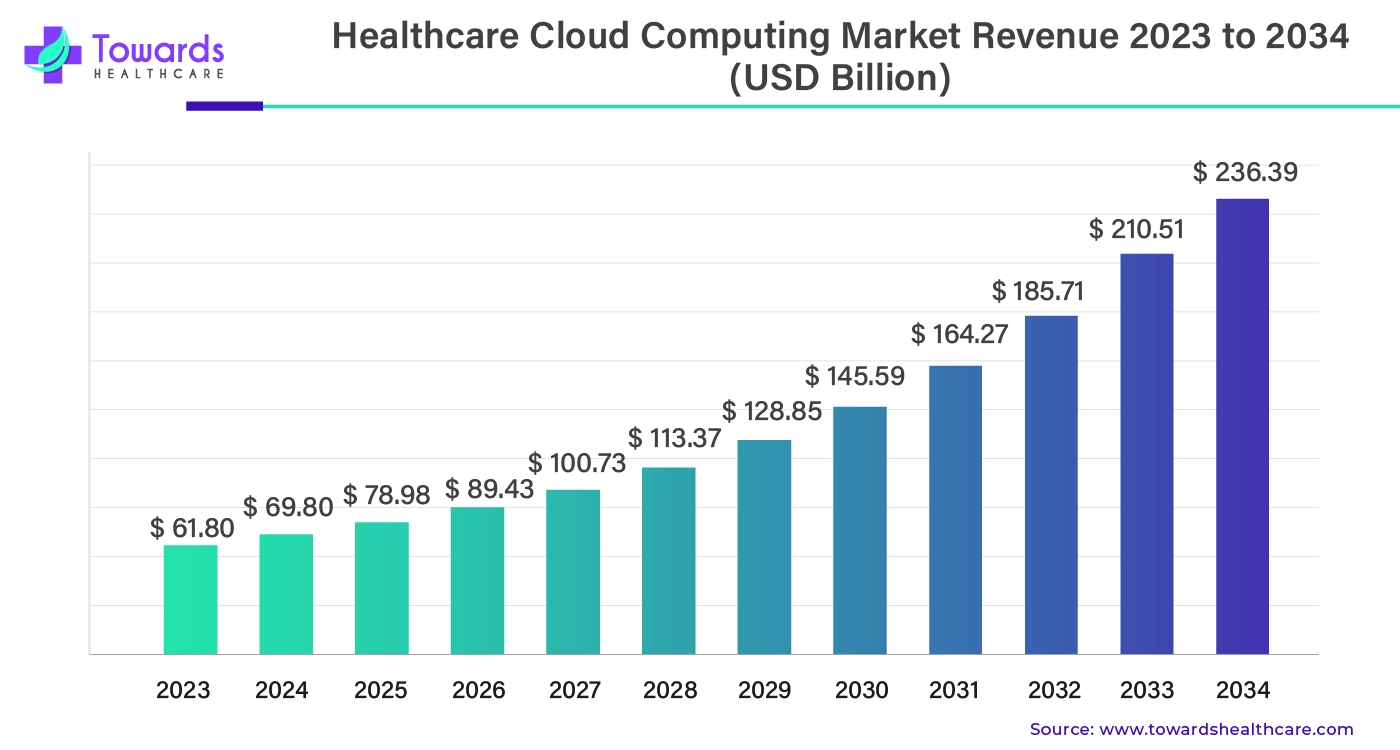

The global healthcare cloud computing market was estimated at US$61.80 billion (2023) and is projected to reach US$236.39 billion by 2034 — a 13.05% CAGR (2024–2034) — driven by hospital digitization, SaaS adoption for non-clinical systems, private cloud uptake and rising telehealth and AI workloads.

Download this Free Sample Now and Get the Complete Report and Insights of this Market Easily @ https://www.towardshealthcare.com/download-sample/5221

Market size

• Base / forecast numbers (your data): US$61.80B in 2023 → US$236.39B by 2034 (CAGR 13.05% for 2024–2034).

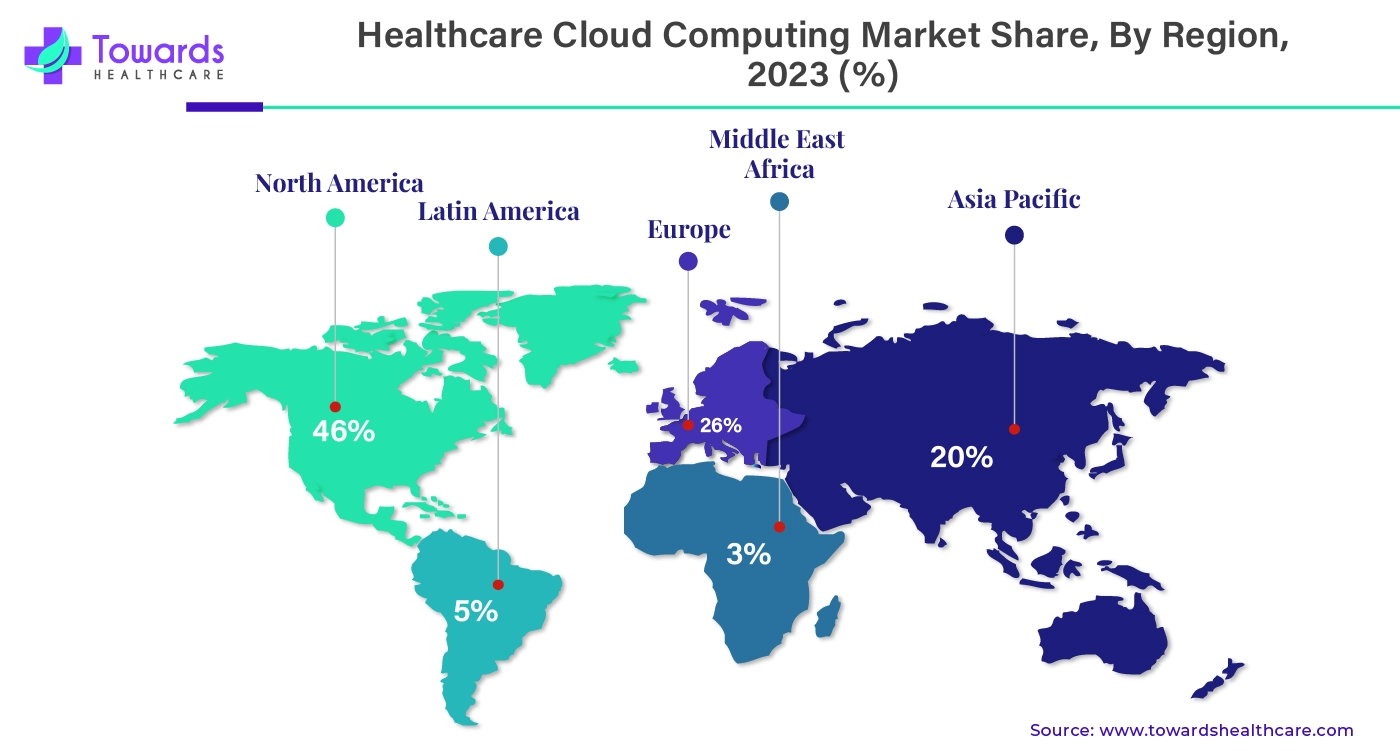

• 2023 regional split (headline): North America ~46% share in 2023 (single largest region).

• 2023 deployment split (headline): Private cloud 53% share (largest deployment).

• 2023 service model dominance: SaaS was the dominant service in 2023 (largest revenue share among SaaS/PaaS/IaaS).

• 2023 end-user: Healthcare providers comprised 57% of end-user market share in 2023.

• Revenue concentration: The market shows a classic skew — a few large vendors and major hospital systems account for a large share of commercial spend (implied by SaaS and private cloud dominance).

• Market scale drivers: rising health data volumes (EHR, imaging, genomics), telehealth growth, regulatory modernization and vendor partnerships (examples included below).

• Capital intensity: heavy vendor investment in compliant private/hybrid stacks and imaging/AI compute creates a multi-billion dollar addressable infrastructure and services opportunity.

• Time horizon: 2024–2034 is a long, AI-heavy growth window — expect iterative waves (telehealth → imaging & PHM → AI/omics).

• Implication for buyers: shifting from CapEx (on-prem) to OpEx (cloud subscriptions) — hospitals prioritize security/compliance and predictable costs.

Market trends

SaaS first: SaaS dominates because it lowers deployment friction for RCM, EHR add-ons, telehealth and patient engagement tools. Example: Oneview/MyStay Mobile (Feb 2024) as a SaaS patient-facing service.

Private/hybrid emphasis: Private cloud had 53% share (2023) — large providers prefer private/hybrid for control, data residency and integration with legacy systems (Macquarie/VITG private cloud example).

Non-clinical workloads lead: Non-clinical systems (billing, RCM, accounts) were 68% of application share in 2023 — money flows first to revenue, admin and scalability wins.

Provider spending concentration: Healthcare providers (57%) drive the majority of demand — hospitals and health systems are primary buyers.

Regional leader & follower pattern: North America leads (~46%) with APAC fastest growing — implications: innovation in NA, rapid capacity build in APAC.

Imaging & enterprise PACS to cloud: Cloud enterprise imaging (GE Healthcare Genesis, Philips HealthSuite Imaging) is a major new SKU category driving large storage + compute spend.

AI as a platform pull: Vendors partner with cloud hyperscalers and build AI-ready platforms (Bayer + Google Cloud; Cognizant + Google Cloud LLMs) — cloud is the delivery vehicle for AI.

Security & compliance as buying filters: New legal frameworks (Germany’s §393, NHS Cloud Center of Excellence) and HIPAA expectations push customers to certified private/hybrid deployments.

Telehealth normalization: Telehealth increases demand for always-on cloud services, patient portals and remote monitoring.

Edge + 10G / low latency: Growth of imaging, remote monitoring and real-time analytics drives investment in high-bandwidth networks and edge/cloud blends (your 10G note).

AI impacts / roles in this market

AI as demand amplifier for cloud compute & storage

Generative AI models, imaging AI and LLM assistants need large GPU/TPU clusters and scalable object storage for imaging/genomics — clouds supply elastic capacity.

Example tie: Bayer → Google Cloud genAI for radiology; Cognizant → Vertex/Gemini LLM stacks.

AI-enabled clinician assistants reduce admin time

AI digital assistants (NLP summarizers, note generation) cut charting time — reduces administrative overhead and increases EHR/SaaS uptake (Qventus estimate on admin time loss referenced in your content).

Automated revenue cycle optimization

ML for claim denial prediction, automated coding and billing optimization run as SaaS on cloud — increases collections and ROI from cloud migrations.

Real-time imaging analytics at scale

Cloud enterprise imaging + AI enables distributed reading, triage, and decision support (GE Genesis, Philips HealthSuite Imaging examples).

Personalized medicine & genomics pipelines

Sequence analysis and omics require burst compute; cloud + AI pipelines accelerate variant calling, enabling cloud to capture genomics workloads.

Federated / privacy-preserving AI models

Private/hybrid clouds enable federated learning across hospitals without moving raw PHI — preserves privacy while enabling model training.

Operational automation & observability

AI for anomaly detection in infrastructure/security (cloud security telemetry) improves uptime and compliance posture; lowers hidden ops costs.

Clinical triage & population health

AI models running on cloud aggregate multi-site data to stratify risk and guide interventions for PHM (cloud enables central orchestration).

Conversational interfaces & patient engagement

GenAI chatbots, appointment schedulers, discharge instructions delivered as SaaS increase patient portal value and cloud recurring revenue.

Regulatory compliance automation & evidence generation

AI to scan logs, enforce encryption, generate audit trails and prepare evidence for certifications (helps meet frameworks like NHS cloud guidance and national standards).

Regional insights

North America (46% share in 2023)

• Why dominant: advanced IT infrastructure, large hospital systems, regulatory clarity (HIPAA guidance for cloud).

• Buying behavior: willingness to pay for SaaS, private/hybrid and AI-ready cloud stacks; major vendor presence (Microsoft, AWS, Oracle, VMware).

• Product focus: enterprise imaging, RCM SaaS, LLM assistants for admin tasks.

Asia Pacific (fastest growth)

• Why fastest: large populations, rising hospital investments (China, India, Japan, SK), national digital health pushes.

• Country nuance: China — scale & domestic cloud providers; India — telemedicine growth (your India growth numbers), government digital health initiatives driving cloud adoption.

Europe

• Regulatory nuance: country-level standards (Germany §393) and NHS cloud strategy guide public cloud adoption with strong compliance requirements.

• Adoption pattern: gradual modernization, strong emphasis on data residency and sovereign/private cloud options (Macquarie/VITG example fits the sovereignty trend).

Latin America & MEA

• Emerging demand: cloud literacy rising; telehealth and imaging pilots push early adoption; often rely on multi-region cloud vendors and partner programs (AWS Industry Quest example for LATAM).

Country highlights (subpoints)

• China: strong in scale & funding for cloud health platforms — large user bases for national health programs.

• India: hospital sector growth (INR numbers you provided) + telemedicine projected growth to $5.4B by 2025 fosters cloud adoption.

• UK/Germany: centralized programs (NHS Cloud Center, Germany §393) provide frameworks to accelerate compliant cloud migration.

Market dynamics

Drivers

Data growth from EHRs, imaging, genomics → need for elastic storage/compute.

Telehealth adoption → always-on cloud apps and patient portals.

SaaS economics → predictable OpEx, faster upgrades and interoperability.

Vendor partnerships & hyperscaler AI stacks (Bayer+Google, Cognizant+Google) accelerate productization.

Private/hybrid options → balance between control and cloud scalability (53% private share).

Restraints

Security & data breach risk → sensitive PHI, financial and national security concerns; requires heavy investment in cloud security.

Regulatory/compliance uncertainty across borders → data residency, national frameworks slow adoption.

Legacy systems & integration costs → complex EHR integrations make migrations expensive.

Opportunities

Imaging & enterprise PACS to cloud (large storage revenues; GE & Philips moves highlight this).

AI-first clinical and non-clinical apps — new recurring revenue for SaaS vendors.

Sovereign cloud offerings — government-certified private clouds (Macquarie/VITG) for regulated markets.

Edge + cloud hybrid for low latency care — 10G networks enabling richer remote monitoring experiences.

Top Companies

1. Microsoft Corp

Product: Azure + Healthcare Platform Services

Overview: Major hyperscaler offering PaaS, IaaS, and SaaS solutions for healthcare, enabling interoperability across hospital systems and cloud applications.

Strength: Enterprise reach, strong compliance tooling, seamless integration with EHR vendors, and AI ecosystem support.

2. Amazon Web Services (AWS)

Product: AWS Cloud & Health Suite (including Industry Quest)

Overview: Cloud platform providing scalable infrastructure, training programs, and specialized healthcare services.

Strength: Broad service portfolio, large partner network, and healthcare-specific training and support.

3. Google Cloud

Product: Vertex AI, Generative AI, and healthcare-specific cloud services

Overview: Cloud platform focused on AI/ML integration for healthcare, working with partners like Bayer and Cognizant.

Strength: Advanced AI/ML capabilities, strong genomics and radiology partnerships, and scalable cloud infrastructure.

4. IBM / VMware

Product: Private/hybrid infrastructure and cloud management platforms

Overview: Solutions for enterprise virtualization, hybrid cloud deployments, and IT infrastructure management in healthcare.

Strength: Strong on-prem integration, trusted enterprise footprint, and expertise in regulated healthcare environments.

5. GE Healthcare

Product: Genesis — Cloud Enterprise Imaging SaaS

Overview: Specialized in cloud-based imaging workflows, enabling hospitals to store, manage, and analyze medical images.

Strength: Domain expertise in imaging, established clinical adoption channels, and SaaS delivery for radiology departments.

6. Philips

Product: HealthSuite Imaging (cloud deployment on AWS)

Overview: Cloud-based radiology informatics solutions to manage imaging data across hospitals and regions.

Strength: Expertise in imaging workflows, scalable cloud deployment, and strong clinical user adoption.

7. Oracle / Dell / EMC

Product: Enterprise databases, storage, and private cloud stacks

Overview: Provides foundational IT infrastructure for healthcare organizations transitioning from on-premise to cloud solutions.

Strength: Secure, scalable solutions; deep enterprise relationships; strong private cloud capabilities for regulated healthcare data.

8. Cognizant

Product: LLM and Generative AI solutions built on Google Cloud

Overview: System integrator delivering AI-powered administrative and clinical workflows for healthcare providers.

Strength: Ability to integrate cloud infrastructure with enterprise health IT systems and develop vertical-specific AI applications.

9. Allscripts / Athenahealth

Product: EHR/SaaS products and Revenue Cycle Management (RCM) solutions

Overview: Cloud-based software for clinical workflows, billing, and administrative management.

Strength: Strong EHR footprint, robust payer/provider integrations, and recurring revenue through SaaS deployment.

10. Iron Mountain / Zadara / Rackspace

Product: Secure storage and managed private cloud operations

Overview: Vendors providing cloud storage, data management, and managed services tailored for regulated healthcare environments.

Strength: Compliance-ready solutions, secure storage, and operational expertise for healthcare IT systems.

Latest announcements

GE Healthcare (March 2025) — What: Launch of Genesis portfolio — cloud enterprise imaging SaaS. Why it matters: consolidates imaging storage, reading workflows and AI tool integration into SaaS; reduces on-prem PACS spend and drives recurring revenue.

Philips (Feb 2025) — What: Expansion of Philips HealthSuite Imaging to Europe (hosted on AWS). Why: scaling a cloud radiology platform across regions increases addressable market and interop with AWS AI services.

Bayer + Google Cloud (April 2024) — What: Partnership to leverage Google Cloud genAI for radiology apps. Why: an example of pharma/medtech pairing with hyperscalers to accelerate clinical AI app dev.

Cognizant + Google Cloud (June/August 2024) — What: First LLM solutions for healthcare on Google Cloud (Vertex/Gemini). Why: system integrators productizing LLMs for administrative workflows and patient experience.

Hitachi Vantara (Aug 2024) — What: Private & hybrid cloud environment introduction to improve hospital IT infrastructures and reduce vendor friction. Why: reinforces private cloud demand for hospitals.

Oneview Healthcare (Feb 2024) — What: MyStay Mobile SaaS for patient digital services (NYU Langone testing). Why: example of bedside/patient experience SaaS driving SaaS adoption in hospitals.

Macquarie Cloud Services + VITG (Sep 2023) — What: Sovereign private cloud for healthcare clients (government hosting certification). Why: shows the sovereign cloud trend for regulated health data.

AWS Industry Quest (Aug 2023) — What: Training labs in Latin America/Canada for designing healthcare cloud solutions. Why: ecosystem development to increase cloud skill supply.

Fujitsu (Mar 2023) — What: Cloud platform for secure aggregation and HL7 FHIR conversion. Why: demonstrates cloud adoption to meet interoperability standards.

Recent developments

• Multiple major vendors launched imaging-focused cloud SaaS (GE Genesis, Philips HealthSuite) — signals a platform shift for radiology workloads.

• Partnerships between life sciences/medical device firms and hyperscalers (Bayer/Google) accelerate model creation and productization.

• System integrators (Cognizant) are packaging LLM/GenAI offerings for healthcare administrative automation.

• Sovereign/private cloud offerings proliferate (Macquarie/VITG, Hitachi) to meet government and large provider needs.

• Education/training initiatives (AWS Industry Quest) target skill gaps in regional markets.

Segments covered

1. By Deployment

Private Cloud

Definition: Single-tenant cloud environments dedicated to a single healthcare organization.

Importance: Offers enhanced data residency, security, and regulatory compliance, making it ideal for hospitals managing sensitive patient data (PHI, financial records, genomics).

Market Data: Dominated the deployment segment with 53% share in 2023.

Use Case Examples:

Macquarie Cloud Services + VITG — sovereign private cloud for regulated healthcare clients.

Hitachi Vantara’s private/hybrid cloud environment — designed to reduce vendor friction and improve IT infrastructure.

Public Cloud

Definition: Multi-tenant cloud services offered by hyperscalers (AWS, Azure, Google Cloud).

Importance: Provides scale, cost efficiency, and elasticity, especially for workloads that do not require storing sensitive PHI.

Use Case Examples: Startups and digital health companies leveraging SaaS applications for telehealth, patient engagement, or analytics.

Hybrid Cloud

Definition: Combination of on-premises systems, private cloud, and public cloud bursts for dynamic workloads.

Importance: Ideal for AI-intensive workloads such as imaging analysis, genomics pipelines, and telehealth video streaming.

Advantages: Balances compliance (private/on-prem) with scalability and flexibility (public cloud bursts).

2. By Service

Software as a Service (SaaS)

Definition: Cloud-delivered applications accessed via browsers or mobile apps.

Importance: Dominant revenue model; enables healthcare organizations to deploy quickly without large upfront CapEx.

Applications:

Electronic Health Records (EHR) add-ons

Revenue Cycle Management (RCM)

Telehealth platforms

Patient engagement apps (e.g., Oneview Healthcare’s MyStay Mobile)

Advantage: Low friction for adoption and upgrades, recurring subscription revenue for vendors.

Platform as a Service (PaaS)

Definition: Cloud platforms that allow developers to build, deploy, and manage applications.

Importance: Facilitates custom clinical and analytics applications, enabling system integrators and hospitals to create tailored solutions.

Use Case: LLM/GenAI solutions for administrative workflow automation (Cognizant + Google Cloud Vertex AI).

Infrastructure as a Service (IaaS)

Definition: Raw compute, storage, and networking resources provided on-demand.

Importance: Supports large-scale workloads, including medical imaging, genomics analysis, and AI training models.

Use Case Examples:

Cloud storage for imaging archives (GE Healthcare Genesis, Philips HealthSuite Imaging)

Scalable GPU clusters for AI-based diagnostics

3. By End-User

Healthcare Providers

Definition: Hospitals, clinics, and other patient care facilities.

Market Share: 57% in 2023 — the largest end-user segment.

Importance: Primary buyers for SaaS applications, imaging platforms, EHR add-ons, telehealth solutions.

Impact: Cloud computing improves workflow efficiency, data sharing, patient experience, and administrative automation.

Healthcare Payers

Definition: Insurance companies and payers managing claims, reimbursements, and analytics.

Importance: Leverage cloud computing for fraud detection, claims processing, cost analytics, and population health management.

Advantage: Reduces operational costs and improves data-driven decision-making for payers.

4. By Region

North America (NA)

Share: 46% in 2023

Drivers: Advanced IT infrastructure, strong adoption of private/hybrid clouds, government support, large hospital networks.

Examples: Microsoft Azure, AWS Health Suite deployments; GE & Philips cloud imaging SaaS.

Asia Pacific (APAC)

Forecast: Fastest-growing region

Drivers:

Rising population and patient volumes

Growing hospital infrastructure investments (China, India, Japan, South Korea)

Telemedicine expansion and National Digital Health initiatives in India (projected $5.4B telemedicine by 2025)

Impact: Rapid cloud adoption for both clinical and non-clinical workflows.

Europe

Drivers: Regulatory frameworks (e.g., Germany §393, NHS Cloud Strategy), growing healthtech startups, and adoption of telehealth & digital solutions.

Trend: Focus on sovereign/private cloud adoption for compliance and secure data storage.

Latin America (LA)

Drivers: Cloud literacy growth, telehealth and imaging initiatives, regional AWS training programs (Industry Quest).

Trend: Emerging adoption with reliance on hyperscalers and managed cloud services.

Middle East & Africa (MEA)

Drivers: Early-stage cloud adoption in hospitals, government health digitization initiatives, telemedicine pilots.

Trend: Investments in secure and compliant cloud infrastructure, often via regional partnerships with global vendors.

Top 5 FAQs

-

Q: How big is the healthcare cloud computing market?

A: US$61.80 billion (2023) with a projection to US$236.39 billion by 2034, at a 13.05% CAGR for 2024–2034 (your figures). -

Q: Which region leads and which is growing fastest?

A: North America led with 46% market share in 2023; Asia Pacific is expected to grow the fastest during the forecast period. -

Q: What deployment and service models dominate?

A: Private cloud (53% share in 2023) leads deployments; SaaS is the dominant service model for healthcare cloud offerings. -

Q: What are the main restraints?

A: Primary restraint is security & data privacy — patient PHI and financial data make cloud security and compliance essential; regulatory fragmentation also slows some cross-border cloud moves. -

Q: Where will vendors find the largest near-term opportunities?

A: Enterprise imaging SaaS, RCM/billing SaaS, telehealth platforms, AI-first clinical and admin solutions, and sovereign/private cloud offerings — these map directly to the announcements and trends you provided (GE, Philips, Bayer/Google, Macquarie/VITG).

Access our exclusive, data-rich dashboard dedicated to the healthcare market – built specifically for decision-makers, strategists, and industry leaders. The dashboard features comprehensive statistical data, segment-wise market breakdowns, regional performance shares, detailed company profiles, annual updates, and much more. From market sizing to competitive intelligence, this powerful tool is one-stop solution to your gateway.

Access the Dashboard: https://www.towardshealthcare.com/access-dashboard

Immediate Delivery Available | Buy This Premium Research @ https://www.towardshealthcare.com/price/5221

Become a valued research partner with us – https://www.towardshealthcare.com/schedule-meeting

You can place an order or ask any questions, please feel free to contact us at [email protected]

Powering Healthcare Leaders with Real-Time Insights: https://www.towardshealthcare.com/healthcare-intelligence-platform

Europe Region – +44 778 256 0738

North America Region – +1 8044 4193 44

APAC Region: +91 9356 9282 04

Web: https://www.towardshealthcare.com

Find us on social platforms: LinkedIn | Twitter | Instagram | Medium | Pinterest