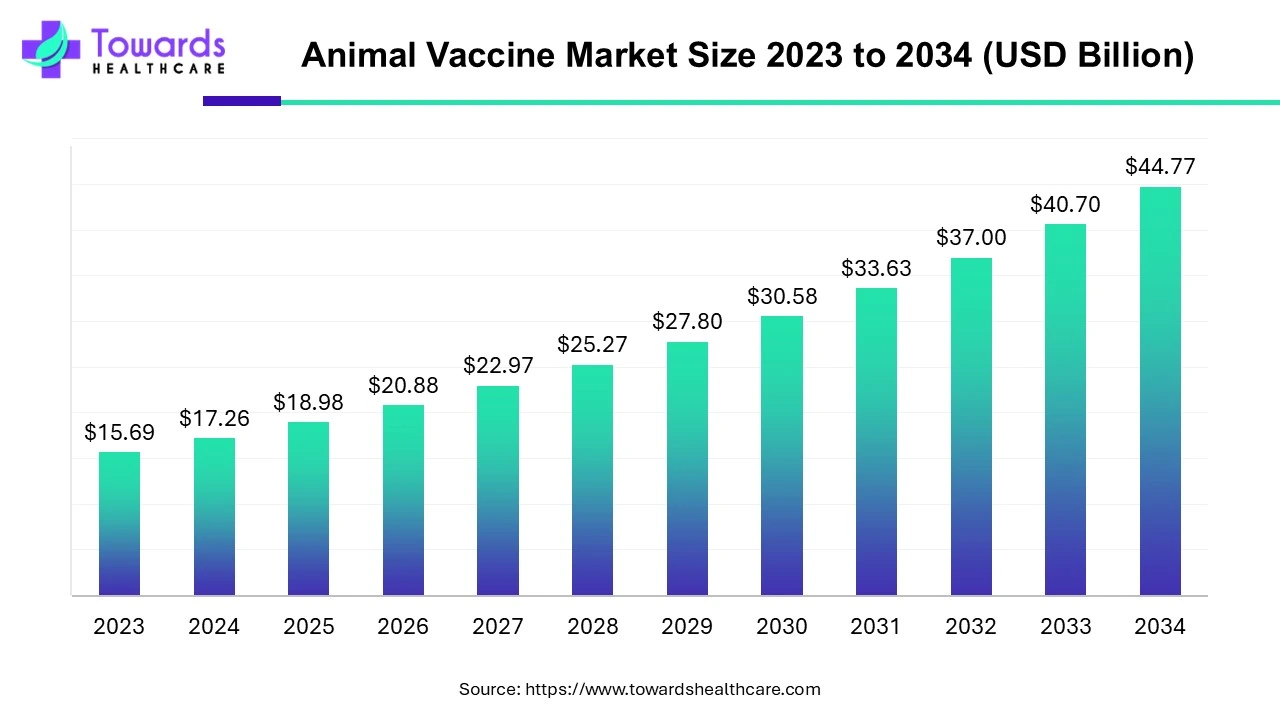

Global animal vaccine market is set to grow from USD 18.98 Bn (2025) to USD 44.77 Bn (2034) at 10% CAGR (2025–2034), propelled by food safety/security priorities, control of zoonoses (75% of new human infections originate in animals), rising pet care, and tech advances (recombinant, vector, intranasal, precision vaccines).

Download Free Sample of Animal Vaccine Market Now and Get the Complete Report Easily at: https://www.towardshealthcare.com/download-sample/5059

Market Size

Base & Forecast: 2025 USD 18.98 Bn → 2034 USD 44.77 Bn (CAGR 10%; growth factor ~2.36 over 9 years).

Annual Momentum Indicators:

2025–2027: capacity build-out and new platforms (e.g., vPTMF in EU) accelerate approvals and tech transfer.

2028–2030: peak adoption in livestock biosecurity programs (trade requirements; OIE/FAO alignment).

2031–2034: mix shift toward recombinant/DNA and needle-free/intranasal formats improves ASPs and adherence.

Demand Anchors:

Livestock biosecurity: mandatory/export-linked vaccination; herd productivity focus.

Companion animals: fastest owner spend growth; clinic workflows favor premium combo and intranasal options.

Route/Delivery Implications for Revenue Mix:

Subcutaneous dominates revenue today (broad label coverage, low admin cost).

Intranasal grows fastest (respiratory pathogens; compliance; reduced viral shedding).

Channel Mix:

Hospital/clinic pharmacies hold majority share (prescription + cold-chain assurance).

E-commerce fastest growth vector (convenience, price promos, tele-vet tie-ins).

Technology Mix Trajectory:

2024 leader: attenuated live (broad, durable immunity).

2025–2034: recombinant/vector/DNA gain share (safety, strain agility, platform speed).

Policy Catalysts:

EU: EMA/CVMP platform files + BTV3 approvals shorten time-to-market.

India: DAHD–UNDP cold-chain digitization scales last-mile reliability.

Global supply: New BSL-3/FF lines (e.g., Genome Valley) expand capacity.

Market Trends

Platformization of Vet Vaccines: EMA’s first vPTMF (Innovax, HVT vector) enables faster strain swaps and label extensions (Nov 2024).

Cold-chain Digitalization: DAHD–UNDP MoU (May 2024) to track temperatures, inventory, and routing for fewer potency losses.

Capacity Expansion in Emerging Hubs: IIL’s new BSL-3 + fill-finish facility at Genome Valley (Dec 2023) to target Indian livestock diseases.

Rapid Response to Outbreaks: EMA approvals (Jan 2025) Bluevac-3, Syvazul BTV3 for emergent bluetongue serotype-3.

Shift to Recombinant/Vector & DNA: Safer profiles, targeted antigens, quicker updates to variants.

Needle-free & Mucosal Delivery: Intranasal/oral formats reduce stress, improve compliance, and cut transmission via lower shedding.

Precision Vaccination: Segmented by age/breed/immune status/region; minimizes over-vaccination and ADRs; supports AMR stewardship.

Companion Animal Upswing: Higher pet ownership; clinic standards require routine immunization (NOBIVAC NXT expansion, Sept 2024).

Trade-Driven Biosecurity: Export markets require disease-free certification; vaccination becomes a market-access tool.

Data & Automation: AI/ML across design, QA, and manufacturing to compress timelines and reduce batch variability.

10 Ways AI is Impacting This Market

Epitope & Antigen Design: ML models predict conserved, immunodominant epitopes for strain-inclusive coverage, cutting wet-lab iterations.

Vector Payload Optimization: Algorithms balance insert size, promoter strength, and stability for HVT/other vectors to maximize expression without attenuation risks.

Adjuvant Discovery: In-silico screening suggests TLR agonists/ISCOMs with desired cytokine signatures, improving mucosal/systemic responses.

Strain Surveillance & Forecasting: ML on sequencing + outbreak data flags drift/shift and recommends platform updates (e.g., vPTMF-like workflows).

Dose & Schedule Personalization: Predictive models tailor prime-boost intervals by breed/age/weight/prevaccination titers to reduce ADRs and costs.

Manufacturing Automation: AI-driven bioprocess control (feed rates, temp, DO, pH) improves yields and batch consistency; earlier OOS detection.

Cold-chain Integrity: Computer vision/IoT + anomaly detection preempts temperature excursions; dynamic rerouting reduces spoilage (aligns with DAHD–UNDP aims).

Pharmacovigilance Mining: NLP scans clinic notes to surface rare AEs by lot/region rapidly, enabling label updates or targeted investigations.

Clinical Trial Optimization: Bayesian/AI adaptive designs reduce animal counts and duration while preserving statistical power.

Supply/Demand S&OP: ML forecasts demand by pathogen seasonality, trade events, and weather, preventing stock-outs and minimizing wastage.

Regional Insights

North America (U.S. lead; 2024 regional leader)

Drivers: Advanced vet infrastructure; strong companion segment; large meat/dairy output.

Regulatory/Market: Robust approval pathways; clinics as primary channel; rapid adoption of premium vectors and intranasal products.

Outlook: Stable growth; innovation-led ASPs, combo vaccines, and respiratory indications sustain momentum.

Asia Pacific (fastest growth through 2034)

Scale: Population growth + protein demand → expanded livestock vaccination.

Programs: High-volume disease control (e.g., FMD, PPR doses distributed region-wide).

Capabilities: India/China increasing production capacity; cold-chain digitization to expand rural coverage.

Outlook: Highest CAGR; platform tech and government tenders underpin volumes.

Europe

Policy/Innovation: EU Animal Health Law and EMA’s vPTMF accelerate platform vaccines; quick reaction to BTV3 outbreaks.

Companion Care: High pet ownership; strict welfare/traceability boost routine immunization.

Outlook: Premiumization and fast pathogen-variant response sustain share.

China (country focus)

Demand: Rising pets; frequent livestock disease events (e.g., ASF) heighten prevention focus.

Policy/Industry: Mandated immunizations; consolidation upgrades QA/capacity.

Outlook: Major producer/consumer; increasing exports as GMP capacity scales.

India (country focus)

Scale: Massive livestock base; NADCP targets FMD/Brucellosis vaccination at national scale.

Enablers: DAHD–UNDP cold-chain digitization; IIL Genome Valley facility for domestic needs.

Outlook: Rapid growth; improved last-mile integrity widens effective coverage.

United Kingdom / Germany (country drills within Europe)

UK: Pet ownership surge; Animal Health & Welfare Pathway supports farm health; adoption of recombinant & needle-free.

Germany: Large livestock + pet base; prior FMD experience underpins preventive culture; strong R&D ecosystem.

Outlook: Both sustain high standards and early adoption of precision approaches.

Latin America

Drivers: Beef/poultry exporters need certification; increasing companion animal spend in Brazil/Mexico.

Outlook: Modernization of cold-chain and surveillance systems boosts uptake.

Middle East & Africa (MEA)

Needs: Targeted programs for ruminant diseases; logistics challenges make thermostable and platform solutions valuable.

Outlook: Stepwise growth tied to infrastructure and donor-backed campaigns.

Market Dynamics

Drivers

Zoonoses control (75% of new human diseases are animal-origin).

Food safety/security; trade prerequisites tied to vaccination.

Companion animal health spend; clinic-based standard of care.

Tech advances: recombinant/DNA/vector, intranasal, adjuvants.

Restraints

High R&D/scale-up/regulatory costs; barrier for SMEs.

Cold-chain fragility and rural logistics; potency loss risk.

Opportunities

Precision vaccines customized by population/region; AMR stewardship.

Emerging markets (APAC, LatAm) volume expansion; tenders & public programs.

Thermostable formulations and last-mile innovation (digital cold-chain).

Challenges/Threats

Stringent, time-consuming approvals and post-marketing PV workload.

Price pressure from generics/low-cost competitors in sensitive markets.

Meet the Top Vendors Transforming Animal Vaccine Market

Zoetis

Product: Broad portfolio across livestock/companion; strong parasiticides + vaccines.

Overview: Global leader in animal health innovation and commercialization.

Strengths: Scale, R&D engine, distribution into clinics and producers.

Boehringer Ingelheim

Product: Extensive swine, ruminant, and pet vaccines; respiratory focus.

Overview: Top-tier vet franchise within diversified pharma.

Strengths: Science depth, biologics know-how, farmer engagement.

Merck (Merck Animal Health / NOBIVAC platform)

Product: NOBIVAC NXT platform incl. FeLV RNA-particle vaccine.

Overview: Innovation track record; strong U.S./EU presence.

Strengths: Platformization, clinic relationships, label breadth.

Elanco

Product: Companion + farm vaccines and therapeutics.

Overview: Focus on productivity and pet wellness segments.

Strengths: Portfolio synergy, channel access, brand equity.

Virbac

Product: Companion animal core with expanding vaccines.

Overview: Vet-centric firm with European roots and global reach.

Strengths: Strong vet practice footprint; nimble innovation.

Ceva Santé Animale (Ceva)

Product: Poultry and ruminant vaccines; hatchery solutions.

Overview: Privately held; strong in biologics and delivery systems.

Strengths: Field execution, emerging-market presence, service model.

Phibro Animal Health

Product: Livestock vaccines; health and nutrition portfolio.

Overview: Focus on production animal outcomes.

Strengths: Integrated offerings; cost-effective solutions.

Biogénesis Bagó

Product: FMD and ruminant vaccines; regional leadership.

Overview: Strong LatAm presence with export capacity.

Strengths: Outbreak response, government tenders, technical depth.

Indian Immunologicals Ltd. (IIL)

Product: Livestock vaccines targeting Indian priority diseases.

Overview: Expanding with BSL-3 + fill-finish capacity (Genome Valley).

Strengths: Local scale, program alignment (national disease control).

Neogen Corporation (animal health portfolio)

Product: Diagnostics plus select biologics interface with vaccination programs.

Overview: Safety and diagnostics company with animal health adjacency.

Strengths: Diagnostics-vaccine synergy, QA influence at farms.

(Also notable from list: Intas; Merck KGaA (as listed); Ourofino; Rom-region players.)

Latest Announcements

EMA (Jan 2025): Approval of Bluevac-3 and Syvazul BTV3 to protect sheep against emergent BTV serotype-3, addressing ongoing European outbreaks; demonstrates rapid regulatory response to novel serotypes.

Merck Animal Health (Sept 2024): Expansion of NOBIVAC NXT vaccine platform to FeLV (RNA-particle tech), availability through clinics/hospitals; underscores platform scalability for companion care.

EMA/CVMP (Nov 2024): First vPTMF certificate (Innovax; turkey herpesvirus vector backbone) to speed EU vet vaccine development and lifecycle management.

DAHD–UNDP India (May 2024): MoU to digitalize vaccine cold-chain, capacity building, and communications—targeting potency retention and coverage.

IIL (Dec 2023): New Genome Valley plant (~INR 700 Cr), BSL-3 drug substance + fill-finish, aimed at two major Indian livestock diseases—boosts domestic self-reliance.

Recent Developments

Outbreak-driven EU approvals for BTV3 vaccines (sheep) enable immediate field protection.

Platform certification (vPTMF) institutionalizes faster changes/updates for vector vaccines.

India’s cold-chain digitalization program reduces wastage and supports rural penetration.

Capacity scale-up in India (IIL) adds bio-containment and throughput for priority pathogens.

NOBIVAC NXT broadening signals companion vaccine platform race and RNA-particle adoption.

Segments Covered

By Product Type

Attenuated Live (2024 Leader)

Dominance Rationale: These vaccines provide broad, durable immunity and rapid onset of protection at a low production cost, making them the preferred choice for mass immunization.

Examples: Commonly used for Bluetongue, Lumpy Skin Disease (LSD), and Foot-and-Mouth Disease (FMD).

Immunological Response: Live but weakened pathogens replicate in the host to elicit both humoral and cell-mediated responses, ensuring long-term protection with often a single dose.

Operational Advantage: Ideal for large-scale government programs or export certification campaigns due to quick coverage and affordability.

Risk Management: Reversion to virulence risk mitigated through controlled attenuation, genetic stability testing, and tight QC protocols.

Market Implication: High-volume, low-cost product; competitive pricing and manufacturing consistency drive share retention.

Recombinant (Fastest Growing Segment)

Growth Catalyst: Driven by biotechnology and genetic engineering, recombinant vaccines offer targeted antigen specificity, eliminating the need for the whole pathogen.

Platform Example: Turkey Herpesvirus (HVT) vector technology, used in EMA’s Innovax vPTMF-certified platform.

Advantages: Safer profile, minimal side effects, easy to update for emerging strains or serotypes.

Regulatory Advantage: Fits within platform certification frameworks (vPTMF) that shorten approval timelines for new variants.

Market Impact: Higher ASPs, strong traction in companion animal and premium livestock categories; supports one-health safety initiatives.

Inactivated (Killed)

Use Case: Applied where live vaccines are contraindicated, such as in pregnant or immunocompromised animals.

Safety Profile: Non-replicating, ensuring high biosafety; adjuvants are added to boost immune response.

Limitations: Typically requires multiple doses or boosters, increasing campaign complexity.

Commercial Utilization: Commonly adopted in routine herd vaccination and export compliance programs where consistent titers are required.

Economic Outlook: Mid-range pricing; stable revenue from institutional tenders and regulatory-driven demand.

Subunit

Composition: Contains purified antigenic fragments or proteins that trigger immune response without introducing the entire pathogen.

Clinical Edge: Reduced risk of adverse reactions or cross-reactivity; suitable for animals sensitive to reactogenic vaccines.

Applications: Growing use in precision vaccination programs targeting specific regional strains or animal subpopulations.

R&D Link: Enhanced performance when paired with novel adjuvants such as TLR agonists or immune-stimulating complexes (ISCOMs).

Market Position: Increasing adoption in companion animals and specialized poultry/swine programs emphasizing safety and precision.

DNA (Emerging Technology)

Innovation Factor: DNA vaccines use genetic blueprints of antigens to generate protective immune responses; supports fast, flexible design cycles.

Performance Advantage: Elicits strong cell-mediated (T-cell) and humoral (antibody) immunity.

Pipeline Use: Particularly suitable for highly mutable pathogens where strain turnover is rapid.

Barriers: Still at regulatory infancy; delivery optimization and cost constraints limit commercial uptake.

Long-Term Outlook: Expected to gain traction post-2030 as delivery systems and platform reliability improve.

By Animal Type

Livestock (Largest Share in 2024)

Market Role: Central to ensuring food security, export access, and disease-free certifications; accounts for majority global vaccine consumption.

Diseases Covered: Foot-and-Mouth Disease, PPR, Lumpy Skin Disease, Clostridial infections, and respiratory viruses.

Procurement Channels: Primarily through government tenders, public–private partnerships, and cooperative programs.

Economic Logic: Vaccination reduces mortality/morbidity, improves yield, and secures trade access — especially critical for beef and dairy exports.

Growth Support: Increasing outbreaks and strong government funding (India, China, Brazil) sustain high demand levels.

Companion Animals (Fastest Growth Segment)

Demand Engine: Rising pet ownership, urbanization, and emotional investment in animal wellness.

Healthcare Culture: Routine vaccinations integrated into clinic wellness programs; mandatory in many countries.

Technological Edge: Rapid uptake of RNA-particle and recombinant vaccines due to high safety expectations.

Distribution: Dominated by clinic and hospital pharmacies, supported by vet-led recommendations.

Commercial Outlook: High-margin category; brands like NOBIVAC NXT FeLV from Merck define innovation leadership.

Poultry / Aqua / Ruminants / Swine (High-Volume Segments)

Poultry: Uses mass immunization methods (spray, in-ovo, or drinking water); critical for respiratory and enteric diseases.

Aqua: Relies on immersion/oral vaccination, minimizing handling stress and optimizing farm-level coverage.

Ruminants: Focused on respiratory and clostridial infections; tied to seasonal herd health programs.

Swine: Controlled vaccination for PRRS, influenza, and Mycoplasma; heavy reliance on diagnostic precision.

Market Value: Key to large-volume sales; logistics mastery and low wastage rates define supplier competitiveness.

By Route of Administration

Subcutaneous (2024 Leader)

Dominant Position: Widely used due to ease of administration and long-lasting immune response.

Pharmacokinetics: Slow absorption via fatty tissue leads to sustained antigen presentation.

Cost Advantage: Economical for mass administration; minimal training needed for handlers.

Applicability: Ideal for attenuated and inactivated vaccines where controlled release improves efficacy.

Intramuscular

Purpose: Required when vaccine label specifies deeper tissue delivery to optimize immune activation.

Limitations: Slightly higher discomfort; requires skilled administration.

Use Case: Predominantly used for inactivated or subunit formulations; reliable uptake in livestock and swine programs.

Market Significance: Moderate growth with ongoing training programs ensuring correct technique and dosage accuracy.

Intranasal (Fastest Growing Route)

Advantage: Non-invasive, stress-free, and preferred for respiratory pathogens like pneumonia or parainfluenza.

Immunity Mechanism: Triggers local mucosal immunity (IgA) in respiratory tract, limiting viral replication and transmission.

Key Benefit: Reduces viral shedding, leading to improved herd or kennel-wide protection.

Adoption Curve: Rapid acceptance among pet owners and calf rearing farms seeking ease and compliance.

By Distribution Channel

Hospital/Clinic Pharmacy (Largest Market Share)

Dominance Rationale: Centralized vaccine dispensing ensures cold-chain integrity and professional administration.

Value Chain Control: Vets handle diagnosis, storage, and record-keeping, ensuring traceability.

Market Drivers: Growth in veterinary service centers (e.g., 48,000+ in the U.S.) and clinic-based technology adoption.

Business Edge: Facilitates patient follow-up, AE reporting, and cross-sell opportunities (deworming, supplements).

Retail

Market Role: Sells OTC-permitted vaccines in countries allowing direct purchase; mostly for rural or smallholder use.

Benefits: Convenient, cost-effective for routine doses.

Limitations: Requires user education on handling and administration; limited penetration in urban regulated markets.

Growth Scope: Strengthened by urban vet pharmacies expanding product offerings beyond clinics.

E-Commerce (Fastest-Growing Channel)

Growth Catalyst: Increasing online purchasing behavior, digital vet consultations, and home-delivery solutions.

Customer Appeal: Greater choice, competitive pricing, auto-refill options, and tele-vet integration.

Cold-Chain Assurance: Suppliers employ temperature-controlled packaging and real-time tracking to maintain potency.

Strategic Potential: Opportunity for subscription-based vaccination programs and data-driven adherence reminders.

By Region

North America (U.S., Canada)

Market Leadership: Dominated 2024 with strong veterinary infrastructure and high companion animal vaccination rates.

Innovation Hub: Early adoption of recombinant and intranasal products; emphasis on pet wellness programs.

Commercial Ecosystem: Structured distributor networks and advanced regulatory standards.

Outlook: Sustained growth from companion animal healthcare, R&D leadership, and platform diversification.

Asia Pacific (China, Japan, India, South Korea, Thailand)

Growth Rate: Fastest-growing region; demand tied to rising meat, dairy, and pet ownership trends.

Government Programs: Large-scale initiatives such as India’s NADCP and China’s ASF control programs.

Supply Chain Evolution: Investments in cold-chain digitization (India) and local vaccine manufacturing (IIL, China).

Regional Advantage: High population density and rapid urbanization fuel structural demand for animal health interventions.

Europe (Germany, UK, France, Italy, Spain, Nordics)

Regulatory Backbone: Strong frameworks under EU Animal Health Law; EMA fast-tracks outbreak-response vaccines.

Innovation Trends: Transition to mRNA and nanoparticle-based animal vaccines; focus on companion animal safety.

Outlook: Stable, innovation-driven market emphasizing quality, traceability, and rapid outbreak containment.

Latin America (Brazil, Mexico, Argentina)

Export-Linked Growth: Meat exporters adopt vaccination to maintain disease-free status and trade eligibility.

Companion Animal Upside: Increasing pet ownership and vet service modernization enhance vaccine penetration.

Strategic Focus: Partnerships with local governments and agribusiness cooperatives ensure reliable distribution.

Middle East & Africa (Saudi Arabia, UAE, South Africa, Kuwait)

Market Character: Emerging but constrained by infrastructure and cold-chain challenges.

Program Orientation: Targeted campaigns for ruminant and zoonotic disease control supported by international aid.

Opportunity Space: Demand for thermostable vaccines and simplified logistics solutions is high.

Outlook: Gradual growth tied to infrastructure upgrades, donor funding, and technology transfer.

Top 5 FAQs

-

What is the market size and growth outlook?

USD 18.98 Bn (2025) to USD 44.77 Bn (2034) at ~10% CAGR. -

Which region leads today, and which grows fastest?

North America dominated in 2024; Asia Pacific is fastest-growing through 2034. -

Which product types are leading and rising?

Attenuated live dominated in 2024; recombinant vaccines will expand most rapidly. -

What routes of administration matter most?

Subcutaneous led in 2024; intranasal is the fastest-growing (non-invasive, respiratory focus). -

What recent regulatory/industry moves should I know?

EMA approved BTV3 vaccines (Jan 2025); EMA/CVMP issued first vPTMF (Nov 2024); Merck Animal Health expanded NOBIVAC NXT FeLV (Sept 2024); DAHD–UNDP cold-chain digitization (May 2024); IIL launched a new BSL-3 manufacturing site (Dec 2023).

Access our exclusive, data-rich dashboard dedicated to the therapeutic area industry – built specifically for decision-makers, strategists, and industry leaders. The dashboard features comprehensive statistical data, segment-wise market breakdowns, regional performance shares, detailed company profiles, annual updates, and much more. From market sizing to competitive intelligence, this powerful tool is one-stop solution to your gateway.

Access the Dashboard: https://www.towardshealthcare.com/access-dashboard

Checkout Animal Vaccine Market Report Now at: https://www.towardshealthcare.com/checkout/5059

Become a valued research partner with us – https://www.towardshealthcare.com/schedule-meeting

You can place an order or ask any questions, please feel free to contact us at sales@towardshealthcare.com

Powering Healthcare Leaders with Real-Time Insights: https://www.towardshealthcare.com/healthcare-intelligence-platform

Europe Region – +44 778 256 0738

North America Region – +1 8044 4193 44

APAC Region: +91 9356 9282 04

Visit Our Website: https://www.towardshealthcare.com

Find us on social platforms: LinkedIn | Twitter | Instagram | Medium | Pinterest