The global human insulin market stands at a defining moment. As diabetes tightens its grip on populations across continents, insulin, one of modern medicine’s most transformative discoveries, continues to anchor treatment strategies. Yet the story unfolding today goes beyond steady demand curves and product launches. It reflects demographic shifts, healthcare modernization, digital health integration, biosimilar disruption, and the moral urgency of affordability.

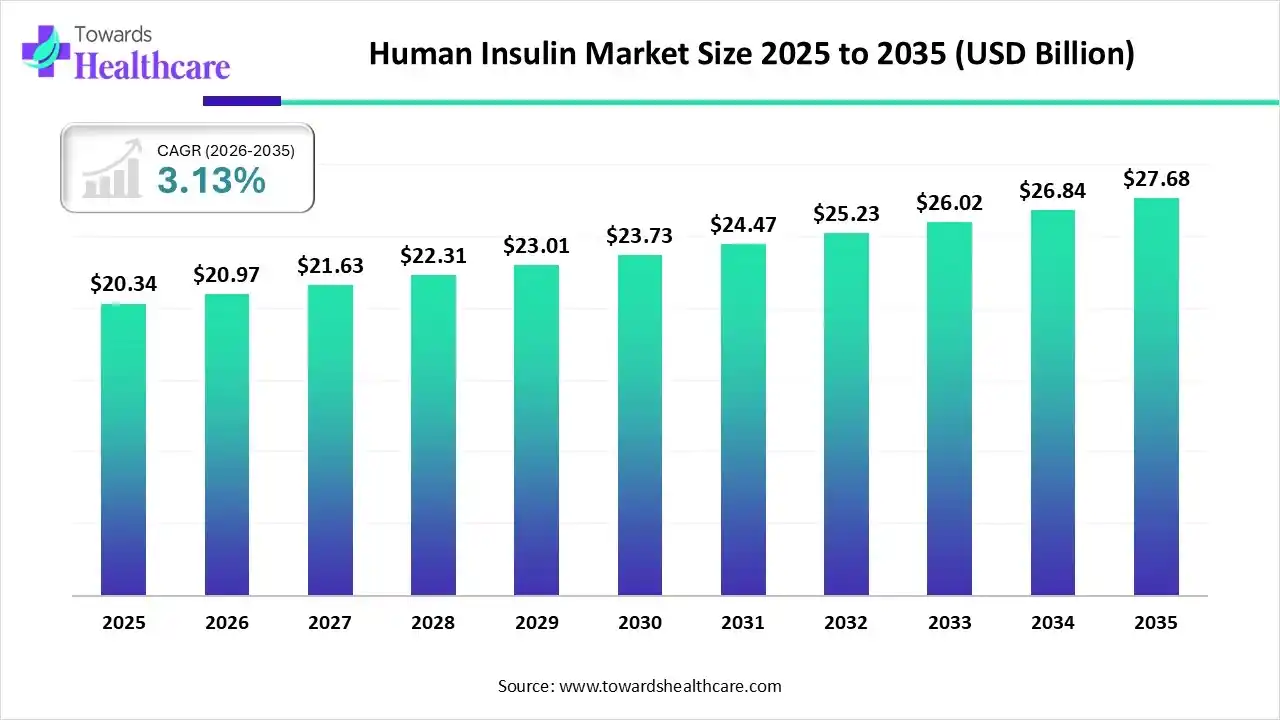

In 2025, the global human insulin market reached an estimated value of USD 20.34 billion. It is projected to grow from USD 20.97 billion in 2026 to nearly USD 27.68 billion by 2035, expanding at a compound annual growth rate (CAGR) of 3.13% between 2026 and 2035. These figures reveal stability, but the forces shaping this market signal far deeper structural transformation.

Download the Free Customized Sample Report: https://www.towardshealthcare.com/download-sample/6501

This is not merely a growth story. It is a global health narrative.

The Expanding Diabetes Burden: A Relentless Driver

Diabetes has shifted from a chronic condition affecting limited populations to a global epidemic with sweeping consequences. In 2024, approximately 589 million people worldwide lived with diabetes. By 2050, that number could rise to 853 million.

The surge is not confined to high-income nations. Emerging economies, rapid urbanization, aging populations, sedentary lifestyles, and dietary transitions are accelerating incidence rates across Asia Pacific, the Middle East, Africa, and Latin America.

Insulin remains essential—especially for individuals with type 1 diabetes, who depend entirely on external insulin for survival. Meanwhile, an increasing number of type 2 diabetes patients require insulin therapy as disease progression limits oral medication efficacy.

This rising clinical need forms the backbone of the human insulin market.

What Defines Human Insulin in Today’s Landscape?

Human insulin is biologically identical to endogenous insulin and is typically produced using recombinant DNA technology. It regulates blood glucose levels by facilitating cellular glucose uptake and preventing hyperglycemia-related complications.

The market includes several key product categories:

-

Rapid-acting insulin (e.g., insulin aspart, insulin lispro)

-

Short-acting insulin (regular insulin)

-

Intermediate-acting insulin (NPH insulin)

-

Long-acting insulin (insulin glargine, insulin detemir)

In 2025, rapid-acting insulin dominated the market, accounting for approximately 50% of total share. Clinicians favor it for post-meal glucose control and flexible dosing. However, long-acting insulin is expected to grow at the fastest rate, with an anticipated CAGR of 8.0% during the forecast period. Once-daily dosing and reduced hypoglycemia risk enhance patient adherence and long-term management.

North America Leads—But Asia Pacific Accelerates

Regional dynamics reveal two powerful narratives: dominance and acceleration.

North America captured around 40% of the global human insulin market in 2025. A sophisticated healthcare infrastructure, early adoption of insulin analogs, high diagnosis rates, and strong reimbursement mechanisms underpin this leadership. The United States remains the primary revenue generator within the region, driven by technological innovation and high per capita healthcare expenditure.

Yet the fastest growth emerges elsewhere.

Asia Pacific is projected to grow at a CAGR of 9.0% between 2026 and 2035. Expanding healthcare access, large diabetic populations, rising awareness, and government initiatives drive adoption. India, in particular, reflects a dramatic trajectory: diabetes cases rose from 32.7 million in 2000 to 89.8 million in 2024, and projections suggest they could reach 156.7 million by 2050.

Europe also presents steady momentum. With an aging population and rising type 2 diabetes incidence, countries such as the UK and Germany increasingly adopt biosimilar insulin products under strong reimbursement frameworks.

The geography of insulin demand is shifting—and manufacturers are responding.

The Rise of Biosimilars: Affordability Meets Competition

Affordability remains one of the most sensitive and debated dimensions of the insulin ecosystem. As biologic therapies, insulin products historically carried significant manufacturing complexity and regulatory scrutiny, often translating into high costs.

Biosimilars are altering this equation.

As patents expire and regulatory pathways mature, manufacturers are introducing biosimilar insulin products that offer comparable efficacy and safety at reduced costs. These alternatives improve accessibility, particularly in middle-income economies where price sensitivity remains high.

In recent years, several insulin analog biosimilars have gained regulatory approval, signaling intensifying competition. As governments seek to contain healthcare expenditures, biosimilars may redefine procurement strategies, reimbursement models, and market share distribution.

This shift introduces both opportunity and strategic recalibration for established players.

Smart Technology Changes the Insulin Conversation

Insulin therapy no longer revolves solely around the molecule. The delivery ecosystem is evolving rapidly.

Manufacturers now integrate artificial intelligence into insulin management systems. AI algorithms analyze glucose patterns, personalize dosing recommendations, and assist in real-time adjustments. Remote monitoring platforms enable clinicians to track patient adherence and glycemic control from afar.

Smart insulin pumps, wearable continuous glucose monitors (CGMs), and connected pen devices increasingly define modern diabetes care. These technologies reduce dosing errors, enhance patient autonomy, and improve clinical outcomes.

The injectable segment continues to dominate, accounting for 65% of the market in 2025 due to precise dosing and rapid absorption. However, inhalable insulin is projected to grow at an 8.5% CAGR. Its non-invasive nature and portability appeal to patients seeking alternatives to daily injections.

The human insulin market is becoming as much about digital integration as pharmacology.

Hospitals Hold Ground—But Homecare Expands

In 2025, hospitals represented approximately 45% of market share among end users. Hospitals remain primary sites for insulin initiation, complex case management, and inpatient diabetes control. Trained professionals ensure safe titration and monitor adverse effects.

However, the homecare segment is poised for the fastest expansion, with an expected CAGR of 8.0%. Several forces drive this transition:

-

Increased patient education

-

Growth of telemedicine platforms

-

Digital health monitoring tools

-

Desire for convenience and autonomy

Patients increasingly self-administer insulin and rely on connected devices for tracking and feedback. This decentralization of care signals a structural shift in diabetes management.

Distribution channels mirror this pattern. Hospital pharmacies still dominate with a 45% share, but online pharmacies are growing at a 9.0% CAGR, driven by home delivery models and broader product availability.

Healthcare is moving closer to the patient.

Innovation Pipeline: Beyond Daily Injections

Research and development teams focus on more than incremental improvements. They aim to redefine insulin therapy itself.

Current innovation priorities include:

-

Once-weekly basal insulin formulations

-

Heat-stable insulin products

-

Smart microneedle patches

-

Ultra-rapid onset analogs

-

Integrated insulin pump systems

Recent funding rounds and product approvals highlight sustained investor confidence. Companies are developing smaller insulin patch pumps, improving portability and patient comfort. Others are pursuing heat-stable formulations to address cold-chain limitations in low-resource settings.

Manufacturing remains complex. Human insulin production demands stringent biotechnological processes and temperature-controlled logistics. Cold-chain dependency continues to restrict distribution in certain regions, creating both a challenge and an innovation opportunity.

SWOT Snapshot: Stability Meets Structural Pressures

Strengths

-

Essential therapy for type 1 diabetes

-

Strong clinical efficacy and safety track record

-

Government reimbursement programs

-

Expanding long-acting insulin adoption

Weaknesses

-

High production and retail costs

-

Hypoglycemia risk

-

Complex manufacturing requirements

Opportunities

-

Rising early diagnosis rates

-

Growth of biosimilars

-

Smart delivery devices

-

Remote patient monitoring ecosystems

Threats

-

Cold-chain logistics constraints

-

Pricing scrutiny

-

Competitive biosimilar pressure

-

Regulatory stringency

The market rests on a stable therapeutic foundation but faces constant pressure to balance affordability, innovation, and accessibility.

The Value Chain: From Lab Bench to Bedside

The human insulin value chain reflects scientific rigor and regulatory oversight.

Research & Development

Companies focus on molecule optimization, stability enhancement, and delivery innovation. The goal: extend duration, reduce side effects, and simplify administration.

Clinical Trials & Regulatory Approval

Manufacturers must demonstrate bioequivalence, safety, and efficacy. Regulatory bodies closely examine biosimilars to ensure parity with originator products.

Manufacturing

Recombinant DNA production requires advanced bioreactors, purification systems, and strict quality control standards.

Distribution

Cold storage remains mandatory. Efficient logistics networks determine access in remote or resource-limited regions.

Patient Support Services

Educational programs, copay assistance initiatives, and injection training improve adherence and long-term outcomes.

Each stage demands precision and compliance.

Market Leaders and Competitive Landscape

The competitive environment features established pharmaceutical giants and regional biosimilar manufacturers.

Key participants include:

-

Novo Nordisk

-

Sanofi

-

Eli Lilly and Company

-

Biocon Limited

-

Wockhardt Limited

-

Boehringer Ingelheim

-

Medtronic

-

AstraZeneca

These companies compete across product portfolios, biosimilar development, digital health integration, and geographic expansion.

Strategic collaborations between pharmaceutical firms and device manufacturers increasingly define competitive positioning.

Access our exclusive, data-rich dashboard dedicated to the pharmaceuticals market – built specifically for decision-makers, strategists, and industry leaders. The dashboard features comprehensive statistical data, segment-wise market breakdowns, regional performance shares, detailed company profiles, annual updates, and much more. From market sizing to competitive intelligence, this powerful tool is one-stop solution to your gateway.

Access the Dashboard: https://www.towardshealthcare.com/access-dashboard

Checkout Human Insulin Market Report Now at: https://www.towardshealthcare.com/checkout/6501

You can place an order or ask any questions, please feel free to contact us at [email protected]

Europe Region – +44 778 256 0738

North America Region – +1 8044 4193 44

APAC Region: +91 9356 9282 04

Visit Our Website: https://www.towardshealthcare.com

Find us on social platforms: LinkedIn | Twitter | Instagram | Medium | Pinterest