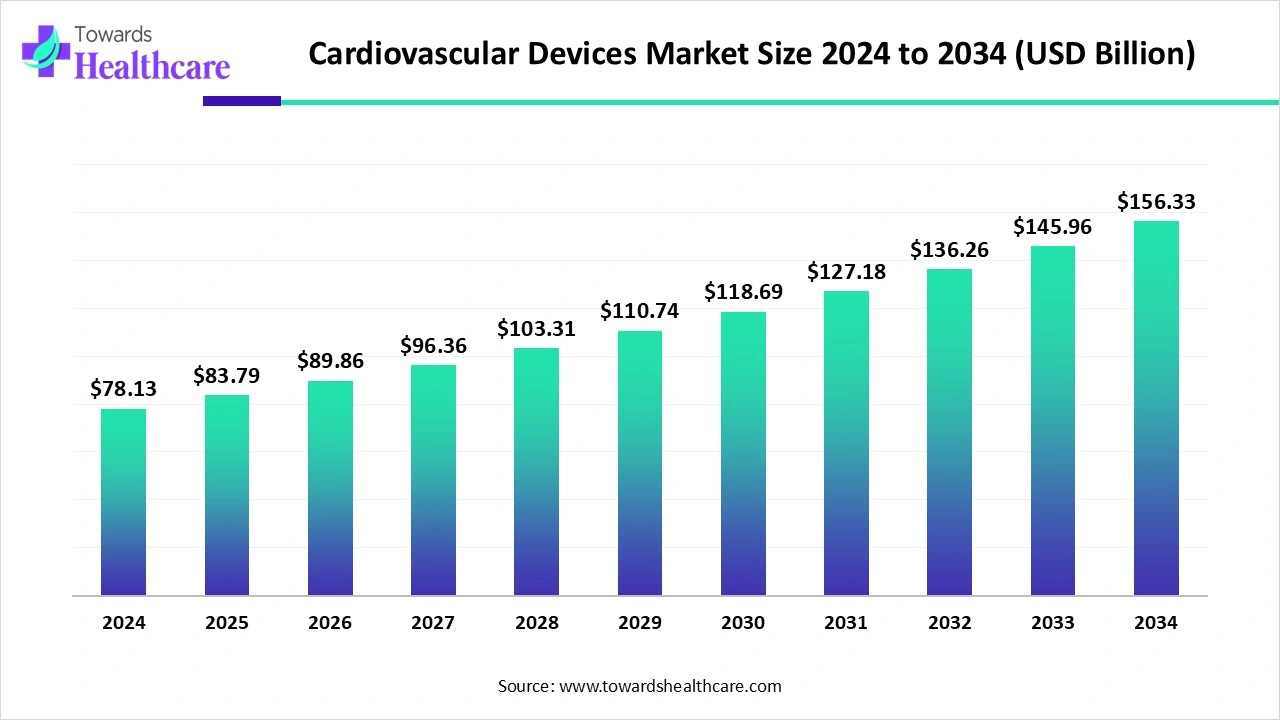

The global cardiovascular devices market is rapidly expanding, valued at USD 78.13 billion in 2024 and growing to USD 83.79 billion in 2025, with projections reaching USD 156.33 billion by 2034 at a CAGR of 7.24%. Growth is driven by rising cardiovascular disease prevalence, technological advancements, AI integration, and increased adoption of minimally invasive procedures across hospitals, ambulatory centers, and home healthcare.

Download this Free Sample Now and Get the Complete Report and Insights of this Market Easily @ https://www.towardshealthcare.com/download-sample/5911

Market Size

Global Market Size

●2024: USD 78.13 billion

●2025: USD 83.79 billion

●2034: USD 156.33 billion

●CAGR: 7.24% (2025–2034)

Product Class Share (2024)

●Implantable devices: 62%

●Non-implantable devices: projected fastest growth

Technology Adoption (2024)

●Minimally invasive & transcatheter: 45%

●Robotic-assisted intervention: projected fastest growth

End User Share (2024)

●Hospitals: 55%

●Ambulatory surgical centers: projected fastest growth

Product Type Dominance

●Interventional cardiology devices: 32%

●Structural heart devices: fastest growth segment

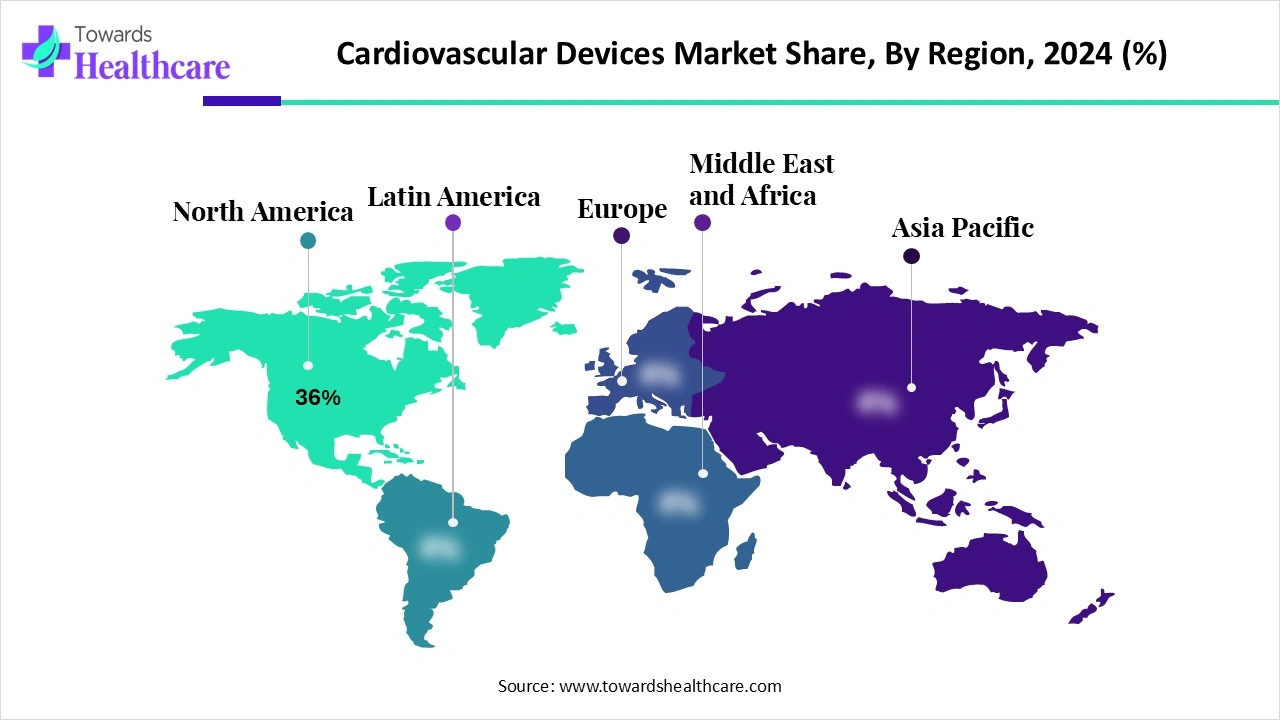

Regional Market Share (2024)

●North America: 36%

●Asia Pacific: fastest-growing region (2025–2034)

Market Trends

Minimally Invasive & Transcatheter Technologies

●Preferred due to reduced complications, shorter recovery, and high efficacy in aging populations.

Robotic-Assisted Intervention Systems

●Increasing adoption for high-precision surgeries and complex procedures.

AI Integration

●AI-driven diagnostics, predictive analytics, and treatment planning becoming standard.

Wearable Monitoring Devices

●Rise of home monitoring and early detection solutions like MyoBioScan patch.

Biodegradable & Drug-Eluting Materials

●Enhancing safety and performance of stents and vascular grafts.

3D Printing & Patient-Specific Implants

●Used in structural heart interventions for complex anatomies.

Telehealth & Remote Monitoring

●Remote cardiac care platforms (e.g., KeeboHealth by OMRON & Tricog) supporting “Going for Zero” cardiovascular events.

Government Reimbursement Policies

●Encourage adoption of advanced cardiovascular devices in hospitals and clinics.

Rising Investment & Collaborations

●Series E funding for Cardiac Dimensions ($53M), ADIA investment in Meril ($200M).

Medical Tourism & Access Expansion

●High adoption in Asia Pacific driven by advanced healthcare facilities and cost-effective care.

Role of AI in Cardiovascular Devices Market

Early Diagnosis

●AI algorithms detect early signs of heart diseases via imaging and wearable devices.

Predictive Analytics

●Machine learning predicts device performance and potential complications.

Treatment Personalization

●AI provides tailored therapy plans based on patient-specific data.

Monitoring & Alerts

●Continuous monitoring platforms like MyoBioScan alert patients to cardiovascular stress.

Procedure Optimization

●AI-assisted platforms guide surgeons in real-time during complex interventions.

Clinical Decision Support

●Reduces errors and improves outcomes by suggesting optimal interventions.

Device Development

●AI enhances design of stents, pacemakers, and valve replacement systems.

Remote Care Management

●Telehealth platforms integrate AI to track patients’ vitals remotely.

Predicting Disease Progression

●AI predicts heart failure progression and arrhythmia risks.

Risk Assessment & Precision Prevention

●Systems like AnginaX AI enable precision-led risk assessment and prevention strategies.

Regional Insights

North America

Market Share (2024): 36%

Key Drivers:

●Robust healthcare infrastructure and presence of advanced medical technologies.

●High investments in R&D and clinical studies.

U.S.:

●Rising prevalence of cardiovascular diseases drives demand for monitoring and therapeutic devices.

●Reimbursement policies by government and insurance providers encourage adoption of high-cost cardiovascular devices.

●Rapid integration of innovations such as robotic-assisted systems, AI-based monitoring, and minimally invasive procedures.

Canada:

●Well-developed healthcare sector supports widespread device adoption.

●Collaborative R&D initiatives between medical institutions and device manufacturers accelerate innovation.

●Early adoption of advanced imaging, wearable monitors, and structural heart devices enhances patient outcomes.

Subpoint:

●The combination of strong regulatory frameworks, funding support, and patient awareness positions North America as the leading regional market.

Asia Pacific

Growth Outlook: Fastest-growing region (2025–2034)

Key Drivers:

●Increasing cardiovascular disease prevalence due to urbanization, lifestyle changes, and aging populations.

●Rapidly improving healthcare infrastructure and hospital capacity.

●Expansion of medical tourism, particularly in countries like India and Thailand.

China:

●Large population base leads to a significant cardiovascular disease burden.

●Government initiatives and hospital expansions encourage adoption of minimally invasive devices, stents, and pacemakers.

●Increasing awareness and affordability drive demand for diagnostic and therapeutic cardiovascular devices.

India:

●Healthcare advancements and government support for cardiovascular interventions boost adoption of advanced devices.

●Growing private healthcare sector and medical tourism facilitate access to modern treatments.

●Rising awareness among patients and healthcare providers promotes early diagnosis and device utilization.

Subpoint:

●Asia Pacific represents a high-potential growth market due to demographic trends, rising disposable income, and adoption of innovative cardiovascular solutions.

Europe

Market Drivers: Strong healthcare infrastructure and established regulatory frameworks.

Germany:

●Emphasis on minimally invasive interventions for structural heart and interventional cardiology devices.

●Integration of advanced technologies like robotic-assisted surgery and AI-driven imaging enhances procedural precision.

UK:

●Growing adoption of wearable diagnostic devices for early detection of cardiovascular conditions.

●Funding and support for clinical trials accelerate introduction of innovative devices.

Subpoint:

●Europe’s high clinical standards, supportive reimbursement systems, and innovative healthcare environment sustain steady market growth.

Latin America & Middle East & Africa (MEA)

Market Drivers:

●Emerging awareness of cardiovascular diseases among populations.

●Improving healthcare infrastructure in major countries like Brazil, Mexico, UAE, and South Africa.

Challenges:

●Limited access to advanced devices in rural or resource-constrained areas.

●Dependence on imports for high-end cardiovascular devices.

Opportunities:

●Growing private healthcare sector and medical tourism in urban centers can accelerate adoption.

●Increasing government initiatives for preventive healthcare support expansion of cardiovascular diagnostics and monitoring devices.

Subpoint:

●LATAM and MEA are still developing markets, but rising awareness, better infrastructure, and policy support are enabling gradual growth.

Market Dynamics

Drivers

Rising Cardiovascular Diseases

Global Impact: Cardiovascular diseases (CVDs) remain the leading cause of death worldwide, with prevalence rising due to aging populations, lifestyle factors, and increased chronic conditions.

Market Effect: This growing disease burden fuels demand for diagnostic, monitoring, and therapeutic cardiovascular devices such as stents, pacemakers, and structural heart devices.

Subpoint:

●Early diagnosis tools, like AI-enabled blood pressure monitors and wearable patches (e.g., MyoBioScan), are gaining traction.

●Hospitals and clinics increasingly adopt advanced devices to manage complex cardiac conditions, boosting market revenue.

Technological Innovation

Minimally Invasive Devices: Devices like TAVR systems and interventional catheters reduce surgical risk, shorten recovery times, and improve patient acceptance.

Robotic-Assisted Systems: Enhance procedural precision in complex cardiovascular surgeries, reduce complications, and optimize outcomes.

AI-Based Devices: Artificial intelligence improves diagnosis, predicts device performance, and supports personalized treatment strategies.

Subpoint:

●Innovations in imaging systems (3D echocardiography, intravascular imaging) and bioabsorbable stents are enhancing procedure safety.

●Telehealth and remote monitoring platforms allow continuous patient surveillance, increasing device utilization outside hospitals.

Increased Investment & Funding

Impact on Market: Funding supports new product development, clinical trials, and global commercialization.

Examples:

●Abu Dhabi Investment Authority’s $200M stake in Meril supports cardiovascular device innovations.

●Cardiac Dimensions’ $53M Series E funding enables development of the Carillon Mitral Contour System.

Subpoint:

●These investments accelerate R&D, promote collaborations between companies, and encourage entry of new players in emerging markets.

Restraints

High Device Costs

Market Challenge: Many cardiovascular devices are expensive due to advanced technology, high-quality materials, and rigorous clinical testing.

Effect:

●Low-resource hospitals and developing regions may find devices unaffordable, limiting adoption.

●Patients without adequate insurance or reimbursement options may opt for cheaper alternatives.

Limited Access in Developing Markets

Infrastructure Constraint: Lack of specialized healthcare facilities, trained personnel, and regulatory support reduces adoption.

Effect on Market:

●Slower market growth in regions where hospital infrastructure and device availability are limited.

●Hinders penetration of advanced devices such as robotic-assisted systems and TAVR platforms.

Opportunities

Innovation in Personalized & 3D-Printed Devices

Patient-Specific Solutions: Use of 3D printing for valves, stents, and surgical models enables highly customized treatments.

Market Benefit:

●Reduces procedural complications and recovery time.

●Enhances clinical outcomes, especially in complex structural heart diseases.

Subpoint:

●Hospitals and specialized cardiac centers adopt these technologies for high-risk patients, promoting device innovation.

AI-Driven Early Detection

Impact: AI-enabled wearables, telehealth platforms, and diagnostic devices improve early identification of cardiovascular stress or disease progression.

Benefits:

●Enables preventive strategies, reduces hospitalizations, and optimizes patient management.

●Increases demand for home-based monitoring devices and wearable cardiovascular solutions.

Examples:

●AI platforms like AnginaX and MyoBioScan help clinicians predict cardiovascular risks and personalize treatment plans.

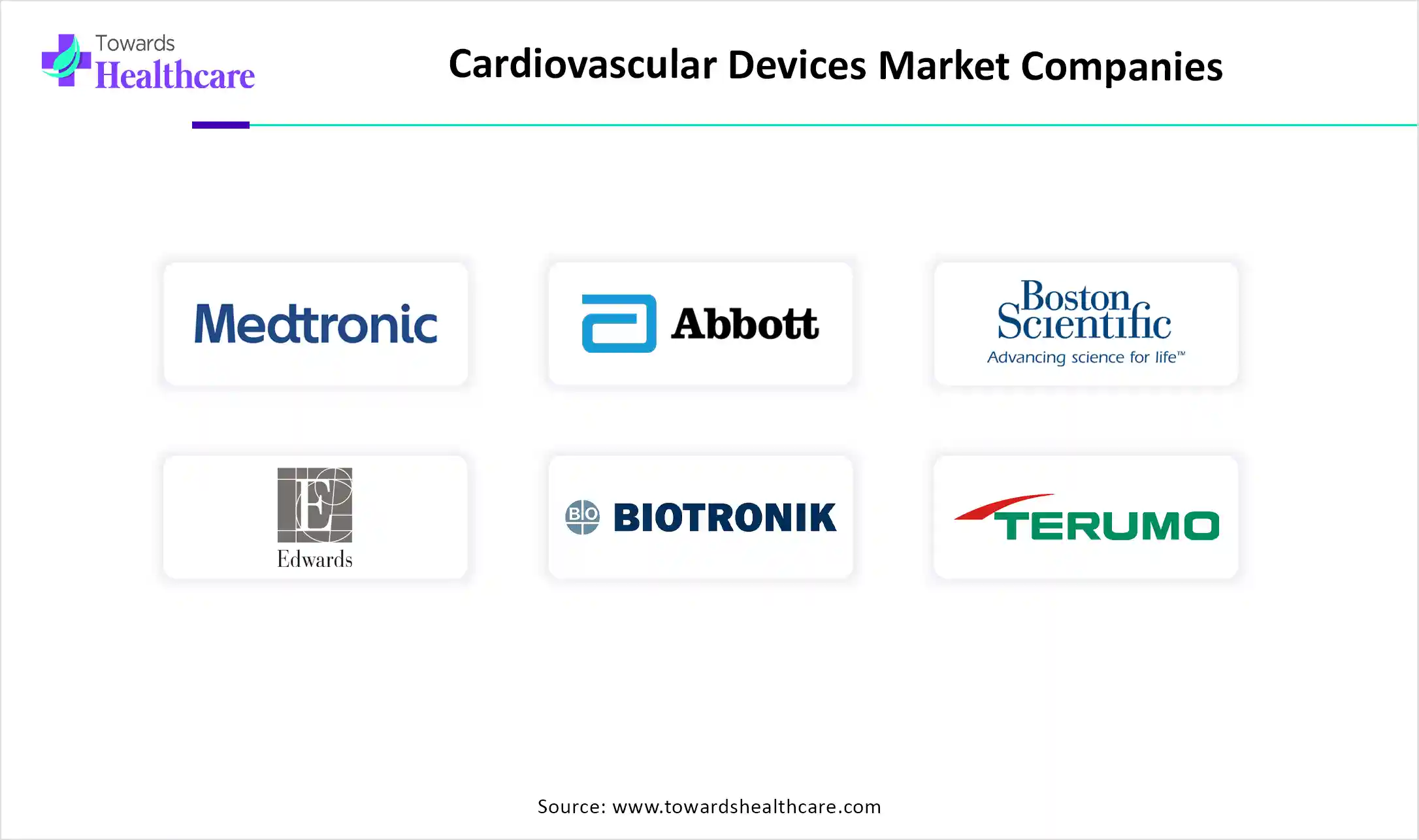

Top Companies

1. Medtronic plc

Products: Pacemakers, Implantable Cardioverter-Defibrillators (ICDs), Cardiac Resynchronization Therapy (CRT) devices

Overview: Global leader in implantable cardiac devices; provides solutions for chronic heart disorders and arrhythmia management

Strength: Extensive R&D, broad product portfolio, strong global market presence

2. Abbott Laboratories

Products: Structural heart devices, vascular devices, minimally invasive platforms

Overview: Specializes in structural heart interventions and interventional cardiology solutions

Strength: Innovations in minimally invasive devices, strong global distribution network

3. Boston Scientific Corporation

Products: Coronary stents, catheters, rhythm management devices

Overview: Focused on interventional cardiology and cardiac rhythm management solutions

Strength: Robust interventional cardiology portfolio, wide clinical adoption

4. Edwards Lifesciences Corporation

Products: Heart valves, transcatheter devices, TAVR systems

Overview: Leader in structural heart interventions and minimally invasive valve replacement

Strength: Advanced structural heart technologies, global recognition in valve treatments

5. BIOTRONIK SE & Co. KG

Products: Cardiac rhythm management devices, stents

Overview: Provides innovative solutions for arrhythmia management and vascular interventions

Strength: Advanced device technology, strong global presence, focus on precision medicine

6. Terumo Corporation

Products: Vascular intervention devices, cardiac catheters

Overview: Develops interventional cardiology and minimally invasive cardiovascular solutions

Strength: Strong presence in Asia Pacific, broad device portfolio

7. B. Braun Melsungen AG

Products: Catheters, vascular products, interventional supplies

Overview: Supplies integrated cardiovascular solutions for hospitals and clinics

Strength: Comprehensive hospital solutions, high-quality vascular products

8. Johnson & Johnson (Cordis, Biosense Webster)

Products: Pacemakers, electrophysiology devices, cardiac mapping systems

Overview: Offers broad cardiac rhythm and interventional solutions globally

Strength: Extensive R&D, strong global distribution, high clinical adoption

9. Siemens Healthineers

Products: Cardiovascular imaging systems, diagnostic platforms

Overview: Specializes in high-quality imaging for diagnosis, preoperative planning, and monitoring

Strength: Advanced diagnostic imaging, high accuracy, integration with AI analytics

10. GE Healthcare

Products: Cardiovascular imaging & monitoring systems

Overview: Provides imaging, monitoring, and analytic solutions for cardiovascular care

Strength: Innovative imaging platforms, AI-driven diagnostics, strong global reach

Latest Announcements

AnginaX AI (July 2025) – Personalized CVD prevention and treatment in India via AI-driven system.

ARTIST Trial Expansion (July 2025) – Broadening transcatheter aortic valve replacement for severe AR patients.

Meril Investment (July 2025) – $200M by ADIA for 3% stake; boosts cardiovascular device innovation.

Cardiac Dimensions Funding (March 2025) – $53M for pivotal mitral valve repair study (Carillon system).

BD AI Hemodynamic Platform (April 2025) – Optimizes intraoperative blood flow and stability.

KeeboHealth Launch (July 2025) – OMRON & Tricog AI-driven remote cardiac care platform.

Recent Developments

MyoBioScan AI Device (July 2025) – Wearable patch for early cardiovascular stress detection by KSOU, Mysuru.

KeeboHealth AI Platform (July 2025) – Advanced connected health system for remote cardiac monitoring.

Expansion of ARTIST Trial (July 2025) – Guides structural heart treatment decisions and patient eligibility.

Segments Covered

By Product Type

Interventional Cardiology Devices

Components: Coronary stents, PTCA (percutaneous transluminal coronary angioplasty) balloons, guidewires, and catheters.

Role: These devices are used for minimally invasive procedures to open blocked arteries, restore blood flow, and reduce cardiovascular events.

Trends:

●Increasing adoption of drug-eluting and bioabsorbable stents.

●Catheters and balloons are being improved with AI-guided navigation for higher precision.

Market Impact: Led the product type segment with ~32% share in 2024.

Cardiac Rhythm Management Devices

Components: Pacemakers, Implantable Cardioverter-Defibrillators (ICDs), Cardiac Resynchronization Therapy (CRT) devices.

Role: Manage arrhythmias, prevent sudden cardiac death, and synchronize heart chambers.

Trends:

●Leadless pacemakers and subcutaneous ICDs are gaining traction.

●Remote monitoring via AI and telehealth platforms enhances device management.

Market Impact: Widely used in hospitals and cardiac clinics; adoption is growing due to rising arrhythmia prevalence.

Structural Heart Devices

Components: Transcatheter Aortic Valve Replacement (TAVR) systems, mitral valve repair/replacement devices, Left Atrial Appendage (LAA) closure devices.

Role: Treat structural defects and valve disorders without open-heart surgery.

Trends:

●Increasing use of patient-specific implants and 3D-printed surgical models.

●Structural heart devices expected to show the fastest growth in product type.

Market Impact: Addresses aging population and complex valve disease cases.

Imaging Systems & Vascular Prostheses

Components: Intravascular imaging systems, cardiovascular imaging platforms, vascular grafts, and prostheses.

Role: Aid in diagnostics, preoperative planning, and post-procedure monitoring.

Trends:

●3D imaging and AI-based analysis improve accuracy of diagnosis.

●Integration with robotic-assisted systems enhances procedural efficiency.

Market Impact: Critical for planning minimally invasive procedures and reducing surgical risks.

Heart Failure & Assist Devices

Components: Intra-Aortic Balloon Pumps (IABP), Ventricular Assist Devices (VAD).

Role: Provide mechanical circulatory support in severe heart failure and during cardiac surgeries.

Trends:

●Growing adoption in intensive care and hospital settings.

●AI-based monitoring improves patient outcomes and device performance.

Market Impact: Supports high-risk cardiac patients, especially in tertiary care hospitals.

Non-Invasive Monitors

Components: Blood pressure monitors, heart rate monitors, electrophysiology catheters.

Role: Enable early detection, remote monitoring, and continuous cardiovascular health tracking.

Trends:

●Wearable AI-enabled patches like MyoBioScan alert patients to cardiovascular stress.

●Integration with telehealth platforms for home-based care.

Market Impact: Increasing patient awareness and self-monitoring are driving adoption outside hospital settings.

By End User

Hospitals

Role: Primary centers for cardiovascular procedures, offering advanced devices and skilled personnel.

Market Impact: Held ~55% share in 2024 due to high patient volume and infrastructure.

Ambulatory Surgical Centers

Role: Provide cost-effective, fast, and minimally invasive cardiovascular treatments.

Market Trend: Expected to be the fastest-growing end user segment.

Cardiac Clinics

Role: Focus on diagnostics, outpatient monitoring, and chronic cardiovascular management.

Trend: Increasing adoption of portable monitors and AI-guided devices.

Diagnostic Imaging Centers

Role: Support precise cardiovascular imaging and pre-surgical planning.

Trend: Growth linked to AI-driven imaging technologies.

Home Healthcare

Role: Remote monitoring and management of cardiovascular health using wearable devices.

Trend: Driven by telehealth and patient preference for convenience.

By Technology

Minimally Invasive & Transcatheter Technologies

●Reduce surgical risk, shorten recovery, and are widely adopted in interventional cardiology.

Robotic-Assisted Intervention Systems

●Enhance accuracy in complex procedures and allow precise manipulation in confined spaces.

3D Imaging & Echocardiography

●Improve diagnostics, preoperative planning, and procedural outcomes.

Remote Patient Monitoring & Telehealth Platforms

●Enable continuous tracking of vitals, early risk detection, and reduced hospital visits.

3D Printing for Patient-Specific Implants

●Customizes valves, stents, and grafts for individual patient anatomy, improving efficacy.

Bioabsorbable & Drug-Eluting Materials

●Reduce long-term complications and improve safety of stents and vascular devices.

By Product Class

Implantable Devices

●Includes pacemakers, ICDs, CRT devices, and TAVR systems.

●Dominated the market in 2024 with ~62% share.

Non-Implantable Devices

●Includes portable monitors, IABP, VADs.

●Expected to show the fastest growth due to early detection and wearable adoption.

Diagnostic Monitors

●Blood pressure monitors, heart rate monitors, electrophysiology devices.

●Increasing adoption in home healthcare and outpatient clinics.

External Assist Devices

●Devices supporting cardiac function externally, e.g., external pacemakers or temporary circulatory assist.

Disposable Cath Lab Supplies

●Consumables used during interventional procedures, including catheters, guidewires, and balloons.

●Growth tied to rising minimally invasive procedures and hospital throughput.

Top 5 FAQs

What is the current size of the cardiovascular devices market?

●USD 78.13B in 2024; USD 83.79B in 2025; projected USD 156.33B by 2034.

Which region leads the cardiovascular devices market?

●North America, with 36% share in 2024.

What is the fastest-growing segment in technology?

●Robotic-assisted intervention systems are projected to grow fastest.

How is AI impacting the cardiovascular devices market?

●AI supports early diagnosis, predictive analytics, treatment personalization, monitoring, and device development.

Who are the top companies in the market?

●Medtronic, Abbott, Boston Scientific, Edwards Lifesciences, BIOTRONIK, Terumo, B. Braun, Johnson & Johnson, Siemens Healthineers, GE Healthcare.

Access our exclusive, data-rich dashboard dedicated to the medical devices industry – built specifically for decision-makers, strategists, and industry leaders. The dashboard features comprehensive statistical data, segment-wise market breakdowns, regional performance shares, detailed company profiles, annual updates, and much more. From market sizing to competitive intelligence, this powerful tool is one-stop solution to your gateway.

Access the Dashboard: https://www.towardshealthcare.com/access-dashboard

Immediate Delivery Available | Buy This Premium Research @ https://www.towardshealthcare.com/price/5911

Become a valued research partner with us – https://www.towardshealthcare.com/schedule-meeting

You can place an order or ask any questions, please feel free to contact us at sales@towardshealthcare.com

Powering Healthcare Leaders with Real-Time Insights: https://www.towardshealthcare.com/healthcare-intelligence-platform

Europe Region – +44 778 256 0738

North America Region – +1 8044 4193 44

APAC Region: +91 9356 9282 04

Web: https://www.towardshealthcare.com

Find us on social platforms: LinkedIn | Twitter | Instagram | Medium | Pinterest