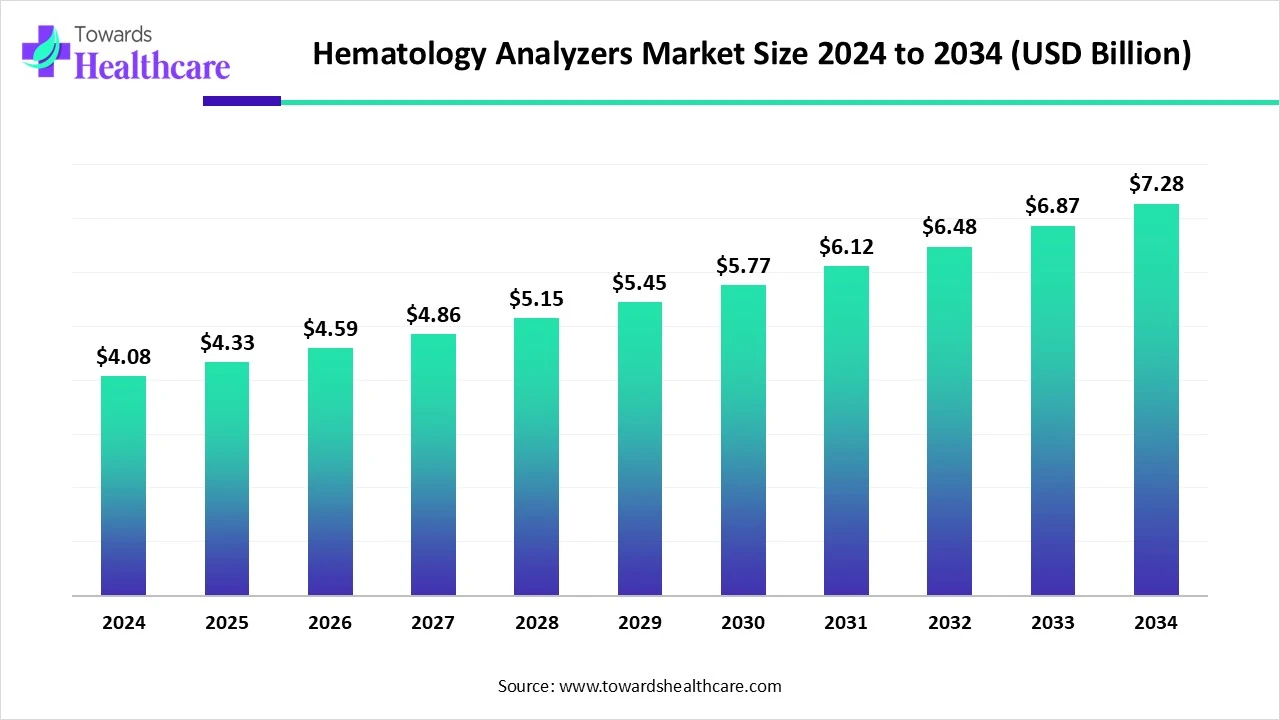

The global hematology analyzers market was US$ 4.08 billion in 2024, is US$ 4.33 billion in 2025, and is projected to reach US$ 7.28 billion by 2034 at a 5.97% CAGR (2025–2034), led by North America (41% share, 2024) and fastest growth in Asia Pacific.

Download the free sample and get the complete insights and forecasts report on this market @ https://www.towardshealthcare.com/download-sample/5838

Market Size

1) Baseline & Forecast

●2024: US$ 4.08 B → 2025: US$ 4.33 B → 2034: US$ 7.28 B (CAGR 5.97%, 2025–2034).

●Absolute growth addition 2025–2034: US$ 2.95 B.

2) Growth Drivers Shaping Dollars

●Clinical burden: Rising anemia, leukemias, coagulation disorders; aging cohorts increase routine CBC demand.

●Technology mix: Shift toward automated high-throughput, AI/ML-assisted analyzers, and POCT adds premium ASPs.

●Lab consolidation: Centralized reference labs and hospital networks expand installed base & reagent pull-through.

3) Product Mix Impact on Revenue

●5-part differential analyzers held 51% (2024)—main volume/value anchor.

●6-part & high-end forecast as fastest-growing tier (2025–2034), lifting blended ASPs.

4) Technology Mix Influence

●Flow-cytometry–based platforms commanded 46% (2024); AI/ML-integrated systems to outpace on growth.

5) Customer & Modality Effects

●Hospitals were 42% (2024) of spend; ASC/physician offices to grow fastest with POCT diffusion.

●Standalone systems led 2024 revenue; integrated chemistry/immunoassay combos to accelerate.

6) Regional Dollar Pools

●North America: largest 2024 pool (41%).

●Asia Pacific: fastest incremental dollar creation through 2034, supported by infrastructure build-out.

Market Trends

1) Automation & High Throughput

●Labs upgrade to high-throughput analyzers to handle chronic disease screening and oncology workflows.

2) AI/ML Integration

●Movement toward AI-driven differentials, morphology pre-classification, QC anomaly detection, and workflow orchestration.

3) Point-of-Care Expansion

●POCT CBC analyzers gain traction in clinics/EDs; faster triage and decentralized screening.

4) Strategic Partnerships

●Dec 2024: Axonia Medical partners with multiple OEMs to broaden lab equipment access.

●Apr 2024: PixCell Medical expands U.S. distribution of HemoScreen via Medline, Henry Schein, Thermo Fisher.

●Mar 2024: Sysmex–CellaVision alliance advances integrated hematology solutions.

5) Integrated Diagnostic Platforms

●Combined hematology + chem/immunoassay systems targeted for throughput and single-vendor service.

6) Preventive & Oncology Screening

●Preventive checkups and cancer pathways (pre-chemo, monitoring) sustain recurring CBC volumes.

7) Supply/Trade Dynamics

●China led exports (Oct 2023–Sep 2024; 59 exporters to 85 buyers; +19% growth); France #2 by shipments; Hong Kong exports grew +121% (May 2024–Apr 2025).

●Top importers include Indonesia (210 shipments), Uganda (64), and India (135).

8) Home Healthcare & Telemedicine

●Early interest in home phlebotomy/remote monitoring nudges demand for compact/microfluidic analyzers.

9) Regulatory & Access Push

●Government programs (e.g., Ayushman Bharat in India) and national lab networks improve awareness and test uptake.

10) Compact Instruments with ESR On-board

●HORIBA (Jun 2024) added compact models with ESR on board to reduce reflex testing steps.

10 Ways AI Impacts Hematology Analyzers

1) Differential Pre-classification

●AI models pre-classify WBC subtypes and flag atypical cells, cutting manual review time and inter-observer variability.

2) Image-assisted Morphology

●Vision models on digital slides integrate with analyzers to prioritize smears requiring pathologist review.

3) QC Drift Detection

●Unsupervised algorithms monitor reagent/instrument drift; trigger recalibration before failures.

4) Anomaly & Rare Event Detection

●Outlier detection surfaces blasts, schistocytes, or platelet clumps—improving early leukemia/hemolysis flags.

5) Reflex Testing Orchestration

●Rules engines auto-order retests/ESR/flow cytometry when patterns meet confidence thresholds.

6) Throughput Optimization

●Predictive batching and smart routing balance workload across multi-site lab networks.

7) Error Reduction & Traceability

●Intelligent checks catch sample ID mismatches, anticoagulant issues, or clotted samples before result release.

8) Personalized Baselines

●Patient-specific trend models (delta checks) differentiate biological change from noise—useful in oncology monitoring.

9) POCT Decision Support

●On-device AI in POCT analyzers guides non-specialist users, standardizing performance outside core labs.

10) Cost-to-Serve Analytics

●AI maps utilization, reagent consumption, and service cycles to optimize TCO and service contracts.

Regional Insights

North America (41% share, 2024)

Diagnostic Volume: High chronic disease screening and oncology workloads sustain high CBC/test densities.

Lab Consolidation: Centralized reference labs standardize analyzer fleets, boosting reagent annuities.

Innovation & Pilots: BD + Babson fingertip blood collection (Dec 2024) and AI pilots accelerate decentralized testing.

Asia Pacific (Fastest CAGR 2025–2034)

Infrastructure Build-out: India/China/SEA invest in labs; demand for standalone and mid-tier analyzers.

Disease Burden: Elevated anemia/thalassemia/cancers—especially rural India—raises testing needs.

Policy Levers: Programs like Ayushman Bharat expand awareness/access; private chains scale hubs.

Europe (Solid Growth; tech preference & POCT)

Tech Integration: Flow cytometry + AI + automation adopted to address staffing gaps.

POCT in Outpatient/Emergency: Demand for compact devices with ESR on-board (e.g., HORIBA updates, 2024).

Research Focus: Emphasis on translational medicine and precision diagnostics fuels high-end analyzer uptake.

China

Aging Demographics: Higher hematologic disease susceptibility; government promotes routine testing.

Digital Access: Online healthcare platforms expand therapy awareness and routine follow-ups.

India

Rising Disorders: Anemia/thalassemia prevalence drives CBC penetration beyond metros.

Public-Private Initiatives: Blood donation drives and national insurance coverage support diagnosis pipelines.

Latin America

Modernization: Brazil/Mexico labs upgrade analyzers; logistics improvements aid reagent continuity.

Access Challenges: Public procurement cycles can delay refresh; POCT fills service gaps.

Middle East & Africa

Selective Modernization: Tertiary centers adopt high-end systems; NGOs/private labs drive POCT.

Trade Patterns: Imports from China/HK/US supply growth markets like Uganda.

Market Dynamics

Drivers

Rising blood disorders (anemia, leukemia, coagulation) and aging populations expanding CBC volumes.

Technology advances: AI/ML integration, high-throughput automation, POCT, and microfluidics raise accuracy and speed.

Oncology & Preventive Health: Routine monitoring and screenings cement recurring demand.

Restraints

High upfront costs for advanced systems; budget constraints in developing markets.

Skilled personnel shortages for complex instruments; training/retention gaps.

Regulatory latency can slow the adoption of novel technologies.

Opportunities

6-part/high-end analyzers and integrated platforms for consolidated labs.

Home healthcare & telemedicine: miniaturized, cloud-connected devices for remote monitoring.

AI-enhanced accuracy and automated workflows; microfluidics/LoC innovations.

Top 10 Companies

Sysmex Corporation

Overview: Global IVD leader in hematology with strong presence across core labs and hospitals.

Key Products: 5-part/6-part analyzers; automation lines; digital morphology (with partners).

Strengths: Hematology focus & breadth, strong service network, integration with cell-image workflows.

Beckman Coulter (Danaher)

Overview: Diagnostics major with automation and informatics depth.

Key Products: Hematology analyzers integrated into automated tracks; middleware connectivity.

Strengths: Danaher operational rigor, enterprise lab contracts, interoperability with chemistry/immunoassay.

Abbott Laboratories

Overview: Broad diagnostics portfolio; extensive installed base in chemistry/immunoassay.

Key Products: Hematology systems and reagents aligned to core lab ecosystems.

Strengths: Cross-menu bundling, global distribution, strong POCT heritage.

Siemens Healthineers

Overview: Enterprise diagnostics and imaging giant with integrated lab solutions.

Key Products: Hematology within total lab automation and data platforms.

Strengths: End-to-end integration, hospital system relationships, digital/AI stack.

HORIBA Ltd.

Overview: Analytical technology leader with compact hematology systems.

Key Products: Benchtop analyzers incl. ESR on-board (2024 upgrades).

Strengths: Footprint in decentralized sites, user-friendly workflows, cost-effective models.

Mindray Medical

Overview: High-value medtech with strong growth in IVD.

Key Products: 3-part/5-part analyzers, automation modules, reagents.

Strengths: Value pricing, rapid innovation cycles, expanding global channel.

Roche Diagnostics

Overview: Leading diagnostics player with dominant chemistry/immunoassay footprint.

Key Products: Hematology solutions synergized with Roche middleware/IT.

Strengths: Enterprise access, strong oncology ecosystem, data platforms.

Bio-Rad Laboratories

Overview: Specialty diagnostics and QC leader.

Key Products: Hematology controls, QA/QC tools; specialty analyzers.

Strengths: QC credibility, research ties, specialty niche innovation.

Nihon Kohden

Overview: Clinical instrumentation specialist with lab/monitoring presence.

Key Products: Hematology analyzers for hospitals/clinics.

Strengths: Reliability, hospital channel strength, service quality.

Boule Diagnostics AB

Overview: Focused hematology company serving decentralized labs.

Key Products: Compact analyzers and reagents for routine CBCs.

Strengths: Ease of use, reagent security, affordability for emerging markets.

(Other active players in the market include: Roche, Diatron/STRATEC, PixCell, Dymind, Ortho Clinical, Drucker Diagnostics, Heska (veterinary), Agappe, Dirui, Erba Mannheim, Thermo Fisher—reagents/kits.)

Latest Announcements

Foundation Medicine & Sumitomo Pharma America (Feb 2025, U.S.)

Collaboration to accelerate investigational treatment for acute leukemia with NPM1 mutations or KMT2A rearrangements using FoundationOne® Heme—upstream signal that sustains high-acuity hematology testing demand.

BD & Babson Diagnostics (Dec 2024, U.S.)

Expansion of fingertip blood collection/testing for health systems—supports decentralized blood testing flows and POCT readiness.

Avanzanite Bioscience & Agios (Jun 2025, Europe)

Exclusive agreement to expand access to rare disease medicines—driving specialized hematology pathways needing precise CBC/platelet/coagulation monitoring.

India Blood Donation Drives (May 2025)

Sattva Group + Sankalp India Foundation drive city-wide blood donations—indirectly raising awareness and demand for hematology diagnostics.

Recent Developments

Sysmex America—XQ-320™ 3-part Differential (Mar 2025)

Extends entry segment with reliable CBC in low-volume labs, shortening TAT; strengthens laddered portfolio.

AbbVie—Venetoclax India Launch (Apr 2025)

Expands AML/CLL therapy options; oncology adoption increases pre-/on-treatment monitoring via CBC/differentials.

Novo Nordisk—Therapy Expansion (Mar 2025)

Moves beyond diabetes/obesity into blood & growth disorders—broadens hematology testing cohorts.

HORIBA—Compact ESR-Onboard Models (Jun 2024)

Reduces reflex testing by embedding ESR, improving workflow efficiency in decentralized settings.

Sysmex–CellaVision Alliance (Mar 2024)

End-to-end cell morphology + analyzer synergy; foundation for AI-assisted smear reviews.

PixCell Medical—U.S. Distribution Scale-up (Apr 2024)

HemoScreen POCT CBC expansion via leading distributors—accelerates clinic/office adoption.

Segments Covered

By Product Type

3-Part Differential Analyzers: Entry-level CBCs for smaller labs/clinics; attractive TCO.

5-Part Differential Analyzers (51% in 2024): Standard of care in hospitals; deeper WBC characterization (neutrophils, lymphocytes, monocytes, eosinophils, basophils).

6-Part & High-End: Adds immature granulocyte counts/advanced flags; fastest growth on oncology/critical care needs.

POC Hematology Analyzers: Decentralized settings; rapid triage; expanding via partnerships (e.g., PixCell).

Reagents & Consumables: Recurring revenue backbone; QC/controls critical for accreditation.

By Technology

Impedance-Based: Robust, cost-effective for routine CBC.

Flow Cytometry-Based (46% in 2024): Multiparameter cell analysis; superior specificity for complex cases.

Digital Imaging: Morphology digitization for remote review/AI assist.

AI/ML Integration (Fastest growth): Accuracy, automation, and triage gains across the workflow.

Microfluidics (Miniaturized/Portable): Low sample volumes; drives POCT and potential home-use evolution.

By Application

Complete Blood Count (CBC 58% in 2024): Cornerstone for screening/monitoring across conditions.

Hemoglobin & Hematocrit: Anemia management programs.

Reticulocyte Count: Bone marrow/therapy response insight.

White Cell Differential Count: Infection/oncology decision support.

Coagulation & Platelet Studies: Oncology/cardiovascular pathways; ties to advanced drug delivery monitoring.

By End User

Hospitals (42% in 2024): High acuity; need rapid, reliable results.

Clinical Diagnostic Labs: High-throughput hubs; automation heavy.

Research & Academics: Method development, translational studies.

Blood Banks: Donor screening, quality checks.

ASCs & Physician Offices (Fastest growth): POCT and ambulatory expansion.

By Modality

Standalone Analyzers (2024 leader): Preferred in hospitals/reference labs for throughput & accuracy.

Integrated Systems (Fastest growth): Combined with immunoassay/chemistry; single-workflow patient view.

By Region

North America: Largest share; advanced infrastructure, consolidation.

Asia Pacific: Fastest growth; infrastructure + disease burden.

Europe: Tech integration & POCT preference.

Latin America / MEA: Mix of modernization and POCT bridging access gaps.

Top 5 FAQs

1) What is the market size and growth outlook?

US$ 4.08 B (2024) → US$ 4.33 B (2025) → ~US$ 7.28 B (2034) at 5.97% CAGR (2025–2034).

2) Which region leads and which grows fastest?

North America led with 41% (2024); Asia Pacific grows fastest through 2034.

3) Which product and technology led in 2024?

5-part differential analyzers (51%) and flow cytometry–based technology (46%).

4) Who are the key end users today?

Hospitals dominate (42% in 2024); ASCs/physician offices show fastest growth (2025–2034).

5) Where is AI having the biggest impact?

Differential pre-classification, morphology imaging, QC drift detection, POCT decision support, and workflow automation, improving accuracy and reducing turnaround times and manual workload.

Access our exclusive, data-rich dashboard dedicated to the laboratory equipment sector – built specifically for decision-makers, strategists, and industry leaders. The dashboard features comprehensive statistical data, segment-wise market breakdowns, regional performance shares, detailed company profiles, annual updates, and much more. From market sizing to competitive intelligence, this powerful tool is one-stop solution to your gateway.

Access the Dashboard: https://www.towardshealthcare.com/access-dashboard

Immediate Delivery Available | Buy This Premium Research @ https://www.towardshealthcare.com/checkout/5838

Become a valued research partner with us – https://www.towardshealthcare.com/schedule-meeting

You can place an order or ask any questions, please feel free to contact us at [email protected]

Powering Healthcare Leaders with Real-Time Insights: https://www.towardshealthcare.com/healthcare-intelligence-platform

Europe Region – +44 778 256 0738

North America Region – +1 8044 4193 44

APAC Region: +91 9356 9282 04

Web: https://www.towardshealthcare.com

Find us on social platforms: LinkedIn | Twitter | Instagram | Medium | Pinterest