare.com/healthcare-intelligence-platform

Europe Region – +44 778 256 0738

North America Region – +1 8044 4193 44

APAC Region: +91 9356 9282 04

Web: https://www.towardshealthcare.com

Find us on social platforms: LinkedIn | Twitter | Instagram | Medium | Pinterest