The global hemophilia market was US$14.34 billion in 2024, grew to US$15.29 billion in 2025, and is projected to reach US$27.27 billion by 2034 ( 6.64% CAGR, 2025–2034), led by North America (50% share, 2024) and accelerating gene therapy / non-factor approaches alongside strong R&D and supportive government initiatives.

Download the free sample and get the complete insights and forecasts report on this market @ https://www.towardshealthcare.com/download-sample/5534

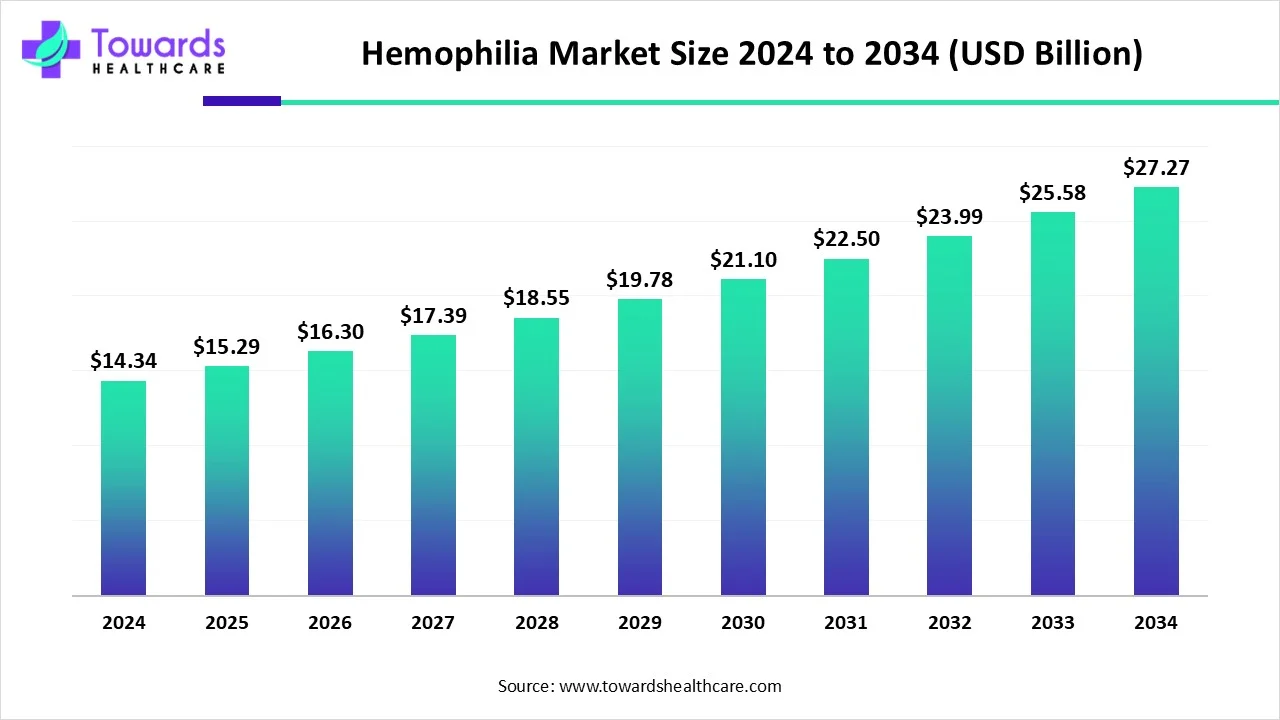

Market Size

➤2024 baseline: US$14.34B.

➤2025 step-up: US$15.29B, reflecting early adoption of long-acting factors, mAbs, and initial gene therapy launches.

➤2034 outlook: ~US$27.27B total addressable market.

➤Growth vector: 6.64% CAGR (2025–2034), outpacing historical therapy spend due to premium-priced innovations and wider diagnosis.

➤Volume vs. value: Patient counts rise (undiagnosed pool up to ~1.1M globally); value growth amplified by high-ticket therapies (e.g., US$3.5M/dose gene therapy; US$600k/year Hemlibra reference).

➤Mix shift: From factor replacement dominance (2024) toward gene therapy & monoclonals as fastest-growing buckets through 2034.

➤Channel economics: Specialty pharmacies lead 2024 revenue capture; hospital pharmacies grow fastest with increasing gene therapy and acute management integration.

➤Use pattern: Prophylaxis largest in 2024; “Cure” cohort (gene therapy) expands fastest as access broadens.

➤Type weight: Hemophilia A (80–85% of cases) anchors current spend; Hemophilia B shows the steepest growth curve (2025–2034) on gene therapy traction.

➤Regional tilt: North America 50% (2024); Europe fastest-growing on policy, diagnosis, and innovation funding; APAC scaling on awareness and capacity.

Market Trends

●Shift to non-factor therapies: Growth of bispecific mAbs (e.g., Emicizumab/Hemlibra) and TFPI-targeting agents enables subcutaneous regimens and lower treatment burden.

●Gene therapy inflection: Increasing approvals (e.g., Beqvez; list ~US$3.5M), with one-time administration targeting long-term factor expression.

●Extended half-life (EHL) factors: Fewer infusions (up to 10-day intervals) improve adherence, expanding prophylaxis penetration.

●Undiagnosed pool recognition: From 200k known to 1.1M potential patients—diagnostic lift underpins addressable market.

●Care delivery redesign: Specialty pharmacy orchestration of high-cost biologics—data-driven adherence, financing, and logistics.

●Government support: Free factor programs (e.g., Gujarat), EU/UK compensation measures, national listings (e.g., India NHM priority).

●Capital formation: Be Biopharma financing (Oct-2024) illustrates investor appetite for next-gen B-cell/gene programs.

●Academic-industry bridges: Grants (e.g., UB US$1.5M) to mitigate immunogenicity and improve tolerance.

●Access tension: Price points (Hemlibra US$600k/yr; gene therapy multi-million) pressure payers; outcomes-based models likely.

●Subcutaneous & home care: Patient-centric modalities reduce clinic time and broaden prophylaxis feasibility.

10 Deep AI Impacts / Roles

●Early detection & triage: ML on claims + lab + ultrasound flags suspected cases, shrinking the undiagnosed gap.

●Genetic variant interpretation: AI annotates F8/F9 mutations to predict severity, inhibitor risk, and candidate suitability for gene therapy.

●Personalized dosing: PK/PD models optimize factor/mAb dosing schedules to minimize bleeds with fewer units.

●Inhibitor risk forecasting: Predictive analytics stratify inhibitor formation risk in Hemophilia A vs. B to guide prophylaxis starts and immune tolerance protocols.

●Gene therapy eligibility & durability modeling: AI estimates vector response and transgene persistence, informing patient selection and follow-up cadence.

●Ultrasound image analysis: Computer vision quantifies joint health / micro-bleeds, enabling proactive interventions.

●Adherence monitoring & nudging: Behavioral AI detects non-adherence patterns; tailors reminders via specialty pharmacy apps.

●Supply chain optimization: Forecasting high-cost biologic demand across specialty/hospital pharmacies, minimizing wastage.

●Real-world evidence curation: NLP assembles outcomes from disparate EHRs to support value-based contracts for million-dollar therapies.

●Health-economic simulation: AI scenario tests for payer policy, copay assistance, and budget impact to widen access with sustainable spend.

Regional Insights

North America (50% share, 2024)

●Drivers: Mature reimbursement, high awareness, broad prophylaxis; 33,000 men with hemophilia in the U.S.

●Innovation hub: Early gene/mAb adoption; extensive specialty pharmacy networks.

●Constraint: Treatment cost—adult Hemophilia B annual therapy US$700k–800k; access disparity despite innovation.

Europe (Fastest-growing)

●Policy tailwinds: Revised UK infected blood compensation (2022–2024 payments) and broader EU support enhance patient resources.

●Data infrastructure: German Haemophilia Registry standardizes outcomes and supports research translation.

●Therapy mix shift: Accelerated move to recombinant, mAbs, gene therapy with high diagnostic capture.

Asia Pacific

●Scale opportunity: Rising diagnoses in China (2.73–3.09/100k) and India (0.9/100k); large populations expand the base.

●Government action: India NHM priority listing; expanding rural access; capacity build-out for comprehensive centers (China).

●Trajectory: Fast adoption curve as awareness and infrastructure improve.

Middle East & Africa

●Prevalence signal: Africa Hemophilia A in males 6.82/100k; rising research activity and collaborations.

●UAE 2025: Pfizer TFPI-targeting prefilled injectable launch improves convenience.

●South Africa: National rare disease initiatives target diagnosis & affordability.

Canada

●BEQVEZ approval momentum; Canadian Hemophilia Society working with provinces to expand gene therapy access.

Market Dynamics

Drivers

●Non-factor therapies improving convenience and prophylaxis adherence (e.g., Emicizumab/Hemlibra; subcutaneous dosing).

●Gene therapy programs promising long-term factor expression and reduced infusion burden.

●R&D intensity (grants, venture financing like Be Biopharma US$82M, Oct-2024).

●Government programs (e.g., Gujarat free factor injections; EU/UK supportive measures).

Restraints

●High cost of care: Hemlibra ~US$600k/yr; Hemgenix/Beqvez ~US$3.5M/dose—payer strain and access variability.

●Immunogenicity/inhibitors: Higher in Hemophilia A, complicating factor replacement strategies.

●Infrastructure gaps: Limited specialist centers in emerging markets.

Opportunities

●Undiagnosed patient conversion (up to 1.1M true prevalence).

●Monoclonal antibodies & TFPI agents, EHL factors, one-and-done therapies.

●AI-enabled care pathways to lift diagnosis, adherence, and outcomes.

●Hospital pharmacy growth with complex therapy administration and monitoring.

Top 10 Companies

Takeda Pharmaceutical Company Limited

Products: Factor replacements, plasma-derived and recombinant portfolio.

Overview: Global rare disease leader.

Strengths: Deep hemophilia heritage, broad access programs, manufacturing scale.

CSL Behring

Products: Hemgenix (gene therapy for Hemophilia B), plasma/recombinant factors.

Overview: Plasma protein therapeutics stalwart.

Strengths: First-mover credentials in gene therapy, plasma supply chain depth.

Pfizer, Inc.

Products: HYMPAVZI (EU, Nov-2024), Beqvez (FDA Apr-2024), TFPI-targeting therapy (UAE 2025).

Overview: Diversified biopharma; FY-2024 revenue US$63.6B.

Strengths: Late-stage pipeline execution, global launch muscle, once-weekly simplicity (HYMPAVZI).

Bayer AG

Products: Recombinant factors; long-standing hemophilia franchise.

Overview: Broad pharma innovator.

Strengths: Clinical experience base, safety datasets, brand equity.

BioMarin

Products: Gene therapy/rare disease innovation.

Overview: Pioneering genetic medicines.

Strengths: Platform for AAV programs, regulatory navigation in advanced therapies.

Spark Therapeutics, Inc.

Products: Gene therapy R&D in bleeding disorders.

Overview: A Roche company focused on genetic disease cures.

Strengths: Gene therapy know-how, manufacturing and development synergies.

Sanofi

Products: Expanding hemophilia options incl. Qfitlia (announced Mar-2025 positioning).

Overview: Global specialty care footprint.

Strengths: mAb expertise, scalable commercial reach across EU/US.

F. Hoffmann-La Roche Ltd.

Products: Hemlibra (Emicizumab)—subcutaneous prophylaxis.

Overview: Leader in biologics and diagnostics.

Strengths: Category-defining mAb, robust real-world evidence, broad label penetration.

Novo Nordisk A/S

Products: Recombinant factor concentrates; EHL assets.

Overview: Biologics leader with hemostasis legacy.

Strengths: Manufacturing reliability, clinician relationships in prophylaxis.

Octapharma AG

Products: Plasma-derived factors; hemophilia portfolio.

Overview: Swiss plasma specialist; €3.466B sales in 2024 (+6.1%).

Strengths: Vertical plasma integration, steady global growth and supply.

Latest Announcements

Sanofi (Mar-2025): Positioned Qfitlia as a next-generation prophylaxis option emphasizing effective bleed prevention, infrequent dosing, and simple administration to lower treatment burden across diverse patient needs.

UAE (2025): Pfizer launched a prefilled TFPI-targeting injectable, the first of its kind in the country, improving convenience and access.

Recent Developments

Nov-2024 (EU): Pfizer’s HYMPAVZI approved for Hemophilia A or B without inhibitors (≥12 years, ≥35 kg), once-weekly dosing with minimal preparation.

Apr-2024 (US): FDA authorized Pfizer’s Beqvez for Hemophilia B; list price ~US$3.5M.

Oct-2024: Be Biopharma raised US$82M to advance a Hemophilia B gene therapy into Phase I/II.

Jun-2023: UB researcher awarded US$1.5M for work on immune tolerance in hemophilia therapy.

Jul-2023 (Taiwan): Chugai launched Hemlibra for Hemophilia A patients without inhibitors.

Segments Covered

By Type

Hemophilia A (dominant, 2024; 80–85% of cases)

Epidemiology & burden

●Drives the bulk of prophylaxis spend due to higher prevalence and higher inhibitor incidence than Hemophilia B (notably in severe A).

●Large undiagnosed pool contributes to latent demand; moving patients from episodic to prophylaxis is the biggest near-term value unlock.

Therapy mix & standard of care

●Factor VIII replacement remains foundational; extended half-life (EHL) variants reduce infusion frequency, enabling tighter bleed control.

●Monoclonal antibodies (e.g., Emicizumab) shift care to subcutaneous administration, lowering treatment burden and improving adherence.

Inhibitor management

●Higher inhibitor rates in A trigger immune tolerance induction (ITI) pathways and increase reliance on non-factor options for bleed prevention.

Pipeline & access

●Active innovation in gene therapy for sustained FVIII expression; payer models (risk-sharing, outcomes-based) will shape uptake given high upfront costs.

Operational implications

●More home-based, subcutaneous regimens; specialty pharmacies centralize training, adherence coaching, and cold-chain integrity.

●Imaging (ultrasound) and joint health scoring support earlier intervention and outcome tracking.

Hemophilia B (fastest growth 2025–2034)

Epidemiology profile

●Lower prevalence than A (with severe B estimated at ~1.5/100,000 male population in your data), but disproportionately high growth from gene therapy.

Growth flywheel

●One-time gene therapy for Hemophilia B catalyzes market acceleration: rapid bleed reduction, lowered ongoing infusion needs, and clinic capacity freed.

Adoption considerations

●Eligibility screening (liver function, prior vector exposure), post-infusion monitoring, and center readiness are critical to scale.

Economic dynamics

●High upfront price tags shift economics from continuous spend to front-loaded capex, prompting outcomes-linked reimbursement and longitudinal registries.

By Treatment Type

Prophylaxis (largest, 2024)

Clinical rationale

●Early prophylaxis in children is the gold standard, continued into adulthood to prevent cumulative joint damage; more rigorous regimens nearly eliminate joint bleeds.

Tools & modalities

●EHL factors for fewer infusions; mAbs for subcutaneous convenience; broader home therapy penetration.

Program design

●Individualized, PK-guided dosing; adherence programs via specialty pharmacies; ultrasound-based joint surveillance to verify “silent bleed” suppression.

Impact

●Better quality of life, reduced ED visits, and improved long-term musculoskeletal outcomes—key proof points for payer renewals.

“Cure” (fastest-growing; gene therapy)

Mechanism & promise

●AAV-based administration aims for durable endogenous factor production, reducing or eliminating exogenous replacement.

Access & economics

●High upfront list prices balanced by potential lifetime savings; value-based contracts and registries track durability and re-intervention rates.

Clinical operations

●Centralized infusion at qualified sites, structured follow-up (liver enzymes, factor levels), and standardized adverse-event reporting.

On-demand (episodic)

Role & use cases

●Continues for milder phenotypes, newly diagnosed patients, and access-limited geographies; essential for breakthrough bleeds and procedures.

Pathway

●Rapid access to factor/bypass agents; escalation protocols and transition planning toward prophylaxis where feasible.

By Therapy

Factor Replacement Therapy (major share, 2024)

Archetypes

●Plasma-derived and recombinant factors (VIII/IX); EHL designs extend dosing intervals (e.g., toward ~10 days for some use cases in your data).

Clinical outcomes

●Where accessible and affordable, life expectancy approximates the general male population; robust real-world data support safety and efficacy.

Complexities

●Inhibitors complicate Hemophilia A management; may require ITI or switch to non-factor prophylaxis.

●Gene Therapy & Monoclonal Antibodies (fastest-growing)

Monoclonals

●Bispecifics (e.g., Emicizumab) mimic FVIII function; APC-pathway targeting mAbs protect FVa from proteolysis; TFPI-targeting agents reduce natural anticoagulation—each improving hemostasis with subcutaneous or less frequent dosing.

Gene therapy

●Aims for one-and-done mitigation of bleeding; requires eligibility workup, post-infusion monitoring, and payer-approved centers.

Desmopressin & Fibrin Sealants (adjuncts)

Use cases

●Procedure-related prophylaxis, select mild cases, and local hemostasis; not a replacement for long-term bleed prevention in severe disease.

By Distribution Channel

Specialty Pharmacies (largest, 2024)

Core services

●Prior authorization navigation, copay/assistance programs, cold-chain logistics, patient training, refill synchronization, and adherence analytics.

Data advantage

●Centralized dispensing enables outcomes tracking (bleed rates, missed doses) that supports renewals and value-based arrangements.

Patient experience

●Home delivery, subcutaneous self-administration onboarding, and 24/7 clinical support reduce clinic load and improve continuity.

Hospital Pharmacies (fastest growth)

Why accelerating

●Gene therapy administration (one-time IV) and management of acute bleeds and complex cases are hospital-anchored.

Workflow

●Therapy acquisition and inventory controls, infusion scheduling, post-infusion monitoring protocols, coordination with hematology teams, and documentation for payer outcomes.

Network role

●Serve as regional hubs (centers of excellence) that train community sites and link to registries.

By Region

North America (leadership at 50% share in 2024)

What drives leadership

●Mature reimbursement, high diagnosis and prophylaxis rates, deep specialty pharmacy networks, early adoption of mAbs/gene therapy.

Pressure points

●High cost of care (e.g., yearly spend for adult Hemophilia B in the U.S. ~US$700k–800k in your data) and affordability gaps despite clinical progress.

System design

●Hemophilia treatment centers, case-management programs, and outcomes data underpin payer negotiations.

Europe (fastest-growing)

Policy & data

●Registries (e.g., Germany) elevate data quality; UK compensation actions improve patient support.

Clinical adoption

●Strong movement toward recombinant factors, mAbs, and gene therapy as diagnostic capture remains high.

Access model

●National/HTA frameworks emphasize cost-effectiveness and real-world outcomes, favoring modalities that reduce lifetime bleed burden.

Asia Pacific

Scale runway

●Rising diagnosis and infrastructure investment in China and India expand the treated base; inclusion on India’s NHM priority list elevates funding and awareness.

Capacity build-out

●Comprehensive management centers, independent diagnostic capability, and rural outreach broaden access.

Trajectory

●From episodic to structured prophylaxis and selective adoption of subcutaneous and gene options as systems mature.

Latin America / Middle East & Africa

Frameworks & initiatives

●National rare disease initiatives and targeted launches (e.g., UAE TFPI-targeting prefilled injectable) improve convenience and access.

Epidemiology signals

●In Africa, reported Hemophilia A prevalence in males ~6.82/100,000 (in your data) underscores unmet need.

Access path

●Tender-based procurement, strengthening specialty centers, and partnerships with patient organizations to sustain supply and training.

Canada (added depth from your notes)

Gene therapy momentum

●Positive regulatory steps (e.g., BEQVEZ) with the Canadian Hemophilia Society collaborating to speed equitable access across provinces.

Operationalization

●Provincial funding decisions, center accreditation, and longitudinal monitoring are key to durable outcomes.

Top 5 FAQs

-

What is the current market size and outlook?

US$14.34B (2024) → US$15.29B (2025) → US$27.27B (2034) at 6.64% CAGR (2025–2034). -

Which region leads and which grows fastest?

North America led with 50% share in 2024; Europe is expected to grow the fastest. -

Which type and therapy dominate today?

Hemophilia A and factor replacement dominated 2024; gene therapy & monoclonals will grow fastest ahead. -

What’s the biggest access barrier?

Cost: examples include Hemlibra US$600k/year and gene therapy US$3.5M/dose. -

What recent approvals/launches matter most?

HYMPAVZI (EU, Nov-2024), Beqvez (US, Apr-2024), TFPI prefilled injectable (UAE, 2025); financing for Be Biopharma supports pipeline depth.

Access our exclusive, data-rich dashboard dedicated to the therapeutic area sector – built specifically for decision-makers, strategists, and industry leaders. The dashboard features comprehensive statistical data, segment-wise market breakdowns, regional performance shares, detailed company profiles, annual updates, and much more. From market sizing to competitive intelligence, this powerful tool is one-stop solution to your gateway.

Access the Dashboard: https://www.towardshealthcare.com/access-dashboard

Immediate Delivery Available | Checkout this Premium Research Report @ https://www.towardshealthcare.com/checkout/5534

Become a valued research partner with us – https://www.towardshealthcare.com/schedule-meeting

You can place an order or ask any questions, please feel free to contact us at [email protected]

Powering Healthcare Leaders with Real-Time Insights: https://www.towardshealthcare.com/healthcare-intelligence-platform

Europe Region – +44 778 256 0738

North America Region – +1 8044 4193 44

APAC Region: +91 9356 9282 04

Web: https://www.towardshealthcare.com

Find us on social platforms: LinkedIn | Twitter | Instagram | Medium | Pinterest