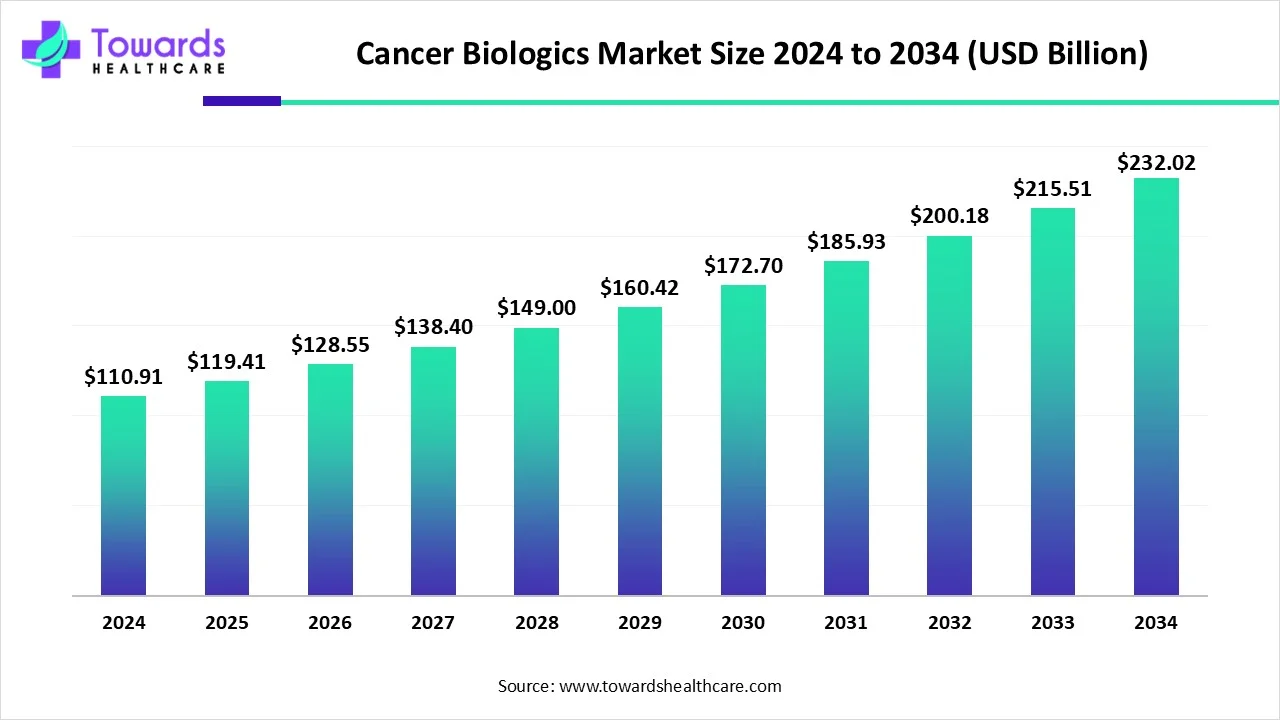

The global cancer biologics market is forecast to grow from USD 119.41 billion in 2025 to USD 232.02 billion by 2034 (an absolute increase of USD 112.61 billion) at a CAGR of 7.66%, driven by advances in monoclonal antibodies, targeted growth-inhibitor therapies, rising cancer incidence, and expanding biotech R&D and manufacturing capacity.

Download the free sample and get the complete insights and forecasts report on this market @ https://www.towardshealthcare.com/download-sample/5183

Market size

Headline numbers & math

➤2025 market value: USD 119.41B.

➤2034 market value (forecast): USD 232.02B.

➤Absolute growth (2025→2034): USD 232.02B − 119.41B = 112.61B.

➤CAGR (2025–2034): 7.66% (the forecasted growth rate that produces the above end value).

What this growth represents (revenue pools)

➤Sales growth will come from: (a) incremental uptake of next-generation biologics (ADCs, bispecifics, engineered mAbs), (b) expansion of biologics into indications previously dominated by small molecules, (c) geographic market expansion (emerging market adoption), and (d) biosimilar adoption that expands patient access while shifting revenue to new manufacturers.

Magnitude vs. time

➤The market nearly doubles in the 9-year forecast window, implying sustained mid-single digit to high-single digit growth across product classes and geographies rather than a single short boom.

Revenue composition drivers (high level)

➤Platform winners (monoclonal antibodies and engineered derivatives) take the largest share due to clinical breadth and durability of revenue streams.

➤Fastest incremental growth comes from cancer growth inhibitors (next-gen targeted small/biologic inhibitors) and novel modalities (cell therapies, CAR-T, therapeutic vaccines).

Investment multiplier

➤Growth is not only commercial — a large portion of the market size increase reflects heavy R&D, licensing, and M&A investments that monetize pipeline assets or expand manufacturing/clinical capacity.

Access & price effect

➤High prices for many biologics mean even relatively small patient volume increases can produce large revenue gains; conversely, price pressure or payer restrictions can blunt realized revenue growth.

Capacity & manufacturing economics

➤Biologic manufacturing scale (mAbs, ADCs, cell therapies) is capital-intensive—investment in GMP facilities and contractor capacity is baked into future supply and thus into the market size.

Biosimilar & generic influence

➤Biosimilars shift established biologic revenues but simultaneously increase treatment penetration, changing the net value dynamics of the market.

Clinical access effects

➤Some biologics remain available mainly via clinical trials—converting trial access to commercial approvals shifts revenue recognition dramatically.

Risk-weighted nature

➤The headline market size aggregates approved product sales and the expected commercialized share of pipeline assets — the forecast implicitly assumes a steady success rate for late-stage biologics.

Market trends

Monoclonal antibodies (mAbs) remain the dominant platform

➤The report notes mAbs dominated in 2023: their modularity (naked, conjugated, bispecific) and proven clinical efficacy keep them as the primary revenue engine.

Cancer growth inhibitors are the fastest-growing drug class

➤Targeted inhibitors (e.g., PARP inhibitors, kinase inhibitors) are expanding into more tumor types and earlier lines of therapy — this is the fastest growth segment per the report.

Therapeutic combinations increase clinical value

➤Combination regimens (immunotherapy + targeted agents or oncolytic viruses + vaccines) are growing, increasing per-patient lifetime value and expanding addressable populations.

Precision medicine and theranostics gaining real commercial weight

➤Companion diagnostics, biomarker stratification and precision drug delivery systems increase response rates and justify premium pricing for targeted biologics.

Hospitals dominate current end-use; specialized cancer centers growing fastest

➤Hospitals are today the primary delivery channel (2023), but cancer centers and integrated oncology clinics are expanding faster thanks to multidisciplinary care models and clinical trial activity.

Regional shift: North America leads today; Asia-Pacific grows fastest

➤North America domination reflects infrastructure and reimbursement; Asia-Pacific’s rapid expansion is driven by rising cancer incidence, healthcare build-out, and domestic biopharma investment (India/China examples).

Rising clinical trial activity and late-stage launches

➤Late-stage trials and launches (e.g., joint BioNTech–Duality Phase III mentioned) are expanding the near-term launch calendar, keeping the innovation pipeline robust.

Biosimilars & cost dynamics changing access

➤Biosimilar approvals/manufacturing (e.g., Biocon’s manufacturing permission for bevacizumab) increase supply and price competition in mature biologic classes.

Manufacturing and quality complexity remains a limitation

➤High capital and quality demands for biologics production are a structural restraint on how quickly supply can scale.

High cost of therapies limits access and payer acceptance

➤The high cost of biologics is explicitly cited as a growth restraint—payers and health systems create hurdles that can slow real-world uptake despite clinical value.

M&A, partnerships, and venture funding are active

➤Significant deals, Series B/seed rounds, and collaborative trials (TORL Series B; Commit Biologics seed funding) show active capital deployment to commercialize new modalities.

Therapies transitioning from niche to mainstream

➤CAR-T, ADCs, and therapeutic vaccines are moving from late-stage research to more standard-of-care roles in certain tumor types, broadening the market.

Roles / impacts of AI in the cancer biologics market

Target discovery & validation at scale

➤What AI does: mine multi-omics datasets, literature, and clinical records to rank/validate novel targets (tumor-specific antigens, synthetic lethal partners).

➤Impact: reduces bench time for identifying biologically relevant targets, increases hit rate entering preclinical development, shortens time-to-first-in-vivo proof-of-concept.

➤Commercial effect: accelerates pipeline throughput and reduces cost per validated program, improving the economics behind the market’s expansion.

In-silico antibody and binder design (generative models)

➤What AI does: uses sequence-to-structure and generative models to propose antibody/hit sequences optimized for affinity, specificity, developability (e.g., solubility, immunogenicity).

➤Impact: cuts cycles in lead optimization, reduces attrition from biophysical liabilities, increases success probability of mAbs and bispecifics.

➤Commercial effect: raises effective R&D productivity and shortens preclinical timelines; more biologics reach clinical stages, expanding future market size.

Antibody-drug conjugate (ADC) payload/linker optimization

➤What AI does: model ADC pharmacokinetics, linker cleavage, and payload cell permeability to optimize therapeutic index.

➤Impact: better balancing potency and toxicity, enabling ADCs in indications previously too narrow.

➤Commercial effect: unlocks new ADC launches and broadens indications, boosting revenue potential in the ADC subsegment.

Cell therapy (CAR-T / engineered cell) design and manufacturing control

➤What AI does: optimize CAR constructs, predict off-target activity, and implement process control models for autologous/allogeneic manufacturing.

➤Impact: increases safety, scalability, and batch consistency; lowers manufacturing failure rates for CAR-T.

➤Commercial effect: reduces per-patient manufacturing costs and increases commercial scalability of cell therapies.

Preclinical to clinical translation modelling

➤What AI does: integrate animal and in-vitro data with human datasets to predict human efficacy/safety and to select better first-in-human doses.

➤Impact: enhances dose selection and endpoint choice, reduces Phase II/III failure risk.

➤Commercial effect: better R&D ROI; higher fraction of programs reach commercialization.

Patient stratification & companion diagnostics

➤What AI does: from imaging, genomics, and EHRs, identify biomarker signatures predicting responders vs non-responders.

➤Impact: improves trial design, reduces sample sizes, and increases likelihood of positive pivotal trials via enriched cohorts.

➤Commercial effect: faster approvals and premium pricing for precision biologics; improved payer acceptance due to demonstrable value.

Clinical trial optimization & synthetic control arms

➤What AI does: use real-world data (RWD) and predictive models to design trials, identify sites/patients, and create synthetic control arms where ethical/operationally feasible.

➤Impact: shortens recruitment timelines, cuts trial costs, and can speed regulatory review.

➤Commercial effect: quicker market entry and lower development costs raise net present value of new biologic assets.

Manufacturing yield & supply chain predictive analytics

➤What AI does: monitor process parameters in real time (PAT), predict yield deviations, and optimize upstream/downstream bioprocess conditions.

➤Impact: raises batch yields, reduces lot failures, and shortens cycle times.

➤Commercial effect: lowers unit production cost of biologics and reduces supply constraints, enabling wider adoption.

Market access, pricing & value modelling

➤What AI does: simulate payer responses, cost-effectiveness models, and coverage scenarios using local epidemiology and cost inputs.

➤Impact: helps companies craft evidence and pricing strategies tailored to national health systems.

➤Commercial effect: improves reimbursement success, accelerating commercial uptake and realized market size.

Post-market safety surveillance & pharmacovigilance

➤What AI does: mine claims, EHRs, and social data for early detection of adverse events and signal management.

➤Impact: faster risk mitigation, improved product labels, and better long-term safety profiles.

➤Commercial effect: preserves product lifecycle value and reduces costly safety-driven withdrawals or label restrictions.

Regional insights

North America (dominant, mature)

Why dominant

➤Advanced biotech ecosystem, large venture and pharma R&D budgets, dense clinical trial networks, favorable reimbursement frameworks.

Commercial advantages

➤Regulatory predictability, established specialty care infrastructure (cancer centers & hospitals), historically faster uptake for new biologics.

Constraints

➤Increasing payer scrutiny and pricing debates may slow uptake unless clear value is demonstrated.

Europe

Strengths

➤Strong regulatory science (EMA), high clinical trial activity, high biosimilar adoption in some countries creating cost pressure.

Dynamics

➤Pricing negotiations and HTA (health technology assessment) shape launch sequencing and pricing strategy.

Opportunities

➤Cross-border procurement and centralized approval can accelerate multi-country launches if HTA evidence aligns.

Asia-Pacific (fastest growing)

Drivers

➤Aging populations, rising incidence, expanding healthcare infrastructure, government bio-investment, growing domestic manufacturing (India, China).

Country subpoints

China: large patient base and increasing local R&D; early stage trials and local partnership strategies are common.

India: domestic demand and rising bio-investment; Biocon example (EMA permission for biosimilar bevacizumab) signals capacity expansion aimed at exports and domestic access.

Challenges

Price sensitivity, heterogeneous regulatory systems, variable payer coverage.

Latin America

Characteristics

Growing private healthcare and selective public reimbursement; rollout of high-cost biologics lags relative to NA/EU.

Commercial approach

Partnerships, tiered pricing, and local manufacturing/biosimilars may be key access strategies.

Middle East & Africa (MEA)

Current state

Lower per-capita access, high out-of-pocket costs in many regions.

Trends

Investment in specialized cancer centers and regional hubs could create pockets of demand.

Market dynamics

Primary driver — growing cancer prevalence

Higher incidence → larger patient pools → expanded demand for biologics, particularly targeted and immune modulatory agents.

R&D innovation as a growth engine

Novel modalities (ADCs, bispecifics, CAR-T, vaccines) and combination regimens prolong therapeutic lifecycles and create new indications.

Restraint — high cost of biologics

Complex manufacture and premium pricing limit access and invite payer pushback; cost is explicitly listed as a primary restraint.

Opportunity — precision medicine & drug delivery

Personalized dosing, companion diagnostics, and targeted delivery systems (theranostics) can improve efficacy and justify premium reimbursement.

Threat — manufacturing scale & quality bottlenecks

Capacity constraints and GMP complexity can cause supply shortages and delay launches.

Opportunity — biosimilars & endogenous competition

Biosimilars lower treatment costs and broaden access, but also shift revenue away from originators — net market expands but unit prices may compress.

Driver — regulatory and reimbursement evolution

Adaptive approvals, breakthrough designations, and real-world evidence acceptance accelerate commercialization for high-value biologics.

Threat — clinical failure risk

Late-stage trial failures can wipe projected revenue for specific programs; diversified pipelines and partnerships are risk mitigation.

Driver — capital availability

Venture funding, large pharma investment and strategic partnerships (Series B, seed rounds, licensing) sustain pipeline progression.

Opportunity — regional manufacturing & exports

Investments in regional manufacturing (e.g., Biocon’s mAbs facility) enable cost arbitrage and export potential to developed markets.

Top 10 companies

Roche (Hoffmann-La Roche Ltd.)

Product focus: Oncology biologics and diagnostics (major mAb platforms and companion diagnostics historically).

Overview: Legacy leader in antibody therapeutics with integrated diagnostics strengths.

Strengths: Deep oncology pipeline, vertical integration (drug + diagnostic), strong commercial footprint in oncology centers.

Pfizer Inc.

Product focus: Biologics and immuno-oncology partnerships; large commercial reach.

Overview: Global pharma with capacity for rapid commercialization and distribution.

Strengths: Scale, global sales force, capability to partner and co-develop oncology biologics.

Amgen, Inc.

Product focus: Protein therapeutics and antibody engineering.

Overview: Biotech pioneer transitioning biologic R&D into oncology indications.

Strengths: Biologic R&D heritage, manufacturing expertise, strong biologics commercial experience.

BioNTech

Product focus: mRNA, personalized cancer vaccines, ADC partnerships (content cites BioNTech–Duality trial).

Overview: Fast-growing oncology biotech with platformed approaches (mRNA & conjugates).

Strengths: Platform technology, partnerships for regional trials (e.g., Duality in China), agility to run late-stage oncology programs.

Biocon Biologics

Product focus: Biosimilars and mAb manufacturing (content notes EMA permission for bevacizumab manufacture).

Overview: India-based biologics manufacturer scaling into global biosimilar markets.

Strengths: Cost-competitive manufacturing, regulatory milestones (EMA manufacturing permission), and export focus.

AstraZeneca PLC

Product focus: Oncology biologics and targeted therapies.

Overview: Strong oncology franchise with global commercial capability.

Strengths: Late-stage clinical assets, commercial collaborations, and hospital/cancer center relationships.

Bristol Myers Squibb (BMS)

Product focus: Immuno-oncology biologics (checkpoint inhibitors and combination regimens).

Overview: Major oncology player with emphasis on durable immunotherapies.

Strengths: Large oncology portfolio and experience in combination regimens and line extensions.

Merck & Co., Inc.

Product focus: Immune checkpoint biology and precision oncology approaches.

Overview: Global leader in immuno-oncology with high impact therapies.

Strengths: Strong clinical evidence base, broad global uptake, payer recognition.

Novartis

Product focus: Cell therapies & biologics (including CAR-T), and antibody therapeutics.

Overview: Integrated pharma with major investments in cell therapy manufacturing and commercialization.

Strengths: Manufacturing scale for advanced therapies and global commercialization infrastructure.

Takeda Pharmaceutical Company Limited

Product focus: Biologics across specialty areas including oncology.

Overview: Japan-based global pharma with selective oncology biologic programs and global reach.

Strengths: Global distribution, regional market knowledge in APAC, capability for strategic alliances.

Latest announcements

BioNTech & Duality Biologics — January 2024

Announcement: Partnership to launch a late-stage (Phase III) trial in China for an antibody-drug conjugate (ADC) targeting low-HER2 advanced breast cancer.

Significance: Late-stage trial in a large patient population (China) expands global development footprint and could unlock a major commercial opportunity in a region with growing oncology demand.

Biocon Biologics — June 2024

Announcement: EMA granted permission for Biocon’s Bengaluru facility to manufacture biosimilar Bevacizumab (mAb).

Significance: Regulatory clearance for mAb manufacturing at an EU standard facility positions Biocon to supply biosimilar bevacizumab to regulated markets, improving access and export potential.

Commit Biologics — May 2024

Announcement: Emerged from stealth with €16M seed funding to pursue BiCE (bispecific complement engaging) antibody therapeutics.

Significance: New modality companies raise capital to enter the oncology biologics space, reflecting investor appetite for bispecific platforms.

Dr. Reddy’s Laboratories — March 2024

Announcement: Launched Versavo, a biosimilar for multiple cancers (regulatory filing noted).

Significance: Additional biosimilar market entries expand affordable options for multiple tumor types and strengthen competition.

Biocon Biologics — July 2023

Announcement: U.S. launch of HULIO® (adalimumab biosimilar) after earlier approvals in Europe/Canada.

Significance: Although adalimumab is not a cancer drug, the commercial launch demonstrates Biocon’s ability to bring large-volume biologics to major markets — an operational template transferable to oncology biosimilars.

TORL BioTherapeutics — April 2023

Announcement: $158M Series B and launch, with an ADC & mAb pipeline discovered from established oncology research lab.

Significance: Big venture rounds for ADC/mAb developers indicate high investor confidence in antibody platforms.

Recent developments

Late-stage oncology ADC trial activity is expanding

Example: BioNTech + Duality Phase III in China for low-HER2 breast cancer shows ADCs moving into later-line/registrational studies — a pipeline maturation signal.

Biosimilar manufacturing capacity and regulatory acceptance increasing

Biocon’s EMA permission for mAb manufacturing shows emerging market manufacturers meeting strict EU GMP standards — this will increase global supply and may compress originator prices.

New modality start-ups receiving meaningful capital

Commit Biologics’ seed round and TORL’s Series B reflect investor support for innovative platforms (bispecifics/ADCs) that could produce next-generation biologics.

Commercial biosimilar launches continue to broaden access

Dr. Reddy’s Versavo and Biocon’s HULIO U.S. entry exemplify how biosimilars are being commercialized across multiple markets, enlarging the addressable patient pool.

Hospital and cancer center infrastructure upgrades

Launch of AI-Precision Oncology Centers (example in content: Apollo Cancer Centre, Bengaluru, Jan 2024) shows health systems adopting tech to enable precision biologic deployment.

Segments covered

Monoclonal Antibodies (mAbs)

Naked mAbs: Unconjugated antibodies that bind tumor antigen and mediate immune/effector functions.

Development notes: Well-established R&D track; manufacturing scale is known; patent cliffs enable biosimilars.

Conjugated mAbs (ADCs): mAb linked to cytotoxic payloads to deliver potent drugs selectively.

Development notes: Complex linking chemistry, required payload selection and linker stability; high therapeutic index if optimized.

Bispecific mAbs: Single molecules binding two targets (e.g., tumor antigen + T-cell engager).

Development notes: Design complexity higher; promising for redirecting immunity and dual pathway blockade.

Cancer Growth Inhibitors

Tyrosine Kinase Inhibitors (TKIs): Block oncogenic kinase signaling (when biologic/large molecule analogs exist they target growth receptor biology).

mTOR inhibitors / Proteasome inhibitors / Others: Inhibit intracellular growth/survival pathways.

Commercial note: While many are small molecules, biologic approaches to inhibit growth (antibodies against growth factor receptors) fall in this segment.

Vaccines

Preventive vaccines: Aim to prevent cancer (e.g., HPV vaccines are classical examples; relevance in oncology biologics is prevention of virus-related cancers).

Therapeutic vaccines: Stimulate anti-tumor immunity in existing cancer.

Development notes: Immune response variability and need for robust adjuvant/antigen selection; companion diagnostics often required.

Recombinant Proteins

Cytokines, growth factors, supportive biologics

Use: Modulate immune response, support recovery, or target tumor microenvironment.

CAR-T Cells

Autologous & allogeneic engineered T cells

Development notes: Very high complexity manufacturing (patient cell collection, engineering, expansion), high per-patient cost, intense safety monitoring.

Angiogenesis Inhibitors

Anti-VEGF mAbs and related molecules

Mechanism: Cut off tumor blood supply; useful in multiple solid tumors.

Interleukins (IL) & Interferons (IFN)

Cytokine therapies to boost immune responses.

Challenges: Systemic toxicity; engineered cytokines or targeted delivery increases therapeutic index.

Gene Therapy

Gene-modulating strategies to correct or reprogram tumor/immune cells.

Status: High innovation with high regulatory complexity.

Other Modalities

Theranostics, radiolabeled biologics, peptide vaccines, etc.

Commercial note: Often niche but high-value when matched with precise diagnostics.

Top 5 FAQs

-

Q: What is the projected size and growth rate of the cancer biologics market?

A: The market is forecast to grow from USD 119.41 billion in 2025 to USD 232.02 billion by 2034, representing an absolute increase of USD 112.61B and a CAGR of 7.66% over the period. -

Q: Which drug class currently dominates the market and which is growing fastest?

A: Monoclonal antibodies dominated the market in 2023; cancer growth inhibitors are estimated to grow the fastest during the forecast period (per the provided report). -

Q: Which regions lead and which are growing most quickly?

A: North America dominated the market in 2023 due to infrastructure and reimbursement frameworks. Asia-Pacific is expected to grow at the fastest rate over the forecast period, driven by rising incidence and expanding healthcare capacity. -

Q: What major restraints could limit market growth?

A: The high cost of biologics (development, manufacturing, and treatment) is a primary restraint that can limit access, payer acceptance, and thus market growth. -

Q: What recent industry developments signal future growth?

A: Recent items from the report include: (a) BioNTech + Duality launching a Phase III ADC trial in China (Jan 2024), (b) Biocon receiving EMA manufacturing permission for biosimilar bevacizumab (June 2024), and (c) multiple new company financings and biosimilar launches (Commit Biologics seed funding; Dr. Reddy’s Versavo launch) — collectively indicating active pipeline maturation, biosimilar scale-up, and investment flow.

Access our exclusive, data-rich dashboard dedicated to the healthcare market – built specifically for decision-makers, strategists, and industry leaders. The dashboard features comprehensive statistical data, segment-wise market breakdowns, regional performance shares, detailed company profiles, annual updates, and much more. From market sizing to competitive intelligence, this powerful tool is one-stop solution to your gateway.

Access the Dashboard: https://www.towardshealthcare.com/access-dashboard

Immediate Delivery Available | Buy This Premium Research @ https://www.towardshealthcare.com/price/5183

Become a valued research partner with us – https://www.towardshealthcare.com/schedule-meeting

You can place an order or ask any questions, please feel free to contact us at sales@towardshealthcare.com

Powering Healthcare Leaders with Real-Time Insights: https://www.towardshealthcare.com/healthcare-intelligence-platform

Europe Region – +44 778 256 0738

North America Region – +1 8044 4193 44

APAC Region: +91 9356 9282 04

Web: https://www.towardshealthcare.com

Find us on social platforms: LinkedIn | Twitter | Instagram | Medium | Pinterest