North America Dominates GLP-1 Drugs Market Adoption as Asia Pacific Ramps Up Growth in 2025

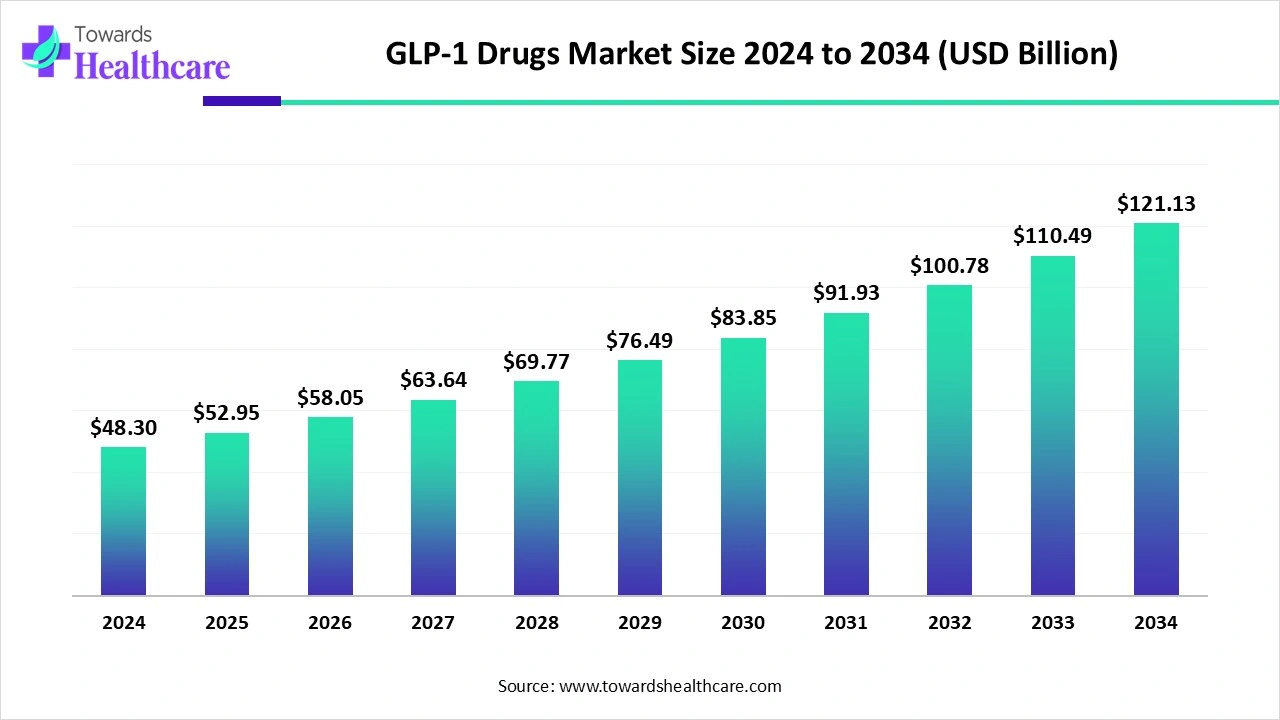

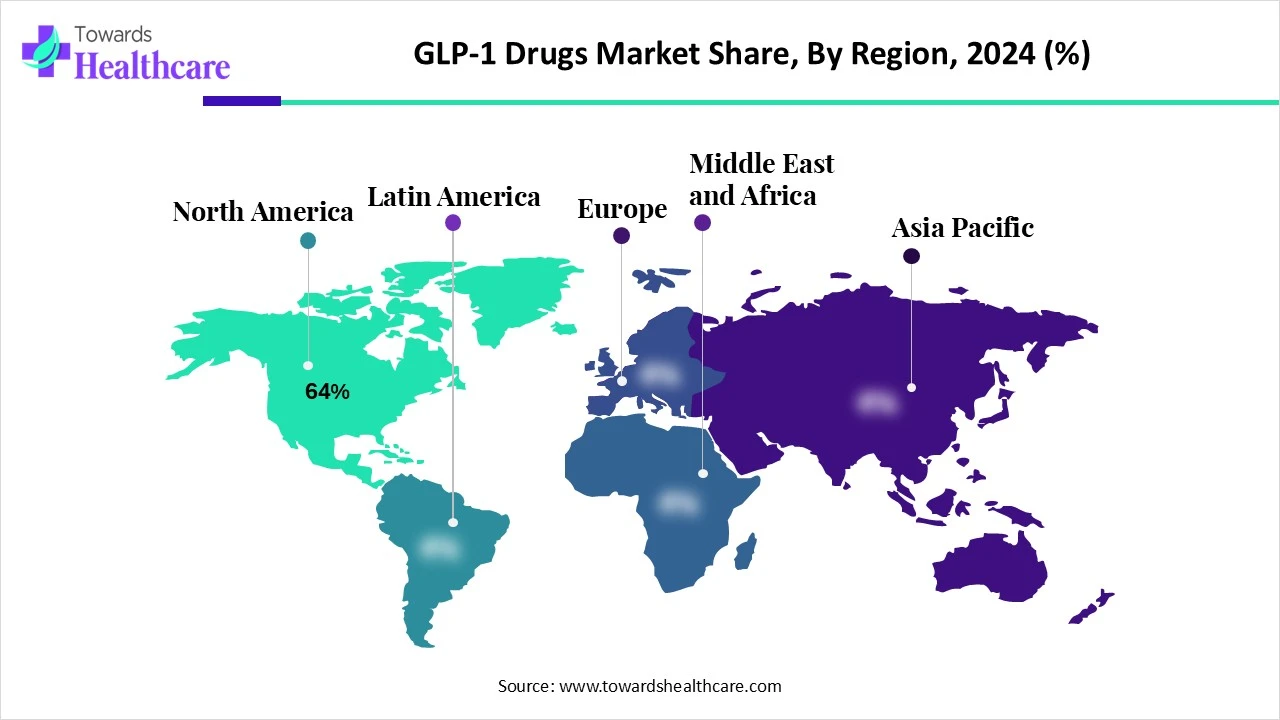

The global GLP-1 drugs market was US$48.3B in 2024, is projected to reach US$52.95B in 2025, and US$121.13B by 2034 at a 9.63% CAGR (2025-2034), propelled by diabetes/obesity demand, blockbuster brands (semaglutide, tirzepatide), AI-enabled R&D, and strong North America (64% share, 2024) leadership.

Download the free sample and get the complete insights and forecasts report on this market @ https://www.towardshealthcare.com/download-sample/5878

Table of Contents

ToggleMarket Size

➤2024 Baseline: US$48.3B global revenues; heavy skew to semaglutide (49% brand share) and injectables (83% route share).

➤2025 Step-up: US$52.95B, reflecting continued uptake of obesity indications, retail pharmacy dominance (51% end-user share) and early momentum in online/DTC channels.

➤2034 Outlook: US$121.13B, underpinned by broader access (retail + DTC), new orals, and next-gen dual agonists (e.g., tirzepatide fastest-growing).

➤CAGR Math: 9.63% (2025-2034) sustained by volume expansion, label growth beyond T2D, and improved adherence programs.

Revenue Mix Dynamics:

➤Brand concentration: Semaglutide family at 49% (2024); tirzepatide expected to outgrow peers.

➤Route mix: Injectables 83% (2024); orals are the fastest-growing through 2034.

➤Channel Shift: Retail pharmacies (51% in 2024) remain core; online/DTC fastest-growing on telehealth + weight-management programs.

➤Regional Weighting: North America 64% (2024); Asia Pacific fastest-growing 2025-2034 on lifestyle-disease burden and capacity build-out.

➤Price/Access Tension: High prices + variable obesity coverage temper upside in low/middle-income markets; government support and generics/biosimilars (where applicable) can unlock incremental volume.

➤Pipeline Pull-Through: Dual/tri-agonists, oral analogs, and long-acting formats expand eligible populations and dosing convenience into the 2030s.

➤Supply Chain Enablement: Tailored cold-chain solutions for GLP-1 stability reduce spoilage and support scale.

Market Trends

Obesity as Growth Flywheel: Regulatory approvals and clinical outcomes drive fastest growth in obesity/weight management usage, alongside T2D’s 58% share (2024).

Brand Leadership: Semaglutide dominates (49% 2024), with tirzepatide the fastest-growing due to dual GLP-1/GIP action.

Oral Acceleration: Rybelsus validates oral path; multiple oral GLP-1 analogs in development (e.g., Pfizer, Structure Therapeutics, TheracosBio).

Channel Evolution: Retail pharmacies (51% in 2024) anchor volume; online/DTC surges on telehealth, doorstep delivery, and privacy preferences.

Cold-Chain Innovation: Nordic Cold Chain Solutions (Jul 2025) launching tailored packaging for consistent temperature during transport.

AI-Driven Design: AI-designed GLP-1RA sequences (Jun 2025) showed comparable/superior receptor activation vs. semaglutide (in vitro).

China Commercial Scale-Up: Innovent Biologics x JD Health (Jul 2025) to build sales/supply chains before mazdutide launch.

Strong US Demand Signals: Mounjaro uptake (Jun 2025); quarter-of-launch: tirzepatide ~8% share, semaglutide 66% (Pharma Trac).

Care Ecosystem Apps: Shotsy highlighted as a 2025 GLP-1 tracker co-piloting dosing, symptoms, and nutrition syncing.

Expanding Indications: Exploration into CV risk, NASH, PCOS, and neurodegenerative conditions increases long-run TAM.

AI Impacts on the GLP-1 Drugs Market

De-novo Peptide Design: Generating GLP-1RA sequences with targeted receptor bias and stability (e.g., AI-designed sequences with strong activation).

Multitarget Optimization: In-silico screening for dual/tri-agonists (GLP-1/GIP/glucagon), balancing efficacy with tolerability.

Oral Bioavailability Models: Predicting permeability, protease resistance, and transporter interactions to accelerate oral analogs.

Dose Optimization & Titration: ML-driven titration schedules minimizing GI AEs while preserving efficacy.

Responder Prediction: Patient-level response models using EHRs/biometrics to tailor therapy selection and dosing.

Safety Signal Detection: NLP across pharmacovigilance reports to flag rare AEs and interaction risks earlier.

Manufacturing Yield Uplift: AI-assisted process control for peptide synthesis/formulation to improve yields and reduce COGS.

Cold-Chain Risk Forecasting: Predictive models to manage excursions and route logistics (aligned with bespoke cold-chain launches).

Digital Companion Tools: Apps like Shotsy translating injections into insights—adherence nudges, nutrition syncing, symptom prediction.

Label Expansion Analytics: Simulation platforms to prioritize new indications (CV, NASH, PCOS, neuro) and trial designs.

Regional Insights

North America — 64% Share (2024) | Global Anchor Market

✅ Core Demand Drivers

➤High chronic disease burden: Leading global rates of obesity and T2D.

➤Cultural adoption curve: GLP-1s normalized through DTC ads, celebrity endorsements, and social media.

Insurance leverage:

➤T2D coverage: Strong, standardized reimbursement.

➤Obesity coverage: Expanding but variable by employer programs and state mandates.

✅ Market Structure & Access

Retail pharmacies as default: CVS, Walgreens, Walmart dominate initiation and refills.

DTC/Telehealth Acceleration:

➤Hims & Hers, Found, Ro, WeightWatchers+Sequence, Eden, etc.

➤Growing privacy-first patient base.

➤Integrated coaching, nutrition sync, and subscription refills.

✅ Brand Dynamics

➤Semaglutide (Ozempic, Wegovy, Rybelsus): Strong public familiarity; >$13B US sales alone.

➤Tirzepatide (Mounjaro, Zepbound): Fastest adoption curve; dual-agonist buzz.

➤Trulicity/Liraglutide: Still prescribed for legacy diabetes cohorts.

✅ Outlook to 2034

➤Obesity treatment will shift from “elective” to “preventive care” category.

➤High retention due to cardiometabolic outcomes.

➤AI/telehealth + pharmacy partnerships will drive adherence.

Europe — Policy-Driven Growth & Clinical Deepening

✅ Access & Reimbursement Evolution

➤Reimbursement models expanding due to:

➤Rising obesity costs.

➤Pressure on cardiovascular and diabetes systems.

➤National health services adopting phased inclusion (France, Nordics, UK).

✅ Country-Level Dynamics

🇩🇪 Germany

➤Insurance-backed uptake of T2D drugs; obesity reimbursement in pilot phases.

➤Industry and universities studying GLP-1s for:

PCOS

➤Cardiovascular prevention

➤Metabolic syndrome

🇬🇧 United Kingdom

➤Government-backed R&D into neurodegenerative GLP-1 applications.

➤Early-stage PCOS clinical interest.

➤Pharma pipeline development underway (collaborations + clinical units).

✅ Market Trajectory

➤Demand growth tied to formal reimbursement rollouts.

➤Bottlenecks: Pricing negotiations + supply chain stabilization.

➤Strongest adoption expected in UK, Nordics, Germany, France.

Asia Pacific — Fastest-Growing (2025–2034)

✅ Demand Foundation

➤Rising obesity and diabetes due to urban diets and sedentary living.

➤Underpenetrated therapeutic markets.

➤Younger demographics entering risk categories earlier.

✅ Country Insight

🇨🇳 China

➤Manufacturing scale-up to reduce dependency on imports.

➤Partnership spotlight: Innovent + JD Health (Jul 2025)

➤Prepares commercialization infrastructure for mazdutide.

➤Focus on digital logistics and channel-building.

🇮🇳 India

➤Government incentives for affordability and access.

➤T2D detection programs boost diagnosis rates.

➤Private sector + online platforms expanding obesity treatment.

✅ Outlook

➤Local manufacturing + low-cost analogs will drive volume.

➤Fastest CAGR globally through 2034.

➤Digital-first distribution likely to bypass legacy bottlenecks.

Canada — Increasing Coverage & Generic Disruption

✅ Utilization Drivers

➤Clinical adoption for both T2D and obesity.

➤Strong hospital and endocrinology channel uptake.

➤Insurance programs expanding beyond diabetes.

✅ Commercial Shift

Hims & Hers (Jul 2025):

➤Targets Canada as launchpad for global generic semaglutide.

➤Focus on affordability + scalability.

✅ Market Outlook

➤Generic introduction will lower cost barriers materially.

➤Adherence expected to improve with subsidized obesity coverage.

Latin America & MEA — Emerging but Uneven Markets

✅ Latin America (LATAM)

➤Urban pockets dominate: Brazil, Mexico, Argentina metros.

Constraint: Affordability and fragmented reimbursement.

➤Telemedicine models slowly introducing weight-loss prescriptions.

➤Expansion tied to localized manufacturing and subsidies.

✅ Middle East & Africa (MEA)

Gulf States (UAE, Saudi, Kuwait):

➤Premium access, private clinics, wellness centers.

➤High medical tourism for obesity treatments.

Wider MEA:

➤Adoption gated by price and insurer inclusion.

➤Potential uptake via biosimilars and tiered pricing.

✅ Outlook

➤Tiered access models and local licensing agreements will shape penetration.

➤Sponsorship by insurers and employers crucial for scale.

Market Dynamics

Drivers

➤Rising T2D & Obesity: T2D 58% share in 2024; obesity now the fastest-growing indication segment.

➤Clinical & Brand Momentum: Semaglutide 49% brand share (2024); tirzepatide as fastest-growing dual agonist.

➤Channel Accessibility: Retail pharmacies 51% (2024); online/DTC accelerates adherence and privacy.

➤R&D Expansion: AI-enabled design; new indications (CV, NASH, PCOS, neuro).

Restraints

➤High Prices & Coverage Gaps: Especially for obesity indications and in LMICs; affects adherence and persistence.

➤Supply/Cold-Chain Complexity: Temperature sensitivity necessitates specialized logistics.

Opportunities

➤Oral GLP-1 Pipeline: Convenience boosts adherence; lowers infection risk; supports earlier initiation.

➤AI & Digital Health: Personalization, monitoring (e.g., Shotsy), and manufacturing efficiencies.

➤Partnerships & Local Scale: E-commerce alliances (e.g., Innovent x JD Health) and localized manufacturing to cut costs.

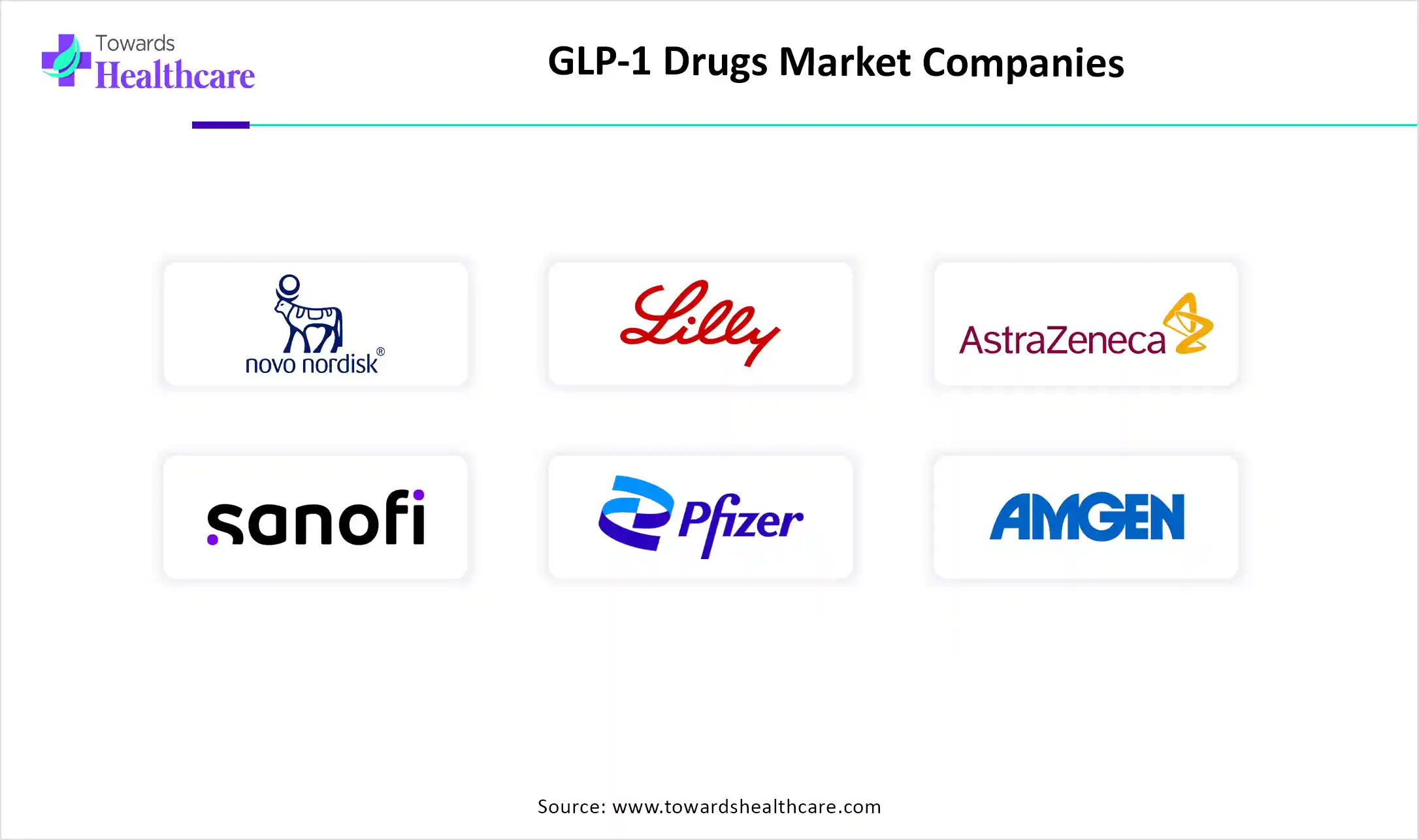

Top 10 Companies

Novo Nordisk — Ozempic, Wegovy, Rybelsus, Victoza

➤Overview: Category pioneer with dominant semaglutide franchise.

➤Strengths: Broad label, injectable + oral presence, global supply and brand equity.

Eli Lilly — Mounjaro (tirzepatide), Zepbound

➤Overview: Dual GLP-1/GIP leader with fastest growth.

➤Strengths: Superior weight/glucose efficacy signals; scaling production and adherence programs.

AstraZeneca — Bydureon (legacy)

➤Overview: Earlier GLP-1 presence via exenatide ER.

➤Strengths: Experience in metabolic portfolios; combination therapy insights.

Sanofi — Efpeglenatide (in development)

➤Overview: Pipeline re-engagement in incretins.

➤Strengths: Global development, market access capabilities.

Pfizer — Oral GLP-1 analogs (pipeline)

➤Overview: Focus on oral delivery innovations.

➤Strengths: Oral formulation know-how; large-scale trials and commercialization.

Amgen — AMG133 (long-acting GLP-1/GIP)

➤Overview: Next-gen dual agonist approach.

➤Strengths: Long-acting engineering; obesity focus.

Structure Therapeutics — Oral GLP-1 analogs (early)

➤Overview: Small-molecule/peptidomimetic path to oral incretins.

➤Strengths: Oral convenience vector; nimble development.

Zealand Pharma — GLP-1/glucagon duals

➤Overview: Peptide specialist advancing multi-agonists.

➤Strengths: Design expertise and partnering track record.

Boehringer Ingelheim — Obesity-focused GLP-1 pipeline

➤Overview: Building presence in obesity therapeutics.

➤Strengths: CV-metabolic integration; long-term R&D funding.

Innovent Biologics — Biosimilars; mazdutide (commercial prep)

➤Overview: China-based scale player leveraging e-commerce.

➤Strengths: JD Health partnership for channel/supply; local manufacturing.

Latest Announcements

Innovent Biologics x JD Health (Jul 2025): Strategic partnership to build online distribution, sales channels, and supply chains prior to mazdutide launch—aimed at rapid market penetration and nationwide reach in China.

Hengrui Pharma x Kailera Therapeutics (Jul 2025): Collaboration drug moving toward clinical trials, with reported ≥20% weight loss in 44.4% and ≥5% weight loss in 88% of participants—positioning as a competitive next-gen contender.

Hims & Hers (Jul 2025): CEO highlights Canada as a major opportunity; strategy to merge personalized care + affordability and introduce generic semaglutide accessibility at scale.

Mounjaro Uptick (Jun 2025): Pharma Trac notes strong onboarding/adherence; tirzepatide ~8% market share in launch quarter vs. semaglutide 66%.

Recent Developments

Cold-Chain Packaging (Jul 2025): Nordic Cold Chain Solutions launches tailored GLP-1 packaging to maintain consistent temperatures, protect therapeutic integrity, and support regulatory compliance during transport.

AI-Designed GLP-1RAs (Jun 2025): ImmunoPrecise Antibodies reports in vitro GLP-1RA sequences with comparable or superior receptor activation to semaglutide—validating AI as an engine for meaningful molecular innovation.

Segments Covered

By Indication

✔ Type 2 Diabetes (T2D) – 58% market share (2024)

➤Primary Revenue Anchor: Remains the largest commercial use-case due to decades of clinical validation.

➤Reimbursement Advantage: Coverage by major insurers and public health systems drives volume.

➤Chronic Treatment Lifespan: Prescriptions extend over years, ensuring recurring revenue.

➤Aging Population Impact: Rising geriatric demographic fuels sustained demand.

➤Combination Therapies: Co-prescription with SGLT-2 inhibitors and metformin increases uptake.

✔ Obesity & Weight Management – Fastest-growing segment

➤High Consumer Pull: Driven by aesthetics, wellness brands, and DTC programs.

➤Celebrity & Social Media Influence: “Ozempic effect” drives mainstream adoption.

➤Self-pay Markets: Especially strong in US & Gulf regions lacking obesity drug reimbursement.

➤Telehealth Platforms: Companies like Hims & Hers, Ro, Found, Sequence fuel access.

✔ Cardiovascular Risk Reduction (Secondary Prevention)

➤Expanded Label Strategy: Piggybacks on cardiometabolic benefits of GLP-1s.

➤Heart Disease Burden: GLP-1s reduce stroke, heart attack risk, and mortality.

➤Clinical Outcome Trials (CVOTs): Positive data supports broader prescribing.

✔ Emerging Indications (Future TAM Expansion)

➤PCOS: Addresses insulin resistance & metabolic dysfunction.

➤NASH/NAFLD: Liver fat reduction trials show promising endpoints.

➤Neurodegenerative Diseases (Alzheimer’s, Parkinson’s):

➤Explored for neuroinflammation and metabolic-brain axis.

➤Attracts biotech and AI-based peptide discovery companies.

➤Reproductive Age Women & Young Adults: Requires safety adaptation and dosimetrics.

By Drug Type / Brand

✔ Semaglutide (Ozempic, Wegovy, Rybelsus) – 49% share (2024)

➤Blockbuster Dominance: Leads both injectable and oral GLP-1 markets.

➤Route Flexibility: First-in-class oral and injection SKUs drive loyalty.

➤Clinical Trust: Proven effect on HbA1c, BMI, and cardiovascular risk.

➤Scalability: Strong manufacturing footprint (Novo Nordisk).

✔ Tirzepatide (Mounjaro, Zepbound) – Fastest-growing

➤Dual Agonist Platform: GLP-1 + GIP synergy enhances weight loss and glycemic control.

➤Pipeline Expansion: Trials underway for obesity, PCOS, and NAFLD.

➤Competitive Pricing Strategy: Targeting payer negotiations and DTC models.

✔ Other Key Molecules (Sustains Market Baseline)

➤Liraglutide – Earlier gen but used in pediatrics and cardiac profiles.

➤Dulaglutide (Trulicity) – Strong adherence and injector pen optimization.

➤Exenatide / Albiglutide – Legacy use, biosimilar opportunities.

By Route of Administration

✔ Injectable – 83% market share (2024)

➤Weekly / Biweekly Dosage: Minimizes patient burden.

➤Long-acting Formulations: Reduced clinic visits and wastage.

➤Depot Technologies: Microneedle patches and biodegradable carriers in development.

➤Specialty Distribution: Managed via retail, clinics, and wellness centers.

✔ Oral – Fastest-growing

➤Improved Compliance: Attracts needle-averse populations.

➤Rybelsus as Market Proof: Breaks the stigma of peptide-only injectables.

➤Pipeline Promise: AI-designed peptides + absorption boosters in Phase I/II.

By End User

✔ Retail Pharmacies – 51% (2024)

➤Advisor Role: Patient counseling on dosing, side effects, and refills.

➤Chronic Supply Chain: Supports automatic refill subscriptions.

➤Brand Loyalty Centers: Often tied to insurer and manufacturer programs.

✔ Hospitals, Specialty Clinics & Physician Offices

➤Therapy Initiation: First-dose supervision and eligibility checks.

➤Diagnostic Bundling: Linked to glucose testing and cardiology visits.

➤Programs for Comorbidity Management: Supports complex obesity and diabetic profiles.

✔ Weight Loss & Wellness Clinics

➤Lifestyle + Drug Protocols: Integrated coaching, nutrition, and diagnostics.

➤Cash-Pay Growth: Particularly in urban metros and Gulf regions.

✔ Online Pharmacies / Direct-to-Consumer (DTC) – Fastest-growing

➤Telehealth Momentum: Digital Rx and virtual consults accelerate adoption.

➤Logistics Integration: Home delivery, auto-refill, and temperature-controlled shipping.

➤Privacy-First Access: Popular among self-paying obesity users.

➤Subscription Business Models: Enhances retention and dosage adherence.

Top 5 FAQs

-

What is the market size and growth rate?

US$48.3B (2024) → US$52.95B (2025) → US$121.13B (2034); 9.63% CAGR (2025–2034). -

Which region leads today?

North America with 64% share in 2024; Asia Pacific is fastest-growing through 2034. -

Which brands and routes dominate?

Semaglutide family holds 49% (2024); injectables are 83% (2024), while oral options grow fastest. -

Which channels matter most?

Retail pharmacies (51% in 2024) lead distribution; online/DTC channels are the fastest-growing. -

What’s driving the market?

Rising T2D (58% share in 2024) and obesity demand, AI-enabled R&D, partnerships (e.g., Innovent-JD Health), logistics innovation, and strong brand performance (e.g., semaglutide leadership; tirzepatide rapid uptake).

Access our exclusive, data-rich dashboard dedicated to the therapeutics area sector – built specifically for decision-makers, strategists, and industry leaders. The dashboard features comprehensive statistical data, segment-wise market breakdowns, regional performance shares, detailed company profiles, annual updates, and much more. From market sizing to competitive intelligence, this powerful tool is one-stop solution to your gateway.

Access the Dashboard: https://www.towardshealthcare.com/access-dashboard

Immediate Delivery Available | Buy This Premium Research @ https://www.towardshealthcare.com/price/5878

Become a valued research partner with us – https://www.towardshealthcare.com/schedule-meeting

You can place an order or ask any questions, please feel free to contact us at sales@towardshealthcare.com

Powering Healthcare Leaders with Real-Time Insights: https://www.towardshealthcare.com/healthcare-intelligence-platform

Europe Region – +44 778 256 0738

North America Region – +1 8044 4193 44

APAC Region: +91 9356 9282 04

Web: https://www.towardshealthcare.com

Find us on social platforms: LinkedIn | Twitter | Instagram | Medium | Pinterest