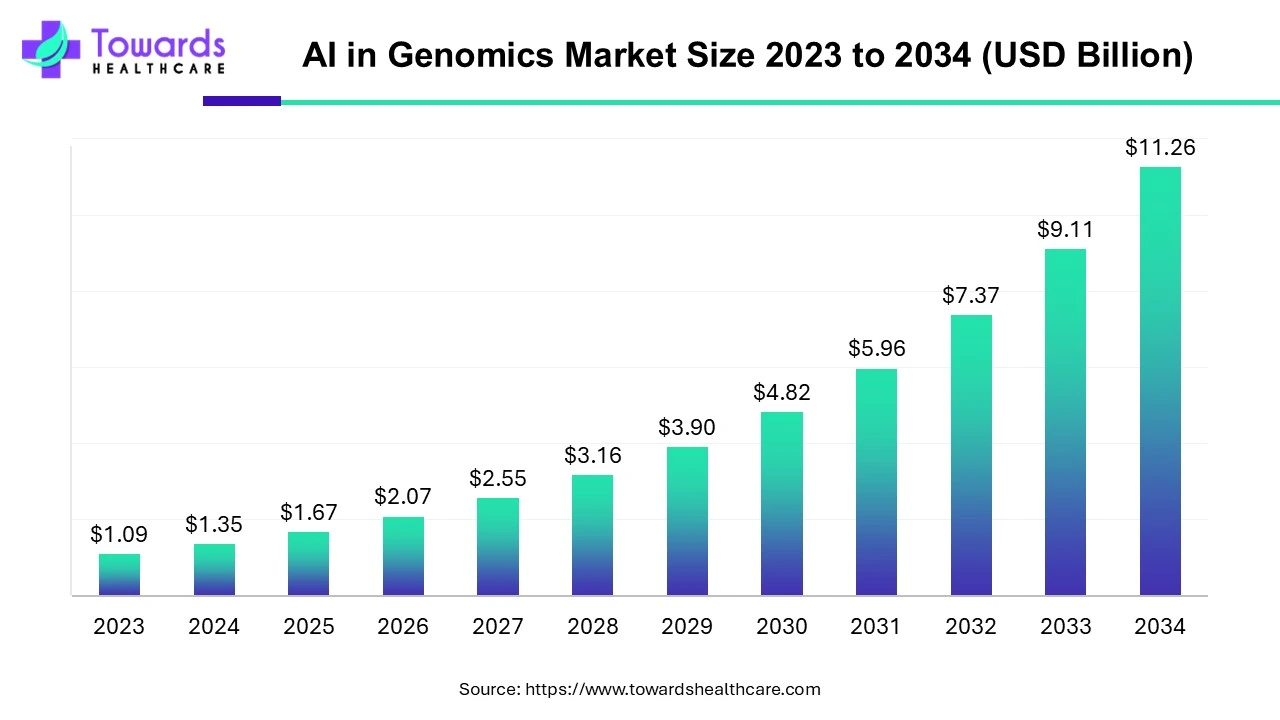

AI in Genomics Market Accelerates Growth from $1.67 Bn in 2025 to $11.26 Bn in 2034

The AI in genomics market is projected to grow from USD 1.67 billion in 2025 to USD 11.26 billion by 2034 (CAGR 23.6%), driven by rising R&D, cross-industry collaborations, and expanded clinical and commercial adoption.

Download the free sample and get the complete insights and forecasts report on this market @ https://www.towardshealthcare.com/download-sample/5046

Table of Contents

ToggleMarket size

Base & forecast figures

●Estimated market value: USD 1.67 billion (2025).

●Forecast value: USD 11.26 billion (2034).

●Compound annual growth rate (2025–2034): 23.6%.

Growth drivers quantified (relative emphasis)

●R&D and venture investment: accelerating funding for genomics/AI startups (supports high CAGR).

●Commercial deployments: increasing uptake by pharma/biotech, clinical labs, and DTC players (expands addressable market and recurring revenues).

●Government programs & grants: public funding (e.g., national strategies and awards) lowers risk for translation and adoption.

Component mix implication on revenue

●Software dominance (2024) implies high-margin recurring revenue potential (licenses, cloud/analysis platforms).

●Hardware and services remain important for one-time revenue and professional services uptake, but software will drive long-term ARR.

Technology mix impact on monetization

●Machine learning led share (2024) — broad applicability across interpretation, variant calling, and predictive models → multiple monetizable products.

●Emerging tech segments (computer vision, deep learning for multi-omics) will create new product categories and specialized services.

End-user spend behavior

●Pharma & biotech lead spend (2024) → larger, longer contracts and strategic partnerships.

●Healthcare providers fastest growth → smaller average contracts but high volume and potential for scale via SaaS/clinical decision support.

Geographic growth split

●North America: largest share (2024) — mature market, largest per-capita R&D spend.

●Asia-Pacific: fastest CAGR — emerging adoption, government prioritization, and large patient populations.

Market size sensitivity (key variables)

●Dependent on data access/standards, regulatory clarity (e.g., FDA guidance), and cost reductions in sequencing/NGS.

Addressable-market segmentation (revenue pools)

●Platform/software subscriptions & analysis fees (largest and fastest-growing revenue source).

●Professional services, validation & integration (moderate, one-time but recurring with upgrades).

●Hardware & sequencing consumables (steady, correlated with NGS adoption).

Timeframe to mainstream clinical revenue

●Expect bulk of growth from 2026–2032 as platforms move from pilot to scaled clinical use and pharma pipelines increasingly integrate AI genomics.

Investment implication

●High growth justifies continued VC/strategic acquisitions (e.g., 2025 M&A activity) and partnerships between sequencing, AI analytics, and healthcare incumbents.

Market Trends

Consolidation via M&A and acquisitions

●Example: Tempus AI acquired Ambry Genetics (Feb 2025) — strategic vertical integration of testing & AI interpretation.

●Implication: consolidation accelerates platform scale and vertical offerings.

Strategic alliances between tech and genomics

●Accenture’s investment in Ocean Genomics (Feb 2023) and Ultima Genomics + Genome Insight collaboration (Apr 2023) show sequencing + AI analysis bundling becoming standard.

Government-backed programs fueling translation

●UK NHS AI Lab awards, NSF expansion (May 2023), and national genomics investments (Canada, other nations) reduce commercialization risk and fund pilots.

Shift from research to clinical & commercial deployments

●Platforms evolving from research-only tools to clinical decision support and decentralized testing (e.g., GeneDx + Fabric Genomics acquisition aims at decentralized testing).

Lowering cost of sequencing enabling scale

●“$100 genome” initiatives (e.g., Ultima Genomics) combine with AI to make population-scale genomics commercially feasible.

Product diversification: DTC to enterprise

●Examples: Unite Genomics’ DTC platform (Dec 2024) and enterprise clinical platforms — market expanding across consumer, clinical, and pharma segments.

Rising regulatory guidance and scrutiny

●Regulatory agencies publishing AI considerations (e.g., FDA guidance referenced) increase compliance burdens but also legitimacy for clinical use.

Focus on precision medicine & pharmacogenomics

●Precision medicine identified as fastest-growing application; AI models increasingly used for drug response prediction and stratification.

Data privacy, standardization, and harmonization emphasis

●Push toward standards (GA4GH-like efforts implied) to mitigate data heterogeneity constraints and improve model generalizability.

Emergence of multimodal AI

●Combining genomics with phenotypes, EHRs and imaging (computer vision) to generate richer predictive models and broaden product capabilities.

AI impacts / roles in the AI in genomics market

High-throughput variant interpretation

●AI automates pathogenicity classification, prioritizes variants from millions of hits, and drastically reduces manual curation time.

Biomarker discovery and target identification

●Machine learning identifies patterns across cohorts to propose novel biomarkers and therapeutic targets, accelerating preclinical pipelines.

Patient stratification for trials

●AI models match genetic signatures to predicted drug response, improving cohort selection and boosting trial success probability.

Clinical decision support

●AI synthesizes genomic and clinical data to recommend diagnostics, treatment options, and pharmacogenomic guidance at point of care.

NGS data QC, harmonization & preprocessing

●AI flags sequencing artifacts, normalizes cross-platform differences, and standardizes datasets for downstream analysis.

Phenotype-to-genotype mapping via computer vision

●Image analysis (e.g., facial phenotyping or histology) links observable features to genomic variants, aiding rare disease diagnosis.

CRISPR and gene editing optimization

●Deep learning predicts off-target effects and optimizes guide RNA design, increasing editing precision.

End-to-end automation of genomic pipelines

●Software platforms orchestrate sample tracking, alignment, variant calling, annotation, and reporting — reducing time-to-result.

Population genetics and epidemiology at scale

●AI analyzes population datasets to track variant prevalence, predict outbreak dynamics, and inform public health decisions.

Drug repurposing and in-silico screening

●AI uses genomic signatures to match existing drugs to new indications or prioritize compounds for development, cutting discovery timelines.

Regional insights

North America — market leader

●Subpoint: Largest share in 2024 due to concentrated R&D, venture capital, and early regulatory frameworks.

●Explanation: High per-capita healthcare spend, large pharma/biotech presence, and government funding (NHGRI, etc.) create a robust demand and rapid adoption of AI genomics platforms.

Asia-Pacific — fastest growth

●Subpoint: Rapid government prioritization (China treating genomic data as strategic; India’s 9,000 biotech startups).

●Explanation: Large populations, rising healthcare investment, and national strategies translate to high absolute growth even from a smaller base; cost-sensitive solutions (e.g., low-cost sequencing + AI) scale rapidly.

Europe — regulated, innovation focused

●Subpoint: Strong research institutions and gene therapy demand; emphasis on privacy/regulatory compliance.

●Explanation: Europe balances innovation with strict data privacy (GDPR), creating opportunities for compliant AI platforms and partnerships with established clinical networks.

United Kingdom — NHS-driven adoption

●Subpoint: NHS AI Lab awards and other funding support pilot-to-clinic transitions.

●Explanation: Centralized healthcare systems (like the NHS) enable national implementations and faster evidence collection—helpful for clinical validation.

Germany — industrial R&D strength

●Subpoint: Academic–industry collaborations and regulatory alignment.

●Explanation: Germany’s manufacturing and biotech ecosystem fosters development of integrated solutions, especially for diagnostics and gene therapies.

Canada — strategic investments

●Subpoint: Large public investments (e.g., Genome Canada funds) to scale genomics infrastructure.

●Explanation: Public funding accelerates platform validation and national cohort studies useful for model training and validation.

India — growing startup ecosystem

●Subpoint: Local companies launching AI genomics diagnostics platforms (e.g., Bioheaven360 Genotec, May 2025).

●Explanation: Strong clinician networks and large patient pools make India attractive for both cost-effective solutions and clinical validation.

China — strategic data & scale

●Subpoint: State focus on treating genomic resources as national assets.

●Explanation: Centralized data initiatives and scale of sequencing efforts can fuel AI model training, though international data sharing may be constrained by policy.

Latin America & MEA — nascent but opportunistic

●Subpoint: Slower adoption but opportunity for leapfrog implementations with cloud-native AI solutions.

●Explanation: As sequencing costs fall, these regions can adopt turnkey AI genomics platforms to improve diagnostics where clinical genetics capacity is limited.

Cross-regional collaborations

●Subpoint: Partnerships (tech + genomics) are bridging capability gaps across regions (e.g., Ultima + Genome Insight).

●Explanation: Global collaborations allow technology transfer, shared best practices, and pooled datasets to improve model robustness.

Market dynamics

Demand drivers

●Rising incidence of chronic and genetic diseases; need for precision medicine; pharma investment in genomics-driven pipelines.

Supply-side forces

●Proliferation of AI software platforms, cheaper NGS, and specialized services (annotation, interpretation).

Regulatory environment

●Emerging guidance (FDA, other agencies) increases barriers to market entry but legitimizes clinical deployments, encouraging enterprise buyers.

Competitive dynamics

●Mix of big tech (IBM, Microsoft, NVIDIA), specialized AI genomics firms (SOPHiA GENETICS, Fabric Genomics), and startups — competition around data access, model performance, and clinical validation.

Technological substitution

●Advancements in ML and computer vision can replace manual curation and phenotype interpretation tasks, shifting labor needs.

Data & standards constraints

●Heterogeneous data formats and annotation gaps impede large-scale model generalizability — creates demand for harmonization services and standard formats.

Pricing & reimbursement

●Reimbursement uncertainty for genomic AI tools affects hospital adoption; pharma-sponsored deployments (RD partnerships) smooth commercialization.

Partnerships & M&A as go-to-market

●Strategic acquisitions (Tempus + Ambry; GeneDx + Fabric Genomics) accelerate access to clinical samples and testing networks.

Barriers to entry

●Need for clinical validation, regulatory compliance, access to large annotated datasets, and domain expertise.

Opportunities

●Democratization via DTC and centralized intelligence; expansion into healthcare provider workflows; move from research to real-world clinical decision support.

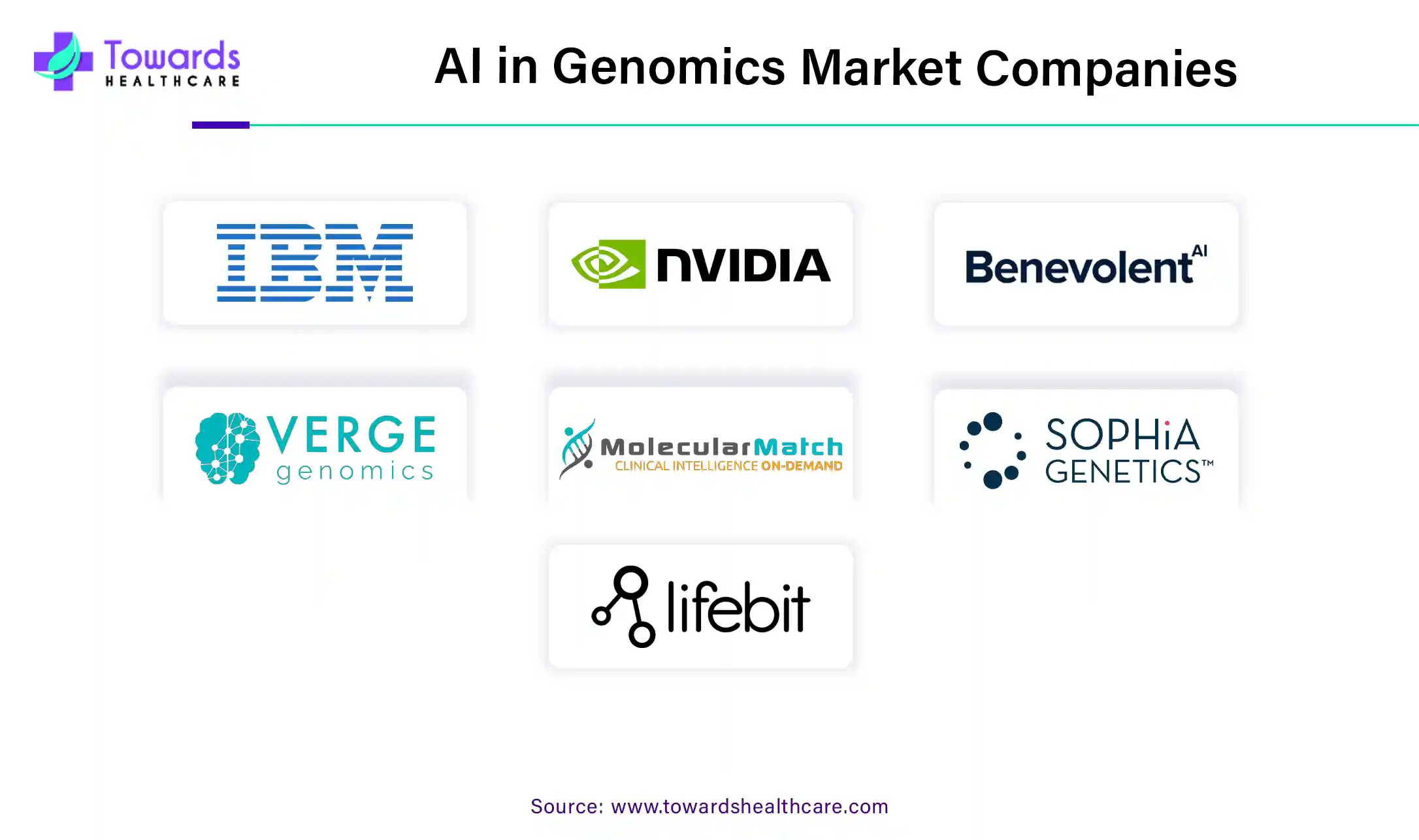

Top 10 companies

IBM

●Product/Overview: Enterprise AI platforms applied to health data and genomics workflows.

●Strength: Strong enterprise relationships and experience integrating clinical IT systems.

NVIDIA Corporation

●Product/Overview: Hardware (GPUs) and software stacks that accelerate ML/deep learning for genomics.

●Strength: Leading compute platform enabling large-scale model training and inference.

BenevolentAI

●Product/Overview: AI-driven drug discovery & development platforms leveraging genomics and other modalities.

●Strength: Focus on translational AI for target identification and drug discovery.

Verge Genomics

●Product/Overview: Genomics-centric AI for discovering therapeutic targets.

●Strength: Specialized in applying ML to genomic datasets to prioritize targets for neurology and other areas.

MolecularMatch, Inc.

●Product/Overview: Genomic interpretation and clinical decision support for oncology.

●Strength: Curated genomic–clinical databases and oncology-focused clinical workflows.

SOPHiA GENETICS

●Product/Overview: Multimodal AI platform for genomic data interpretation; engaged in clinical studies (e.g., UroCCR collaboration).

●Strength: Proven clinical collaborations and multimodal research capabilities.

PrecisionLife Ltd.

●Product/Overview: AI-driven analytics for complex disease stratification and biomarker discovery.

●Strength: Sophisticated patient stratification and multi-feature analysis capability.

Lifebit

●Product/Overview: Cloud-based genomics data platforms enabling large-scale analysis.

●Strength: Data orchestration, scalability, and reproducible workflows.

FDNA, Inc.

●Product/Overview: Phenotype-driven genomic interpretation (facial/clinical phenotype to genotype).

●Strength: Computer vision expertise linking phenotype and genotype, valuable for rare disease diagnosis.

Deep Genomics

●Product/Overview: AI approaches to predict genetic variant effects and guide therapeutic design.

●Strength: Variant effect prediction and expertise in molecular-level modeling for therapeutics.

Latest announcements

Tempus AI acquires Ambry Genetics (February 2025)

Details: Acquisition to combine Tempus’ AI/precision medicine capabilities with Ambry’s genetic testing footprint.

Strategic intent: Integrate testing and AI interpretation to offer end-to-end genomic diagnostics and accelerate clinical adoption.

GeneDx announced acquisition of Fabric Genomics (May 2025)

Details: Fabric Genomics — pioneer in AI-powered genomic interpretation; GeneDx aims to develop decentralized testing powered by centralized intelligence.

Strategic intent: Scale genomic testing while centralizing advanced AI interpretation to standardize care globally.

Bioheaven360 Genotec launches AI-powered genomics diagnostics platform in India (May 2025)

Details: Platform developed with AIIMS New Delhi; aimed at early detection and personalized treatment planning.

Strategic intent: Localized AI clinical solutions supporting precision medicine in Indian healthcare.

Unite Genomics launches DTC AI platform (Dec 2024)

Details: DTC platform analyzes care gaps and suggests missing tests/treatments; integrates EHR access for 90% of U.S. patients.

Strategic intent: Consumer and clinician engagement to unify patient data for proactive care.

SOPHiA GENETICS study with UroCCR (quote from Thierry Colin)

Details: Study to predict post-operative outcomes for renal cell carcinoma using multimodal AI.

Strategic intent: Clinical validation of AI in oncologic prognostication.

Recent developments

Multiple strategic investments and collaborations

Accenture’s investment in Ocean Genomics (Feb 2023) and Integrate.ai involvement in Canada (Feb 2023) demonstrate continued cross-sector partnerships to accelerate AI-driven discovery and precision health.

Government & public funding expansions

NSF expansion (May 2023) increasing AI research institutes; NHS AI Lab awards applied to health/AI projects (three rounds totaling ~$138M invested in technologies across 86 projects), which have impacted >300,000 patients.

Platform commercialization & DTC moves

Unite Genomics (Dec 2024) and Bioheaven360 (May 2025) illustrate movement toward consumer and local clinical markets.

Scientific advances

Google DeepMind (Sep 2023) — AI development to identify DNA changes that may cause disease, indicating progress in variant effect prediction.

Acquisition activity

Tempus + Ambry (Feb 2025), GeneDx + Fabric Genomics (May 2025) — consolidation to combine sequencing/testing capabilities with AI interpretation.

NGS cost reduction efforts

Ultima Genomics’ “$100 genome” collaboration with Genome Insight (Apr 2023) suggests cost declines enabling larger cohort sequencing.

Clinical validation focus

SOPHiA GENETICS’ work with UroCCR and other study partnerships highlight a trend toward publishing/validating clinical outcomes to support adoption.

Localized market launches

India example: Bioheaven360 + AIIMS collaboration shows national adaptation and clinical trials bridging technology to local health systems.

Decentralized testing models

GeneDx’s stated aim to combine decentralized testing with centralized intelligence signals a hybrid operational model for scaling genomic testing.

Rise of multimodal AI techniques

Increasing attention to combining genomics with phenotype, imaging (computer vision), and clinical data to improve diagnosis and treatment recommendations.

Segments covered

By Component

Hardware

●Subpoint: Sequencers, GPUs and edge devices required for data generation and model training.

●Explanation: Hardware supports throughput and latency requirements for NGS and ML model workloads.

Software

●Subpoint: Analysis platforms, interpretation engines, clinical decision support — dominant in 2024.

●Explanation: Software enables value capture via subscriptions, updates, and integrations; high margins and scale.

Services

●Subpoint: Professional services, clinical validation, consulting and managed analysis.

●Explanation: Services help customers implement, validate, and clinicalize AI genomics solutions.

By Technology

Machine Learning

●Subpoint: Largest share (2024) covering variant calling, predictive models.

●Explanation: ML is versatile and forms the backbone of most genomic AI workflows.

Deep Learning

●Subpoint: Used for complex pattern recognition and molecular modeling.

●Explanation: Useful in multi-omics integration and sequence-to-function predictions.

Computer Vision

●Subpoint: Growing use in phenotyping and histopathology analysis.

●Explanation: Bridges imaging data with genomic interpretation for richer diagnostics.

Supervised / Unsupervised / Reinforcement Learning

●Subpoint: Methodologies applied depending on label availability and use case.

●Explanation: Supervised for clinical outcomes, unsupervised for clustering/phenotyping, reinforcement for iterative optimization tasks.

By Functionality

Genome Sequencing

●Subpoint: Led in 2024; base for downstream AI analysis.

●Explanation: Sequencing is the raw data input; costs and throughput determine market expansion.

Gene Editing

●Subpoint: AI supports guide design and off-target prediction.

●Explanation: Ties genomics AI to therapeutic development and precision editing workflows.

Others

●Subpoint: Annotation, multi-omics integration, population analytics.

●Explanation: Additional modules that increase platform stickiness.

By End-User

Pharmaceutical & Biotech Companies

●Subpoint: Dominant spenders, using genomics for drug discovery and stratification.

●Explanation: They provide larger, longer contracts and are primary early adopters.

Healthcare Providers

●Subpoint: Fastest growth — clinical diagnostics and personalized care adoption.

●Explanation: Clinical workflows and provider integration are the next major revenue source.

Research Centers / Others

●Subpoint: Academia and public health institutions for discovery and validation.

●Explanation: Serve as testing grounds and generate annotated datasets for AI models.

Top 5 FAQs

Q1 — What is the projected market size and growth rate for AI in genomics?

A — Projected to grow from USD 1.67 billion (2025) to USD 11.26 billion (2034) at a 23.6% CAGR.

Q2 — Which component or segment leads revenue?

A — Software dominated in 2024 and is expected to expand rapidly, representing the primary high-margin revenue pool.

Q3 — Which technologies are most important?

A — Machine learning held the largest market share in 2024; computer vision and other deep learning approaches are significant growth areas.

Q4 — Which end users spend the most and which are growing fastest?

A — Pharmaceutical & biotechnology companies dominated spend in 2024; healthcare providers are the fastest-growing end-user segment.

Q 5— What are the main barriers to growth?

A — Data quality and standardization challenges, regulatory complexity, privacy concerns, and the need for clinical validation are the primary restraints.

Access our exclusive, data-rich dashboard dedicated to the biotechnology sector – built specifically for decision-makers, strategists, and industry leaders. The dashboard features comprehensive statistical data, segment-wise market breakdowns, regional performance shares, detailed company profiles, annual updates, and much more. From market sizing to competitive intelligence, this powerful tool is one-stop solution to your gateway.

Access the Dashboard: https://www.towardshealthcare.com/access-dashboard

Immediate Delivery Available | Buy This Premium Research @ https://www.towardshealthcare.com/price/5046

Become a valued research partner with us – https://www.towardshealthcare.com/schedule-meeting

You can place an order or ask any questions, please feel free to contact us at sales@towardshealthcare.com

Powering Healthcare Leaders with Real-Time Insights: https://www.towardshealthcare.com/healthcare-intelligence-platform

Europe Region – +44 778 256 0738

North America Region – +1 8044 4193 44

APAC Region: +91 9356 9282 04

Web: https://www.towardshealthcare.com

Find us on social platforms: LinkedIn | Twitter | Instagram | Medium | Pinterest