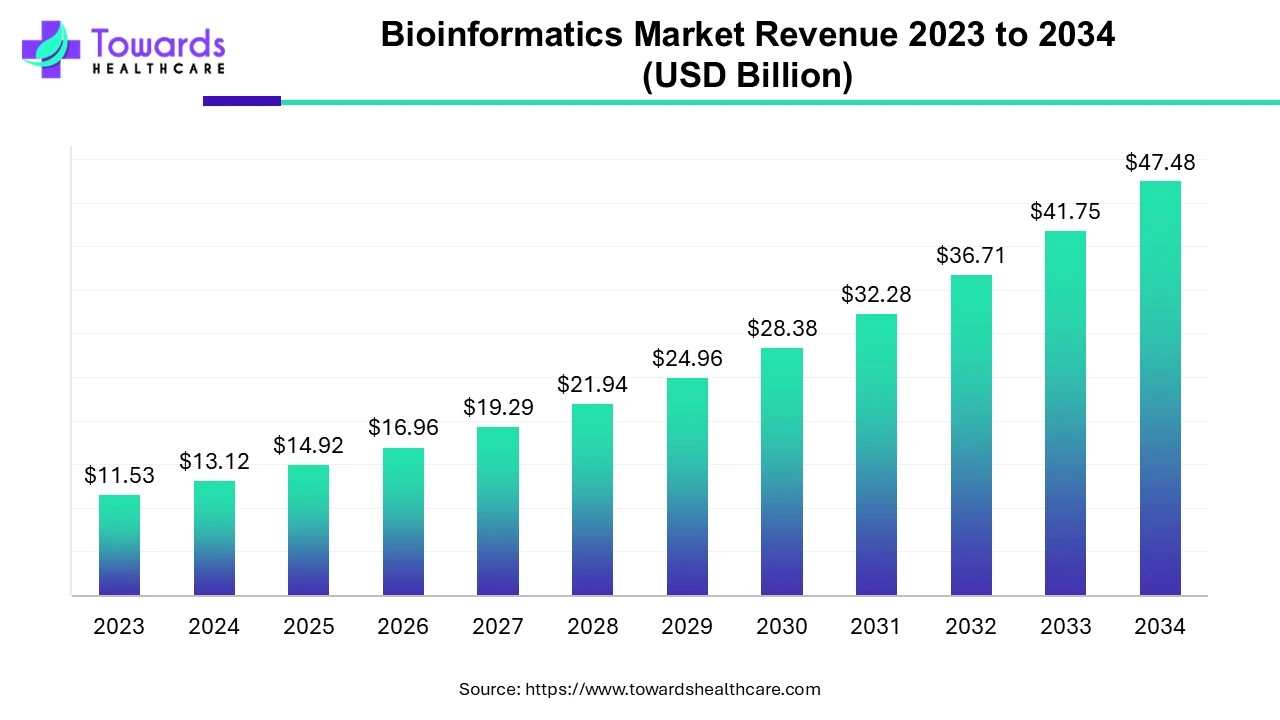

The global bioinformatics market was US$ 11.53B in 2023 and is projected to reach US$ 47.48B by 2034 at a 13.73% CAGR (2024–2034), propelled by expanding genomics/proteomics programs, drug discovery needs, and steady tech advances.

Download this Free Sample Now and Get the Complete Report and Insights of this Market Easily @ https://www.towardshealthcare.com/checkout/5337

Market Size

Base & outlook (constant USD):

➣2023: US$ 11.53B (given)

➣2024 (implied base for CAGR): US$ 13.11B

➣2034: US$ 47.48B (given)

Select year projections (at 13.73% CAGR from 2024):

➣2025: US$ 14.92B

➣2027: US$ 19.29B

➣2029: US$ 24.95B

➣2031: US$ 32.28B

➣2033: US$ 41.75B

By product family (qualitative size dynamics):

➣Biocontent management (dominated 2023): growing on the back of unified platforms for generating/storing/delivering complex biological data.

➣Bioinformatics services (fastest growth): end-to-end data lifecycle management (intake → integrity → use), saving scientist time via expert bioinformaticians.

➣Bioinformatics platforms (steady expansion): sequence analysis/alignment/manipulation and structural/functional suites underpin day-to-day workflows.

➣Customer spending motions: increasing multiyear service contracts, managed analysis pipelines, and cloud data-ops alongside on-prem high-compute nodes where needed.

➣Deal sizes: moving from department-level tool buys to enterprise-wide frameworks attached to omics programs and translational medicine initiatives.

Market Trends

➣Genomic surveillance mainstreaming: WHO (Sept 2024) workshop advanced genomic surveillance/data-sharing/bioinformatics for respiratory viruses within GISRS, strengthening national–global readiness.

➣Services deepening: Almaden Genomics (Sept 2024) launched Data Management & Informatics Services to tackle data scale and complexity for pharma/biotech/academia.

➣Sequencing economics shifting: Inocras (Aug 2024) offering WGS on Ultima Genomics UG 100 highlights a push toward lower-cost, high-throughput WGS with custom bioinformatics stacks.

➣Large-scale clinico-genomic integration: Genomics England (Jan 2024) built a pipeline integrating 13,880 tumor WGS with matched clinical data to resolve germline & somatic drivers influencing prognosis.

➣CRISPR accuracy via AI: Würzburg Helmholtz Institute (Jan 2024) improved CRISPR efficacy prediction using ML-based data integration.

➣AI/ML pervasiveness: NLP literature mining, neural nets for structure prediction, and ML-assisted variant calling are accelerating insight cycles.

➣Omics expansion: Favorable government support for genomics, proteomics, metabolomics, transcriptomics keeps widening downstream informatics demand.

➣Enterprise data governance: Rising emphasis on quality, lineage, and FAIR data across pipelines to enable regulated clinical use.

➣Cloud-first workflows: Scale-out compute + elastic storage for cohort-scale analyses; hybrid architectures for sensitive datasets.

➣From ‘sick care’ to ‘health care’: Industry leaders (e.g., Li Qing’s remarks) emphasize genomics moving upstream into prevention & population health.

10 Deep AI Impacts / Roles in Bioinformatics

➣Variant discovery & prioritization: ML-enhanced variant calling, pathogenicity scoring, and phenotype-genotype linking for faster diagnostics.

➣Protein structure & function inference: Deep models accelerate structure prediction, binding-site mapping, and protein-protein interaction insights for target validation.

➣Drug discovery acceleration: AI for virtual screening, de-novo design, ADMET prediction, and multi-parameter optimization, cutting cycle times.

➣CRISPR guide optimization: ML models predict on-target efficiency and off-target risk to design safer, more effective edits.

➣NLP literature intelligence: Automated extraction of entities/relations from millions of papers—hypothesis generation and evidence aggregation at scale.

➣Multi-omics fusion: Graph and representation learning integrate genomics–transcriptomics–proteomics–metabolomics to reveal disease mechanisms.

➣Clinical decision support: AI-assisted molecular tumor boards: actionable variants, trial matching, and therapy ranking with transparent evidence trails.

➣Population genomics & surveillance: Streaming analytics for outbreak detection, lineage tracking, and antimicrobial resistance patterning.

➣Data ops & automation: Active learning and AutoML to tune pipelines, reduce manual QC, and maintain performance as data drifts.

➣Privacy-preserving analytics: Federated learning and privacy tech to analyze distributed cohorts without centralizing PHI.

Regional Insights

North America — 2023 leader

➣Policy & funding backbone: Support from NIST, NCTR, NCIP and others sustains standards, reference datasets, and oncology informatics programs.

➣Clinical adoption: Mature payer/provider ecosystems support WGS/NGS in oncology and rare disease, driving demand for validated pipelines.

➣Talent & infrastructure: Dense clusters of bioinformaticians, cloud hyperscalers, and specialized HPC centers.

➣Canada momentum: Oct 2023: US$ 15M toward a Pan-Canadian Genome Library to unlock genomic medicine value chains.

Asia–Pacific — fastest growth ahead

➣China: World’s #2 biopharma market; rapid advances in gene therapy/genome editing spur local sequencing and informatics capacity.

➣India & Japan: Attractive for investment due to demographics, R&D incentives, and infrastructure scale-up.

➣Japan (2022): “Strengthening Drug Discovery Venture Ecosystem Project” (~¥300B) catalyzes startups and platform tooling.

➣Healthcare expansion: Public and private initiatives upgrading data standards, biobanks, and training in clinical bioinformatics.

Europe

➣Public-private consortia: Pan-European programs harmonize standards (e.g., cancer & rare disease genomics) and boost cross-border data utility.

➣Regulatory rigor: Strong data-protection frameworks stimulate growth in privacy-preserving bioinformatics and audit-ready pipelines.

Latin America / Middle East & Africa

➣Early-stage but rising: Focus on capacity building, regional reference labs, and cloud-hosted platforms to bypass capex barriers.

➣Adoption gating factors: Budget constraints and skilled-talent shortages—offset via collaborations and managed services.

Market Dynamics

Drivers:

➣Surge in genomic/proteomic research and novel drug discovery;

➣Technological advancements in sequencing and analytics;

➣Supportive policies for omics (genomics, proteomics, metabolomics, transcriptomics).

Restraints:

➣Computational complexity of large-scale datasets;

➣High infrastructure costs (HPC, storage) limiting LMIC uptake.

Challenges:

➣Shortage of trained bioinformaticians;

➣Interoperability & data quality issues across disparate sources.

Opportunities:

➣Expansion of bioinformatics services (fastest-growing product segment);

➣Increasing genomic surveillance (e.g., WHO/GISRS), national genome libraries, and hospital molecular programs;

➣Cloud-first deployments, ML-native pipelines, and privacy-preserving analytics.

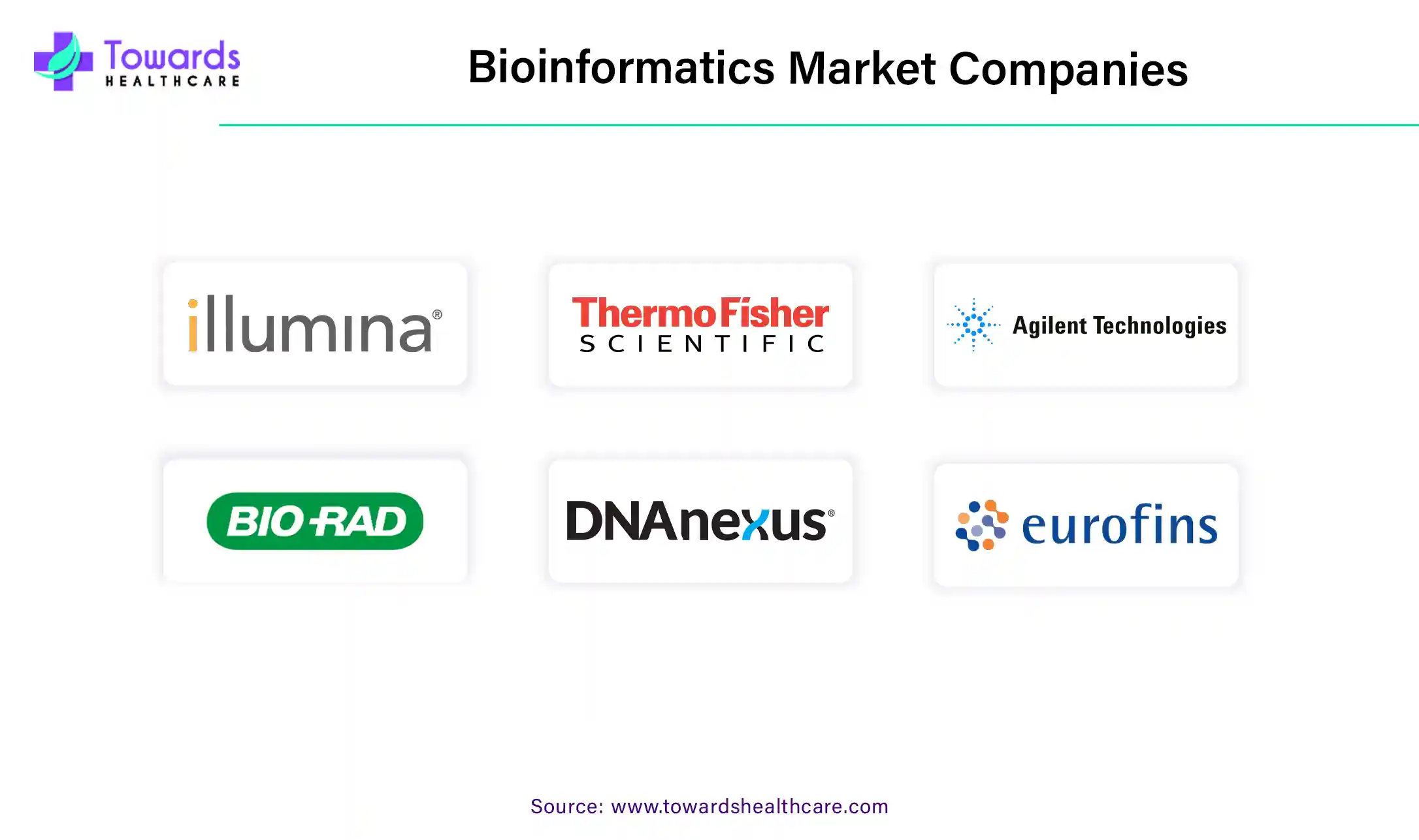

Top 10 Leading Bioinformatics Market Companies

Illumina, Inc.

Products: Sequencers; analysis stacks (e.g., alignment/variant calling).

Overview: Core technology vendor anchoring WGS/NGS workflows.

Strength: Massive installed base; end-to-end ecosystem from reagents to informatics.

Thermo Fisher Scientific

Products: Sequencers (e.g., semiconductor-based), sample-to-answer kits, analysis software.

Overview: Broad life-science portfolio integrated with informatics.

Strength: Enterprise reach, regulated-market expertise.

Agilent Technologies, Inc.

Products: Omics instruments and informatics toolchains.

Overview: Strong in analytical instrumentation with bioinformatics overlays.

Strength: Data quality, integration with lab ecosystems.

QIAGEN

Products: CLC Genomics-style software, sample prep/NGS solutions.

Overview: Widely used analysis suites in clinical/academic labs.

Strength: Usability, curated workflows, and clinical orientation.

Bio-Rad Laboratories, Inc.

Products: Genomics/proteomics tools with supporting analysis software.

Overview: Proteomics and gene expression pillars.

Strength: Assay depth; QC-focused informatics.

DNAnexus

Products: Cloud bioinformatics platform (secure data management, pipelines).

Overview: Cohort-scale, compliance-ready analysis hub.

Strength: Scalability, security, collaboration at population-genomics scale.

Waters Corporation

Products: Mass-spec/LC with informatics for proteomics/metabolomics.

Overview: Analytical chemistry leader enabling systems biology.

Strength: High-fidelity data + domain toolchains.

PerkinElmer (Revvity)

Products: Omics/analytics software and services.

Overview: Instruments + informatics across discovery to diagnostics.

Strength: Broad modality coverage, integration services.

Eurofins Scientific

Products: Contract bioinformatics & lab services.

Overview: Global network for sequencing/analysis outsourcing.

Strength: Scale, turnaround options, compliance.

Fios Genomics

Products: Specialist bioinformatics services (multi-omics, study design → analysis).

Overview: CRO-style analytics partner to pharma/biotech/academia.

Strength: Expert benches, bespoke pipelines.

Latest Announcements

➣WHO (Sept 2024): Workshop to elevate genomic surveillance, data sharing, and bioinformatics analysis for respiratory viruses within GISRS—expected to expand demand for validated, shareable pipelines in public health.

➣Almaden Genomics (Sept 2024): Launch of Data Management & Informatics Services to resolve pain points in data ingestion, stewardship, and analysis operations for researchers and industry.

➣Inocras (Aug 2024): Offering WGS on Ultima Genomics UG 100, indicating growing ecosystem choices for high-throughput, cost-efficient sequencing with tailored informatics.

➣Leadership perspective (Li Qing): Emphasis on genomics transitioning from reactive care to proactive health care—supporting population-scale programs.

Recent Developments

➣Genomics England (Jan 2024): Built a pipeline integrating 13,880 tumor WGS with matched clinical data; surfaced somatic & germline variants tied to prognosis—template for clinic-grade, large-cohort analytics.

➣Würzburg Helmholtz Institute (Jan 2024): ML approach using data integration + AI to improve CRISPR efficacy prediction—supports design-time decisions in gene editing.

Top 5 FAQs

-

What is the market size and growth rate?

US$ 11.53B (2023) → US$ 47.48B (2034) at 13.73% CAGR (2024–2034). -

Which product area led in 2023?

Biocontent management led, driven by unified platforms for complex data generation–storage–delivery. -

Which product area will grow fastest?

Bioinformatics services, covering intake, integrity, analysis, and expert interpretation across the data lifecycle. -

Which regions are most important?

North America led in 2023 (policy/funding, infrastructure, talent; Canada’s US$ 15M genome library in Oct 2023). Asia–Pacific is the fastest-growing (China’s biopharma scale; Japan’s ¥300B venture program; India’s expanding infrastructure). -

What are the main restraints?

Computational complexity, high infrastructure costs, and shortage of trained professionals, particularly in LMICs.

Access our exclusive, data-rich dashboard dedicated to the biotechnology market – built specifically for decision-makers, strategists, and industry leaders. The dashboard features comprehensive statistical data, segment-wise market breakdowns, regional performance shares, detailed company profiles, annual updates, and much more. From market sizing to competitive intelligence, this powerful tool is one-stop solution to your gateway.

Access the Dashboard: https://www.towardshealthcare.com/access-dashboard

Immediate Delivery Available | Checkout this Premium Research Report @ https://www.towardshealthcare.com/checkout/5337

Become a valued research partner with us – https://www.towardshealthcare.com/schedule-meeting

You can place an order or ask any questions, please feel free to contact us at [email protected]

Powering Healthcare Leaders with Real-Time Insights: https://www.towardshealthcare.com/healthcare-intelligence-platform

Europe Region – +44 778 256 0738

North America Region – +1 8044 4193 44

APAC Region: +91 9356 9282 04

Web: https://www.towardshealthcare.com

Find us on social platforms: LinkedIn | Twitter | Instagram | Medium | Pinterest