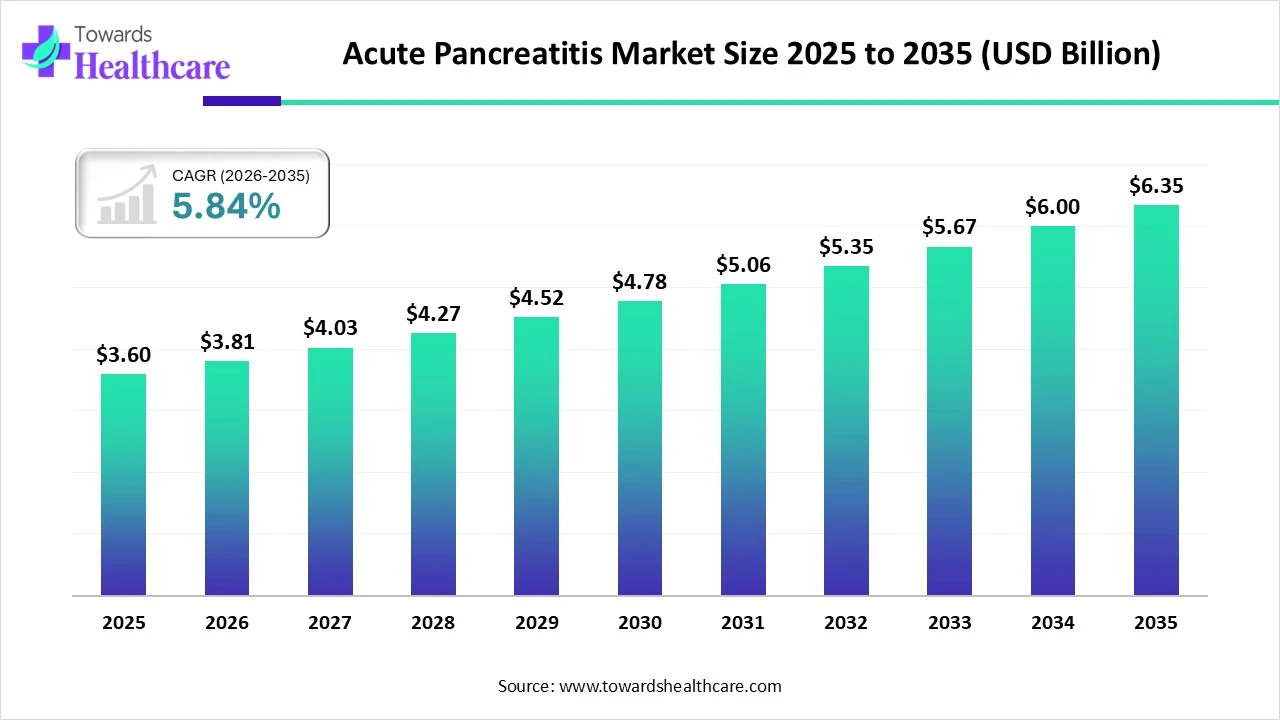

The global acute pancreatitis market valued at USD 3.6 billion in 2025, rising to USD 3.81 billion in 2026 is projected to reach about USD 6.35 billion by 2035, growing at a CAGR of 5.84% thanks to rising incidence, improved diagnostics, and greater adoption of minimally invasive and supportive therapies.

Download Free Sample of Acute Pancreatitis Market Now and Get the Complete Report Easily at: https://www.towardshealthcare.com/download-sample/6451

Market Size

Base Value (2025): USD 3.6 billion.

Near-Term Value (2026): USD 3.81 billion.

Long-Term Projection (2035): USD 6.35 billion.

Compound Annual Growth Rate (2026–2035): 5.84%.

Segment Shares (as of 2024):

Supportive care: 45% of market revenue.

Mild acute pancreatitis (by severity): 55%.

Hospitals (as end‑user): 65%.

Intravenous route (of administration): 50%.

Hospital pharmacies (distribution channel): 55%.

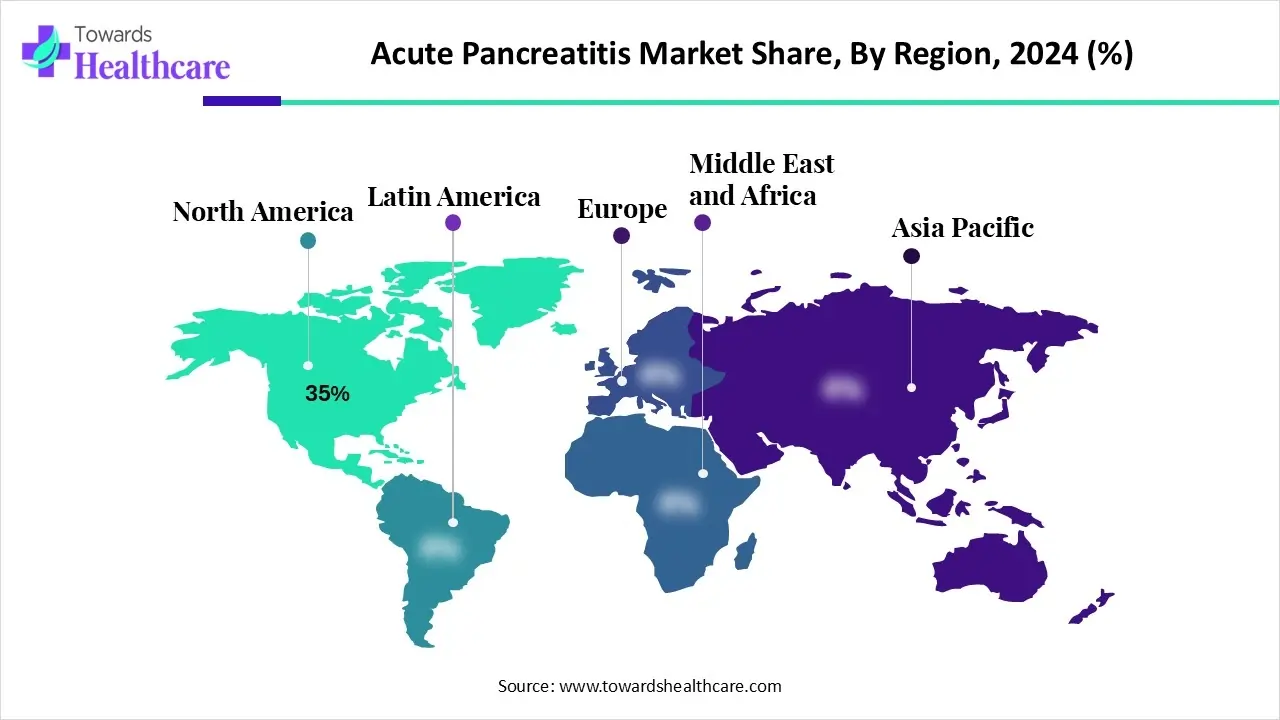

Regional: North America accounted for 35% of total market revenues; Asia Pacific poised to grow fastest (10% CAGR).

Market Trends

Growing Disease Prevalence & Changing Risk Profile

Rising incidence of gallstone disease, alcohol use, obesity, hypertriglyceridemia globally — all classical risk factors for AP.

As these risk factors spread (especially in developing regions), more cases of AP are likely, driving demand for diagnosis and treatment.

Improved Diagnostics and Early Detection

Wider use of imaging (CT, MRI, endoscopic ultrasound) enables earlier and more accurate diagnosis. This helps in early intervention which may reduce complications and shift treatment toward less intensive care.

Early detection also fuels demand for imaging services and follow-up care, expanding the market ecosystem.

Supportive Care as the Backbone of Treatment

Supportive care (IV fluids, pain relief, nutritional support) remains the dominant treatment paradigm (45% share in 2024), reflecting that many AP cases are managed conservatively rather than via surgery or aggressive interventions.

As supportive care protocols become more standardized and fluid/nutrition products improve, their adoption stays stable or grows.

Rise of Minimally Invasive & Endoscopic Interventions

Endoscopic procedures (e.g. ERCP, EUS-guided drainage) are gaining popularity because they are less invasive than open surgery, with shorter recovery and fewer complications.

This trend likely fuels growth in equipment, endoscopes, anesthesia support, and hospital services — expanding the overall market beyond just pharmaceuticals.

Increasing Demand for Pharmacotherapy & Novel Therapeutics

Traditional pharmacotherapy (analgesics, anti‑inflammatories, enzyme modulators, antibiotics) remains essential, especially in severe cases.

As research into novel therapies (e.g. enzyme inhibitors, anti‑inflammatory biologics) advances, the pharmacotherapy segment is expected to grow significantly.

Growing Need for Nutritional Support

Enteral feeding (tube feeding) and parenteral nutrition are more widely accepted — especially in moderate to severe cases — boosting demand for nutrition products and feeding supplies.

Hospitals and specialty clinics offering nutritional support and critical‑care management stand to benefit.

Shift in Distribution Channels

While hospital pharmacies remain dominant (55% in 2024), there is growing potential for online pharmacies and direct-to-patient models — particularly for supportive care drugs and nutrition products.

This shift could improve accessibility in remote or underserved regions.

Regional Shifts — Emerging Markets Growing Faster

Developed markets (North America, Europe) remain stable due to established infrastructure; but emerging regions (Asia Pacific, Latin America, MEA) show higher growth potential, driven by changing lifestyle, rising healthcare access, and growing awareness.

Increase in Hospital & Specialized Care Utilization

Given that 65% of demand (2024) came from hospitals, there’s rising pressure to upgrade hospital infrastructure, ICU capacity, monitoring, fluid management, endoscopy suites — which drives investment in medical devices, IV systems, imaging, etc.

Growing Focus on Post-Acute Care & Prevention

As recurrence risk and complications (necrosis, organ failure) become better understood, there is greater emphasis on follow-up care, prophylactic interventions, lifestyle counseling — expanding the market sideways into supportive services, patient education, and chronic‑disease management.

10 Roles / Potential Impact of AI in the Acute Pancreatitis Market

AI (machine learning, deep learning, predictive analytics) — though more recently mentioned — can significantly transform the AP market. Here are ten detailed roles / impacts, with explanations:

Early and Accurate Diagnosis via Imaging Analysis

AI algorithms can analyze CT, MRI, and endoscopic‑ultrasound images to detect subtle signs of pancreatic inflammation, edema, or early necrosis — potentially before human radiologists can reliably do so.

This leads to earlier intervention, reducing complications, treatment costs, and improving patient outcomes.

Risk Stratification & Prognosis Prediction

By feeding clinical data (blood biomarkers, vitals, imaging features) into ML models, AI can predict which patients are likely to progress from mild to severe AP.

This helps doctors decide who needs intensive care vs conservative care — optimizing resource use and reducing mortality.

Personalized Treatment Planning

AI-driven decision-support tools can recommend tailored treatment plans (IV fluids volume/rate, nutrition route, drug combinations) based on individual patient’s risk profile and comorbidities.

Personalized care improves efficacy and reduces unnecessary interventions.

Predicting Complications & Need for Interventions

Models can forecast complications such as necrosis, pseudocysts, organ failure, or infection — triggering preventive measures or early interventions.

Optimizing Nutritional Support & Enteral Feeding Timings

AI can help determine the optimal timing for initiating enteral feeding (vs keeping patient nil-per-oral) based on real‑time monitoring (inflammation markers, vitals), improving recovery and reducing gut-related complications.

Drug Discovery & Novel Therapeutic Development

AI and network‑pharmacology platforms can accelerate identification of new molecules (e.g. anti‑inflammatory agents, enzyme inhibitors) by predicting which compounds may block pathological pathways in AP.

This reduces R&D time and cost, potentially leading to better pharmacotherapies.

Clinical Trial Optimization

For new therapies (biologics, enzyme inhibitors), AI can help identify optimal patient subgroups, predict which patients are most likely to respond, and monitor safety signals — increasing success rates of trials.

Hospital Resource Management

AI‑powered dashboards can forecast ICU bed occupancy, fluid/nutrition demand, staffing needs, and endoscopy scheduling — helping hospitals manage capacity and cost.

Post‑Discharge Monitoring & Recurrence Prevention

AI-driven mobile apps or remote-monitoring tools can track patient vitals, dietary compliance, recurrence signs — alerting physicians early if relapse is likely.

Epidemiological Surveillance & Public Health Planning

Aggregated data from hospitals, imaging centers, pharmacies can be analyzed via AI to detect regional trends (rising AP incidence due to alcohol, obesity, hyperlipidemia) — helping health authorities allocate resources or launch prevention campaigns.

Thus, AI integration has the potential not only to improve clinical outcomes but also to expand and reshape the entire acute pancreatitis market — from diagnostics to treatment, patient‑management, and public health.

Regional Insights

North America

Market Dominance (35% share as of 2024): Mature healthcare infrastructure, widespread use of advanced diagnostics (CT, MRI, EUS), high hospital penetration — ensures stable demand for AP diagnosis and treatment.

High Incidence of Risk Factors: Obesity, gallstones, alcohol use — contribute to steady AP case load.

Strong R&D and Adoption of Novel Therapies: Large pharmaceutical/biotech presence encourages development and use of advanced pharmacotherapy and supportive care regimens.

Asia Pacific (Fastest Growth 10% CAGR)

Rapid Lifestyle Changes: Urbanization, rising obesity, alcohol consumption, altered diets increase risk factors for AP.

Improving Healthcare Infrastructure: Expansion of hospitals, diagnostic centers, endoscopy units; growing access to critical care and supportive nutrition — expands addressable patient pool.

Untapped Market Potential: Lower base penetration compared to Western markets — greater scope for growth in diagnostics, nutrition support, hospital services, and novel therapies.

Europe

Advanced Medical Systems: High access to minimally invasive procedures, endoscopy, imaging — similar to North America, though growth may be slower due to mature market.

Focus on Minimally Invasive & Supportive Care: Emphasis on cost-efficient care, hospital-based supportive treatment, and outpatient follow-up.

South America

Emerging Healthcare Access: As hospitals and diagnostic services expand, regions like Brazil will see increased diagnosis and treatment rates.

Rising Risk Factors: Alcohol consumption, gallstones, obesity — contribute to growing AP incidence.

Middle East & Africa (MEA)

Expanding Healthcare Spending: Investments in hospital infrastructure, critical‑care units, nutrition support may grow demand.

Rising Lifestyle Disorders: Increasing obesity and triglyceride disorders may raise AP incidence.

Potential Challenges: Access to advanced diagnostics and novel therapies may lag — but growing awareness can gradually drive growth.

Market Dynamics

Drivers:

Rising incidence of AP due to gallstones, alcohol use, hypertriglyceridemia, obesity.

Improved diagnostics (imaging, endoscopy) enabling early detection.

Growing adoption of minimally invasive procedures (endoscopy, ERCP/EUS drainage).

Increased demand for supportive care, IV fluids, nutrition support, pain management.

Rising penetration of hospital pharmacies, IV products, enteral feeding supplies.

Expanding healthcare access in emerging regions, driving incremental patient volume.

Growing interest and R&D in novel pharmacotherapies / biologics for severe cases.

Shift toward ambulatory care settings and outpatient follow-up for mild cases.

Challenges / Restraints:

Many AP cases are mild and self‑limiting — which may limit demand for high‑cost interventions or novel therapeutics (market saturation in mild segment).

High cost of advanced imaging and endoscopic interventions may limit access in low-resource settings.

Variation in treatment protocols — some patients may receive minimal supportive care only, limiting uniform market growth.

Regulatory and clinical-trial hurdles for novel therapies (especially biologics / enzyme modulators) — long development timelines.

Recurrence risk and chronicity can be unpredictable — complicating long-term market forecasting.

Opportunities:

Growing unmet need for better therapies to treat moderate to severe AP / prevent complications.

Expansion of outpatient and ambulatory‑surgical settings for mild/moderate AP management.

Rising adoption of enteral nutrition and advanced nutrition products in moderate/severe cases.

Increase in online pharmacy and direct‑to-patient distribution channels.

Use of AI and digital health to streamline diagnosis, monitoring, and personalized care.

Outlook (2025–2035): Given the steady growth in risk factors, expanding healthcare infrastructure globally, and rising demand for minimally invasive and supportive therapies, the market is likely to see continued double‑digit growth in certain segments (e.g., diagnostics, nutrition support, endoscopy), even if mature segments (supportive care in hospitals) grow more moderately.

Top 10 Companies in Acute Pancreatitis Market (Pointwise)

Pfizer

Offers analgesics, antibiotics, and sterile injectables for supportive care in AP.

Strength: Global reach, diversified portfolio, strong hospital supply chains, widely adopted in supportive care.

Merck & Co.

Provides supportive care drugs used in AP, including pain relievers and antibiotics.

Strength: Large R&D infrastructure, global distribution, trusted by hospitals across multiple therapeutic areas.

Baxter International

Supplies intravenous (IV) fluids and sterile IV administration sets critical for AP fluid resuscitation.

Strength: Leader in hospital IV solutions, strong global supply, and critical-care product suite.

Abbott Laboratories

Offers IV fluids, nutritional products (enteral/parenteral), and diagnostic tools/assays.

Strength: Diversified offerings combining nutrition, diagnostics, and fluid management; broad hospital presence.

B. Braun SE

Provides IV solutions, infusion pumps, pain therapy systems, and surgical/supportive-care products.

Strength: Expertise in fluid management and precise drug delivery, essential for controlled supportive care.

CalciMedica Inc.

Develops novel therapeutics such as CRAC channel inhibitors targeting severe AP with organ failure.

Strength: Focus on root-cause therapeutics, potential to address unmet needs in severe AP cases, innovative pipeline.

Fresenius SE & Co.

Supplies hospital care products, nutrition, dialysis/critical-care support relevant to AP complications.

Strength: Strong presence in critical care, global reach, able to support AP complication management (e.g., renal, ICU).

Olympus Corporation

Produces endoscopic equipment for ERCP and EUS used in minimally invasive AP interventions.

Strength: Leader in endoscopy equipment, enabling hospitals to adopt minimally invasive procedures.

Boston Scientific Corporation

Offers endoscopy tools and interventional devices (drainage, stents) for managing AP complications.

Strength: Strong portfolio in interventional gastroenterology, global distribution, trusted by hospitals.

Medtronic

Provides critical-care and monitoring systems, fluid delivery pumps, and supportive-care devices.

Strength: Broad critical-care infrastructure, integration in hospital ICU workflows, supports severe AP management.

Latest Announcements & Recent Developments

In September 2025, Ionis Pharmaceuticals (via “Olezarsen” trials) reportedly showed that Olezarsen led to an 85% reduction in acute pancreatitis events and up to 72% reduction in fasting triglycerides, compared with placebo — a potentially major breakthrough for prevention/therapy of hypertriglyceridemia‑induced AP.

In August 2025, Arctx Medical announced new leadership and received FDA IDE approval for a pivotal clinical trial of its “ACC kit” for AP treatment — signaling entry of new device‑ or therapy‑based solutions into AP care.

These developments reflect growing industry interest in both novel pharmacologic therapies and innovative device‑based interventions / kits beyond conventional supportive care or endoscopy — which may reshape market dynamics in coming years.

Market Segments Covered

By Treatment Type:

-

Supportive Care (IV fluids, pain management, nutrition)

-

Pharmacotherapy (antibiotics, enzyme modulators, anti‑inflammatory agents)

-

Endoscopic Interventions (ERCP, EUS-guided drainage)

-

Surgical Interventions (e.g. necrosectomy, gallbladder removal)

-

Nutritional Support (enteral feeding, parenteral nutrition)

Explanation: This captures the full spectrum of AP management — from conservative care to invasive procedures to nutrition and drug therapy.

By Severity Type:

-

Mild Acute Pancreatitis

-

Moderately Severe Acute Pancreatitis

-

Severe Acute Pancreatitis

Explanation: Severity influences treatment approach: mild cases often need only supportive care; severe cases may require intensive care, interventions, or novel therapies.

By End-User:

-

Hospitals (general & specialty)

-

Ambulatory Surgical Centers (ASCs)

-

Diagnostic Imaging Centers

-

Clinics & Emergency Care Units

Explanation: Different care settings reflect where patients get diagnosed and treated — from emergency rooms to day-care ASCs to diagnostic centers for imaging.

By Route of Administration (for treatments):

-

Oral

-

Intravenous (IV)

-

Enteral Feeding Tubes

-

Parenteral Routes

Explanation: Reflects how treatments (fluids, nutrition, medications) are delivered depending on the patient’s condition and ability to tolerate oral intake.

By Distribution Channel:

-

Hospital Pharmacies

-

Retail Pharmacies

-

Online Pharmacies

-

Specialty Clinics / Direct Supply

Explanation: Captures how treatment products and medications reach patients — from in-hospital dispensing to retail and online pharmacies.

By Region:

-

North America (U.S., Canada, Mexico, etc.)

-

South America (e.g. Brazil, Argentina, others)

-

Europe (Western & Eastern)

-

Asia Pacific (China, India, Japan, ASEAN, etc.)

-

MEA (Middle East & Africa: GCC, other countries)

Explanation: Regional segmentation helps account for variations in healthcare infrastructure, disease prevalence, risk factors, and market growth potential.

This segmentation framework provides a comprehensive lens to analyze the acute pancreatitis market from multiple angles, addressing therapies, care settings, delivery methods, patients’ severity, and geography.

Top 5 FAQs

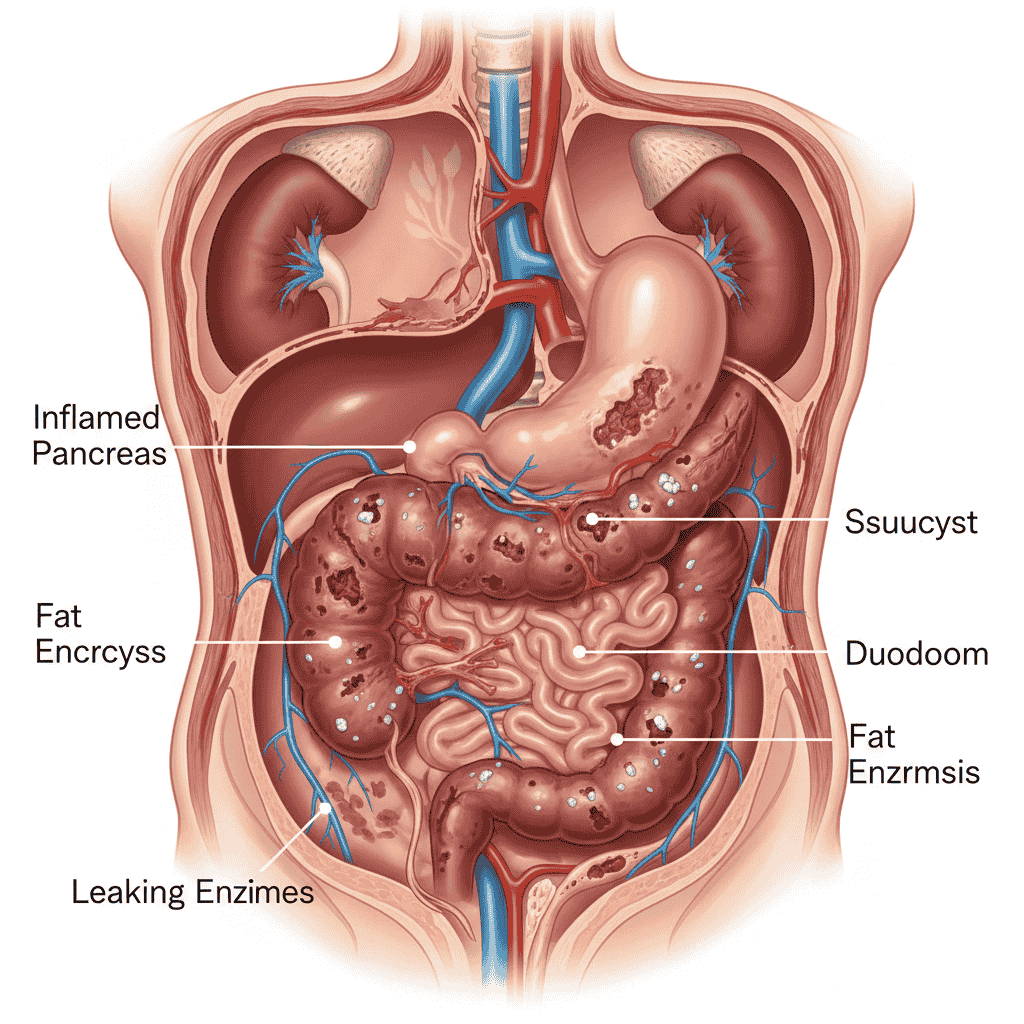

Q1: What is acute pancreatitis and how common is it?

A: Acute pancreatitis is a sudden inflammation of the pancreas, caused when digestive enzymes activate inside the pancreas and damage tissue. Most patients recover with treatment mild cases being common but about 15–20% develop more severe forms with risk of complications.

Q2: What is driving the growth of the acute pancreatitis market?

A: Rising incidence due to gallstones, alcohol use, obesity and hypertriglyceridemia; better diagnostic imaging; greater use of supportive care and minimally invasive interventions; and expansion of care infrastructure globally.

Q3: Which segment of the market currently holds the largest share?

A: As of 2024, supportive care dominates (≈ 45%), mild cases by severity (≈ 55%), hospitals as end-user (≈ 65%), intravenous route (≈ 50%), and hospital pharmacies as distribution channel (≈ 55%).

Q4: What is the projected market size by 2035 and the growth rate?

A: The market is expected to reach USD 6.35 billion by 2035, growing at a CAGR of 5.84% from 2026 to 2035.

Q5: Which companies lead the acute pancreatitis market and what do they offer?

A: Major players include pharmaceutical giants like Pfizer, Merck & Co., Baxter International, Abbott Laboratories, B. Braun SE offering supportive‑care drugs, IV fluids, nutrition, and hospital supplies; as well as device / interventional firms like Olympus Corporation, Boston Scientific, Medtronic, Fresenius enabling endoscopic or critical‑care interventions.

Access our exclusive, data-rich dashboard dedicated to the life science industry – built specifically for decision-makers, strategists, and industry leaders. The dashboard features comprehensive statistical data, segment-wise market breakdowns, regional performance shares, detailed company profiles, annual updates, and much more. From market sizing to competitive intelligence, this powerful tool is one-stop solution to your gateway.

Access the Dashboard: https://www.towardshealthcare.com/access-dashboard

Checkout Acute Pancreatitis Market Report Now at: https://www.towardshealthcare.com/checkout/6451

Become a valued research partner with us – https://www.towardshealthcare.com/schedule-meeting

You can place an order or ask any questions, please feel free to contact us at sales@towardshealthcare.com

Powering Healthcare Leaders with Real-Time Insights: https://www.towardshealthcare.com/healthcare-intelligence-platform

Europe Region – +44 778 256 0738

North America Region – +1 8044 4193 44

APAC Region: +91 9356 9282 04

Visit Our Website: https://www.towardshealthcare.com

Find us on social platforms: LinkedIn | Twitter | Instagram | Medium | Pinterest