Latin America life science market was US$4.49 billion in 2024, is set to reach US$4.90 billion in 2025, and US$12.05 billion by 2034 at a 10.38% CAGR, led by Brazil and powered by biotech, biopharma, and digital health adoption.

Download this Free Sample Now and Get the Complete Report and Insights of this Market Easily @ https://www.towardshealthcare.com/download-sample/6289

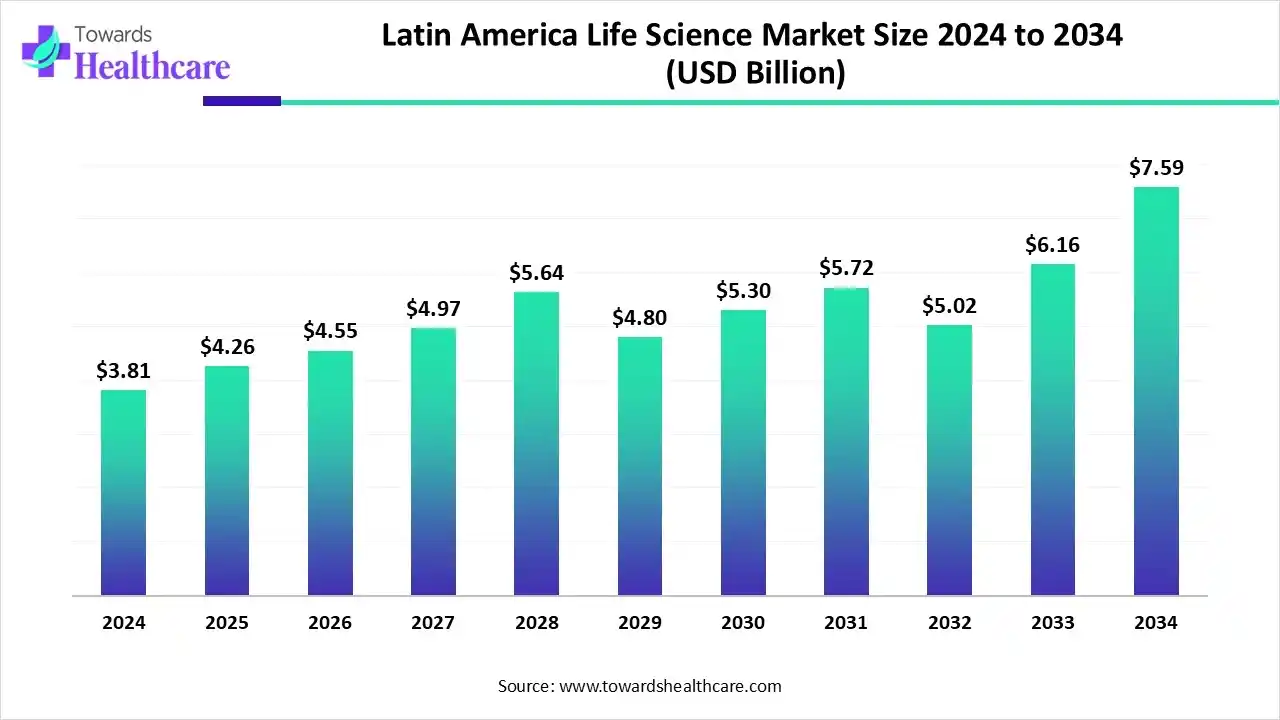

Market size

➤ Baseline & near-term: 2024 value US$4.49B; 2025 value US$4.90B (+9.1% YoY), reflecting momentum from R&D spending, diagnostics demand, and public programs.

➤Long-term trajectory: Reaching US$12.05B by 2034, implying more than a 2.6× expansion over 2024 as biologics, vaccines, and CDMO/CRO services scale.

➤Growth engine: Biopharmaceuticals remained the largest 2024 component (incl. small molecules, biologics, biosimilars, cell & gene therapy), supported by manufacturing expansions and partnerships.

➤Technology tilt: Biotechnology led in 2024, while Digital health & AI shows the fastest growth ahead (informatics, lab automation, clinical software).

➤Product mix: Small molecules dominated 2024 revenue; biologics are the fastest rising on the back of vaccines, mAbs, and engineered proteins.

➤End-market pull: Pharma & biotech companies were the largest 2024 buyers; academic & research institutes are the fastest-growing as grants, trials, and lab upgrades rise.

➤Therapy focus: Oncology held the top 2024 share; rare diseases & orphan drugs poised for quickest expansion with incentives and precision modalities.

➤Pipeline maturity: Phase II dominated 2024 revenues (proof-of-concept concentration), while preclinical grows fastest as early pipelines widen.

➤Regional footing: Brazil led 2024 revenue; Mexico & Chile projected fastest CAGR on startup activity, FDI, and lab infrastructure.

Market trends

Biopharma primacy: Large molecules, biosimilars, and advanced delivery systems keep biopharmaceuticals as 2024’s largest component; biologics/CGT investments accelerate.

Digital acceleration: Healthcare IT & digital solutions expected to post the fastest CAGR, riding bioinformatics, lab systems, e-trials, and precision workflows.

Biotech backbone: Biotechnology led in 2024 due to genomics/proteomics integration, disease modeling, and scalable biologics production.

Precision health: Personalized/precision medicine surges with companion diagnostics, genomic stratification, and targeted therapies.

Trials expansion: Diverse patient pools and improving oversight make LATAM a growing clinical trial hub (Brazil, Mexico, Argentina).

Policy catalysis: Brazil’s CEIS push—PDPs (GM/MS 4,472/2024) and PDIL (GM/MS 4,473/2024)—invited projects in 2024; first selections expected in 2025.

Data flows & privacy: EU–Brazil GDPR adequacy assessment (Sep 2025) could streamline research data exchange once approved.

Diagnostics demand: Preventive care uptake and public health programs expand diagnostics and vaccines consumption.

Value-chain deepening: CRO/CDMO footprints widen as sponsors localize development and manufacturing steps.

Global context: The global life sciences market rises from US$98.63B (2025) to US$269.56B (2034) at 11.82% CAGR, offering export and partnership tailwinds.

Ten deep roles of AI in LATAM life sciences

Target discovery & prioritization: Multi-omics integration to rank targets; cuts false positives, improves pipeline quality.

In-silico screening & design: Generative models propose small molecules/biologics; narrows wet-lab iterations.

Bioprocess optimization: AI tunes upstream/downstream biomanufacturing (feeds, yields, batch deviations) for biologics and vaccines.

Adaptive clinical trials: AI-assisted site selection, protocol optimization, and real-time enrollment forecasting reduce cycle times.

Virtual/hybrid trials: Remote monitoring and ePRO analytics expand reach to rural/under-served populations while lowering costs.

Diagnostics intelligence: Imaging and assay interpretation (triage, risk scoring) increases accuracy and throughput in oncology/infectious disease.

Supply-chain resilience: Predictive logistics and demand sensing mitigate stock-outs across fragmented LATAM distribution networks.

Regulatory/QA automation: NLP accelerates dossier assembly, traceability, and pharmacovigilance signal detection to meet ANVISA and regional rules.

Personalized medicine: Cohort stratification, companion Dx algorithms, and response prediction drive payer-friendly outcomes.

R&D portfolio strategy: Scenario models balance risk/return across preclinical → Phase II heavy pipelines common in the region.

Regional insights

Brazil (market leader, 2024)

Industrial base: Strong pharma manufacturing, vaccine institutes (e.g., Butantan), and rising biologics capacity anchor scale.

Policy lift: CEIS PDP/PDIL (2024) programs aim to localize innovation and supply; AREE accelerates ANVISA approvals.

Demand profile: Large patient population fuels oncology, vaccines, and precision therapies; digital health pilots expand.

Mexico (fastest-growing cohort)

Startup vitality & FDI: New biotech ventures and global partnerships strengthen discovery and clinical ops.

Infrastructure: Lab and trial capacity upgrades broaden Phase I–III coverage.

Market access: Modernization efforts improve device and therapeutic adoption pathways.

Chile (fastest-growing cohort)

Research orientation: Academic–industry collaboration widens translational pipelines in diagnostics and biotech.

Digital adoption: Strong uptake of informatics and tele-health tools suits geography and dispersion.

Capital efficiency: Lean ecosystems accelerate pilot programs and niche biologics.

Argentina

Clinical trial node: Oncology and infectious-disease trials benefit from experienced sites.

Manufacturing pockets: Selective strengths in finished dose and sterile lines; focus on export readiness.

Talent base: Scientific training supports CRO/CDMO expansion.

Market dynamics

Drivers

Structural growth: US$4.49B (2024) → US$12.05B (2034) at 10.38% CAGR; biopharma, biotech, diagnostics core to expansion.

Policy & programs: Brazil’s PDP/PDIL (2024), ANVISA AREE concept, and potential EU–Brazil adequacy streamline R&D and data exchange.

Digital & AI: Fastest-growing lane, enabling bioinformatics, CTMS/LIMS, and remote trials.

Restraints

Infrastructure gaps: Uneven lab/clinical capacity outside top metros.

Reimbursement complexity: Fragmented payer systems slow uptake of high-cost therapies.

Regulatory heterogeneity: Country-specific variances complicate multi-nation launches.

Opportunities

Biologics & vaccines: Fastest product growth; partnerships with institutes and CDMOs.

Rare disease/orphan: Incentives + precision platforms = rapid niche growth.

CRO/CDMO scale-up: Sponsors seek local execution across preclinical → Phase II concentrations.

Challenges

Workforce depth: Scaling GMP, GCP, and AI/bioprocess skills.

Supply-chain resilience: Cold chain and cross-border logistics for biologics.

Data governance: Harmonizing privacy/security while enabling research collaboration.

Top 10 companies

Biomérieux Latin America

Overview: Diagnostics specialist focused on infectious disease and clinical testing.

Products: Microbiology analyzers, immunoassays, molecular Dx platforms.

Strengths: Hospital footprint, quality systems, syndromic testing know-how.

Fiocruz – Oswaldo Cruz Foundation

Overview: Brazilian public health powerhouse spanning research, manufacturing, and policy support.

Products: Vaccines, diagnostics, reference labs, public health programs.

Strengths: Scale, government linkage, epidemic response capacity.

Cristália

Overview: Brazilian pharma covering branded, generics, and hospital products.

Products: Injectables, anesthetics, specialty medicines.

Strengths: Manufacturing depth, hospital channels, regulatory familiarity.

Laboratorios Liomont

Overview: Mexican pharma with branded and generic portfolios.

Products: Therapeutics across primary care and specialty lines.

Strengths: National reach, cost-effective manufacturing, partner readiness.

Laboratorios Silanes

Overview: Mexican company with focus on metabolic and chronic therapies.

Products: Diabetes and cardiovascular medications, injectables.

Strengths: Specialty expertise, adherence programs, clinician relations.

Grupo Insud

Overview: Regional life sciences group spanning pharma, biotech, and related services.

Products: Prescription drugs, biologics initiatives, supply chain assets.

Strengths: Diversified footprint, cross-border operations, deal-making.

Medix

Overview: Pharma player active in metabolic disorders and wellness.

Products: Obesity/weight-management, endocrine therapies.

Strengths: Niche leadership, patient support programs, brand equity.

EMS Pharma

Overview: Major Brazilian pharma producing generics, branded, and specialty.

Products: Wide therapeutic portfolio; R&D support services.

Strengths: Scale economics, distribution power, R&D–manufacturing integration.

Instituto Butantan

Overview: Leading Brazilian institute for vaccines, antivenoms, and biopharma research.

Products: Vaccines (incl. public immunization), biotherapeutics, antivenoms.

Strengths: Public health mission, tech transfer, biologics capacity.

Ache Laboratórios

Overview: Brazilian pharma across generics, branded, OTC, and specialty.

Products: Broad Rx/OTC lines; R&D and regulatory services.

Strengths: Portfolio breadth, quality compliance, go-to-market reach.

(Alternate regional integrator: Bago Group—distribution/logistics, clinical trial support, regulatory services.)

Latest announcements & recent developments

Ache Laboratórios (May 2025): Reiterated focus on generics, branded, OTC, specialty plus R&D/regulatory services, signaling continued pipeline and line-extension activity.

Clarivate + Global Health Intelligence (Apr 2024): Launched LatAm medtech tracking platform across six countries, aiding manufacturers with validated market/device data.

Brazil policy (2024): PDPs (GM/MS 4,472/2024) and PDIL (GM/MS 4,473/2024) invited project proposals (deadline Sep 30, 2024); first selections in 2025 expected and further windows planned.

EU–Brazil data flows (Sep 2025): GDPR adequacy evaluation commenced; ANPD exploring reciprocal adequacy—aimed at frictionless EU–Brazil research/business data exchange upon approval.

Segments covered

Top 5 FAQs (with embedded data)

Q1. What is the market size and growth outlook?

A. US$4.49B (2024) → US$4.90B (2025) → US$12.05B (2034) at 10.38% CAGR.

Q2. Which country led in 2024, and who grows fastest?

A. Brazil led 2024 revenue; Mexico & Chile are projected to grow at the fastest CAGR.

Q3. Which components and technologies dominate?

A. Biopharmaceuticals led components in 2024; biotechnology led technologies; digital health & AI will grow fastest.

Q4. What product types lead and which are rising fastest?

A. Small molecules dominated 2024; biologics will post the fastest growth.

Q5. Who are key players?

A. Biomérieux LATAM, Fiocruz, Cristália, Liomont, Silanes, Grupo Insud, Medix, EMS Pharma, Instituto Butantan, Ache Laboratórios (plus Bago Group among ecosystem leaders).

Access our exclusive, data-rich dashboard dedicated to the life sciences sector– built specifically for decision-makers, strategists, and industry leaders. The dashboard features comprehensive statistical data, segment-wise market breakdowns, regional performance shares, detailed company profiles, annual updates, and much more. From market sizing to competitive intelligence, this powerful tool is one-stop solution to your gateway.

Access the Dashboard: https://www.towardshealthcare.com/access-dashboard

Immediate Delivery Available | Checkout this Premium Research Report @ https://www.towardshealthcare.com/checkout/6289

Become a valued research partner with us – https://www.towardshealthcare.com/schedule-meeting

You can place an order or ask any questions, please feel free to contact us at [email protected]

Powering Healthcare Leaders with Real-Time Insights: https://www.towardshealthcare.com/healthcare-intelligence-platform

Europe Region – +44 778 256 0738

North America Region – +1 8044 4193 44

APAC Region: +91 9356 9282 04

Web: https://www.towardshealthcare.com

Find us on social platforms: LinkedIn | Twitter | Instagram | Medium | Pinterest