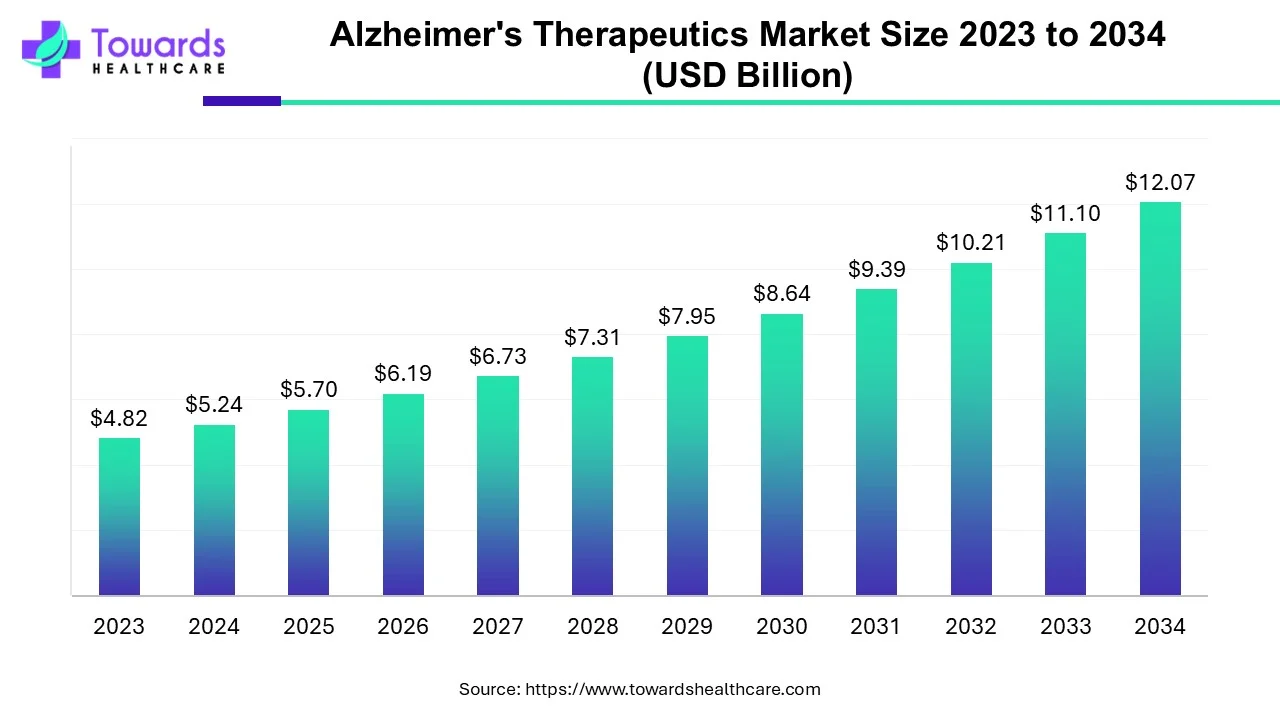

The Alzheimer’s therapeutics market will grow from USD 5.7 billion in 2025 to USD 12.07 billion by 2034 at a CAGR of 8.7%, driven by rising patient numbers, aging demographics, AI-powered R&D, and new therapeutic approvals.

Download this Free Sample Now and Get the Complete Report and Insights of this Market Easily @ https://www.towardshealthcare.com/download-sample/5130

Market Size Insights

2023 Baseline

➣Estimated market size: USD 5.4 billion.

➣Growth driven by existing cholinesterase inhibitors and NMDA antagonists.

➣Mostly symptomatic treatments, limited disease-modifying drugs.

2024 Dominance

➣North America led due to FDA approvals (Leqembi, Adlarity patch).

➣Cholinesterase inhibitors still account for majority prescriptions.

2025 Market Value: USD 5.7B

➣Drivers: Increasing prevalence in elderly (6.7M Americans).

➣End-user: Hospital pharmacies dominate distribution.

2026–2027 Growth

➣Early-onset dementia recognition (29,000 cases in 2024 projected to 41,000 by 2054).

➣More patients identified younger → earlier treatment demand.

Pipeline Expansion

➣127 drugs across 164 clinical trials (2024).

➣Includes amyloid/tau therapies, inflammation blockers, and nanomedicine.

2030 Milestone: >USD 9B

➣New entrants like tau-targeting drugs in Phase 3 drive revenue.

➣Digital health integration improves compliance.

2034 Forecast: USD 12.07B

➣Nearly double from 2025, CAGR 8.7%.

➣Driven by both symptomatic and disease-modifying therapies.

Hospital Pharmacy Strength

➣Benefits from routine checkups and clinical trials.

➣Sub-subpoint: Access to MRI/PET scans supports diagnosis-linked treatment sales.

E-commerce Rise

Convenience for elderly patients → rapid adoption.

Sub-subpoints:

➣Reminders for monthly refills.

➣Home delivery reduces caregiver stress.

➣Discounts attract fixed-income households.

Gender Influence

➣Women = 2/3 of U.S. Alzheimer’s cases.

➣Sub-subpoint: Longer life expectancy increases female patient pool.

Cost Implications

Drug R&D costs push prices up.

Sub-subpoints:

➣Adds pressure on healthcare systems.

➣Strengthens dominance of Big Pharma with deep pockets.

Aging Impact

➣By 2050, 12.7M Americans projected with Alzheimer’s.

➣Sub-subpoint: Chronic therapeutic demand ensures long-term revenue streams.

Market Trends

M&A Consolidation

AbbVie’s USD 1.4B acquisition of Aliada Therapeutics secures ALIA-1758, a novel antibody targeting amyloid beta. This reflects Big Pharma’s strategy of acquiring smaller biotech firms with innovative pipelines.

Biomarker Innovation

Plasma-based pTau217 assays simplify screening by replacing invasive spinal taps. This improves early diagnosis and speeds clinical trial recruitment.

Amyloid Oligomer Targeting

New drugs like sabirnetug target toxic soluble oligomers instead of plaques. This approach may improve cognitive outcomes more effectively than older therapies.

Neuroinflammation Therapies

Hoth Therapeutics’ HT-ALZ works on reducing brain inflammation, a pathway beyond amyloid and tau, opening new treatment options.

Tau-Focused Therapies

Biogen’s BIIB080 antisense therapy reduces abnormal tau protein production, preventing neurofibrillary tangle formation and slowing disease progression.

Nanomedicine Breakthroughs

Porosome Therapeutics is developing neuronal nanomachines to restore secretory pathways. This could potentially reverse early Alzheimer’s damage.

Cholinesterase Inhibitors’ Longevity

Older drugs like donepezil and galantamine remain widely used due to affordability, established safety, and effectiveness in symptom management.

Pipeline Acceleration

Alzheimer’s pipeline includes 127 active drugs in 164 trials, one of the largest in neurology. This reflects strong R&D focus on addressing unmet needs.

E-commerce Surge

Elderly-friendly online platforms with caregiver apps and delivery services are making drug access easier, ensuring better treatment adherence.

Asia-Pacific Expansion

Rapid growth of the elderly population in China, India, and Japan is driving demand. Japan also leads in dementia care innovation.

Collaborations for Innovation

GSK and Muna Therapeutics are working on MiND-MAP to focus on brain resilience, offering a new dimension to drug development.

Regulatory Flexibility

Agencies like the FDA are approving drugs faster (Aduhelm, Leqembi), showing a willingness to address the urgent unmet medical need despite debate over effectiveness.

Role of AI in Alzheimer’s Therapeutics

Early Brain Imaging

AI enhances MRI and PET scans to detect Alzheimer’s years before symptoms, enabling earlier and more effective treatment.

Biomarker Discovery

Machine learning identifies new biomarkers in blood and plasma data, potentially replacing invasive spinal taps for diagnosis.

Drug Repurposing

AI screens millions of existing drugs against Alzheimer’s targets, shortening the discovery timeline and lowering R&D costs.

Trial Recruitment Optimization

Algorithms match patients based on biomarkers and genetics, improving trial efficiency and reducing the risk of failed studies.

Personalized Care Pathways

AI tailors treatments according to individual profiles, disease severity, and lifestyle, making therapy more effective and patient-centered.

Remote Cognitive Monitoring

AI-powered apps track memory and speech changes during daily use, giving early warnings of decline and helping adjust therapy in real time.

Disease Simulation Models

Virtual simulations predict disease progression and test drug effects digitally, reducing reliance on costly, time-consuming trials.

Drug-Target Interaction Modeling

AI predicts how drugs will interact with amyloid, tau, and inflammatory proteins, prioritizing the most promising candidates.

Multimodal Data Integration

AI merges MRI scans, genetic data, and biomarkers into a comprehensive “digital twin” of the patient, enhancing diagnostic accuracy.

Caregiver Support Systems

AI chatbots and reminders assist caregivers with scheduling, adherence, and instant medical advice, reducing caregiver burden.

Market Dynamics

Drivers

Rising Prevalence of Alzheimer’s

➣Globally, 55 million people have dementia; ~10 million new cases yearly.

➣Alzheimer’s accounts for 60–70% of dementia cases.

➣Increasing prevalence drives demand for therapeutics across all stages of the disease.

Aging Population

➣In the U.S., 12.7M people projected with Alzheimer’s by 2050.

➣Asia-Pacific aging population is rapidly expanding, creating fastest-growing market segment.

➣Older age increases disease incidence, ensuring long-term market growth.

Strong Pipeline of Novel Drugs

➣127 drugs in 164 clinical trials (2024) targeting amyloid, tau, and inflammation.

➣Pipeline drugs offer potential disease-modifying effects, expanding the market beyond symptom management.

FDA and Regulatory Approvals

➣Approvals like Adlarity (2022), Aduhelm (2021), Leqembi (2023) increase market adoption.

➣Fast Track designations (BIIB080, 2025) accelerate commercialization and market entry.

Hospital and E-commerce Expansion

➣Hospital pharmacies integrate diagnosis, trials, and drug dispensing.

➣E-commerce supports convenience, adherence, and caregiver engagement, expanding treatment reach.

Increased R&D Funding

➣Both public and private sectors invest heavily in neuroscience research.

➣AI-driven drug discovery and biomarker identification attract investment, speeding innovation.

Gender Demographics

➣Women constitute ~2/3 of Alzheimer’s patients due to longevity.

➣Creates sustained demand for therapies tailored to older female populations.

Technological Innovations

➣AI and nanomedicine accelerate early diagnosis, treatment personalization, and pipeline drug optimization.

➣Digital twins and predictive modeling reduce clinical trial time and improve success rates.

Global Awareness Programs

➣Alzheimer’s associations and NGOs raise awareness of early detection and care.

➣Awareness drives earlier diagnosis and treatment adoption, increasing market penetration.

Collaborations and Partnerships

➣Pharma-biotech collaborations (GSK + Muna, AbbVie + Aliada) strengthen pipelines and innovation.

➣Partnerships help share R&D costs and accelerate novel therapeutic delivery.

Restraints

High Drug Development Cost

➣Developing a single Alzheimer’s drug may exceed USD 2B and 10–15 years.

➣Limits participation to large pharmaceutical companies, reducing competition.

Regulatory Hurdles

➣Strict FDA and EMA guidelines slow trial approvals.

➣Clinical endpoints are challenging due to variable cognitive decline among patients.

Clinical Trial Complexity

➣Heterogeneous patient populations complicate study design.

➣High dropout rates and comorbidities increase trial failure risk.

Limited Awareness in Low-Income Regions

➣Underdiagnosis reduces drug adoption in developing countries.

➣Education and infrastructure gaps hinder market expansion.

Safety and Side Effects

➣Some novel therapies (amyloid antibodies, antisense oligonucleotides) can cause adverse events.

➣Safety monitoring increases cost and may limit prescription uptake.

Opportunities

AI-Driven Drug Discovery

➣AI predicts drug-target interactions, repurposes existing drugs, and identifies biomarkers.

➣Reduces development timelines and costs, enhancing pipeline efficiency.

Telemedicine and E-commerce Integration

➣Elderly patients can access prescriptions, reminders, and consultations remotely.

➣Expands market reach, especially in semi-urban and rural areas.

Expansion in Asia-Pacific

➣Aging population and rising healthcare investments make it the fastest-growing market.

➣Local R&D and collaborations increase treatment adoption and pipeline trials.

Disease-Modifying Therapies

➣Pipeline drugs targeting tau, amyloid oligomers, and neuroinflammation offer potential to slow disease progression.

➣Early adoption could significantly transform patient outcomes and market size.

Collaborations Between Pharma and Biotech

➣Partnerships combine expertise and resources for faster innovation.

➣Examples: GSK + Muna (MiND-MAP), AbbVie + Aliada (ALIA-1758).

Challenges

Patient Adherence and Caregiver Burden

➣Alzheimer’s requires long-term treatment; compliance may drop without support.

➣AI-based reminders and caregiver apps are emerging solutions.

Reimbursement Issues

➣High-cost therapies face insurance limitations in many regions.

➣Reimbursement policies affect adoption of novel, expensive drugs.

Infrastructure Limitations

➣Low-resource regions lack access to diagnostics and hospital networks.

➣Limits market growth in emerging economies.

Trial Recruitment Difficulties

➣Strict inclusion/exclusion criteria reduce eligible patient numbers.

➣Early-stage detection is limited, slowing pipeline progress.

Market Competition

➣Despite pipeline growth, only a few drugs achieve FDA approval.

➣Competition among Big Pharma for limited blockbuster opportunities can be intense.

Regional Insights – Alzheimer’s Therapeutics Market (2025–2034)

North America – Dominant Market

Patient Pool:

6.7 million Americans aged 65+ affected in 2023.

High proportion of elderly population drives consistent demand for therapeutics.

Healthcare Infrastructure:

Advanced hospitals and diagnostic facilities (MRI, PET scans) support early detection.

Strong integration of hospital pharmacies and clinical trials.

Regulatory Strength:

FDA approvals (Adlarity, Aduhelm, Leqembi) accelerate access to novel drugs.

Fast Track designations support pipeline drugs and antisense oligonucleotides (BIIB080).

R&D Leadership:

Biogen, Eisai, AbbVie, and other pharma giants lead innovation in amyloid and tau therapies.

Drivers:

Government funding for Alzheimer’s research.

Advocacy and support groups increasing awareness and early diagnosis.

Breakthroughs in pipeline drugs and AI-assisted drug discovery.

Challenges:

High cost of therapies limits accessibility for uninsured or underinsured patients.

Regulatory bottlenecks in novel drug approvals can slow market expansion.

Opportunities:

AI integration for predictive diagnostics and personalized therapeutics.

Expansion of e-commerce pharmacies for home delivery of Alzheimer’s drugs.

Europe – Strong Presence

Healthcare Infrastructure:

Well-established hospitals and dementia centers across Germany, UK, France.

Cross-border collaboration in clinical trials due to EU research frameworks.

Regulatory Strength:

EMA provides structured regulatory pathways for novel therapies.

Pharma Presence:

Major players include Roche, Novartis, GSK, and Eli Lilly; strong focus on pipeline drugs.

Focus Areas:

Early-onset dementia management.

Adoption of combination therapies and biomarker-based diagnostics.

Drivers:

Government funding for Alzheimer’s research.

Incentives for R&D innovation in disease-modifying therapeutics.

Challenges:

Diverse healthcare reimbursement policies across countries.

Variability in adoption of high-cost novel therapies.

Opportunities:

Harmonized regulatory initiatives for faster approval.

Expansion of personalized care and AI-assisted patient monitoring.

Asia-Pacific – Fastest-Growing Market

Demographics:

Aging populations in China, India, Japan, and Australia.

Rapid urbanization and increase in life expectancy lead to higher Alzheimer’s prevalence.

Healthcare Infrastructure:

Growing hospitals, clinics, and diagnostic centers.

Expansion of digital health platforms and telemedicine for elderly care.

Drivers:

Rising healthcare expenditure in emerging economies.

Increasing awareness campaigns and caregiver education.

Local clinical trials and R&D collaborations accelerate market growth.

Challenges:

Regulatory fragmentation across countries complicates market entry.

Limited rural healthcare infrastructure restricts therapy access.

Opportunities:

Development of region-specific therapeutics and generics.

AI-assisted diagnostics and mobile health apps for remote monitoring.

Expansion of e-commerce pharmacy platforms for rural reach.

Middle East & Africa – Emerging Market

Market Base:

Smaller patient population compared to North America and Europe.

Increasing life expectancy contributes to a growing elderly population.

Healthcare Infrastructure:

Limited specialized dementia care centers.

Urban centers gradually adopting modern diagnostics and hospital pharmacies.

Drivers:

Public-private partnerships to enhance care and access.

International collaborations for clinical trials and knowledge transfer.

Challenges:

Limited awareness of Alzheimer’s among the general population.

Low availability of advanced therapeutics and diagnostic tools.

Opportunities:

Investment in training healthcare professionals in geriatrics and neurology.

Introduction of affordable generics and pipeline drugs via partnerships.

South America – Growing but Constrained

Healthcare Infrastructure:

Brazil leads in hospital-based Alzheimer’s treatment and clinical trials.

Access to generic Alzheimer’s drugs is improving, but advanced therapies are limited.

Drivers:

Expanding access to hospital pharmacies and increasing awareness campaigns.

Growing geriatric population demanding better care.

Challenges:

Economic constraints limit affordability of high-cost novel therapies.

Limited infrastructure in rural areas hinders treatment coverage.

Opportunities:

Expansion of insurance coverage and government-funded programs.

Development of region-specific affordable therapeutics and e-commerce platforms.

Top 10 Alzheimer’s Disease Therapeutics Companies (2025)

1. Biogen

Key Products: Aduhelm (aducanumab), Leqembi (lecanemab)

Focus: Pioneering amyloid-targeting therapies; ongoing research in tau-targeting treatments.

Strengths: Established leadership in Alzheimer’s therapeutics; strong pipeline with multiple Phase 3 trials.

Recent Developments: Continued expansion of clinical trials to assess long-term efficacy and safety of amyloid-targeting agents.

2. Eisai

Key Products: Leqembi (lecanemab), E2609 (in development)

Focus: Collaboration with Biogen on lecanemab; development of next-generation anti-amyloid therapies.

Strengths: Robust R&D infrastructure; strong partnership with Biogen enhancing clinical trial capabilities.

Recent Developments: Advancements in combination therapies targeting both amyloid and tau proteins.

3. Novo Nordisk

Key Products: Semaglutide (GLP-1 agonist)

Focus: Investigating the potential of semaglutide in slowing cognitive decline in Alzheimer’s patients.

Strengths: Expertise in metabolic disorders; leveraging GLP-1 receptor agonists for neurodegenerative diseases.

Recent Developments: Phase 3 trials underway; promising preclinical data suggesting neuroprotective effects.

4. Merck & Co.

Key Products: Verubecestat (BACE1 inhibitor), MK-8931

Focus: Developing disease-modifying therapies targeting amyloid precursor protein processing.

Strengths: Strong oncology background; expanding into neurodegenerative disease therapeutics.

Recent Developments: Ongoing trials assessing the safety and efficacy of BACE inhibitors in Alzheimer’s patients.

5. Johnson & Johnson

Key Products: JNJ-63733657 (anti-tau antibody)

Focus: Developing immunotherapies targeting tau protein aggregation.

Strengths: Diversified portfolio; expertise in immunology and neuroscience.

Recent Developments: Phase 2 trials evaluating the potential of anti-tau antibodies in slowing disease progression.

6. Bristol Myers Squibb

Key Products: ABBV-181 (anti-tau monoclonal antibody)

Focus: Targeting tau pathology in Alzheimer’s disease through monoclonal antibody therapies.

Strengths: Robust oncology pipeline; expanding into neurodegenerative diseases.

Recent Developments: Collaboration with AbbVie to advance anti-tau therapies into clinical trials.

7. Sanofi

Key Products: SAR-260301 (anti-tau monoclonal antibody)

Focus: Developing therapies targeting tau protein to mitigate neurodegeneration.

Strengths: Strong immuno-oncology expertise; leveraging monoclonal antibody platforms.

Recent Developments: Initiation of Phase 1 trials for SAR-260301 in Alzheimer’s patients.

8. Pfizer

Key Products: PF-06751979 (anti-tau antibody)

Focus: Investigating tau-targeted therapies to slow cognitive decline in Alzheimer’s.

Strengths: Extensive experience in immunotherapy; strong R&D capabilities.

Recent Developments: Advancements in biomarker development to monitor treatment efficacy.

9. Teva Pharmaceutical Industries

Key Products: Copaxone (glatiramer acetate), exploring Alzheimer’s indications

Focus: Repurposing existing therapies for Alzheimer’s disease.

Strengths: Established presence in neurology; cost-effective treatment options.

Recent Developments: Early-stage trials assessing the potential of glatiramer acetate in Alzheimer’s patients.

10. AbbVie

Key Products: ABBV-181 (anti-tau monoclonal antibody)

Focus: Collaboration with Bristol Myers Squibb to develop anti-tau therapies.

Strengths: Strong immuno-oncology pipeline; expanding into neurodegenerative diseases.

Recent Developments: Advancements in clinical trials evaluating the efficacy of anti-tau monoclonal antibodies.

Latest Announcements

1. Novo Nordisk’s Alzheimer’s Trial: A High-Risk, High-Reward Endeavor

Trial Focus: Investigating the potential of semaglutide, an obesity drug, to slow cognitive decline in early-stage Alzheimer’s patients.

Strategic Perspective: A senior executive referred to this trial as a “lottery ticket,” highlighting the high-risk but potentially significant reward of the endeavor.

Expected Results: The company anticipates results by the end of 2025, exploring Alzheimer’s as a possible new frontier for GLP-1 drugs.

2. Novartis Enters $5.7 Billion Licensing Deal with Monte Rosa Therapeutics

Deal Details: Novartis signed a licensing agreement valued at up to $5.7 billion with Monte Rosa Therapeutics, focusing on developing drugs for immune-mediated diseases.

Strategic Implications: This collaboration aims to discover small molecule degraders targeting disease-causing proteins, with Novartis handling clinical development and commercialization.

3. Retro Biosciences Launches Clinical Trial for Anti-Aging Pill Targeting Alzheimer’s

Trial Focus: RTR242, an experimental anti-aging pill, aims to revive autophagy to reverse cognitive decline associated with Alzheimer’s.

Innovative Approach: The trial, set in Australia, marks a significant step in exploring anti-aging therapies for neurodegenerative diseases.

Recent Developments in Alzheimer’s Therapeutics

1. Sanofi Acquires Vigil Neuroscience to Strengthen Neurology Division

Acquisition Details: In May 2025, Sanofi announced the acquisition of Vigil Neuroscience, Inc., a biotechnology company specializing in developing innovative treatments for neurodegenerative diseases.

Strategic Goal: This acquisition strengthens Sanofi’s neurology division and bolsters its early-stage pipeline in Alzheimer’s therapeutics.

2. INmune Bio’s Phase 2 Trial Results for XPro™ in Alzheimer’s Patients

Trial Focus: INmune Bio Inc. reported results from its Phase 2 MINDFuL trial assessing XPro™, a targeted soluble TNF inhibitor, in patients with early-stage Alzheimer’s disease showing signs of inflammation.

Implications: The trial’s outcomes could provide insights into the efficacy of targeting neuroinflammation in Alzheimer’s treatment.

Segments Covered

By Product Type

Cholinesterase Inhibitors

➣Dominant segment in 2024, widely prescribed due to affordability and well-established efficacy in memory and cognition management.

➣Key drugs: Donepezil, Galantamine, Rivastigmine.

➣Mechanism: Inhibit acetylcholinesterase, increasing acetylcholine levels in the brain, improving neural signaling.

➣Market relevance: Accounts for over 60–70% of symptomatic AD treatments.

➣Growth factors: Aging population, insurance coverage, and availability in hospital pharmacies ensure steady demand.

NMDA Receptor Antagonist

➣Used primarily for severe or moderate-to-severe Alzheimer’s.

➣Mechanism: Blocks excessive glutamate activity (excitotoxicity) which damages neurons.

➣Key drug example: Memantine.

➣Market relevance: Niche segment, but essential for advanced-stage patients.

➣Growth factors: Integration with combination therapy and hospital care ensures stable usage.

Combination Drugs

➣Target multiple pathways (cholinergic and glutamatergic) to enhance symptom control.

➣Examples: Donepezil + Memantine combination therapies.

➣Market relevance: Growing as clinicians adopt multi-targeted approaches to slow cognitive decline.

➣Advantages: Reduce pill burden, improve patient compliance, address multiple pathological mechanisms simultaneously.

Pipeline Drugs

➣Fastest-growing segment due to high unmet need for disease-modifying therapies.

➣Targets: Amyloid beta plaques, tau protein aggregation, neuroinflammation, secretory dysfunction.

➣Market relevance: 127 drugs under 164 clinical trials (2024), representing the future of Alzheimer’s care.

➣Key innovations: Antisense oligonucleotides (BIIB080), anti-pyroglutamate amyloid antibodies (ALIA-1758), nanomedicine (Porosome).

➣Growth factors: Strong R&D, regulatory incentives (Fast Track approvals), AI-assisted drug discovery.

By End User

Hospital Pharmacy

➣Largest segment in 2024; integrates diagnostics, treatment, and clinical trial access.

➣Advantages: Immediate availability of novel therapeutics, expert oversight, access to specialized neurologists, geriatricians, and psychiatrists.

➣Market impact: Hospitals drive high-volume prescriptions, early adoption of pipeline drugs, and support personalized care models.

➣Future trends: Growing role in early diagnosis using AI-assisted imaging and biomarker screening.

Retail Pharmacy

➣Accessible for daily dispensing; supports maintenance therapy in moderate-stage patients.

➣Limitations: Less integration with clinical trials and diagnostics.

➣Growth factors: Brand recognition, loyalty programs, and insurance coverage increase patient retention.

➣Relevance: Secondary channel but essential for long-term adherence outside hospital settings.

E-commerce / Online Pharmacy

➣Fastest-growing segment due to convenience, home delivery, refill reminders, and caregiver integration.

➣Advantages: Supports elderly patients and caregivers who may have mobility or transportation limitations.

➣Market relevance: Expands treatment access in urban and semi-urban regions.

➣Growth factors: Digital adoption, telemedicine integration, subscription-based delivery, and caregiver-focused apps.

By Geography

North America

➣Largest market share due to high prevalence (6.7M Americans 65+ in 2023) and strong healthcare infrastructure.

➣Drivers: FDA approvals (Adlarity, Aduhelm, Leqembi), research centers, and government/NGO support.

➣Trends: High adoption of AI diagnostics, integration of hospital and e-commerce pharmacies, robust pipeline investment.

Europe

➣Strong R&D presence (Roche, Novartis, GSK) drives pipeline innovation.

➣Drivers: EMA regulatory guidance, multi-country clinical trials, and government-funded dementia programs.

➣Growth trends: Focus on early diagnosis, biomarker use, and combination therapies for better patient outcomes.

Asia-Pacific

➣Fastest-growing market due to rapid aging population (China, India, Japan).

➣Drivers: Rising healthcare investments, expanding hospital and pharmacy infrastructure, increased awareness of Alzheimer’s.

➣Trends: Local R&D collaborations, telemedicine and AI-assisted diagnostics adoption, growing e-commerce platforms for elderly patients.

Middle East & Africa

➣Emerging market with limited awareness and access.

➣Drivers: Increasing geriatric population and urbanization.

➣Trends: Investment in neurology centers, telemedicine expansion, and awareness campaigns for early diagnosis.

South America

➣Brazil leads the region; overall limited advanced drug access due to cost and infrastructure.

➣Drivers: Government programs, insurance coverage, and increasing elderly population.

➣Trends: Gradual adoption of international therapeutics and clinical trial participation, focus on awareness and early-stage care.

Top 5 FAQs

-

What is the current size of the Alzheimer’s therapeutics market?

– USD 5.7B in 2025, projected to reach USD 12.07B by 2034 at a CAGR of 8.7%. -

Which region dominates the Alzheimer’s market?

– North America led in 2024 due to high prevalence, FDA approvals, and strong healthcare infrastructure. -

Which product type is leading the market?

– Cholinesterase inhibitors remain dominant, but pipeline drugs are growing fastest. -

What role does AI play in Alzheimer’s therapeutics?

– AI improves early diagnosis, biomarker discovery, trial recruitment, drug repurposing, and personalized treatment. -

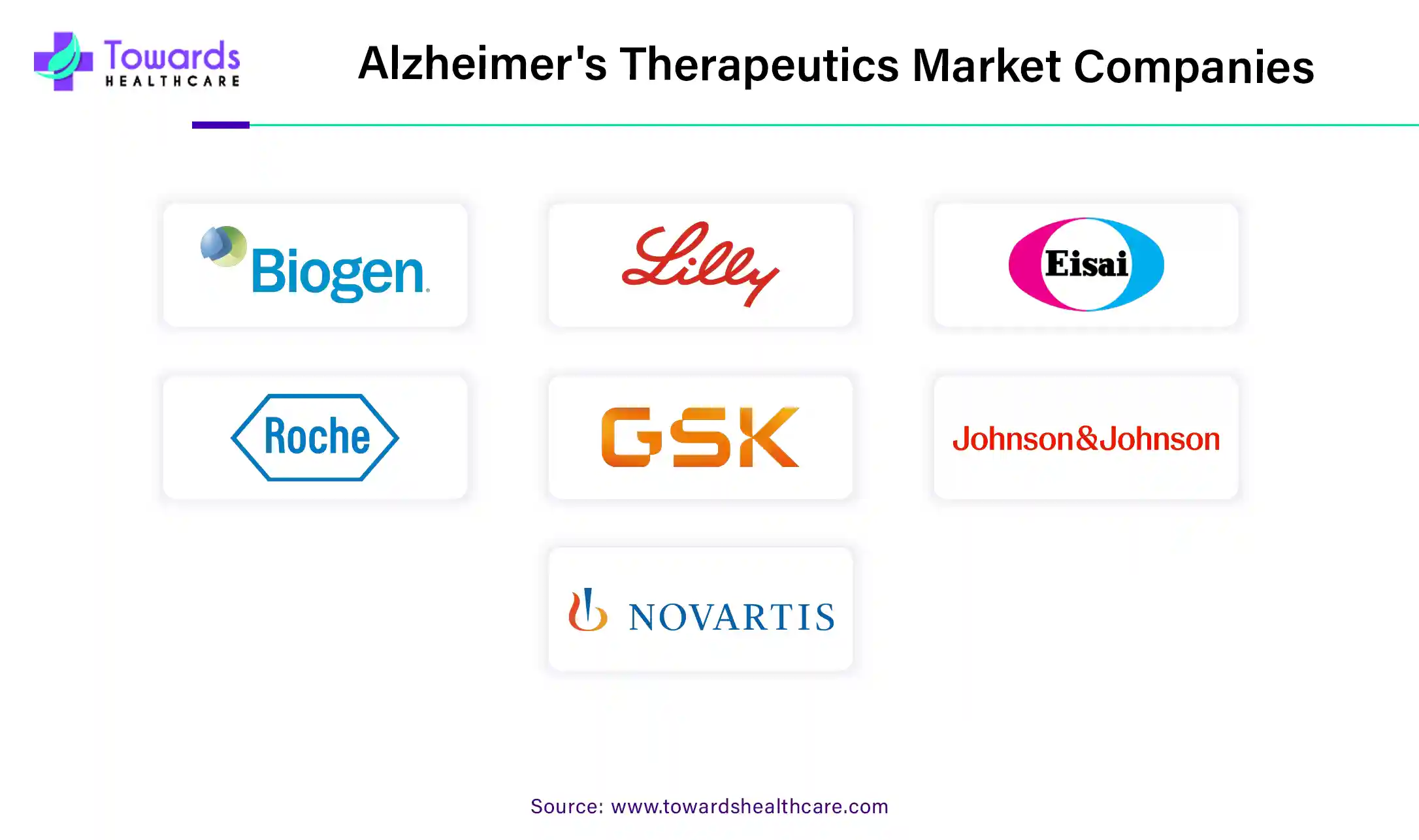

Who are the leading companies in this market?

– Biogen, Eli Lilly, Eisai, Roche, GSK, Johnson & Johnson, Merck, Novartis, Pfizer, and AbbVie.

Access our exclusive, data-rich dashboard dedicated to the healthcare market – built specifically for decision-makers, strategists, and industry leaders. The dashboard features comprehensive statistical data, segment-wise market breakdowns, regional performance shares, detailed company profiles, annual updates, and much more. From market sizing to competitive intelligence, this powerful tool is one-stop solution to your gateway.

Access the Dashboard: https://www.towardshealthcare.com/access-dashboard

Immediate Delivery Available | Buy This Premium Research @ https://www.towardshealthcare.com/price/5130

Become a valued research partner with us – https://www.towardshealthcare.com/schedule-meeting

You can place an order or ask any questions, please feel free to contact us at sales@towardshealthcare.com

Powering Healthcare Leaders with Real-Time Insights: https://www.towardshealthcare.com/healthcare-intelligence-platform

Europe Region – +44 778 256 0738

North America Region – +1 8044 4193 44

APAC Region: +91 9356 9282 04

Web: https://www.towardshealthcare.com

Find us on social platforms: LinkedIn | Twitter | Instagram | Medium | Pinterest