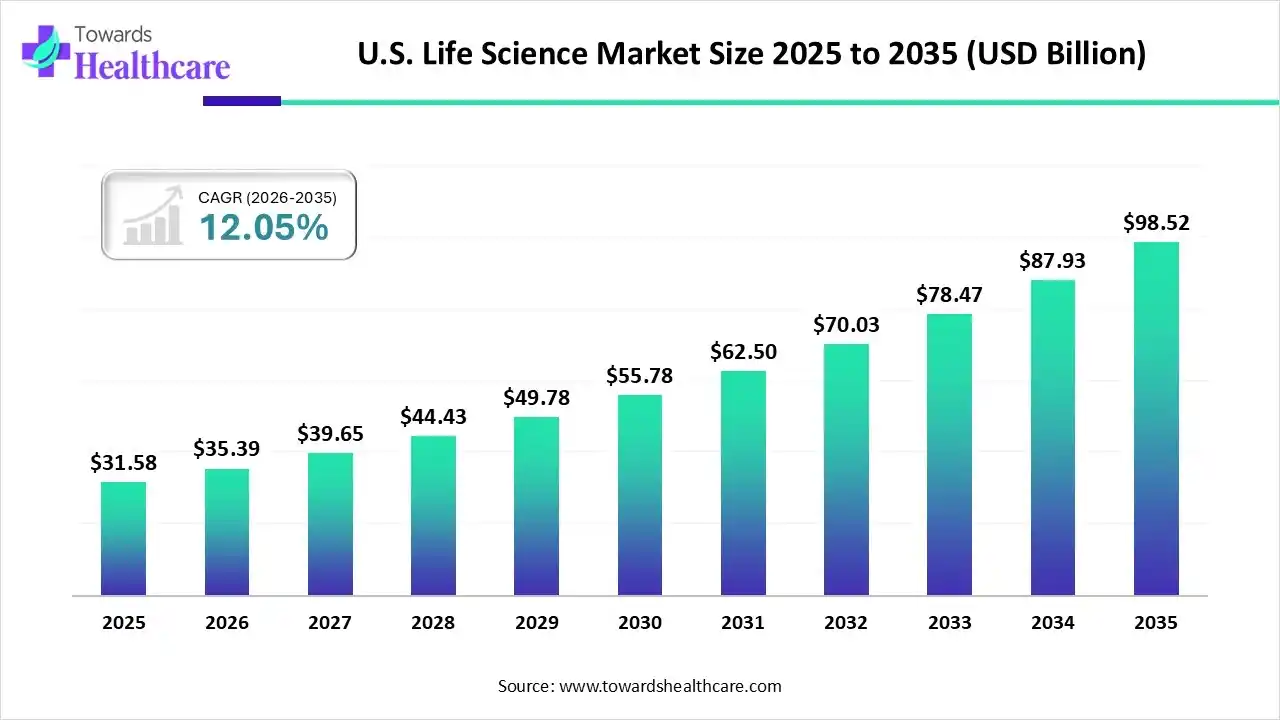

The U.S. life sciences industry is not simply growing; it is transforming. In 2025, the U.S. life science market stood at US$ 31.58 billion. By 2026, it is expected to reach US$ 35.39 billion, and by 2035, it is projected to climb to US$ 98.52 billion, expanding at a robust CAGR of 12.05% between 2026 and 2035.

Download Free Sample Report Easily: https://www.towardshealthcare.com/download-sample/6001

These figures reflect more than financial expansion. They signal a structural shift in how medicine is discovered, developed, manufactured, and delivered. From AI-driven drug discovery to gene editing, from precision oncology to sustainable laboratories, the U.S. life sciences ecosystem is building the blueprint for the future of healthcare.

The New Engine of American Healthcare

Life sciences sit at the intersection of biology, medicine, engineering, and data science. In the United States, this ecosystem includes:

-

Biopharmaceuticals

-

Medical devices

-

Diagnostics and clinical laboratories

-

Genomics and precision medicine

-

Contract research and manufacturing services (CROs and CDMOs)

-

Laboratory technologies, reagents, and analytical tools

What sets the U.S. apart is the integration of research institutions, venture capital, biotech startups, large pharmaceutical enterprises, federal funding, and advanced clinical infrastructure. Together, these components form a self-reinforcing innovation engine.

Technology Is Not Supporting Healthcare; It Is Driving It

The rapid adoption of next-generation sequencing (NGS), CRISPR gene editing, and artificial intelligence has accelerated innovation cycles. These technologies no longer operate in silos; they integrate into drug pipelines, clinical trials, diagnostics platforms, and manufacturing workflows.

Artificial intelligence, in particular, has emerged as a force multiplier.

AI models now:

-

Identify drug targets faster

-

Predict molecular interactions

-

Optimize clinical trial recruitment

-

Analyze complex genomic datasets

-

Enable personalized treatment planning

Organizations such as Moderna and Pfizer have demonstrated how digital tools can compress development timelines. Meanwhile, companies like Eli Lilly are integrating advanced analytics into R&D processes to enhance therapeutic precision.

This digital acceleration is not theoretical. It is operational.

Biopharma Leads the Charge

In 2025, the biopharma and pharmaceutical segment held approximately 45% of the U.S. life science market. Demand for innovative therapies, biologics, gene therapies, and targeted small molecules continues to surge.

Patients now expect treatments that:

-

Target specific genetic mutations

-

Minimize systemic side effects

-

Address rare and complex conditions

-

Improve long-term quality of life

Companies such as Amgen, AbbVie, and Regeneron Pharmaceuticals are expanding portfolios in oncology, immunology, and rare diseases. The focus has shifted from broad-spectrum therapies to highly targeted, biomarker-driven approaches.

This transformation reflects a larger healthcare evolution: treating individuals rather than populations.

CROs and CDMOs: The Silent Powerhouses

While biopharma commands headlines, contract research organizations (CROs) and contract development and manufacturing organizations (CDMOs) are shaping the market’s fastest-growing segment.

CROs and CDMOs enable:

-

Clinical trial management

-

Drug formulation and scale-up

-

Regulatory consulting

-

Biologics manufacturing

-

Post-market surveillance

Industry leaders such as IQVIA are expanding global capabilities through acquisitions and digital integration. The outsourcing model reduces cost burdens for biotech startups while increasing speed-to-market.

As drug pipelines become more complex, collaboration becomes essential. The modern pharmaceutical landscape depends on distributed expertise.

Precision Medicine Is Becoming the Standard

Precision medicine is no longer experimental—it is operational. The integration of genomics, biomarkers, AI analytics, and real-world data has redefined therapeutic strategies.

Sequencing platforms from companies like Illumina enable clinicians to analyze genetic profiles at unprecedented speed. Meanwhile, AI platforms interpret these datasets to recommend targeted therapies.

The rise of multi-cancer early detection (MCED), in vivo gene editing, and personalized oncology reflects a shift from reactive treatment to predictive medicine.

Patients increasingly demand care that matches their biology—not averages.

Federal Funding Fuels the Innovation Pipeline

The U.S. government remains a critical pillar of the life sciences ecosystem. Federal funding for medical research continues to drive early-stage discoveries and clinical expansion.

In fiscal year 2024, nearly half of NIH funding flowed to the top five life sciences states, with California leading. These investments support:

-

University-based translational research

-

Public-private partnerships

-

Clinical trial expansion

-

Biomedical workforce development

Regulatory approvals also reflect strong momentum. The FDA authorized 59 medications through the third quarter of 2024—nearly a record year. While only 12–14% of drugs entering clinical trials ultimately gain approval, the pipeline remains active and competitive.

High risk continues to coexist with high reward.

Clinical Trials Are Expanding in Scale and Complexity

Over the past two decades, U.S. clinical trials have expanded rapidly. In 2024, registered studies reached a new high.

Later-stage trials now require:

-

Larger patient populations

-

Diverse demographic representation

-

Complex data monitoring systems

-

Decentralized trial models

Digital recruitment platforms, remote monitoring tools, and AI-driven patient matching are reducing bottlenecks. Pharmaceutical leaders such as Bristol Myers Squibb and Vertex Pharmaceuticals are leveraging adaptive trial designs to improve efficiency.

Clinical research has become both more inclusive and more data-intensive.

The Distribution Backbone: Logistics at National Scale

Innovation does not stop at discovery. It extends to distribution.

The “Big Three” wholesalers—McKesson, Cencora, and Cardinal Health—manage high-volume logistics systems that move therapies from manufacturing plants to hospitals and pharmacies.

Cold chain integrity, serialization, and anti-counterfeiting measures have become essential. Automated unique device identifiers and real-time tracking ensure regulatory compliance and patient safety.

Distribution is no longer back-end support—it is strategic infrastructure.

Sustainability: The Industry’s Next Imperative

The life sciences sector consumes significant energy and resources. The pharmaceutical industry alone contributes approximately 4.4% of global emissions.

Researchers and manufacturers are now prioritizing:

-

Energy-efficient laboratories

-

Reduced packaging waste

-

Sustainable consumables

-

Extended instrument life cycles

-

Greener manufacturing practices

Sustainability initiatives align environmental responsibility with operational efficiency. Laboratories are adopting energy monitoring systems and exploring circular economy models.

Environmental stewardship is shifting from optional to essential.

AI: The Central Nervous System of Modern Life Sciences

Artificial intelligence has evolved from an experimental tool to an operational backbone.

AI accelerates:

-

Drug target identification

-

Molecular modeling

-

Toxicity prediction

-

Clinical trial optimization

-

Regulatory documentation

Institutions such as Mount Sinai are integrating AI with advanced chemistry and biology to shorten development timelines. Generative AI platforms now propose new molecular structures and simulate clinical outcomes before human trials begin.

The industry is moving toward predictive medicine at scale.

Recent Industry Developments Signal Acceleration

The pace of announcements reflects strong forward momentum.

-

Merck initiated construction of a $1 billion biologics center of excellence in Delaware to support next-generation therapies, including antibody-drug conjugates.

-

Celltrion USA launched biosimilars referencing denosumab products in the U.S., increasing market competition.

-

SK Life Science expanded direct-to-consumer awareness campaigns to address neurological conditions.

These developments highlight diversification, manufacturing expansion, and patient-centered engagement.

The Global Context: America at the Center

Globally, the life science market is projected to grow from US$ 88.2 billion in 2024 to US$ 269.56 billion by 2034, at a CAGR of 11.82%.

The United States remains a dominant contributor due to:

-

Advanced regulatory infrastructure

-

Strong intellectual property protection

-

Venture capital ecosystems

-

Academic research networks

-

Biotech clustering in regions such as the Northeast, West Coast, and Midwest

International companies such as Roche, Novo Nordisk, and Genmab continue to invest heavily in U.S. operations.

America functions not just as a market—but as a global innovation hub.

Market Drivers: Demand Is Structural, Not Cyclical

Several structural forces underpin the 12.05% projected CAGR:

-

Aging Population – Chronic diseases increase therapeutic demand.

-

Chronic Illness Prevalence – Cancer, autoimmune disorders, and metabolic diseases require advanced interventions.

-

Personalized Medicine Expansion – Biomarker-driven therapies gain acceptance.

-

Digital Health Integration – AI enhances productivity across pipelines.

-

Venture Capital Revival – IPO activity signals renewed investor confidence.

These drivers reflect long-term demographic and technological realities.

Challenges That Demand Strategic Response

Despite growth, the sector faces constraints:

-

Supply chain vulnerabilities

-

Geopolitical disruptions

-

Regulatory complexity

-

High development costs

-

Skilled workforce shortages

Companies must diversify manufacturing bases and strengthen domestic production capabilities. The pandemic exposed the risks of over-reliance on single geographies.

Resilience now ranks alongside innovation as a strategic priority.

The Regional Fabric of Innovation

Each U.S. region contributes distinct strengths:

-

Northeast: Academic research hubs and biotech startups

-

West: Genomics, digital health, venture capital

-

Midwest: Manufacturing and clinical trial expansion

-

South: Emerging biotech clusters and infrastructure investment

Regional diversification reduces systemic risk while expanding capacity.

Value Chain: From Discovery to Patient Support

The U.S. life science value chain spans multiple high-complexity stages:

R&D: Generative AI-driven discovery and gene editing

Clinical Trials: Safety validation and regulatory approval

Manufacturing: Biologics scale-up and serialization

Distribution: National logistics and cold-chain management

Patient Support: Adherence coaching and digital engagement

Companies like Johnson & Johnson and Laboratory Corporation of America integrate across multiple value chain segments, increasing operational leverage.

A Decade That Will Define Healthcare

By 2035, the U.S. life science market may approach US$ 100 billion. But the real transformation lies beyond numbers.

The industry is:

-

Moving from generalized medicine to precision therapies

-

Shifting from manual research to AI-guided discovery

-

Transitioning from reactive care to predictive intervention

-

Redesigning laboratories for sustainability

-

Expanding access through biosimilars and biologics

Innovation cycles are shortening. Collaboration networks are expanding. Investment remains strong.

The next decade will not simply advance medicine—it will redefine it.

Conclusion: Innovation with Responsibility

The U.S. life sciences sector stands at a pivotal moment. Growth remains strong, technological adoption accelerates, and global leadership continues.

Yet success will depend on balancing speed with safety, profitability with accessibility, and innovation with sustainability.

If current momentum continues, the U.S. life sciences industry will not only reach US$ 98.52 billion by 2035—it will set new global standards for how healthcare systems innovate, deliver, and evolve.

The transformation has already begun.

Access our exclusive, data-rich dashboard dedicated to the life science industry – built specifically for decision-makers, strategists, and industry leaders. The dashboard features comprehensive statistical data, segment-wise market breakdowns, regional performance shares, detailed company profiles, annual updates, and much more. From market sizing to competitive intelligence, this powerful tool is one-stop solution to your gateway.

Access the Dashboard: https://www.towardshealthcare.com/access-dashboard

Checkout U.S. Life Science Market Report Now at: https://www.towardshealthcare.com/checkout/6001

You can place an order or ask any questions, please feel free to contact us at [email protected]

Europe Region – +44 778 256 0738

North America Region – +1 8044 4193 44

APAC Region: +91 9356 9282 04

Visit Our Website: https://www.towardshealthcare.com

Find us on social platforms: LinkedIn | Twitter | Instagram | Medium | Pinterest