Ambulatory Surgical Center Market Shares, Growth a Report (2023–2034)

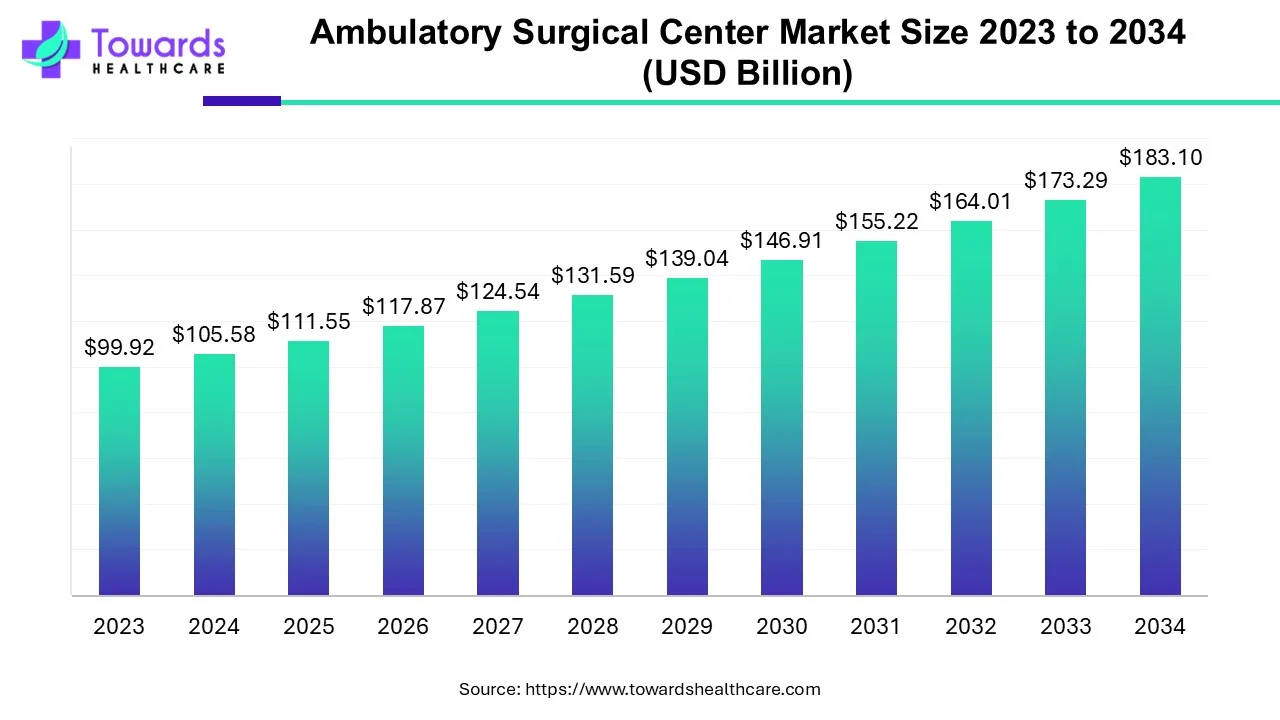

The global Ambulatory Surgical Center market was valued at USD 105.58 billion in 2024 and is projected to reach USD 183.1 billion by 2034, expanding at a CAGR of 5.66% (2025–2034)—driven by rising surgical volumes, growing outpatient preference, and rapid AI-powered technology integration.

Download the free sample and get the complete insights and forecasts report on this market @ https://www.towardshealthcare.com/download-sample/5021

Table of Contents

ToggleMarket Size

Market Value Growth (2024–2034):

●2024: USD 105.58 billion

●2034: USD 183.1 billion

●CAGR: 5.66% (2025–2034)

Historical Growth:

●From 2019–2023, ASC market expanded steadily due to the shift from inpatient to outpatient care, representing more than 60% of outpatient surgeries by 2019.

Procedure Volume Influence:

●Over 300 million surgeries performed annually worldwide.

●80% of all surgeries in the U.S. are now performed in outpatient settings, reflecting ASC dominance.

Cost Efficiency Impact:

●ASCs offer surgical procedures 35%–50% cheaper than hospitals, saving USD 40 billion annually for the U.S. healthcare system.

●Medicare savings: USD 4.2 billion annually via ASC utilization.

Revenue by Ownership:

●Physician-owned centers dominate with maximum revenue share, followed by hospital and corporate-owned facilities.

Patient Demographics Influence:

●Growing geriatric population (49 million aged 65+, projected to reach 24% by 2060) fuels ASC utilization.

Government Role:

●Expanding reimbursement coverage and ASC certification (over 6,223 Medicare-certified ASCs in the U.S.) boosts accessibility.

Technological Drivers:

●Integration of AI, ML, and robotics increases operational efficiency, lowers surgical errors, and reduces recovery time.

Market Trends

Shift to Outpatient Surgeries:

●Movement from hospital to ASC-driven surgical care due to reduced infection risks, quicker recovery, and patient convenience.

Cost Optimization:

●Significant decline in cost-per-procedure due to specialization, efficiency, and fewer hospital overheads.

AI and Robotics Adoption:

●Robotic-assisted surgeries, predictive analytics, and precision imaging enhance accuracy and recovery outcomes.

Government & Private Reimbursements:

●CMS and private payers expanding ASC-approved procedure lists, improving profitability.

Rise of Single-Specialty Centers:

●Dominant presence in ophthalmology and gastroenterology; single-specialty ASCs remain market leaders.

Surge in Multi-Specialty Facilities:

●Increasing patient demand for multi-procedure convenience, fueling multi-specialty ASC growth.

Healthcare Investments:

●Rising public and private capital flow into ASC infrastructure—boosted by digital health partnerships.

AI-driven Operational Optimization:

●Predictive modeling for scheduling, staffing, and post-op monitoring revolutionizes ASC workflows.

Telehealth & Remote Consultations:

●Integration of telemedicine platforms like Doctolib (France) enhances pre- and post-operative care.

Mergers & Acquisitions Surge:

●Consolidation trend, companies merging to form large ASC networks and increase operational scalability.

Role and Impact of AI in Ambulatory Surgical Center Market

AI in Diagnostic Imaging:

●AI algorithms detect anomalies in radiology and imaging, enhancing pre-surgery accuracy and minimizing false diagnoses.

Predictive Analytics in Scheduling:

●ML models predict optimal surgical schedules to reduce wait times and resource waste.

Personalized Patient Pathways:

●AI tailors care plans by analyzing historical patient data, optimizing recovery and satisfaction.

Automated Clinical Documentation:

●Natural Language Processing (NLP) automates charting, allowing surgeons to focus on patient outcomes.

AI in Robotic Surgery:

●Precision-guided robotic instruments powered by AI minimize incision size, blood loss, and complications.

Real-Time Monitoring and Alerts:

●AI-based wearable integration enables continuous post-surgery patient monitoring and early complication detection.

Predictive Maintenance of Equipment:

●Machine learning models predict device maintenance needs, minimizing downtime and increasing operational readiness.

AI-Based Patient Risk Assessment:

●Predictive algorithms evaluate risk scores, assisting clinicians in pre-operative screening and triage decisions.

Administrative Optimization:

●AI automates billing, claims, and insurance verification, streamlining reimbursement cycles.

Data-Driven Strategic Planning:

●Big data analytics help ASC management forecast case volumes, identify growth areas, and enhance financial decisions.

Regional Insights

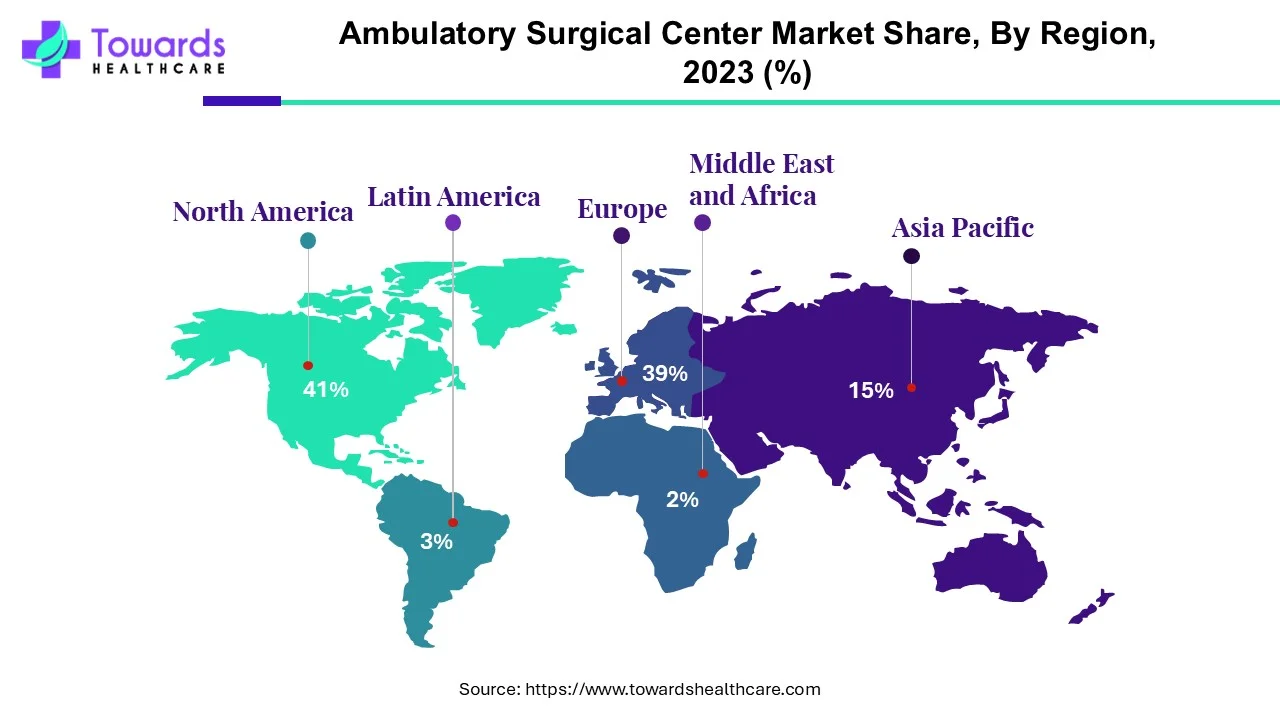

North America (Market Leader)

Market Share: Dominated the global ASC market in 2023.

Key Drivers:

●11,255 ASCs in the U.S. (6,223 Medicare-certified).

●Strong regulatory support and favorable reimbursement structure.

Economic Impact:

●Saves USD 42.2 billion in healthcare spending annually.

●Trend: Increasing geriatric population (15% → 24% by 2060) sustains long-term ASC demand.

Asia-Pacific (Fastest Growing Region)

Key Growth Rate: Fastest CAGR from 2025–2034.

Drivers:

●Rapid healthcare investment, rising chronic diseases, and growing medical tourism.

●Government incentives and infrastructure upgrades in China, Japan, and India.

●Example: China reports over 70% of elective eye surgeries conducted as day surgeries.

●India: Shift towards cost-effective outpatient solutions and minimally invasive surgeries.

Europe (Technological Expansion)

●Focus: AI-enabled surgery and robotic assistance.

Key Developments:

●Platforms like Doctolib (France) enable digital appointment scheduling and patient management.

●Trend: Government-driven healthcare modernization and outpatient procedure incentives.

Latin America (Emerging Market)

●Countries: Brazil, Mexico, Argentina lead ASC adoption.

●Drivers: Growth in urban private healthcare and foreign investment in surgical infrastructure.

Middle East & Africa (MEA)

●Focus: UAE and Saudi Arabia investing in high-end outpatient surgical facilities.

●Drivers: Expansion of private healthcare systems and medical tourism hubs.

Market Dynamics

Drivers

●Increasing number of surgeries worldwide (300+ million annually).

●Aging population driving demand for minimally invasive surgeries.

●Technological advancements (AI, robotics, imaging).

●Government funding and insurance reimbursement expansion.

●Cost-efficiency compared to hospitals (35–50% lower).

Restraints

●High cost of surgical equipment (X-ray units > USD 100,000).

●No overnight accommodation or emergency readiness.

●Complication rates (0.05–20%) limit patient confidence.

●Limited access in rural or low-income regions.

Opportunities

●Expansion of CMS-approved ASC procedures.

●AI and telehealth integration in outpatient care.

●Growth of multi-specialty centers.

●Cross-border medical tourism in APAC.

●Joint ventures between physicians and corporate partners.

Top 10 Companies

1. AmSurg

Overview: Leading U.S.-based ASC operator specializing in gastroenterology and ophthalmology.

Products/Services: Endoscopic and outpatient surgical services.

Strength: Large network of physician-owned ASCs and robust data integration.

2. American Vision Partners

Overview: Focused on ophthalmology surgical centers.

Products/Services: LASIK, cataract, and retina surgeries.

Strength: AI-based diagnostic tools for precision eye surgery.

3. Azura Vascular Care

Overview: Provides minimally invasive vascular and endovascular procedures.

Products/Services: Dialysis access management and peripheral vascular interventions.

Strength: Advanced imaging and outpatient vascular expertise.

4. Covenant Physician Partners

Overview: Joint-venture management company focusing on GI and ophthalmology.

Strength: Strategic partnerships with hospitals for integrated outpatient care.

5. HCA Healthcare

Overview: One of the largest U.S. healthcare systems, expanding into ASC operations.

Products: Multispecialty surgical solutions.

Strength: Strong financial base and technological infrastructure.

6. HST Pathways

Overview: Software solutions provider for ASC operations.

Products: Cloud-based ASC management, billing, and scheduling systems.

Strength: AI-driven workflow automation and analytics.

7. PE GI Solutions

Overview: Focused on gastroenterology center management.

Products: Endoscopy centers and GI practice management.

Strength: Data-driven clinical optimization and scalable partnerships.

8. Surgery Partners

Overview: Operates over 180 surgical facilities across the U.S.

Strength: Multispecialty expertise and strategic acquisitions.

9. SCA Health (Surgical Care Affiliates)

Overview: Manages surgical facilities in partnership with healthcare systems.

Strength: Large national footprint with cost-effective operations.

10. United Surgical Partners International (USPI)

Overview: Operates one of the largest ASC networks globally.

Strength: Backed by Tenet Healthcare; emphasizes multi-specialty expansion.

Latest Announcements

Kemal Erkan (American Surgery Center) emphasized cost reduction by 59% when shifting surgeries from hospitals to ASCs.

SurgNet Health Partners acquired Executive Ambulatory Surgery Center and Lippy Surgery Center within 45 days of funding, expanding its U.S. network.

Recent Developments

August 2024: ChristianaCare and Atlas Healthcare Partners formed a partnership to expand ASC networks across the Mid-Atlantic U.S. region.

April 2024: Commons Clinic invested USD 9.75 million to expand its ASC network and proprietary care platform “Theater.”

Segments Covered

1. By Type of Center

A. Single-Specialty Centers

Overview:

Single-specialty ambulatory surgical centers focus on one specific medical discipline — such as ophthalmology, gastroenterology, orthopedics, or pain management.

They accounted for the largest market share in 2023, maintaining dominance due to focused expertise, cost efficiency, and streamlined operations.

In-Depth Insights:

High Procedure Volume:

●Single-specialty ASCs conduct high volumes of routine, low-risk surgeries like cataract removal, endoscopy, or hernia repair, ensuring faster turnaround and higher profitability.

●These centers significantly reduce per-procedure cost while increasing throughput.

Operational Efficiency:

●Focused staffing, standardized protocols, and optimized equipment utilization minimize downtime and enhance surgical precision.

Market Drivers:

●Increasing prevalence of ophthalmic disorders (e.g., cataract and glaucoma) and gastroenterology procedures such as colonoscopy and endoscopy dominate this category.

●Demand for specialized outpatient centers offering faster recovery and lower costs compared to hospitals drives sustained growth.

Future Outlook:

●Expected to maintain a significant share through 2034 as minimally invasive and same-day surgeries become more common.

B. Multi-Specialty Centers

Overview:

Multi-specialty ASCs accommodate multiple surgical disciplines under one roof — combining orthopedics, ophthalmology, gastroenterology, urology, and pain management.

While smaller in number today, this segment is predicted to grow rapidly over the forecast period (2025–2034).

In-Depth Insights:

Integrated Service Model:

●Multi-specialty centers provide patients the advantage of accessing multiple specialties without the need for hospital-based care.

Rising Patient Preference:

●Patients increasingly prefer multi-specialty ASCs for convenience, continuity of care, and cost efficiency — particularly for those with multiple comorbidities.

Technological Adoption:

●These centers integrate AI-based scheduling, robotic surgery, and advanced imaging systems, making them capable of performing complex procedures with higher precision.

Revenue Growth Outlook:

●Expected to witness one of the highest CAGR rates during 2025–2034, fueled by cross-specialty collaboration and investment from large healthcare systems.

Example:

●Surgery Partners and United Surgical Partners International (USPI) are expanding multi-specialty models through mergers and acquisitions to serve wider patient bases.

2. By Ownership Type

A. Physician-Owned ASCs

Overview:

Physician-owned ASCs remain the largest ownership category, accounting for the majority of market share in 2023. These centers are operated by physicians who hold partial or full equity, ensuring clinical independence and operational flexibility.

In-Depth Insights:

Operational Control:

●Physicians maintain full authority over scheduling, patient flow, and clinical standards, resulting in higher efficiency and satisfaction.

Financial Incentives:

●Direct ownership ensures revenue retention and motivates surgeons to optimize outcomes and volume.

Quality of Care:

●Studies indicate higher patient satisfaction in physician-owned ASCs due to personalized care and shorter wait times.

Market Trend:

●This model is particularly prevalent in the U.S., where over 60% of ASCs are physician-owned.

●Supported by favorable reimbursement and joint ventures with hospital systems.

B. Hospital-Owned ASCs

Overview:

Hospital-owned ASCs are owned or co-managed by hospital systems aiming to diversify service delivery and extend surgical capacity into outpatient settings.

In-Depth Insights:

Strategic Integration:

●Hospitals use ASCs to offload non-critical procedures, reducing inpatient congestion while retaining patient referrals.

Market Drivers:

●Growth in this segment is driven by hospital acquisitions of physician practices and the integration of outpatient care models.

Financial Synergy:

●Hospitals leverage ASCs to optimize operational margins through shared infrastructure and integrated patient management systems.

Example:

ChristianaCare and Atlas Healthcare Partners’ collaboration (2024) exemplifies the hospital-ASC partnership trend, expanding regional access to outpatient surgical care.

Growth Outlook:

●Expected to record steady expansion due to the healthcare system’s push toward outpatient service optimization and cost control.

C. Corporate-Owned ASCs

Overview:

Corporate-owned ASCs are emerging rapidly as private equity firms, healthcare management companies, and large corporations invest heavily in ambulatory care networks.

In-Depth Insights:

Fastest-Growing Ownership Segment:

●Driven by joint ventures between management firms and physicians, offering operational scalability and financial backing.

Investment Momentum:

●Corporate entities like Commons Clinic and SurgNet Health Partners are acquiring and consolidating ASCs to build national networks.

Technological Sophistication:

●Focus on AI-powered management platforms, advanced billing systems, and patient experience solutions to streamline efficiency.

Scalability Advantage:

●Corporate ownership allows bulk purchasing, shared analytics, and centralized management, improving profit margins.

Market Outlook:

●Predicted to grow at the highest CAGR through 2034, supported by venture capital and healthcare IT innovation.

3. By Region

A. North America

Overview:

North America remains the dominant market, driven by mature infrastructure, government support, and high healthcare spending.

In-Depth Insights:

Market Size and Leadership:

●Over 11,255 ASCs in the U.S., including 6,223 Medicare-certified centers.

●Accounts for the largest global market share as of 2023.

Key Growth Factors:

●Aging population (15% → 24% of U.S. by 2060).

●Reimbursement reforms under Medicare and private payers.

●Advanced integration of AI, robotic surgeries, and predictive analytics.

Economic Impact:

●ASCs contribute USD 42.2 billion in annual healthcare savings, including USD 4.2 billion in Medicare savings.

Future Outlook:

●Continued dominance due to value-based care initiatives and outpatient expansion strategies.

B. Asia-Pacific (APAC)

Overview:

Asia-Pacific is the fastest-growing regional market, fueled by healthcare modernization, public-private investments, and rapid urbanization.

In-Depth Insights:

Healthcare Demand Surge:

●High prevalence of chronic diseases and rising middle-class population create demand for affordable outpatient surgeries.

Government Incentives:

●China, Japan, and India are expanding ASC infrastructure through public-private partnerships.

Medical Tourism:

●Countries like India and Thailand attract international patients seeking cost-effective surgeries.

Technological Growth:

●Surge in robotic and minimally invasive surgeries; China reports 70% of elective eye surgeries as day procedures.

Future Outlook:

●Projected to achieve the highest CAGR (2025–2034), driven by healthcare digitalization and investment inflows.

C. Europe

Overview:

Europe represents a technology-driven ASC market, emphasizing digital healthcare platforms, robotic surgery, and quality care reforms.

In-Depth Insights:

Healthcare Digitalization:

●Widespread adoption of telehealth and patient engagement tools like Doctolib (France) streamline care delivery.

Focus on Minimally Invasive Surgery:

●Growth of robotic-assisted surgery for orthopedics and ophthalmology procedures.

Regulatory Support:

●European governments pushing outpatient care for cost reduction and hospital capacity optimization.

Future Outlook:

●Strong potential for cross-border ASC expansion, supported by technology and government-led outpatient policy reforms.

D. Latin America & Middle East & Africa (MEA)

Overview:

These regions are emerging ASC markets, characterized by increasing private investments, healthcare reforms, and expanding insurance penetration.

In-Depth Insights:

Latin America:

Brazil, Mexico, and Argentina are leading in ASC adoption, driven by urbanization and private sector participation.

●Focus on affordable outpatient surgeries amid constrained hospital infrastructure.

Middle East & Africa:

UAE, Saudi Arabia, and South Africa are key hubs investing in high-end ASC facilities.

●Growth supported by national health programs and medical tourism initiatives.

Challenges and Opportunities:

●Limited awareness and lack of trained specialists remain barriers.

●Growing partnerships with global healthcare companies are bridging these gaps.

Future Outlook:

●Expected steady growth as regional governments invest in healthcare infrastructure and training

11. Top 5 FAQs

Q1. What is the projected size of the ASC market by 2034?

→ USD 183.1 billion, growing at a 5.66% CAGR from 2025–2034.

Q2. Which region dominates the ASC market?

→ North America, driven by government support and 11,000+ ASC facilities.

Q3. What factors drive ASC market growth?

→ Increasing surgical volumes, cost-effectiveness (35–50% cheaper), and AI-driven efficiency.

Q4. What role does AI play in the ASC industry?

→ Enhances diagnostics, scheduling, personalized care, and robotic surgeries, improving accuracy and recovery.

Q5. Which company leads in ASC operations?

→ United Surgical Partners International (USPI) and SCA Health are market leaders with vast multi-specialty networks.

Access our exclusive, data-rich dashboard dedicated to the healthcare market – built specifically for decision-makers, strategists, and industry leaders. The dashboard features comprehensive statistical data, segment-wise market breakdowns, regional performance shares, detailed company profiles, annual updates, and much more. From market sizing to competitive intelligence, this powerful tool is one-stop solution to your gateway.

Access the Dashboard: https://www.towardshealthcare.com/access-dashboard

Order your Ambulatory Surgical Center Market report now at: https://www.towardshealthcare.com/checkout/5021

Become a valued research partner with us – https://www.towardshealthcare.com/schedule-meeting

You can place an order or ask any questions, please feel free to contact us at sales@towardshealthcare.com

Powering Healthcare Leaders with Real-Time Insights: https://www.towardshealthcare.com/healthcare-intelligence-platform

Europe Region – +44 778 256 0738

North America Region – +1 8044 4193 44

APAC Region: +91 9356 9282 04

Visit Our Website:https://www.towardshealthcare.com

Find us on social platforms: LinkedIn | Twitter | Instagram | Medium | Pinterest