Generative AI in Life Sciences Market to Reach USD 1.65 Billion by 2034

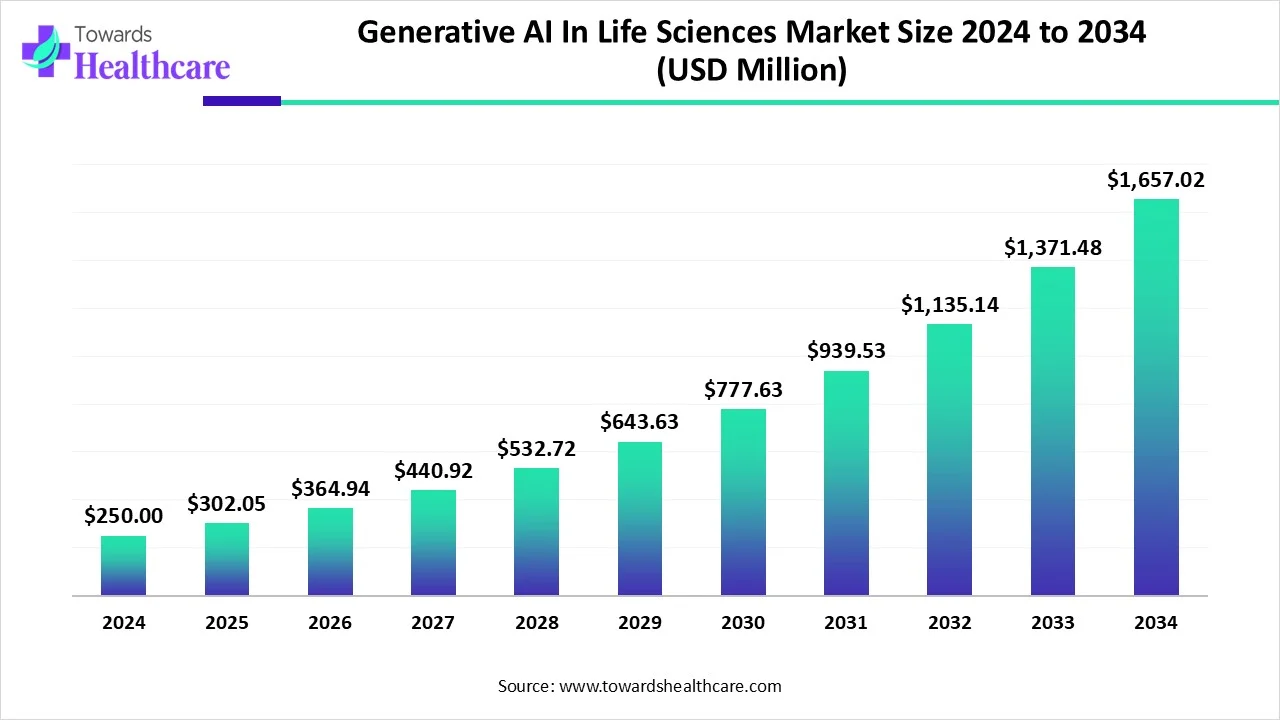

The global Generative AI in Life Sciences market was estimated at USD 250 million in 2024, grew to USD 302.05 million in 2025, and is projected to reach ≈ USD 1,657.02 million by 2034 — implying a CAGR of 20.82% (2025–2034) as GenAI accelerates drug discovery, clinical-trial design and personalized medicine by turning vast chemical, biological and patient datasets into actionable molecular designs, trial optimizations and diagnostic/therapeutic insights.

Download this Free Sample Now and Get the Complete Report and Insights of this Market Easily @ https://www.towardshealthcare.com/download-sample/5735

Table of Contents

ToggleMarket size

●2024 (baseline): USD 250 million (reported estimate).

●2025: USD 302.05 million (reported estimate).

●2034 (projection): USD 1,657.02 million (USD 1.657 billion).

●Compound Annual Growth Rate (2025–2034): 20.82% CAGR — rapid expansion driven by adoption across drug discovery, protein engineering and clinical operations.

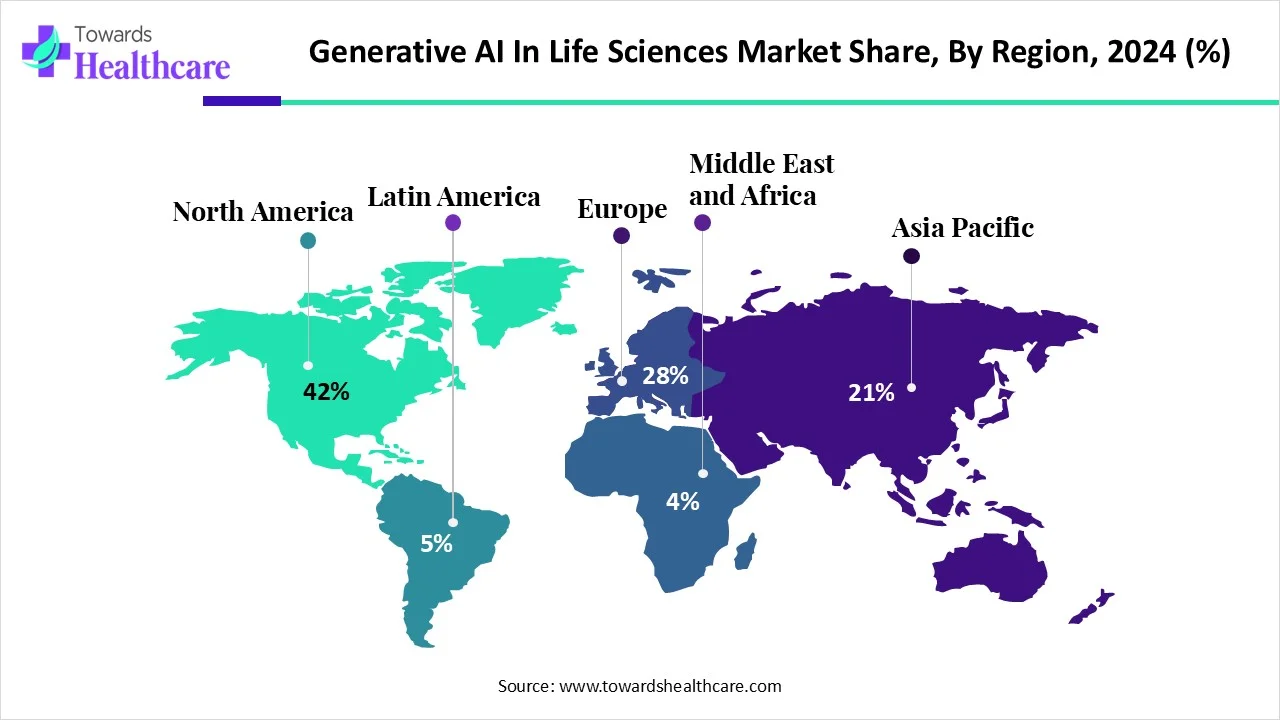

●Regional share snapshot (2024): North America ≈ 42% revenue share (largest single-region share).

●Fastest-growing region (forecast 2025–2034): Asia-Pacific (expected to outpace other regions in percentage growth).

●Market structure: Technology-led segmentation (novel molecule generation, protein sequence design, synthetic gene design, single-cell RNA sequencing, data augmentation) and cross-cutting infrastructure and services (foundation models, model training data pipelines, platform integrations and compute/HPC).

Market Trends

Investment & strategic partnerships are increasing (2024–mid-2025).

●Multiple investments and partnerships reported: e.g., Healthcare Capital → Lifesigns (Feb 2025), AWS ↔ MSK partnership (Feb 2025), Bluenote financing ($10M, Dec 2024).

●Implication: venture and corporate capital is validating GenAI use cases in life sciences beyond pilots into funded scale projects.

Cloud + HPC integration for life-science GenAI is maturing.

●AWS partnership with MSK shows major cloud providers are positioning HPC and GenAI stacks specifically for clinical and drug research workloads.

Verticalized GenAI platforms are emerging.

●Companies are building fit-for-purpose GenAI platforms (e.g., Indegene’s Cortex) rather than generic LLMs — tailored data schemas, regulatory-awareness, domain fine-tuning.

Novel molecule generation leads current tech adoption.

●In 2024, the novel molecule generation segment led revenues because it directly shortens early discovery timelines and reduces costs of candidate generation and virtual screening.

Protein sequence design set for rapid expansion.

●Protein sequence design flagged as a high growth subsegment: GenAI enables rapid in silico engineering and variant testing at scale.

Clinical trial automation and optimization are emerging as a major growth vector.

●Clinical trial application expected to grow fastest: patient selection, eligibility screening, endpoint prediction and monitoring get immediate operational ROI.

Regulatory and compliance focus is increasing (implicit trend).

●As real-world tools influence trial protocols and diagnostics, providers are designing GenAI outputs to be auditable, bias-checked and compliant.

Platformization of chemical and biological generative models.

●Movement from point tools to platform stacks: molecule generator → property predictor → in silico ADMET screening → integration with experimental CROs.

Cross-discipline collaborations (techbiotech partnerships).

●Example: Nxera (Sosei Heptares) + Antiverse (Nov 2024) for antibody design — shows pairing of biotech domain knowledge with GenAI capabilities.

Rising attention on data privacy, bias & model governance.

●Restraint trend: heavy reliance on sensitive patient/clinical data drives investments in privacy-preserving ML, governance and careful training-data curation.

AI impacts / roles

Novel molecule generation — idea → candidate at machine speed.

●Mechanism: generative models propose chemical structures conditioned on target properties; property predictors filter for stability, synthesizability and ADMET.

●Benefit: reduces months/years of iterative medicinal chemistry cycles; multiplies candidate diversity.

Protein sequence design and engineering.

●Mechanism: language-model-style representations of amino acid sequences predict structure–function relationships and suggest beneficial mutations.

●Benefit: accelerates design of enzymes, biologics and therapeutic proteins with targeted functions, fewer wet-lab rounds.

In silico preclinical evaluation (virtual ADMET/PK).

●Mechanism: generative + predictive pipelines simulate absorption, metabolism, toxicity.

●Benefit: early de-risking of candidates and reduced animal testing footprint.

Clinical trial design optimization and synthetic cohorts.

●Mechanism: GenAI simulates trial arms, generates synthetic patient cohorts, and predicts endpoints to refine protocol parameters.

●Benefit: fewer failed trials, better-powered studies and faster go/no-go decisions.

Patient selection and recruitment augmentation.

●Mechanism: models parse EHRs and registries, identify eligible patients and predict recruitment rates.

●Benefit: quicker recruitment, improved representativeness, lower site costs.

Data augmentation and label synthesis for scarce datasets.

●Mechanism: generative models create realistic, diverse synthetic datasets (e.g., patient records, single-cell profiles) for training robust models.

●Benefit: mitigates small-sample problems and reduces sharing of actual PHI when used carefully.

Automated protocol & report generation (regulatory artifacts).

●Mechanism: GenAI drafts trial protocols, clinical study reports, and scientific summaries from structured inputs.

●Benefit: faster documentation, consistent formatting; frees domain experts for strategy rather than admin.

Diagnostics and image-based generative augmentation.

●Mechanism: GenAI helps synthesize rare pathological image variants and suggests diagnostic features.

●Benefit: improves model training for rare diseases and enhances diagnostic assistance tools.

Personalized medicine / treatment personalization.

●Mechanism: integrate patient multi-omics and clinical history to generate individualized treatment hypotheses.

●Benefit: tailored regimens, improved outcomes, fewer adverse events.

Accelerated R&D ideation and human-AI collaboration.

●Mechanism: GenAI acts as a creative partner — proposing hypotheses, mechanisms, and designs for experimental follow-up.

●Benefit: expands researcher creativity, increases throughput of testable ideas and shortens discovery cycles.

Regional insights

1) North America — leader in adoption & funding (2024: 42% revenue share)

●Ecosystem strength: dense concentration of pharma, biotech, top research hospitals and AI/cloud providers.

●Capital & R&D intensity: high private & public investment fueling fast translation from proof-of-concept to deployment.

●Regulatory engagement: active regulators and advisory bodies prompting early compliance frameworks (enabling clinical use-cases).

●Enterprise adoption: large pharma and tech firms (platforms, HPC, foundation models) act as early customers and integrators.

2) Asia-Pacific — fastest growth (forecast 2025–2034)

●Scaling manufacturing & clinical data volume: large patient populations and expanding R&D hubs (India, China, Japan, South Korea).

●Government & national strategy support: policy pushes for AI in healthcare, enabling pilots and localized platforms.

●Local innovation: rising number of home-grown GenAI life-science startups, partnerships with global vendors.

3) Europe (including Germany & UK) — applied adoption in education & diagnostics

●Medical education & simulation: high uptake of GenAI for medical training and simulation tools.

●Regulatory caution & ethics leadership: stronger privacy frameworks leading to careful, compliant deployments; European labs focus on explainability and auditability.

4) China — rapid industrialization of GenAI use in pharma

●Compound screening leadership: intense focus on AI-driven compound screening and rapid pipeline acceleration.

●Scale & data access: large datasets and focused domestic platform development.

5) Japan — methodical clinical & enterprise integration

●Pharma collaboration: established pharma companies deploying GenAI for datasets analysis and administrative automation.

●Operational improvements: use of GenAI for workflow optimization and hospital operations.

6) Canada & UK — national strategies enable startups & research hubs

●National AI strategies: funding and reskilling push fosters commercialization and bridging research → industry.

●Research hubs: specialized centers linking hospitals, universities and industry.

7) Latin America & MEA — nascent adoption with targeted pockets

●Opportunities: improving trial design for regional health burdens and leveraging GenAI to compensate for limited infrastructure.

●Constraints: funding and data access may slow scale-up relative to NA/APAC/EU.

Market dynamics

Drivers

Urgent need to accelerate drug discovery: GenAI reduces early discovery timelines and cost; direct revenue effect reflected in high CAGR (20.82%).

Personalized medicine demand: need to convert multi-omics & clinical data into individualized treatments.

Integration with HPC/cloud: partnerships (e.g., AWS–MSK) and foundation models enable compute-intensive GenAI workloads.

Platform & vertical productization: increasing number of fit-for-purpose platforms (e.g., Indegene Cortex) that lower adoption friction.

Investment influx: venture financing (Bluenote $10M) and strategic corporate investments validate market monetization.

Restraints

Data privacy and security concerns: reliance on sensitive patient datasets increases regulatory/ethical constraints and slows certain deployments.

Model bias and reliability risks: biased training data can produce incorrect / unfair outputs, necessitating governance and human oversight.

Integration challenges: connecting GenAI outputs to wet-lab workflows, CROs and regulated documentation requires complexity and domain validation.

Skill gaps & reskilling needs: domain experts must learn how to safely use GenAI; organizations must invest in reskilling.

Opportunities

Clinical trial modernization: GenAI promises faster designs, synthetic cohorts and improved recruitment — clinical trials segment expected fastest CAGR.

Protein & biologics design expansion: protein sequence design poised for strong growth, offering a large TAM beyond small molecules.

Platform monetization & services: end-to-end GenAI platforms combining model IP, curated data, experimental integration and regulatory artifacts.

Cross-industry compute & tool partnerships: cloud + biotech collaborations extend market reach (e.g., Evogene + Google Cloud foundation model for small molecule design).

Top 10 companies

IBM Corporation

Product / offering: Enterprise AI platforms and life-sciences analytic stacks (historically Watson and enterprise AI services).

Overview: Large incumbent with strengths in regulated enterprise deployments, hybrid cloud and systems integration.

Strengths: Enterprise trust, regulatory experience, systems integration across large pharma pipelines.

AiCure LLC

Product / offering: AI-driven patient monitoring and adherence tracking (video/AI monitoring for trials).

Overview: Focus on measuring patient behavior and outcomes to improve trial data quality.

Strengths: Modalities for remote monitoring, patient engagement, and adherence insight that reduce trial data leakage.

MosaicML

Product / offering: Tools and frameworks to train large models more affordably and efficiently (foundation model training tech).

Overview: Model-training optimization specialist that enables institutions to build domain models.

Strengths: Cost efficiency in training foundation models, flexibility for domain fine-tuning.

NVIDIA

Product / offering: GPUs, software stacks (CUDA, Triton) and optimized AI infrastructure for model training & inference.

Overview: Hardware + software backbone for compute-intensive GenAI workloads in life sciences.

Strengths: Market-leading compute performance, ecosystem integrations (HPC, molecular simulation acceleration).

Insilico Medicine Inc.

Product / offering: AI-driven drug discovery platforms and molecule design pipelines.

Overview: Specialized use of generative models to propose candidate small molecules and prioritize leads.

Strengths: Deep focus on molecule generation and preclinical candidate identification; end-to-end discovery workflows.

Writer

Product / offering: Generative content platforms (enterprise writing assistants) tailored for regulated industries.

Overview: While not life-science specific, Writer’s tech can be applied to generate compliant regulatory or educational text.

Strengths: Content consistency, brand/regulatory guardrails and enterprise governance.

HealthArk

Product / offering: Healthcare data management and analytics platforms (inferred: data integration & insights).

Overview: Data orchestration and platform solutions to feed GenAI models with curated healthcare datasets.

Strengths: Data governance, interoperability and pipeline creation for model training.

Indegene

Product / offering: Cortex (fit-for-purpose GenAI platform for life sciences) and commercialization services.

Overview: Digital-first commercialization partner for pharma combining AI capabilities with domain expertise.

Strengths: Domain knowledge, productized GenAI for life sciences workflows and go-to-market experience.

Microsoft

Product / offering: Cloud (Azure) + AI stack and enterprise integrations; support for regulated deployments.

Overview: Cloud provider enabling secure, scalable GenAI workloads with enterprise compliance features.

Strengths: Broad enterprise reach, security/compliance tooling, partnerships with life-science customers.

(Additional notable) — Evogene / Capgemini / ConcertAI (mentioned in updates)

Evogene: computational biology company building a generative AI foundation model for small molecule design (strength: domain-specific foundation model).

Capgemini: developing pLLMs for protein engineering (strength: consulting + R&D scale to deploy domain models).

ConcertAI: oncology-focused generative & agentic AI solutions (strength: specialization in oncology insights & clinical actionability).

Latest announcements

Evogene Ltd — GenAI foundation model for small molecule design (June 2025)

What happened: Evogene announced completion of its Generative AI foundation model v1.0 (ChemPass AI) built with Google Cloud.

Significance: A domain-specific foundation model focused on small-molecule design suggests major step toward scalable molecule generation — enabling Evogene to generate wholly new molecules and integrate generated candidates into downstream discovery pipelines.

Implication for market: Validates foundation-model approach for chemistry and signals increased cloud + biotech co-development.

Capgemini — pLLM approach for protein engineering (Feb 2025)

What happened: Capgemini announced a GenAI approach employing a protein large language model (pLLM) to predict robust protein variants.

Significance: Shows consultancies moving beyond advisory roles to deliver model-driven R&D capabilities. pLLMs accelerate protein engineering and indicate demand for specialized LLMs in life sciences.

FDA — GenAI Elsa (June 2025)

What happened: FDA launched “GenAI Elsa” to support internal tasks like clinical trial protocol reviews and adverse event conclusions.

Significance: Regulatory body using GenAI internally is a major signal: regulators are evaluating and operationalizing GenAI, which may shorten review cycles and inform best practices for model governance.

ConcertAI — Precision Suite™ (May 2025)

What happened: ConcertAI launched a generative & agentic AI-powered Precision Suite™ for oncology insights and actions.

Significance: Demonstrates verticalized, clinical-action focused GenAI deployments that blend insights (analytics) with prescriptive actions for oncology.

Indegene — Cortex (Feb 2025)

What happened: Indegene launched Cortex, a fit-for-purpose GenAI platform for life sciences.

Significance: Highlights the trend of productized GenAI offerings built specifically for life sciences workflows (regulatory content, commercial ops, scientific workflows).

Quantiphi — Phi Labs (May 2025)

What happened: Quantiphi launched “Phi Labs” as its formal R&D identity to advance real-world AI solutions.

Significance: Firms establishing research hubs indicate longer-term commitments to domain research and model development.

Corporate investments & financing:

Bluenote (Dec 2024): CA-based GenAI platform raised $10M financing — feeds the narrative of venture activity in domain platforms.

Healthcare Capital → Lifesigns (Feb 2025): Investment in AI patient monitoring shows capital focusing on applied real-world health AI.

Recent developments

Regulatory bodies using GenAI (FDA GenAI Elsa, Jun 2025): Signals that regulators are not only evaluating but also adopting GenAI, which should accelerate standards for model validation, documentation and audit trails — making enterprise adoption safer and more mainstream.

Foundation models for chemistry & protein LLMs (Evogene, Capgemini): Domain foundation models (ChemPass AI, pLLMs) are maturing — these reduce model-training friction and allow transfer learning across drug discovery tasks.

Verticalized product launches (Indegene Cortex, ConcertAI Precision Suite): Companies are shipping end-user products (not just APIs); these products are tuned to workflow needs (commercial, clinical, oncology), reducing integration friction for life-science customers.

Increased R&D and financing (Bluenote, Quantiphi): Capital is flowing to both startups and R&D hubs, supporting sustained model development and domain dataset curation.

Collaborations between tech/cloud and life-science institutions (AWS–MSK, Evogene–Google Cloud): Strategic tech partnerships bring compute, domain knowledge and distribution networks together — enabling scale.

Segments covered

By Technology

Novel molecule generation

What it is: Generative models that propose entirely new chemical entities (NCEs) conditioned on desired properties (potency, solubility, synthesizability).

How it works: Generative architectures (autoencoders, flow models, diffusion models) generate SMILES/graph representations; followed by in-silico property predictors and chemoinformatics filters.

Value: Dominant revenue in 2024 because it directly reduces costs/time of hit-to-lead discovery.

Protein sequence design

What it is: Sequence-level generative models (pLLMs) that propose amino-acid substitutions or new proteins with targeted activities.

How it works: Language-model techniques trained on sequence databases map sequence → function and allow conditional generation for desired traits.

Value: Drives biologics/enzymes design, vaccine antigen engineering and therapeutic protein optimization.

Synthetic gene design

What it is: Generation and optimization of nucleotide sequences for expression, stability and manufacturability.

How it works: Models factor in codon usage, secondary structure and host expression constraints to propose gene constructs.

Value: Speeds up design for synthetic biology, gene therapy vectors and expression systems.

Single-cell RNA sequencing (scRNA-seq) augmentation & analysis

What it is: Generative augmentation and modeling of single-cell data to discover cell states and lineage trajectories.

How it works: Models augment sparse scRNA datasets, denoise expression profiles and simulate perturbation responses.

Value: Helps identify cellular targets, biomarkers and mechanism hypotheses.

Data augmentation for model training

What it is: Creating synthetic but realistic data (images, patient records, molecular simulations) to expand training sets.

How it works: Conditional generative models replicate rare cases and increase class balance while limiting PHI exposure.

Value: Improves model robustness, reduces overfitting and addresses small-sample problems.

By Application

Drug Discovery: End-to-end use of GenAI from target ID to lead generation.

Biotechnology: Protein/enzyme design, gene circuits and industrial bioprocess optimization.

Medical Diagnosis: AI-assisted diagnostic models, image augmentation and decision support.

Clinical Trials: Protocol drafting, synthetic cohorts, recruitment optimization and endpoint prediction.

Precision & Personalized Medicine: Multi-omics integration for individualized treatment planning.

Patient Monitoring: Remote monitoring, adherence detection and safety signals using generative augmentation.

Top 5 FAQs

Q: What is the current market size and growth outlook for Generative AI in Life Sciences?

A: The market was USD 250M in 2024, rose to USD 302.05M in 2025, and is projected to reach USD 1,657.02M by 2034, corresponding to a CAGR of 20.82% between 2025 and 2034.

Q: Which region led the market in 2024 and which region will grow fastest?

A: North America held the major revenue share in 2024 (≈42%). Asia-Pacific is expected to be the fastest-growing region during 2025–2034.

Q: Which technology subsegments are dominant or fastest-growing?

A: Novel molecule generation led the market in 2024. Protein sequence design is expected to grow significantly in the coming years.

Q: What are the main restraints to adoption?

A: Key restraints include data privacy & security concerns, model bias and reliability issues, and challenges integrating GenAI outputs into regulated lab/clinical workflows.

Q: Who are the leading companies and what are notable recent announcements?

A: Top players listed include IBM, AiCure, MosaicML, NVIDIA, Insilico, Writer, HealthArk, Indegene, Microsoft. Notable announcements include Evogene’s ChemPass AI foundation model (Jun 2025), Capgemini’s pLLM for protein engineering (Feb 2025), FDA’s GenAI Elsa (Jun 2025), ConcertAI’s Precision Suite (May 2025) and Indegene’s Cortex (Feb 2025).

Access our exclusive, data-rich dashboard dedicated to the healthcare market – built specifically for decision-makers, strategists, and industry leaders. The dashboard features comprehensive statistical data, segment-wise market breakdowns, regional performance shares, detailed company profiles, annual updates, and much more. From market sizing to competitive intelligence, this powerful tool is one-stop solution to your gateway.

Access the Dashboard: https://www.towardshealthcare.com/access-dashboard

Immediate Delivery Available | Buy This Premium Research @ https://www.towardshealthcare.com/price/5735

About Us

Towards Healthcare is a leading global provider of technological solutions, clinical research services, and advanced analytics, with a strong emphasis on life science research. Dedicated to advancing innovation in the life sciences sector, we build strategic partnerships that generate actionable insights and transformative breakthroughs. As a global strategy consulting firm, we empower life science leaders to gain a competitive edge, drive research excellence, and accelerate sustainable growth.

Become a valued research partner with us – https://www.towardshealthcare.com/schedule-meeting

You can place an order or ask any questions, please feel free to contact us at sales@towardshealthcare.com

Powering Healthcare Leaders with Real-Time Insights: https://www.towardshealthcare.com/healthcare-intelligence-platform

Europe Region – +44 778 256 0738

North America Region – +1 8044 4193 44

APAC Region: +91 9356 9282 04

Web: https://www.towardshealthcare.com

Find us on social platforms: LinkedIn | Twitter | Instagram | Medium | Pinterest