Obesity is no longer a silent health concern tucked away in medical journals or policy discussions. It has become one of the defining public health challenges of the modern era, influencing healthcare systems, economies, and individual lives across continents. Over the past decade, the conversation around obesity has shifted dramatically. What was once framed largely as a lifestyle issue is now widely recognized as a chronic, multifactorial disease requiring long-term clinical management. This shift in understanding has laid the foundation for the extraordinary expansion of the global anti-obesity drugs market.

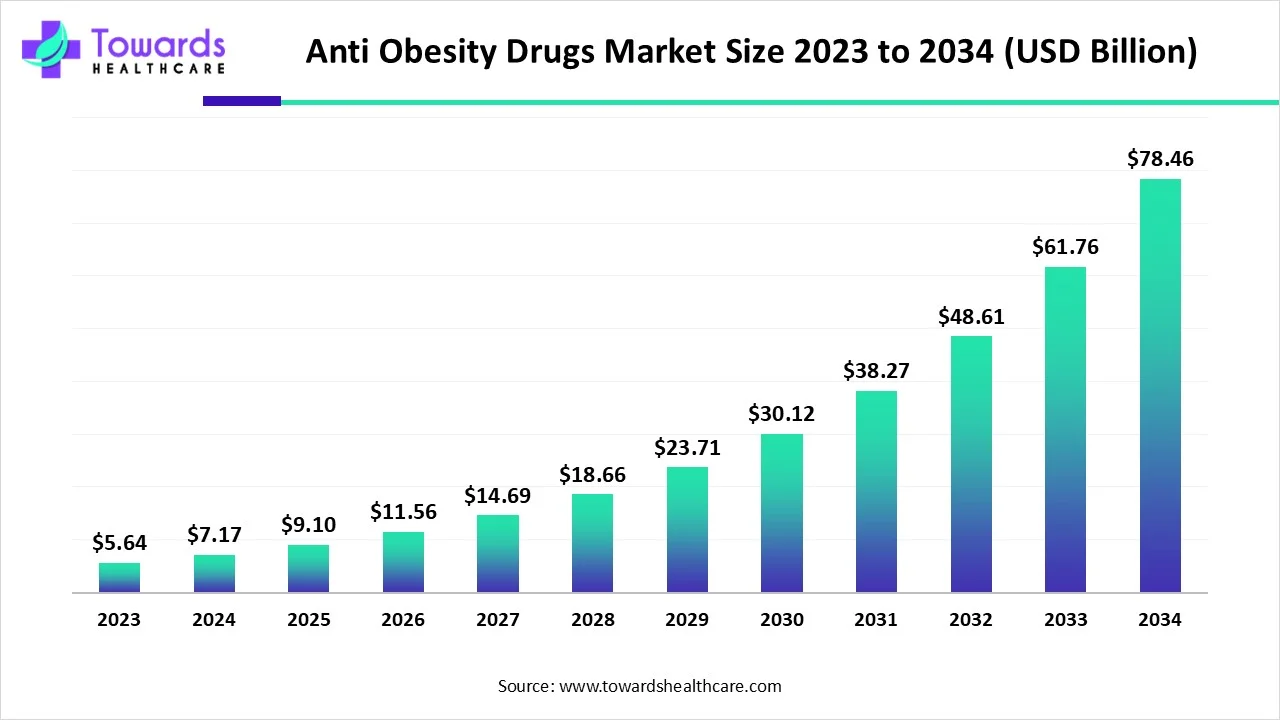

In 2024, the global anti-obesity drugs market stood at approximately USD 7.17 billion. By 2025, it grew to USD 9.1 billion, and projections suggest it could reach an unprecedented USD 78.46 billion by 2034, expanding at a compound annual growth rate of over 27 percent. These figures are not just indicators of commercial opportunity. They reflect a deeper transformation in how societies perceive obesity, how clinicians approach treatment, and how pharmaceutical innovation responds to unmet medical needs.

Download Free Sample Now and Get the Complete Report Easily at: https://www.towardshealthcare.com/download-sample/5513

From Willpower to Biology: A Fundamental Shift in Obesity Treatment

For decades, obesity treatment revolved around calorie restriction, physical activity, and behavioral counseling. While these interventions remain foundational, real-world evidence consistently shows that lifestyle modification alone often fails to deliver sustained weight loss for individuals with moderate to severe obesity. Biological mechanisms, including hormonal regulation, appetite signaling, metabolic adaptation, and genetic predisposition, actively resist long-term weight reduction.

Modern anti-obesity drugs address this biological reality. Current-generation therapies can deliver weight reductions exceeding ten percent, with some agents demonstrating even higher efficacy in clinical trials. This has changed the tone of the conversation among physicians and patients alike. Pharmacotherapy is no longer viewed as a last resort but as an essential component of comprehensive obesity care, particularly for individuals with comorbidities such as type 2 diabetes, cardiovascular disease, and metabolic syndrome.

Why the Market Is Accelerating So Rapidly

The explosive growth of the anti-obesity drugs market is rooted in a convergence of structural and societal forces. Obesity rates have tripled globally over the past few decades, with more than 650 million people now classified as obese. Urbanization, sedentary work patterns, high consumption of processed foods, and reduced physical activity have created an environment where weight gain is almost inevitable for large segments of the population.

At the same time, rising disposable incomes in both developed and emerging economies have increased willingness to pay for medical weight management solutions. Obesity is increasingly associated with long-term healthcare costs, reduced productivity, and diminished quality of life. As awareness grows, individuals are seeking proactive interventions rather than reactive treatment of downstream complications.

Digital health has also become a powerful catalyst. Telemedicine, online pharmacies, and virtual weight management platforms have expanded access to obesity treatments, particularly in remote or underserved regions. Patients can now consult physicians, receive prescriptions, and manage follow-ups without the traditional barriers of geography or time.

Prescription Therapies Take Center Stage

Prescription anti-obesity drugs dominate the current market landscape, accounting for the largest share in 2024. These therapies target diverse physiological pathways, including appetite regulation, satiety signaling, fat absorption, and energy expenditure. Clinical data consistently demonstrate that patients using prescription drugs alongside lifestyle interventions achieve significantly greater weight loss than those relying on lifestyle changes alone.

What makes prescription therapies particularly compelling is not just the magnitude of weight loss but its durability. Sustained reductions of ten percent or more can meaningfully lower the risk of cardiovascular disease, improve glycemic control, and reduce the burden of obesity-related complications. As researchers continue to refine dosing strategies and combination therapies, prescription drugs are expected to remain the backbone of pharmacological obesity management.

OTC Solutions and the Rise of Self-Care Culture

While prescription drugs dominate today, over-the-counter anti-obesity products are gaining momentum. The global healthcare ecosystem is increasingly embracing self-care as a strategic necessity. OTC solutions offer accessibility, convenience, and autonomy, allowing individuals to take early action without navigating complex healthcare pathways.

In many markets, OTC products serve as entry points for weight management, particularly among individuals with mild obesity or overweight conditions. As regulatory frameworks evolve and consumer trust grows, this segment is poised for lucrative growth over the coming decade. The expansion of e-commerce platforms further amplifies this trend, bringing OTC options directly to consumers’ doorsteps.

Central vs. Peripheral Action: A Scientific Balancing Act

Anti-obesity drugs can broadly be categorized by their mechanism of action, with centrally acting and peripherally acting agents shaping the therapeutic landscape. Centrally acting drugs, which influence appetite and satiety through the brain, dominated the market in 2024. Advances in formulation and combination therapy have reduced side effects while improving efficacy, making these agents more acceptable for long-term use.

Peripherally acting drugs, which target processes such as fat absorption without altering central nervous system pathways, are gaining traction. These therapies appeal to patients who are sensitive to neurological side effects or who prefer mechanisms that act outside the brain. Over the forecast period, peripherally acting drugs are expected to capture substantial market share, reflecting a broader shift toward personalized treatment strategies.

Retail Pharmacies Hold the Fort, While E-Commerce Redefines Access

Retail pharmacies continue to serve as the primary distribution channel for anti-obesity drugs, supported by insurance coverage, established supply chains, and patient trust. In many countries, retail pharmacies are deeply integrated into national healthcare systems, playing a critical role in chronic disease management.

However, the fastest growth is occurring in e-commerce. Digital pharmacies are transforming how patients access medications, offering home delivery, teleconsultations, AI-powered chat support, and medication education. As regulatory oversight strengthens and digital literacy improves, online channels are expected to reshape the pharmaceutical retail landscape, particularly for chronic conditions like obesity.

Artificial Intelligence Enters the Equation

Artificial intelligence and advanced analytics are quietly but profoundly reshaping the anti-obesity drugs market. In drug discovery, AI accelerates the identification of novel targets and candidate molecules by analyzing vast datasets that would be impossible for humans to process manually. This reduces development timelines and lowers research costs, enabling faster entry of innovative therapies into clinical trials.

In manufacturing, automation ensures consistent quality and scalability, addressing one of the key challenges in meeting surging global demand. On the clinical side, AI-driven algorithms support personalized medicine by analyzing patient-specific data such as genetics, metabolic markers, and treatment response. This allows clinicians to tailor therapies with greater precision, improving outcomes while minimizing adverse effects.

The Persistent Shadow of Risk and Regulation

Despite remarkable progress, the anti-obesity drugs market faces significant challenges. Safety concerns remain a critical restraint. Historical precedents, such as the withdrawal of fenfluramine due to cardiovascular risks, continue to shape regulatory scrutiny and physician caution. Even approved drugs like orlistat face limitations due to gastrointestinal side effects that affect patient adherence.

Regulators walk a fine line between enabling innovation and ensuring patient safety. Long-term data on cardiovascular outcomes, metabolic effects, and overall mortality remain essential for broad adoption. The industry’s ability to address these concerns transparently will determine the sustainability of its growth.

Research and Development as the Market’s Lifeblood

The future of anti-obesity pharmacotherapy lies in relentless research and development. Pharmaceutical companies are racing to create first-in-class and best-in-class therapies that deliver superior efficacy with fewer side effects. Researchers are exploring gene therapy, co-therapy combinations, and novel dosing regimens to overcome physiological resistance to weight loss.

The pipeline of preclinical and clinical candidates continues to expand, reflecting both the scale of unmet need and the commercial potential of successful therapies. As scientific understanding of appetite regulation and energy balance deepens, the next generation of drugs may redefine what is possible in obesity care.

North America Sets the Pace

North America led the global anti-obesity drugs market in 2024, driven by high obesity prevalence, strong healthcare infrastructure, and the presence of major pharmaceutical players. Strategic collaborations, mergers, and acquisitions continue to shape the competitive landscape, while academic and clinical research adds depth to treatment strategies.

In the United States, obesity affects a growing proportion of both adults and children. Projections suggest that by 2050, nearly two-thirds of Americans could be overweight or obese. This demographic reality is fueling demand for effective pharmacological interventions, supported by increasing awareness of obesity’s links to cancer, diabetes, and cardiovascular disease.

Canada’s Structured Approach to Obesity Management

Canada presents a distinct but equally compelling case. With a significant portion of its population classified as overweight or obese, the country has adopted an integrated approach to chronic disease prevention. Government collaboration with healthcare stakeholders emphasizes long-term management rather than short-term fixes. The approval of multiple prescription anti-obesity drugs reflects a regulatory environment that recognizes obesity as a treatable medical condition.

Asia Pacific Emerges as the Growth Engine

Asia Pacific is poised to become the fastest-growing regional market for anti-obesity drugs. Rising disposable incomes, urbanization, and changing dietary patterns have accelerated obesity rates across countries such as China, India, and South Korea. Governments are responding with public awareness campaigns, healthcare reforms, and increased support for pharmaceutical innovation.

China’s aggressive focus on weight control highlights the scale of the challenge. With nearly half of its adult population classified as overweight or obese, the country has become a focal point for both domestic and international drug developers. India, facing a parallel rise in obesity and diabetes, has begun approving advanced therapies, signaling a new phase in its approach to metabolic health.

Europe’s Policy-Driven Momentum

Europe’s anti-obesity drugs market benefits from strong healthcare systems, proactive government policies, and a growing emphasis on preventive care. Countries such as Germany, France, and the United Kingdom are integrating pharmacotherapy into structured disease management programs. Regulatory approvals at the regional level continue to expand treatment options, reinforcing Europe’s role as a significant contributor to global market growth.

An Industry Defined by Responsibility

Beyond revenue and growth projections, the anti-obesity drugs market carries a profound ethical responsibility. Obesity is deeply intertwined with social determinants of health, including income, education, and access to nutritious food. Pharmacological solutions must complement, not replace, broader public health initiatives aimed at prevention and equity.

The most successful companies in this space will be those that recognize obesity not as a short-term commercial opportunity but as a long-term healthcare commitment. Transparency, patient education, and collaboration with healthcare providers will be essential in building trust and ensuring sustainable impact.

Access our exclusive, data-rich dashboard dedicated to the therapeutic area sector – built specifically for decision-makers, strategists, and industry leaders. The dashboard features comprehensive statistical data, segment-wise market breakdowns, regional performance shares, detailed company profiles, annual updates, and much more. From market sizing to competitive intelligence, this powerful tool is one-stop solution to your gateway.

Access the Dashboard: https://www.towardshealthcare.com/access-dashboard

Checkout Anti-Obesity Drugs Market Report Now at: https://www.towardshealthcare.com/checkout/5513

Become a valued research partner with us - https://www.towardshealthcare.com/schedule-meeting

You can place an order or ask any questions, please feel free to contact us at [email protected]

Powering Healthcare Leaders with Real-Time Insights: https://www.towardshealthcare.com/healthcare-intelligence-platform

Europe Region – +44 778 256 0738

North America Region – +1 8044 4193 44

APAC Region: +91 9356 9282 04

Visit Our Website: https://www.towardshealthcare.com

Find us on social platforms: LinkedIn | Twitter | Instagram | Medium | Pinterest