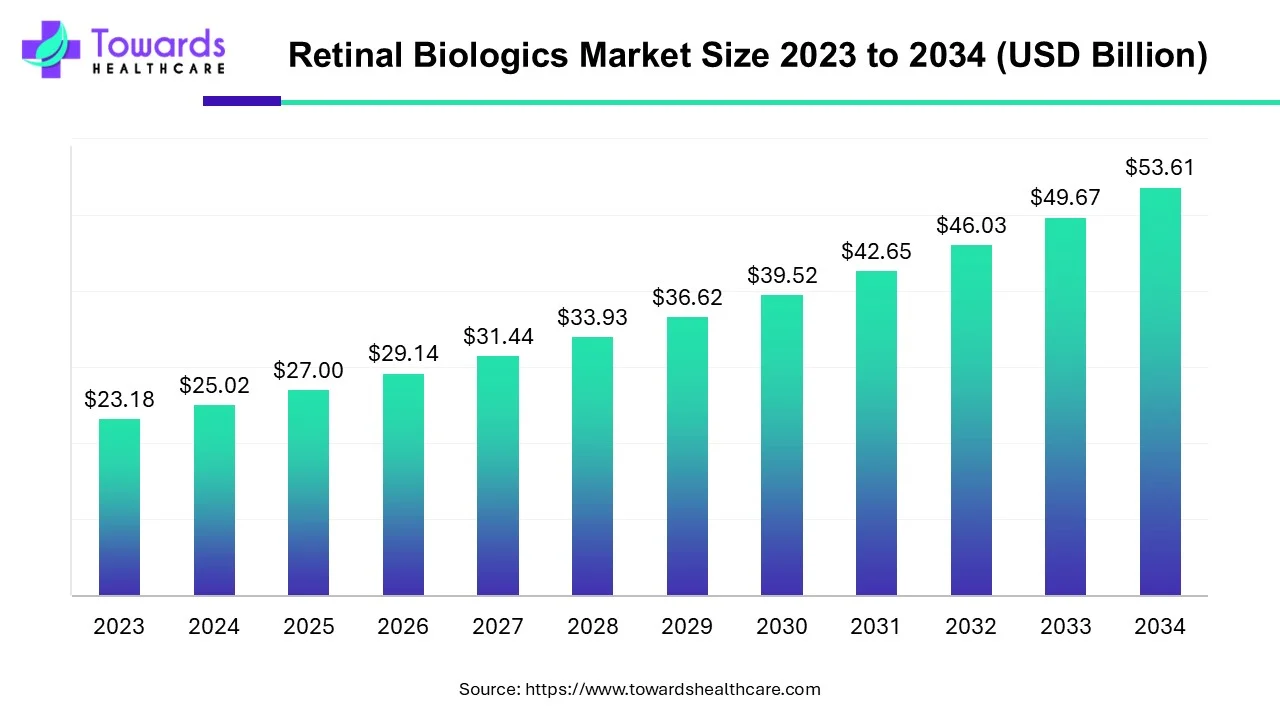

The global retinal biologics market is projected to grow from USD 27.0 billion in 2025 to USD 53.61 billion by 2034, expanding at a CAGR of 7.92% (2025–2034) as biologic therapies (especially VEGF-A antagonists and novel gene/antisense approaches) address rising burdens of age-related macular degeneration and diabetic retinopathy.

Download Free Sample: https://www.towardshealthcare.com/download-sample/5166

Market size

Base and forecast figures: Market value is USD 27.0B (2025) → USD 53.61B (2034). This implies near doubling of market value across the forecast window and reflects both volume growth and introduction/uptake of higher-value biologic therapies.

Compound growth rate: CAGR 7.92% — consistent growth driven by increasing disease prevalence, new drug approvals, and uptake of biosimilars and advanced delivery/therapy formats.

Price / value composition: A sizeable portion of market value is driven by high per-unit cost of biologics (complex production, R&D amortization), compounded by premium prices for novel agents and gene therapies.

Therapeutic class weighting: VEGF-A antagonists form a dominant share (largest drug-class contributor) — legacy biologics and newer entrants (bispecifics, combination biologics) add higher average selling prices.

Biosimilar impact on size composition: Entry of biosimilars (e.g., ranibizumab and aflibercept biosimilars) shifts market value mix — they increase access and volumes but may depress list prices, altering revenue distribution across originator vs biosimilar players.

Pipeline to market conversion: Late-stage pipeline programs and gene therapies (e.g., ABBV-RGX-314 program planned pivotal program) represent upside to market size if approved and broadly commercialized.

Geographic growth mix: North America contributes the largest absolute share; Asia-Pacific expected fastest relative growth (high population base + increasing healthcare infrastructure) — this affects regional revenue shares of the global USD figures.

Channel economics: Hospital pharmacy channel holds largest share historically — hospital procurement and inpatient/outpatient administration patterns influence where revenues are captured.

Reimbursement & payor effect: Public and private payor coverage decisions — especially for expensive biologics and gene therapies — materially influence realized market size versus theoretical demand.

Cost restraints & elasticity: High cost of biologics is a headwind that can cap uptake in price-sensitive regions; however, unmet need and sight-saving value create inelastic demand among covered patients.

Market trends

Dominance of VEGF-A antagonists: Anti-VEGF remains the therapeutic backbone for neovascular retinal disorders; agents like aflibercept, ranibizumab, bevacizumab (and newer bispecifics such as faricimab) continue to command largest market share.

Biosimilar and price competition: Introduction of biosimilars (BYOOVIZ, Yesafili, Cimerli, ABP-938 biosimilar approvals/launches) is expanding access and changing pricing dynamics; biosimilars reduce list price (BYOOVIZ listed ~40% below Lucentis historically) and shift market share.

Gene and long-duration therapies rising: Investigational programs (ABBV-RGX-314, OCU400, Kodiak’s candidates) signal movement toward gene-based or long-durational treatments that could reduce injection frequency and reshape treatment paradigms.

Regional acceleration in Asia-Pacific: Rapid expansion of healthcare infrastructure in China and India and aging populations drive fastest CAGR in Asia-Pacific.

Hospital pharmacies as primary distribution: Hospital pharmacy dominance indicates hospital/clinic administration models persist; hospital procurement controls reimbursement and usage.

Aging population drives demand: Epidemiologic shifts (increased centenarian figures, growing 60+/65+ cohorts) raise AMD and other age-related retinal disease prevalence, increasing lifetime treatment need.

Diabetes epidemic fuels DR demand: Rising diabetes prevalence and projected DR cases (presently ~103 million → projected 161 million by 2045 per cited meta-analysis) directly expand demand for retinal biologics.

Shift to personalized ophthalmology: Advances in diagnostics, sequencing, and translational research promote individualized therapies (gene therapy, modifier gene strategies) — enabling targeted treatment for inherited retinal disorders.

M&A, partnerships, licensing activity: Companies restructure portfolios via settlements and licensing (e.g., Biocon-Bayer settlement for Yesafili) and commercial transactions (Sandoz/Coherus) to accelerate market entry.

Cost and manufacturing complexity remain restraints: High R&D and manufacturing costs (biologics complexity; estimated development costs approaching ~$1.1B) constrain price reductions and may slow access in lower-income regions.

AI 10 deep point-wise roles/impacts on the retinal biologics market

Target identification and discovery acceleration

Subpoint: AI-driven analysis of omics and imaging datasets can uncover novel retinal disease targets and pathways (e.g., new angiogenic modulators beyond VEGF).

Explanation: By integrating genomics, transcriptomics and retinal imaging, AI finds patterns humans miss, shortening discovery timelines and increasing probability of high-value biologic candidates.

Biomarker discovery for patient stratification (personalized medicine enablement)

Subpoint: Machine learning models can identify molecular or imaging biomarkers that predict responder vs non-responder to specific biologics.

Explanation: Enables targeted trials, reduces trial size, and supports payer arguments for cost-effective personalized therapies, aligning with the market’s shift toward personalized ophthalmology.

Clinical trial optimization and virtual trial design

Subpoint: AI selects optimal inclusion criteria, simulates outcomes, and identifies high-yield sites/patients for retinal biologics trials (especially for rare inherited diseases).

Explanation: Reduces trial dropouts and shortens timelines — critical for expensive biologic programs (reducing the near-$1.1B risk).

Automated retinal image analysis for diagnosis, progression monitoring and endpoints

Subpoint: Deep learning algorithms read OCT and fundus images to grade disease severity, quantify fluid/leakage, and measure anatomical endpoints objectively.

Explanation: Provides scalable diagnostics in clinics, enables remote monitoring, and creates standardized endpoints for trials and reimbursement dossiers.

Predictive modeling for dosing regimens and durability

Subpoint: AI models predict individual pharmacodynamic responses, suggesting tailored dosing intervals (e.g., spacing intravitreal injections).

Explanation: Can reduce injection frequency, improve adherence, and support value demonstrations for long-acting gene therapies or bispecifics.

Manufacturing process optimization and batch quality prediction

Subpoint: Machine learning monitors bioreactor sensor data to predict yields, detect deviations, and optimize upstream/downstream processes.

Explanation: Mitigates batch variability (a key biologics challenge), improves yield and reduces cost per dose — directly addressing cost restraints.

Supply chain forecasting and demand planning

Subpoint: AI forecasts regional demand (age cohorts, diabetes prevalence, treatment penetration) to optimize inventory and reduce stockouts in hospital pharmacies.

Explanation: Ensures high-cost biologics are available where needed while minimizing wastage from expired vials.

Real-world evidence (RWE) generation and value demonstration

Subpoint: AI extracts structured insights from electronic health records and imaging archives to show long-term effectiveness and safety.

Explanation: Supports reimbursement negotiations and pharmacoeconomic arguments for expensive biologics and gene therapies.

Regulatory submission support and automated document generation

Subpoint: Natural language models draft parts of regulatory packages, summarize trial findings, and map evidence to regulatory questions.

Explanation: Speeds dossier preparation for approvals and biosimilar filings (reducing time to market).

Patient engagement, adherence prediction and tele-ophthalmology triage

Subpoint: AI chatbots and predictive models identify patients at high risk of non-adherence to injection schedules and trigger outreach or tele-visits.

Explanation: Improves clinical outcomes and helps maintain consistent treatment regimens, particularly important where frequent intravitreal injections are standard of care.

Regional insights

North America — largest absolute market share

Healthcare infrastructure & R&D: Strong clinical research ecosystem and payer systems that reimburse biologics enable high uptake.

Chronic disease burden & aging population: High prevalence of AMD and DR increases demand; forecasts show rising older cohorts and high economic cost of AMD (~USD 30B/year estimate referenced).

Commercial environment: Large commercial launches and rapid adoption of biosimilars/novel agents supported by distribution through hospital pharmacies and clinic networks.

Asia-Pacific — fastest CAGR (highest relative growth)

Demographic drivers: Large and aging populations in China, India, Japan accelerate absolute patient numbers.

Infrastructure investment: Rapid increases in hospital capacity and specialist availability (China’s vast network of hospitals and medical staff).

Access dynamics: Price sensitivity but expanding insurance coverage; biosimilars can play a rapid adoption role to scale volume.

Europe — growth through biosimilars and favorable regulations

Regulatory environment: Supportive biosimilar pathways (e.g., recent approvals like faricimab in EU) encourage competition and access.

Market nuance: National health systems emphasize cost-effectiveness and often negotiate prices, pushing biosimilar uptake.

Latin America — constrained by cost but large unmet need

Access limitations: Public budgets and procurement processes determine access; hospital pharmacy channel still key where available.

Opportunity: Rapid gains possible with lower-cost biosimilars and tiered pricing strategies.

Middle East & Africa — nascent uptake, high unmet need

Infrastructure variability: Limited specialist density in many countries; major urban centers lead adoption.

Access strategies: Tiered pricing, philanthropic programs, and tele-ophthalmology could accelerate adoption.

Cross-regional dynamics — role of biosimilar & gene therapy launches

Timing of launches & licensing agreements (e.g., Biocon-Bayer, Sandoz/Coherus) determines when lower-cost alternatives become available regionally.

Reimbursement heterogeneity will create regional differences in which novel therapies achieve commercial scale.

Market dynamics

Demand drivers: disease prevalence & aging (structural demand)

Evidence: Aging populations and diabetes prevalence (DR currently ~103M projected to 161M by 2045) drive sustained clinical need.

Supply drivers: innovation & pipeline

Evidence: Active pipeline (gene therapy, bispecifics, long-acting biologics like those from Kodiak, REGENXBIO collaborations) can shift standard of care.

Pricing & reimbursement pressures

Explanation: High development/manufacturing costs (~$1.1B) justify premium pricing; payors demand cost-effectiveness and RWE.

Competitive landscape: originators vs biosimilars

Effect: Biosimilar launches (BYOOVIZ, ABP-938, Yesafili, Cimerli) increase competition—volume up, price down for some molecules.

Distribution concentration in hospital pharmacies

Effect: Hospital procurement influences market access and negotiation power; hospitals centralize administration of intravitreal biologics.

Regulatory & intellectual property considerations

Effect: Patent expirations and settlements (e.g., Biocon-Bayer) change entry timing for biosimilars, affecting market dynamics.

Manufacturing complexity & batch variability risk

Effect: Complexity raises cost, raises barrier to smaller entrants, and creates quality consistency challenges.

Commercial partnerships & M&A activity

Effect: Licensing deals and acquisitions speed market access and scale commercialization (e.g., Sandoz/Coherus transaction).

Health economics & value demonstration importance

Effect: Providers and payors demand demonstration of reduced treatment burden (e.g., fewer injections) and long-term visual outcomes.

Technology convergence (AI, digital diagnostics, wearable/telemedicine)

Effect: These technologies can reduce care gaps, improve monitoring, and support rollouts in resource-limited settings — ultimately expanding addressable market.

Top 10 companies

AbbVie Inc. (U.S.)

Key product/program: ABBV-RGX-314 investigational program (gene therapy for wet AMD).

Overview: Large biopharma with robust R&D and commercial infrastructure; full-year 2024 revenue ~$56.334B (growth y/y).

Strength: Financial firepower, clinical development expertise, capability to run pivotal Phase 3 programs and global launches.

Amgen Inc. (U.S.)

Key product/program: ABP-938 — a biosimilar of EYLEA (aflibercept) approved by U.S. FDA.

Overview: Large biotech with proven biologics development and manufacturing capabilities.

Strength: Strong biologics manufacturing scale and established commercial channels for ophthalmology biosimilars.

Santen Pharmaceutical Co., Ltd (Japan)

Key product/program: Eylea® 8 mg (aflibercept recombinant solution) introduced/distributed in Japan (with Bayer Yakuhin marketing license).

Overview: Ophthalmology-focused specialist with regional market knowledge.

Strength: Deep ophthalmic focus and regional market relationships enabling targeted launches.

Biocon Biologics / Biocon (India)

Key product/program: Yesafili biosimilar of EYLEA; Biocon-Bayer settlement enabling Canada access.

Overview: Biosimilar leader leveraging cost advantages to expand access.

Strength: Cost-competitive manufacturing and partnerships to accelerate geographic entry.

Bayer AG (Germany)

Key product/program: Eylea originator marketer (marketing license holder in certain territories).

Overview: Large diversified healthcare company with strong ophthalmology franchise.

Strength: Global reach, established ophthalmology portfolio, and commercialization capacity.

Novartis AG (Switzerland)

Key product/program: Originator company for Lucentis (ranibizumab) historically; competitor in retinal space.

Overview: Global pharmaceuticals leader with scale and R&D.

Strength: Strong clinical development and commercialization, legacy retinal assets.

Kodiak Sciences Inc. (U.S.)

Key product/program: Pipeline candidates (tarcocimab, KSI-501, KSI-101) targeting combined mechanisms (e.g., anti-VEGF ± anti-inflammatory).

Overview: Clinical-stage specialty biotech focused on durable retinal therapeutics.

Strength: Innovative mechanistic approaches and late-stage pipeline candidates that could alter treatment paradigms.

AstraZeneca (U.K.)

Key product/program: Active in biologics, potential pipeline/partnership involvement in ophthalmology.

Overview: Large global pharma with broad biologics expertise.

Strength: R&D depth and global commercialization.

Amneal / Sun Pharmaceutical / Aurobindo / Teva / Fresenius / Merck / Pfizer — (examples from list)

Product/overview: These firms play roles as biosimilar developers, generic injectables suppliers, or global distributors.

Strength: Manufacturing scale, cost efficiency, distribution networks, and ability to support hospital pharmacy channels.

Ocugen, Inc. (U.S.)

Key product/program: OCU400 — gene-modifier platform being evaluated for Leber congenital amaurosis and RP (Phase 1/2 updates).

Overview: Small biotech focusing on inherited retinal diseases with gene-agnostic modifier approach.

Strength: Novel platform potentially addressing genetically heterogeneous retinal disorders.

Latest announcements

AbbVie & REGENXBIO (Jan 2025)

Announcement: Investigation of ABBV-RGX-314 in wet AMD patients; plan for pivotal (Phase 3) program in 2026.

Implication: If successful, a gene therapy that reduces injection burden could materially disrupt chronic anti-VEGF market economics and shift long-term revenue models.

Amgen — ABP-938 FDA approval (date noted)

Announcement: U.S. FDA approval of ABP-938 (aflibercept biosimilar) for certain angiogenic eye disorders.

Implication: Biosimilar competition to EYLEA expands access and compresses pricing for high-value aflibercept market share.

Santen (April 2024)

Announcement: Launch of Eylea® 8mg (114.3 mg/mL) in Japan (with Bayer Yakuhin marketing license).

Implication: New presentations/formulations target dosing convenience and regional distribution synergies.

Biocon Biologics — settlement with Regeneron/Bayer (Mar 2024)

Announcement: Agreement to allow sale of Yesafili in Canada; Biocon to introduce by July 1, 2025 latest.

Implication: Biosimilar entry timelines clarified, enabling market planners and payors to prepare for price competition.

Sandoz & Coherus (Jan 2024 deal)

Announcement: Sandoz paid $170M for biosimilar ranibizumab (Cimerli) assets and commercial support.

Implication: Strategic acquisitions accelerate biosimilar commercialization with ready inventory and sales infrastructure.

Ocugen (Sept 2023 / trial updates)

Announcement: Safety/efficacy updates for OCU400 in LCA and RP — extension data from high-dose cohorts.

Implication: Gene-modifier strategies progress through clinical stages, potentially enabling treatments for inherited retinal degeneration.

Biogen & Samsung Bioepis (June 2022)

Announcement: U.S. launch of BYOOVIZTM (ranibizumab biosimilar) at significant discount versus originator.

Implication: Demonstrates commercial viability of biosimilars in ophthalmology and their effect on pricing dynamics.

Recent developments

Multiple biosimilar launches and deals (BYOOVIZ, Yesafili, Cimerli, ABP-938) increasing competition and access.

Gene therapy programs advancing to pivotal planning (ABBV-RGX-314 planned Phase 3 in 2026).

Novel molecule pipelines (Kodiak’s tarcocimab, KSI series) targeting combined pathways and longer durability.

Commercial transactions accelerating market entry (Sandoz/Coherus purchase of Cimerli assets; Biocon-Bayer settlement).

Market expansion in APAC through launches and distribution agreements (Santen/Bayer in Japan; China hospital expansion metrics).

Clinical updates in inherited retinal disease programs (Ocugen’s OCU400) suggesting movement in rare disease segment.

Segments covered

By Drug Class

VEGF-A Antagonist: Primary therapy group — reductions in vascular leakage and vision restoration (Aflibercept 79–83% effect range; Ranibizumab 61–75%; Bevacizumab 59–68% as reported). Dominant revenue contributor.

TNF-A Inhibitor: Used for inflammatory retinal conditions (e.g., uveitis) — valuable in subsegment where inflammation is key driver.

Other biologic classes: Growth factors, immunomodulators, monoclonal antibodies and blood/plasma products — collectively expand therapeutic options beyond anti-VEGF.

By Indication

Macular degeneration (AMD): Largest indication share — aging population is the primary driver.

Diabetic retinopathy (DR): High unmet need as diabetes prevalence rises; DR affects 30–40% of diabetics and contributes materially to volume demand.

Uveitis and others: Smaller but clinically important subsets where immunomodulatory biologics are used.

By Distribution Channel

Hospital Pharmacies: Largest share — hospitals control in-clinic administration and large volume procurement.

Retail Pharmacies: Important for outpatient prescriptions in markets with community ophthalmology dispensing.

Online Pharmacies: Emerging channel for distribution of ancillary supplies or scripts where permitted.

By Region

North America: Largest share — strong R&D, reimbursement.

Europe: Significant growth with biosimilars and favorable regulation.

Asia-Pacific: Fastest CAGR — driven by population size and infrastructure expansion.

Latin America / MEA: Growing but constrained by access and budgets.

Top 5 FAQs

-

Q: What is the market size and growth rate for retinal biologics?

A: The market is projected to grow from USD 27.0B in 2025 to USD 53.61B by 2034, at a CAGR of 7.92% between 2025–2034. -

Q: Which drug class dominated the retinal biologics market in 2023?

A: VEGF-A antagonists dominated in 2023; they remain the cornerstone of treatment for neovascular retinal disorders. -

Q: What are the main demand drivers for the market?

A: Aging populations (higher AMD prevalence), rising diabetes and diabetic retinopathy burden (current ~103M DR cases projected to 161M by 2045), increasing healthcare infrastructure, and expanding biologic/gene therapy options. -

Q: How do biosimilars and new therapies affect the market?

A: Biosimilars (e.g., BYOOVIZ, Yesafili, Cimerli, ABP-938) expand access and lower list prices, increasing volume but compressing originator revenues; gene/long-acting therapies (e.g., ABBV-RGX-314) could reduce injection frequency and alter lifetime revenue per patient. -

Q: Which regions will show the fastest growth and who dominated in 2023?

A: North America dominated the market in 2023 (largest absolute share); Asia-Pacific is expected to grow at the fastest CAGR during the forecast period due to demographic scale and infrastructure expansion.

Access our exclusive, data-rich dashboard dedicated to the Therapeutics area Sector – built specifically for decision-makers, strategists, and industry leaders. The dashboard features comprehensive statistical data, segment-wise market breakdowns, regional performance shares, detailed company profiles, annual updates, and much more. From market sizing to competitive intelligence, this powerful tool is one-stop solution to your gateway.

Access the Dashboard: https://www.towardshealthcare.com/access-dashboard

Checkout Retinal Biologics Market Report Now at: https://www.towardshealthcare.com/checkout/5166

Become a valued research partner with us – https://www.towardshealthcare.com/schedule-meeting

You can place an order or ask any questions, please feel free to contact us at sales@towardshealthcare.com

Powering Healthcare Leaders with Real-Time Insights: https://www.towardshealthcare.com/healthcare-intelligence-platform

Europe Region – +44 778 256 0738

North America Region – +1 8044 4193 44

APAC Region: +91 9356 9282 04

Visit Our Website: https://www.towardshealthcare.com

Find us on social platforms: LinkedIn | Twitter | Instagram | Medium | Pinterest