The New Frontier of Medicine Accelerates Faster Than Ever

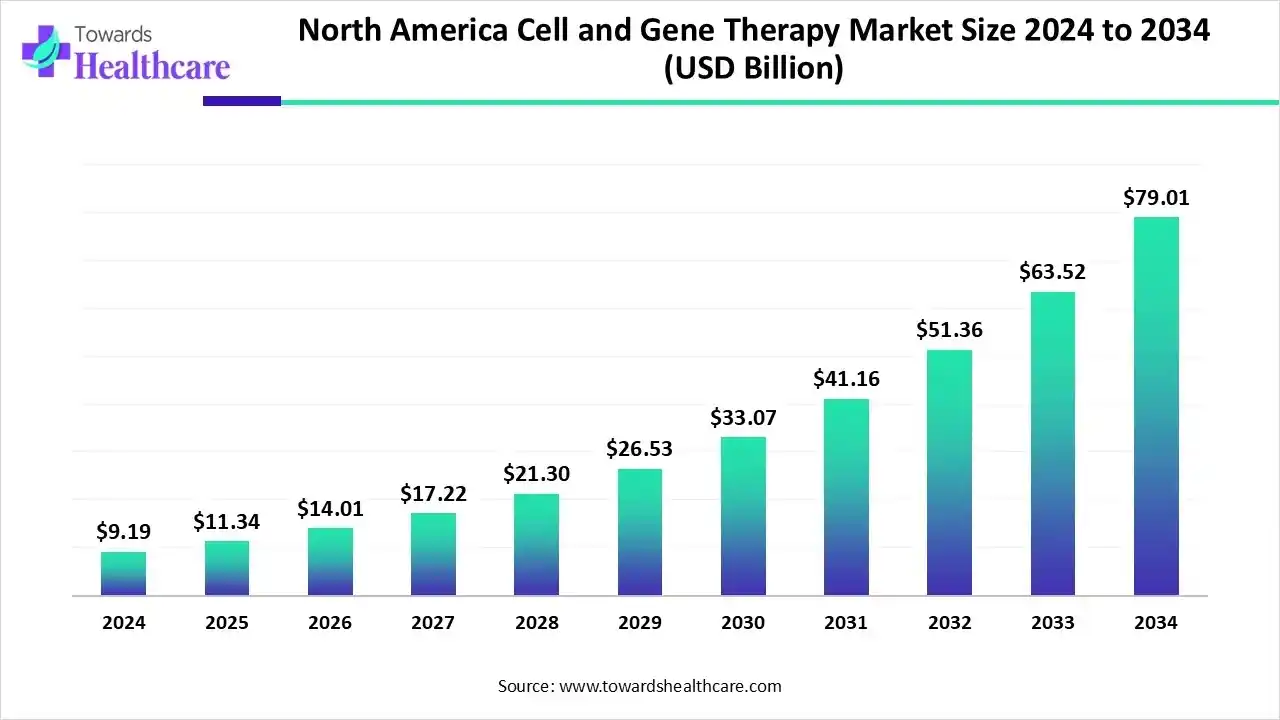

The North America cell and gene therapy market has reached a defining moment, evolving from a niche scientific pursuit into a foundational pillar of modern medicine. In 2024, the market recorded a valuation of USD 9.19 billion, rising to USD 11.34 billion in 2025, and is now projected to surge beyond USD 79 billion by 2034. Such an astonishing growth trajectory, supported by a CAGR of 24.01%, reflects both the pace of scientific innovation and the region’s ability to convert cutting-edge research into real-world therapeutic impact.

Download Sample:

https://www.towardshealthcare.com/download-sample/6297

This transformation rests on a simple but powerful idea: when medicine addresses the biological root of disease rather than just symptoms, the entire framework of healthcare changes. North America, led by the United States, has become the global benchmark for rapid approvals, bold pipeline expansions, adaptive regulations, and advanced manufacturing capacity. With expanding clinical trials, deeper investment, and evolving regulatory clarity, cell and gene therapy has moved from experimental to essential in record time.

A Market Redefining What Treatment and Cure Really Mean

The expansion of the market is driven by a shift in expectations among clinicians, researchers, and patients. In diseases once deemed incurable, curative intent has become a legitimate goal. This shift is particularly impactful in oncology, rare genetic disorders, hematology, metabolic conditions, and inherited retinal diseases. Therapies capable of modifying, replacing, or augmenting genes offer a biological reset for conditions that were traditionally managed through chronic care.

As of 2024, cell therapies accounted for the largest share of the market, representing just over half of total revenues. Their dominance stems from the clinical success of approaches such as stem cell transplantation, engineered immune cells, and regenerative cell platforms that help rebuild or repair damaged tissues. By comparison, gene therapies, while currently smaller in share, are advancing at the fastest growth rate, supported by maturing platforms like viral delivery systems, CRISPR-based editing, and emerging non-viral technologies.

The pace of this evolution reflects scientific maturity that has been decades in the making. What once required years of theoretical work is now backed by clinical evidence, real-world outcomes, and regulatory validation—and the region’s infrastructure shows every sign of keeping pace with future therapeutic breakthroughs.

Why Cancer Remains at the Heart of Market Dominance

Oncology continues to define the direction and scale of the market, accounting for approximately 45% of regional revenue in 2024. Rising cancer incidence, combined with the limitations of conventional treatment modalities, has catalyzed the adoption of advanced cellular and genetic therapies. CAR-T therapies, in particular, have redefined the management of certain hematologic cancers. Their success has encouraged the expansion of next-generation platforms targeting solid tumors and refractory malignancies.

The shifting demographic landscape adds urgency to the oncology focus. Between 2010 and 2030, cancer cases in the United States are expected to increase by nearly 45%. A significant portion of that growth will occur among older adults, those most susceptible to complex, treatment-resistant cancer types. As a result, the demand for therapies that deliver durable responses is set to rise sharply, positioning oncology as the perennial anchor of the CGT ecosystem.

Yet it is the acceleration of rare genetic disorder research that is reshaping future portfolios. Regulatory initiatives such as the FDA’s RDEA Pilot Programme have removed long-standing roadblocks in endpoint validation and trial design for rare disease therapies. With hundreds of gene and cell therapy candidates currently in development for rare disorders, the segment is expected to outpace all others in growth over the next decade.

Viral Vectors Establish Dominance as Non-Viral Systems Rise

Viral vectors remain the backbone of gene therapy manufacturing in North America. In 2024, they accounted for about 70% of the total segment revenue. Their engineering flexibility, strong transduction efficiency, and deep clinical validation provide the foundation for the majority of approved gene therapies today.

Adeno-associated viruses (AAVs), lentiviruses, and retroviruses continue to be preferred for their safety record and durability. Their established role in delivering gene payloads for hematologic, ophthalmologic, and neuromuscular conditions ensures they will retain market dominance in the near term.

However, the momentum behind non-viral vectors is undeniable. Lipid nanoparticles, cationic polymers, and electroporation-based platforms have shown increasing reliability in gene delivery, especially for in vivo applications. Their low immunogenicity and ease of manufacturing position them as the fastest-growing segment. As LNPs become more deeply integrated into genetic medicine, particularly after their success in mRNA vaccine delivery, the balance between viral and non-viral systems may shift significantly by the early 2030s.

Autologous Therapies Lead Today While Allogeneic Platforms Build the Future

Autologous cell therapies captured approximately 60% of the market in 2024, reflecting their strong clinical success and immunological compatibility. These therapies, sourced from a patient’s own cells, enable personalized treatments with lower risk of rejection and often deliver long-term therapeutic benefits.

Yet autologous manufacturing remains slow, costly, and complex. Every production run is unique, tightly controlled, and dependent on the quality of the patient’s cells. These challenges have motivated rapid innovation in allogeneic, or “off-the-shelf,” platforms.

Allogeneic therapies are anticipated to become the fastest-growing segment throughout the next decade. With donor-derived, pre-manufactured cells stored for broad application, allogeneic products offer scalability, faster delivery timelines, and significantly reduced per-patient cost. Their ability to support high-volume manufacturing situates them as critical tools for expanding CAR-T access and broadening adoption across clinical settings.

Why Manufacturing Capability Determines Commercial Success

Clinical-scale manufacturing dominated the market in 2024, accounting for roughly 65% of the segment. At this stage, companies focus heavily on refining processes, validating quality controls, and generating consistent batches for use in trials. This fosters critical flexibility and adaptation before progressing to commercial production.

The fastest growth, however, lies in commercial-scale manufacturing, driven by the pressing need to transition promising therapies into market-ready products. This shift requires advanced facilities, sophisticated automation, digital integration, and highly specialized talent. Companies face increasing pressure to meet regulatory expectations, reduce cost of goods, and deliver reliable therapies at a scale that aligns with rising patient demand.

As more products gain approval, commercial manufacturing capacity could become the industry’s most significant bottleneck, or its greatest accelerator, depending on the sector’s ability to expand intelligently.

Biopharma Leads Today While Hospitals and Clinics Grow Rapidly

Biopharmaceutical and biotechnology companies dominated the market in 2024, contributing roughly half of regional revenue. These organizations, led by established players like Novartis, Gilead’s Kite Pharma, and Bristol Myers Squibb, continue to direct the majority of R&D, pipeline development, and clinical innovation.

Hospitals and specialty clinics, however, represent the fastest-growing end-user group. Their expanding role reflects both rising treatment delivery complexity and the need for specialized infrastructure. In the United States and Canada, advanced centers in oncology, neurology, immunology, and regenerative medicine are increasingly offering CGT-based therapies, supported by cross-disciplinary treatment teams and investment in dedicated facilities.

The United States Extends Its Lead While Canada Expands Capacity

The United States holds an overwhelming share of the North America market—approximately 85% in 2024. Its leadership is supported by a combination of scientific depth, early adoption, strong funding, and rapid regulatory decision-making. The FDA’s readiness to approve complex biologics, particularly CAR-T therapies and gene-based treatments, has solidified the nation’s influence on global development trends.

Canada has begun to carve its own strategic niche. The launch of OmniaBio, the country’s largest CGT-focused CDMO, marks a pivotal moment for Canada’s manufacturing capacity. With a multiyear investment exceeding USD 580 million and a facility designed to accommodate commercial-scale production, Canada is positioning itself as a serious competitor in the region. Its advancements are reinforced by strong regulatory oversight, expanding clinical research, and rising public investment in translational medicine.

AI Emerges as the Silent Catalyst Behind Industry Acceleration

Artificial intelligence is reshaping how cell and gene therapy development unfolds. While still in its formative stages, AI has already demonstrated its ability to accelerate discovery cycles, optimize manufacturing, and predict therapeutic outcomes with increasing accuracy.

Machine learning algorithms analyze massive biological datasets to identify targets, predict stem cell differentiation pathways, and model patient-specific responses to therapy. AI-supported prediction models for gene expression, viral vector performance, and cell fate are shortening timelines that traditionally stretched years. As digital infrastructure grows inside laboratories, manufacturing sites, and clinical networks, AI-enabled workflows are expected to underpin the next decade of breakthroughs.

A Surge in Clinical Trials Signals a More Confident Industry

Clinical research activity has become one of the strongest indicators of market maturity. North America is witnessing record numbers of cell and gene therapy trials, spanning CRISPR-based editing, re-dosing studies, advanced CAR-T platforms, and novel stem cell applications.

Recent milestones continue to raise confidence. In 2025, Immusoft announced the successful re-dosing of a patient with its engineered B-cell candidate for mucopolysaccharidosis type I. This achievement illustrates growing safety and tolerability standards in gene-modified therapeutics. Similarly, the United States welcomed its first clinical trial using non-viral CRISPR editing to repair sickle cell mutations directly in patients—a turning point for next-generation gene therapy.

As trial complexity grows, so does the region’s infrastructure for regulatory support, data monitoring, and long-term patient follow-up, creating an increasingly sophisticated ecosystem for CGT development.

Investment Momentum Strengthens as Strategic Priorities Shift

North America’s CGT landscape is fueled by robust investment across early-stage biotech, established pharma, venture capital, and institutional consortia. Funding flows toward three primary drivers: expanding manufacturing capacity, advancing oncology and rare disease pipelines, and developing novel in vivo gene delivery platforms.

Recent funding rounds—from AvenCell Therapeutics’ USD 112 million raise for CAR-T validation, to Stylus Medicine’s USD 85 million for in vivo genetic medicine, to Cellares and Bristol Myers Squibb’s USD 380 million collaboration—illustrate the growing alignment between investors and the scientific community. This dynamic pipeline signals confidence not only in current technologies but also in the sector’s ability to deliver multi-decade therapeutic impact.

The Region’s Innovation Hubs Shape the Next Decade

California and Massachusetts remain the undisputed epicenters of CGT innovation. Their dominance stems from dense clusters of research institutions, clinical trial networks, technology incubators, and biomanufacturing ecosystems. These hubs attract top scientific talent, channel significant venture funding, and accelerate collaboration between early-stage startups and global pharmaceutical companies.

The combination of academic insight and commercialization pathways allows discoveries in genomic editing, stem cell biology, and vector engineering to move rapidly into clinical environments. This is the foundation that supports North America’s unparalleled speed in bringing advanced therapies from bench to bedside.

A Market Ready for Expansion, But Not Without Challenges

Despite extraordinary progress, the cell and gene therapy market faces several structural challenges. Manufacturing scalability remains one of the biggest hurdles, with supply chain constraints and high production costs limiting widespread access. The complexity of personalized therapies also demands advanced logistics, including cryogenic transport and time-sensitive coordination.

Regulatory frameworks continue to evolve but must keep pace with the scientific trajectory. Long-term safety monitoring, durability assessments, and ethical considerations surrounding genetic modification require constant vigilance.

Yet these challenges are not signs of weakness—they reflect the natural tension between scientific ambition and practical implementation. As regulatory agencies, manufacturers, and clinical networks collaborate more closely, the market is positioned to resolve these constraints and translate innovation into equitable access.

What the Future Holds for North America’s CGT Landscape

The next decade will witness accelerated approvals, deeper integration of AI and automation, broader application of CRISPR tools, growth in in vivo editing, and increased focus on affordability through manufacturing innovation. The rapid shift from autologous to allogeneic platforms will reshape supply chains, while the expansion of LNP-based therapies will support more flexible genetic delivery approaches.

As clinical pipelines multiply and commercial infrastructure strengthens, cell and gene therapy will no longer be considered advanced medicine. It will become standard medicine.

From oncology and rare diseases to regenerative health and chronic conditions, North America’s CGT market is on the brink of transforming how care is delivered, ushering in an era where genomic precision is expected, not exceptional.

Important Links:

Access our exclusive, data-rich dashboard dedicated to the therapeutic area sector – built specifically for decision-makers, strategists, and industry leaders. The dashboard features comprehensive statistical data, segment-wise market breakdowns, regional performance shares, detailed company profiles, annual updates, and much more. From market sizing to competitive intelligence, this powerful tool is one-stop solution to your gateway.

Access the Dashboard: https://www.towardshealthcare.com/access-dashboard

Checkout North America Cell and Gene Therapy Market Report Now at: https://www.towardshealthcare.com/checkout/6297

Become a valued research partner with us – https://www.towardshealthcare.com/schedule-meeting

You can place an order or ask any questions, please feel free to contact us at sales@towardshealthcare.com

Powering Healthcare Leaders with Real-Time Insights: https://www.towardshealthcare.com/healthcare-intelligence-platform

Europe Region – +44 778 256 0738

North America Region – +1 8044 4193 44

APAC Region: +91 9356 9282 04

Visit Our Website: https://www.towardshealthcare.com

Find us on social platforms: LinkedIn | Twitter | Instagram | Medium | Pinterest