Why the Gynecological Devices Market Is Suddenly Everyone’s Focus

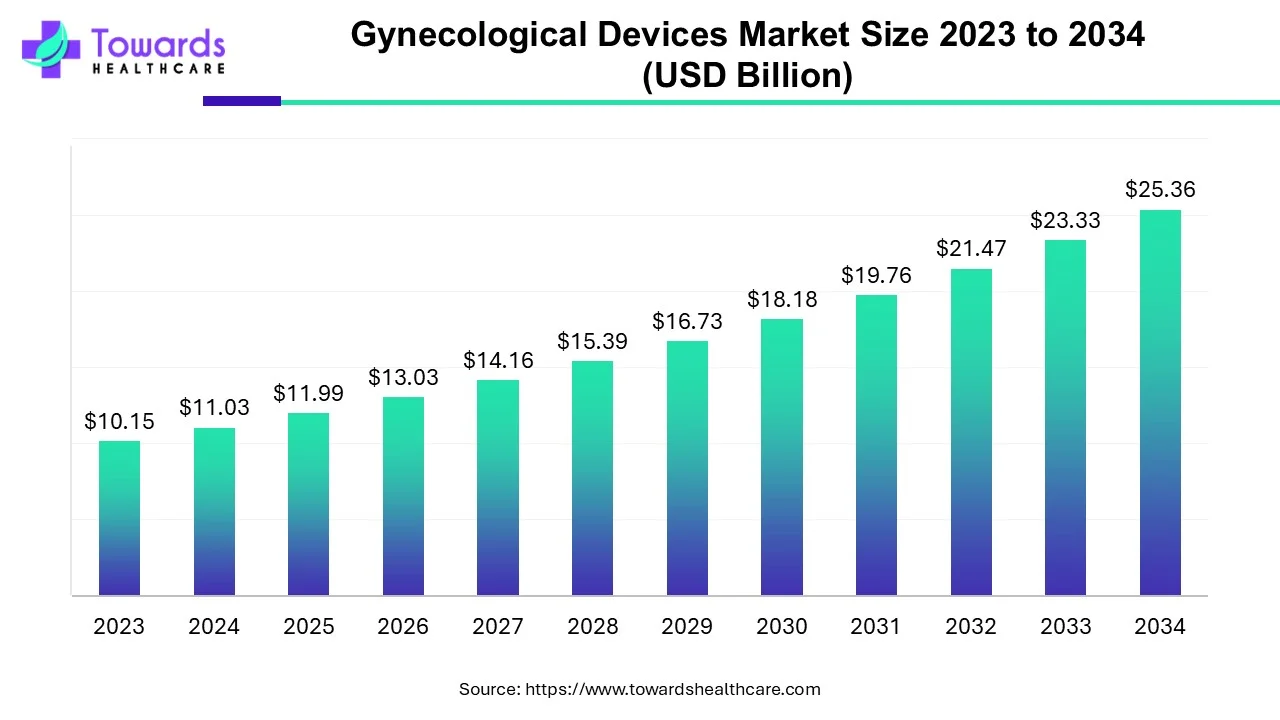

The gynecological devices market has entered a defining decade. After years of steady but understated progress, women’s health technologies are now commanding attention from clinicians, policymakers, manufacturers, and investors alike. With the global gynecological devices market valued at USD 11.03 billion in 2024 and projected to reach approximately USD 25.36 billion by 2034, this sector is no longer a niche corner of medical devices. It is becoming a central pillar of modern healthcare systems worldwide, growing at a robust compound annual growth rate of 8.68 percent between 2025 and 2034.

Download Free Sample Now and Get the Complete Report Easily at: https://www.towardshealthcare.com/download-sample/5496

What makes this market especially compelling is not just its size or growth trajectory, but the depth of transformation underway. Gynecological care is moving beyond basic instruments and conventional procedures toward precision-driven diagnostics, minimally invasive surgeries, and technology-enabled patient monitoring. This evolution reflects a broader realization that women’s health has long been underserved by innovation, and that closing this gap is both a medical necessity and a societal imperative.

From Routine Tools to Critical Care Enablers

Gynecological devices have traditionally been associated with routine examinations, childbirth assistance, and basic surgical procedures. Instruments such as vaginal speculums, forceps, retractors, and cervical dilators formed the backbone of gynecological practice for decades. While these tools remain indispensable, the scope of gynecological devices has expanded dramatically.

Today’s market encompasses advanced endoscopic systems, robotic-assisted surgical platforms, sophisticated imaging technologies, fluid management systems, and a wide array of contraceptive and sterilization devices. These technologies play a crucial role not only in treating gynecological disorders but also in early diagnosis, disease prevention, fertility preservation, and long-term reproductive health management. The shift from reactive treatment to proactive and preventive care defines the current phase of market evolution.

This transformation has been driven by rising clinical demand. Conditions such as endometriosis, uterine fibroids, polycystic ovarian syndrome, menstrual disorders, cervical cancer, and urinary incontinence affect millions of women globally. These conditions often require repeated diagnostic evaluations, long-term management, and, in many cases, surgical intervention. As awareness increases and social stigma declines, more women are seeking timely medical attention, directly increasing the utilization of gynecological devices across healthcare settings.

The Numbers Tell a Story of Momentum

Market growth data underscores this accelerating momentum. From USD 11.99 billion in 2025, the gynecological devices market is on course to more than double by 2034. North America accounted for 39 percent of global market share in 2024, reflecting its advanced healthcare infrastructure, high adoption of minimally invasive procedures, and strong presence of leading medical device manufacturers.

However, the most dynamic growth is unfolding in Asia-Pacific. This region is expected to register the fastest expansion over the coming years, fueled by demographic shifts, rising healthcare expenditure, increasing awareness of women’s health, and proactive government initiatives. Countries such as China and India are rapidly scaling maternal health facilities, promoting domestic medical device manufacturing, and expanding access to advanced gynecological care across urban and semi-urban areas.

Europe continues to represent a mature but steadily advancing market, driven by research and development investments, favorable healthcare policies, and a strong emphasis on quality and safety standards. Meanwhile, Latin America and the Middle East and Africa are gradually emerging as important growth frontiers, supported by improving healthcare access and rising investments in women’s health services.

Surgical Innovation Reshapes Clinical Practice

Among product categories, surgical devices dominate the gynecological devices market and are expected to maintain their leadership position throughout the forecast period. This dominance reflects the increasing volume of gynecological surgeries worldwide, particularly those addressing chronic conditions such as fibroids, endometriosis, and abnormal uterine bleeding.

The demand for minimally invasive procedures has fundamentally reshaped surgical gynecology. Laparoscopic and hysteroscopic techniques have reduced hospital stays, minimized postoperative complications, and improved patient recovery times. The integration of robotic-assisted surgical systems has further enhanced precision, dexterity, and visualization, allowing surgeons to perform complex procedures with greater confidence and consistency.

Technological advancements have also expanded the scope of endometrial ablation, sterilization procedures, and fertility-preserving interventions. These innovations align with changing patient expectations, as women increasingly seek treatments that are effective, safe, and minimally disruptive to their daily lives.

Imaging Technologies Redefine Early Diagnosis

Diagnostic imaging systems represent one of the fastest-growing segments within the gynecological devices market. Early and accurate diagnosis is critical in managing gynecological disorders, many of which present with subtle or overlapping symptoms. Ultrasound remains the cornerstone of gynecological imaging, but advanced modalities such as MRI, CT scans, PET/CT, and sonohysterography are playing an expanding role.

Artificial intelligence and machine learning are now enhancing imaging accuracy by assisting clinicians in image interpretation, anomaly detection, and risk stratification. These technologies reduce diagnostic variability, shorten examination times, and support earlier intervention. As governments and healthcare organizations emphasize early detection of gynecological cancers and chronic reproductive disorders, the adoption of advanced imaging systems is expected to accelerate further.

Hospitals Lead, but ASCs Change the Game

Hospitals and clinics continue to account for the largest share of gynecological device utilization. Their dominance stems from comprehensive infrastructure, multidisciplinary expertise, and access to advanced surgical and diagnostic technologies. Hospitals also benefit from favorable reimbursement frameworks that improve patient access to specialized gynecological care.

At the same time, ambulatory surgical centers are rapidly emerging as the fastest-growing end-use segment. ASCs offer high-quality outpatient procedures without the need for overnight hospitalization, making them attractive to both patients and payers. Procedures such as tubal ligation, endometrial ablation, cervical biopsies, and minimally invasive surgeries are increasingly performed in these settings.

The growth of ASCs reflects broader healthcare system trends toward decentralization, cost efficiency, and patient convenience. As technology enables safer and faster outpatient procedures, ASCs are expected to play an increasingly prominent role in gynecological care delivery.

Artificial Intelligence Moves from Promise to Practice

Artificial intelligence is no longer a theoretical concept in the gynecological devices market. It is actively reshaping product development, clinical workflows, and manufacturing processes. AI-powered imaging systems assist clinicians in detecting abnormalities with higher accuracy, while machine learning algorithms analyze large datasets to identify patterns that inform diagnosis and treatment planning.

Robotic systems equipped with AI capabilities are enhancing surgical outcomes by improving precision and reducing human error. Wearable devices and Internet of Things-enabled platforms allow real-time monitoring of maternal and reproductive health parameters, reducing the need for frequent in-person visits and enabling continuous care.

On the manufacturing side, AI-driven predictive analytics improve quality control, reduce production errors, and enhance reproducibility. These efficiencies not only lower costs but also support compliance with increasingly stringent regulatory requirements.

Policy, Investment, and Public Health Alignment

Government initiatives have played a crucial role in accelerating market growth. In the United States, sustained support for gynecologic research and workforce development has strengthened clinical capacity and innovation. Canada’s targeted investments in women’s reproductive health services are expanding access to menopause care and specialized resources.

In India, large-scale public health programs focused on maternal care and reproductive health have significantly increased the utilization of gynecological services. The government’s commitment to building a national registry for endometriosis and investing heavily in medical device manufacturing signals a long-term strategy to strengthen women’s health infrastructure.

China’s emphasis on expanding maternal health facilities and promoting domestic medical device production has improved accessibility while attracting global manufacturers. European governments, particularly in Germany, continue to fund research, training, and technology upgrades to maintain high standards of gynecological care.

Regulatory Complexity Remains a Persistent Challenge

Despite strong growth prospects, the gynecological devices market faces notable challenges. Regulatory frameworks governing medical devices are becoming increasingly stringent, with rigorous safety, efficacy, and quality requirements. While these standards are essential for patient safety, they often result in lengthy approval timelines and high compliance costs.

Manufacturers operating across multiple regions must navigate a complex landscape of evolving regulations, which can slow innovation and market entry. Smaller companies and startups may find these barriers particularly challenging, potentially limiting competition and diversity within the market.

Sustainability Emerges as a Strategic Opportunity

Sustainability is emerging as a defining opportunity for the future of the gynecological devices market. Environmental concerns, combined with supportive government policies, are encouraging manufacturers to adopt eco-friendly materials, energy-efficient production processes, and waste-reduction strategies.

Single-use devices designed with sustainability in mind are gaining acceptance, as they reduce reprocessing costs and minimize infection risks. Sustainable manufacturing not only aligns with regulatory expectations but also resonates with healthcare providers seeking to reduce their environmental footprint without compromising patient care.

A Market Shaped by Experience and Expectation

After more than a decade of observing the gynecological devices market, one pattern is clear: progress accelerates when clinical need, technological capability, and policy alignment converge. Today, all three forces are moving in the same direction. Women are demanding better care. Clinicians are adopting advanced tools. Governments and manufacturers are investing with renewed urgency.

This market is no longer defined solely by instruments and equipment. It reflects a broader shift toward recognizing women’s health as a cornerstone of public health and economic productivity. The coming years will likely bring deeper integration of digital technologies, expanded access in emerging regions, and a stronger emphasis on patient-centered design.

As the gynecological devices market moves toward 2034, its growth will not simply be measured in dollars. It will be measured in earlier diagnoses, safer procedures, improved quality of life, and a healthcare system that finally gives women’s health the innovation focus it has long deserved.

Access our exclusive, data-rich dashboard dedicated to the medical devices sector – built specifically for decision-makers, strategists, and industry leaders. The dashboard features comprehensive statistical data, segment-wise market breakdowns, regional performance shares, detailed company profiles, annual updates, and much more. From market sizing to competitive intelligence, this powerful tool is one-stop solution to your gateway.

Access the Dashboard: https://www.towardshealthcare.com/access-dashboard

Checkout Gynecological Devices Market Report Now at: https://www.towardshealthcare.com/checkout/5496

Become a valued research partner with us - https://www.towardshealthcare.com/schedule-meeting

You can place an order or ask any questions, please feel free to contact us at sales@towardshealthcare.com

Powering Healthcare Leaders with Real-Time Insights: https://www.towardshealthcare.com/healthcare-intelligence-platform

Europe Region – +44 778 256 0738

North America Region – +1 8044 4193 44

APAC Region: +91 9356 9282 04

Visit Our Website: https://www.towardshealthcare.com

Find us on social platforms: LinkedIn | Twitter | Instagram | Medium | Pinterest

Table of Contents

Toggle