Genomics Market Size, Shares and Industry Reports 2034

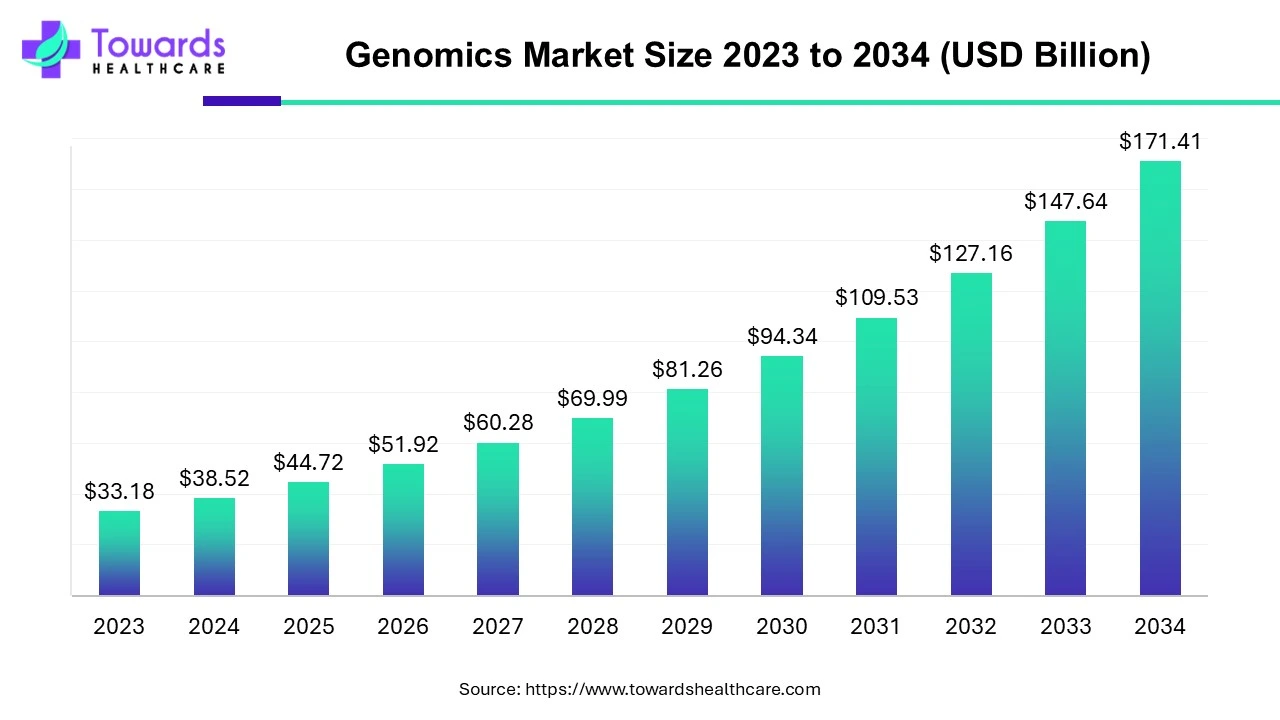

The global genomics market size is projected to reach USD 171.41 billion by 2034, growing from USD 44.72 billion in 2025 at a CAGR of 16.1%, driven by technological advancements, AI integration, and the rising demand for personalized medicine.

Download the Free Sample of Genomics Market Now and Get the Complete Report Easily at: https://www.towardshealthcare.com/download-sample/5065

Table of Contents

ToggleMarket Size and Growth Insights

Market Value Expansion:

●2024: USD 38.52 billion

●2025: USD 44.72 billion

●2034: USD 171.41 billion

●CAGR (2025–2034): 16.1%

Dominant Region:

●North America led the market in 2024 due to advanced infrastructure, high R&D funding, and strong adoption of precision medicine.

●Asia-Pacific projected as the fastest-growing region driven by genomics-focused government programs in India, Japan, and China.

Leading Technology:

●Polymerase Chain Reaction (PCR) held the largest market share in 2024 and is projected to be the fastest-growing technology due to accuracy, cost-effectiveness, and use in drug discovery.

Major Segments by Deliverables:

●Products: Dominated in 2024 (sequencing kits, microarray kits, reagents, and instruments).

●Services: Expected to grow steadily owing to cost-efficient outsourcing of genomic testing.

End-User Insights:

●Pharmaceutical & Biotechnology Companies: Largest contributors due to new product launches and R&D activities.

●Hospitals & Clinics: Rapidly expanding as genomics integrates with diagnostics and patient-specific treatments.

Market Trends

AI Collaboration in Genomics (NVIDIA–Illumina–Mayo Clinic, 2025):

●NVIDIA’s partnership to accelerate drug discovery with agentic AI transforms research capabilities across the $10 trillion healthcare sector.

WHO Ethical Guidelines (2024):

●Framework established for ethical genomic data use and sharing, ensuring equitable and responsible global collaboration.

Investment in AI-Powered Genomic Infrastructure (Accenture & 1910 Genetics, 2024):

●Collaboration supports AI-driven drug target identification and cost-effective therapeutics.

Government Initiatives (India, 2025):

●Launch of IBDC genomic dataset making India self-reliant in genomic data and advancing precision medicine.

Expansion of NGS (Next-Generation Sequencing):

●Enhanced accessibility due to cost reductions and improved throughput.

Multi-Omics Integration:

●Cross-disciplinary integration (proteomics, metabolomics) enhances understanding of disease mechanisms.

Rise of Functional Genomics:

●Increasing R&D in gene expression and disease cause identification accelerates market expansion.

Strategic Collaborations:

●GeneDx acquisition of Fabric Genomics (2025) merges AI interpretation and genomic medicine.

Emerging Data Privacy Regulations:

●Stricter frameworks across Europe and North America ensuring secure genomic data handling.

Shift to Clinical Implementation:

●Hospitals adopting genomic testing for chronic and rare diseases to improve diagnostic precision.

10 Deep AI Impacts and Roles in the Genomics Market

Genomic Data Interpretation:

●AI algorithms decode complex patterns across billions of sequences, enhancing diagnostic accuracy.

Predictive Disease Modeling:

●Machine learning predicts disease susceptibility, treatment responses, and hereditary risks.

3D Genome Structural Analysis:

●AI can compute thousands of 3D genome structures rapidly, supporting advanced research.

Data Integration Across EHRs:

●AI links genomic data with electronic health records to create holistic patient profiles.

Drug Discovery Optimization:

●NVIDIA’s AI accelerates drug identification and clinical trial design efficiency.

Automation of Sequencing Analysis:

●Reduces manual interpretation errors and speeds up genetic variant annotation.

AI-Powered Diagnostics:

●Models like SCADE by Valted Seq deliver real-time genomic interpretation for clinical use.

Personalized Therapy Design:

●AI tailors treatments to genetic and phenotypic profiles, enabling precision oncology.

Bioinformatics Enhancement:

●Advanced algorithms support multi-omics data integration and biomarker discovery.

Scalable Infrastructure for Genomics Data:

●AI cloud systems ensure efficient management of petabyte-scale datasets for research and clinical institutions.

Regional Insights

North America (Leading Region)

Dominance Drivers:

●Robust research funding (NHGRI budget of USD 639 million in 2025).

●Early adoption of genomic initiatives such as the Precision Medicine Initiative.

Industry Presence:

●Home to top players like Illumina, Thermo Fisher, and NVIDIA.

Regulatory Support:

●Favorable U.S. FDA approvals for gene therapies (15 approved by 2024).

Europe

●Key Markets: UK, Germany, France.

●Regulatory Framework: Strong compliance standards for genetic testing enhance reliability.

●Focus Area: Integration of genomics in national healthcare systems.

●Collaborative Programs: EU-funded research advancing personalized healthcare.

Asia-Pacific (Fastest-Growing Region)

Growth Catalysts:

●National genomic data programs (India’s IBDC, China’s genome sequencing initiatives).

●Government investments in precision medicine.

Emerging Players:

●Regional biotech startups integrating AI in sequencing.

Opportunity:

●Large population base and rising chronic disease burden.

Latin America & MEA

●Latin America: Brazil and Argentina are expanding genomic diagnostic centers.

●Middle East & Africa: UAE and Saudi Arabia investing in national genome projects, establishing data centers for precision medicine.

Market Dynamics

Drivers

●Rising prevalence of genetic disorders (70–80 million affected globally).

●Technological advancement in sequencing and PCR.

●Declining sequencing costs improving accessibility.

●Integration of genomics with precision medicine.

●Strong collaborations between AI and genomics companies.

Restraints

●Complexity in interpreting genomic data.

●Lack of skilled bioinformaticians.

●Ethical and privacy concerns.

●Inconsistent reimbursement policies.

●High initial setup costs.

Opportunities

●Multi-omics integration (genomics + proteomics + metabolomics).

●AI-driven drug discovery and diagnostics.

●Expansion in developing regions (India, China).

●New genomic data frameworks enabling global research.

●Agricultural and forensics applications expanding non-clinical revenue.

Challenges

●Data overload and limited functional variant understanding.

●Fragmented global regulatory landscape.

●Security vulnerabilities in genomic databases.

Top 10 Leading Companies in 2025

Illumina Inc.

●Product: NGS platforms and sequencing kits.

●Strength: Market leader with extensive genomic databases and collaborations (AGD initiative).

Thermo Fisher Scientific

●Product: PCR instruments, reagents, sequencing solutions.

●Strength: Global supply network and R&D dominance.

NVIDIA Corporation

●Product: AI computing platforms for genomic data.

●Strength: Industry-leading in AI-based drug discovery and healthcare partnerships.

Danaher Corporation

●Product: Genomic analysis instruments (Cytiva, Beckman Coulter brands).

●Strength: Broad biosciences portfolio and technological innovation.

Agilent Technologies

●Product: Genomic microarrays and bioinformatics software.

●Strength: Precision diagnostics and R&D collaborations.

Qiagen N.V.

●Product: Sample prep and PCR diagnostic kits.

●Strength: Expertise in molecular testing for infectious diseases.

Oxford Nanopore Technologies

●Product: Real-time sequencing devices (MinION, PromethION).

●Strength: Portable, rapid, and scalable sequencing solutions.

Bio-Rad Laboratories

●Product: Digital PCR systems and analytical tools.

●Strength: High-quality genomic testing tools for clinical diagnostics.

Eurofins Scientific

●Product: Genomic testing and laboratory services.

●Strength: Global laboratory presence and multi-industry service range.

F. Hoffmann-La Roche AG

●Product: Diagnostic kits and companion diagnostics.

●Strength: Extensive R&D collaborations (e.g., Janssen Biotech).

Latest Announcements

●10x Genomics (2025):

Announced new single-cell and spatial biology products, enhancing research scalability and data depth.

●NVIDIA (2025):

Expanded partnerships with Mayo Clinic, Illumina, and Arch Institute to drive AI transformation in genomics.

●India’s IBDC Launch (2025):

National genomic data set enabling domestic and global research independence.

Recent Developments

●Ultima Genomics (Feb 2025):

Launched UG 100 Solaris with new chemistry and software, increasing output by 50% and reducing costs by 20%.

●GeneDx Acquisition (Apr 2025):

Acquired Fabric Genomics to integrate AI in genomic interpretation.

●Fore Genomics & Inocras Partnership (Feb 2025):

Focused on enhancing pediatric genomic health screening.

●Singular Genomics Systems Acquisition (Feb 2025):

Acquired by Deerfield Management, emphasizing expansion in NGS and spatial multiomics.

●CareDx & Dovetail Genomics (Oct 2024):

Partnership for advanced HLA genotyping in transplant genomics.

●Valted Seq Launch (Apr 2025):

Introduced AI-driven Single Cell AI Discovery Engine for advanced biomarker discovery.

Segments Covered

A. By Technology

Polymerase Chain Reaction (PCR)

●Dominance: PCR accounted for the largest market share in 2024 and is projected to remain dominant through 2034.

●Key Role: Enables the amplification of specific DNA sequences, essential for molecular diagnostics and research.

Advancements:

●Introduction of digital PCR (dPCR) and real-time PCR (qPCR) enhances accuracy and quantitative capabilities.

●Widely used in disease detection, genotyping, gene expression analysis, and mutational studies.

●Advantages: High specificity, low cost, and scalability across clinical and research environments.

●Growth Factor: Increasing usage in infectious disease diagnostics and oncology research.

Sequencing

●Core Technology: Includes Next-Generation Sequencing (NGS) and Whole Genome Sequencing (WGS).

●Key Function: Allows high-throughput analysis of genetic material, identifying mutations, and mapping genomes.

●Market Impact: Falling sequencing costs and AI integration have accelerated adoption in clinical genomics.

●Applications: Oncology, prenatal testing, pharmacogenomics, and rare disease identification.

●Future Scope: Long-read sequencing and single-cell genomics driving precision medicine advancements.

Flow Cytometry

●Purpose: Enables cell sorting, biomarker detection, and genomic profiling at the cellular level.

●Use Case: Integrates with genomics to identify gene expression patterns in specific cell populations.

●Emerging Area: Increasing use in immunogenomics and oncology diagnostics.

Microarrays

●Function: Facilitate large-scale gene profiling and expression analysis.

●Application: SNP analysis, gene expression monitoring, and epigenetic studies.

●Significance: Offers cost-effective analysis of thousands of genes simultaneously.

●Trend: Declining use in standalone form, but gaining relevance when integrated with NGS for validation.

Others (CRISPR, Bioinformatics, & Genotyping Platforms)

●CRISPR Technology: Revolutionizing genome editing for therapeutic and research purposes.

●Bioinformatics Platforms: Provide analytical tools for sequencing data interpretation.

●Emerging Technologies: Include single-cell multi-omics and high-resolution melt (HRM) assays enhancing genomic data resolution.

B. By Deliverables

Products

●Definition: Includes consumables, instruments, and software used in genomics.

Subsegments:

●Instruments/Systems/Software: Sequencers, analyzers, PCR systems, microarray scanners.

●Consumables & Reagents: Kits, buffers, enzymes, probes used for experiments.

●Dominance: Accounted for the majority market share in 2024 due to continuous usage and replacement demand.

●Applications: Core research laboratories, diagnostic centers, and pharmaceutical R&D.

●Trend: Miniaturization of devices and software integration for real-time genomic data analysis.

Services

●Definition: Outsourced or contract-based genomic analysis and sequencing services.

Subsegments:

●NGS-based Services: Whole genome and exome sequencing for healthcare and research.

●Biomarker Translation Services: Identification of biomarkers for drug response and disease prediction.

●Computational Genomics: AI-powered bioinformatics pipelines for interpreting massive data.

●Core Genomics Services: RNA/DNA extraction, library preparation, and annotation services.

●Growth Trend: Increasing outsourcing by academic institutes and small biotech companies.

●Benefit: Reduces infrastructure and expertise costs while ensuring high-quality analysis.

C. By End-Use

●Pharmaceutical & Biotechnology Companies

●Largest Segment (2024): Accounted for the highest revenue share due to extensive R&D initiatives.

●Role: Utilize genomics for target identification, biomarker discovery, and drug development.

●Growth Factor: Increasing approvals of gene therapies (15 by the U.S. FDA as of 2024).

●Infrastructure: Advanced labs, collaborations with AI firms, and regulatory support for personalized drugs.

Hospitals & Clinics

●Growth Rate: Fastest-growing end-user segment in 2024.

●Role: Adoption of genomics in diagnostics, oncology, and chronic disease management.

Drivers:

●Rising chronic disease prevalence and hospitalizations.

●Integration of genomics into patient care for personalized treatment plans.

●Reimbursement support for genetic testing.

Academic & Government Institutes

●Function: Serve as innovation hubs for genomic data generation and research.

●Key Contributors: Initiatives like NHGRI (U.S.), All of Us Research Program, and Indian Genomic Data Center (IBDC).

●Objective: Strengthen public health genomics and train next-generation scientists.

Clinical Research Organizations (CROs)

●Role: Conduct genomic studies for pharmaceutical partners, enabling faster drug trials.

●Emerging Trend: Increasing collaboration with AI-driven bioinformatics firms for data interpretation.

Others (Diagnostic Centers, Forensic Labs, Agricultural Genomics)

●Forensics: DNA fingerprinting and criminal investigation.

●Agriculture: Crop and livestock genomics improving yield and resistance.

●Diagnostics: Early disease detection through rapid sequencing platforms.

D. By Region

1. North America

Market Leadership: Largest revenue contributor in 2024.

Key Drivers:

●Advanced genomic infrastructure and funding.

●Presence of major players like Illumina, Thermo Fisher, and NVIDIA.

●Precision Medicine Initiative and “All of Us” program promoting large-scale sequencing.

Supportive Ecosystem:

●NHGRI budget increased to USD 639 million (2025).

●Regulatory clarity under the U.S. FDA for genetic therapies.

Outlook:

●Continued dominance with robust R&D collaborations between academia and industry.

2. Europe

Major Countries: UK, Germany, France, Italy, and Spain.

Growth Factors:

●National genome projects and strong ethical frameworks for data protection.

●Expanding clinical genomics testing adoption.

Healthcare Integration:

●Precision medicine incorporated into public health systems.

Research Initiatives:

●Cross-border collaborations under Horizon Europe boosting genomics innovation.

3. Asia-Pacific

Fastest-Growing Region (CAGR > 18%)

Drivers:

●Government initiatives such as India’s PRIP and IBDC genomic data program.

●Rapid adoption of sequencing in Japan and China.

●Large patient pool with genetic disorder prevalence.

Highlights:

●In March 2025, Illumina & Nashville Biosciences completed 250,000 genome sequences for AGD, aiding Asian data mapping.

Future Potential:

●Expansion of genomics startups and biobanks in emerging nations.

4. Latin America

Key Markets: Brazil and Argentina.

Focus: Adoption of genomic diagnostics in cancer and infectious disease studies.

Barriers: Limited research funding and infrastructure compared to developed regions.

Outlook: Government health programs supporting genomic literacy and genetic testing awareness.

5. Middle East & Africa (MEA)

Leading Countries: UAE, Saudi Arabia, South Africa.

Initiatives: National genome projects like the Saudi Genome Program.

Growth Drivers:

●Increasing investment in healthcare digitization.

●Expansion of medical research collaborations with U.S. and European institutes.

Challenges: Data privacy policies and shortage of bioinformatics expertise.

Top 5 FAQs

-

What is the projected market size of the genomics market by 2034?

The market is expected to reach USD 171.41 billion by 2034 from USD 44.72 billion in 2025. -

Which region dominates the genomics market?

North America led in 2024, while Asia-Pacific is the fastest-growing region. -

Which technology leads the genomics market?

PCR technology held the largest share in 2024 and is expected to grow fastest. -

What are the key growth drivers?

Increasing prevalence of genetic disorders, AI integration, and demand for precision medicine. -

Who are the major players?

Illumina, Thermo Fisher, NVIDIA, Agilent, Qiagen, Bio-Rad, Eurofins, Danaher, Roche, and Oxford Nanopore.

Access our exclusive, data-rich dashboard dedicated to the biotechnology industry – built specifically for decision-makers, strategists, and industry leaders. The dashboard features comprehensive statistical data, segment-wise market breakdowns, regional performance shares, detailed company profiles, annual updates, and much more. From market sizing to competitive intelligence, this powerful tool is one-stop solution to your gateway.

Access the Dashboard: https://www.towardshealthcare.com/access-dashboard

Order your Genomics Market report now at: https://www.towardshealthcare.com/checkout/5065

Become a valued research partner with us – https://www.towardshealthcare.com/schedule-meeting

You can place an order or ask any questions, please feel free to contact us at sales@towardshealthcare.com

Powering Healthcare Leaders with Real-Time Insights: https://www.towardshealthcare.com/healthcare-intelligence-platform

Europe Region – +44 778 256 0738

North America Region – +1 8044 4193 44

APAC Region: +91 9356 9282 04

Visit Our Website:https://www.towardshealthcare.com

Find us on social platforms: LinkedIn | Twitter | Instagram | Medium | Pinterest