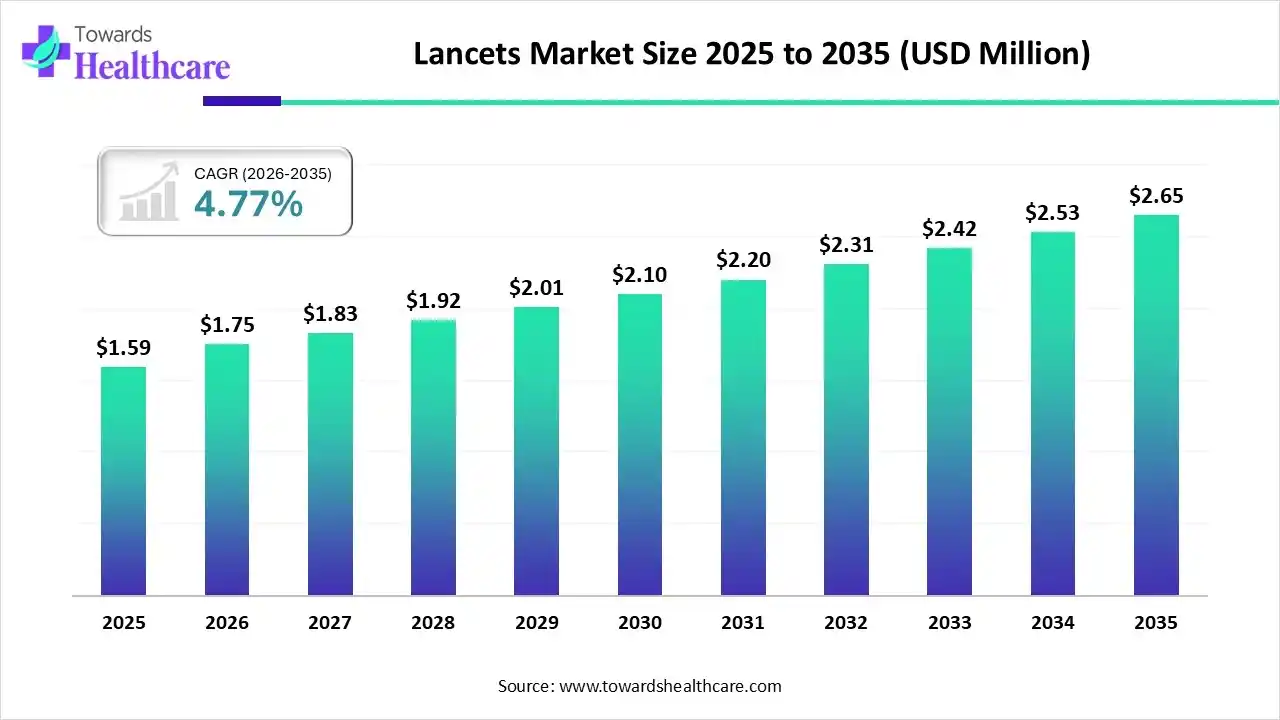

The global lancets market is projected to rise from USD 1.59 billion in 2025 to USD 2.65 billion by 2035, reflecting a steady CAGR of 4.77%, propelled by growing diabetes prevalence, aging populations, rising demand for at‑home blood testing, and innovations toward safer, pain‑reduced lancing.

Download Free Sample of Lancets Market Now and Get the Complete Report Easily at: https://www.towardshealthcare.com/download-sample/5251

Market Size

Base Market (2025): USD 1.59 billion.

Forecast Market (2035): USD 2.65 billion.

Overall Growth Rate: CAGR of 4.77% between 2026 and 2035.

Regional Importance:

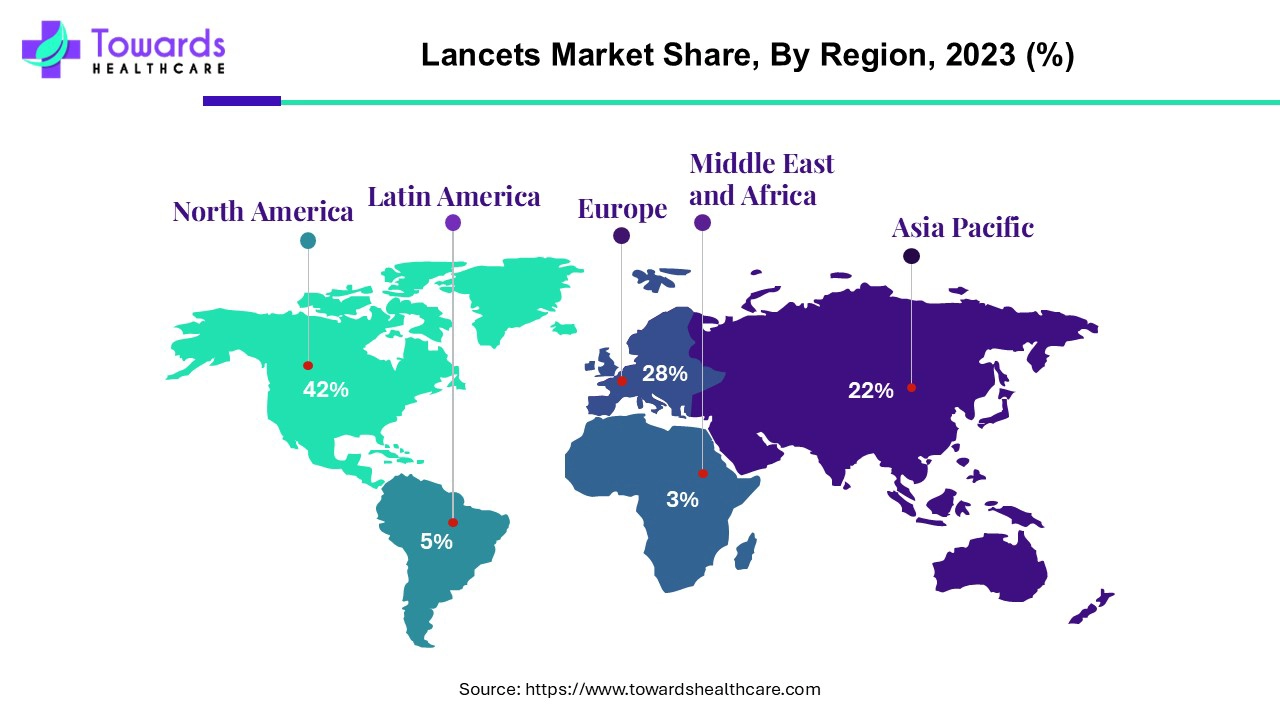

North America holds the largest share globally (≈ 42% in 2024), due to advanced healthcare infrastructure and high chronic disease burden.

Asia‑Pacific is the fastest-growing region over the forecast period.

India shows especially strong growth potential: from ~USD 120 million (2024) to ~USD 414.35 million by 2034 — implying a high regional CAGR (~13.2%).

Segment Strength:

By type, “Standard lancets” remain the volume leaders.

By needle gauge, 23G–33G sizes dominate in volume (versatile for general blood tests).

By end‑user facility type, hospitals currently lead usage.

Growth Potential Zones: Growing adoption of safety and advanced lancing technologies, especially in emerging regions (Asia-Pacific, India), indicates significant upside beyond base-case projections.

Market Trends

Rising Diabetes and Chronic Disease Prevalence: As global diabetes cases (type I & II) and other chronic conditions (like cholesterol, hemoglobin disorders) increase, demand for regular blood sampling hence lancets climbs sharply.

Shift toward At-Home Testing: There’s growing demand for home blood tests (diabetes monitoring, cholesterol, HbA1c, etc.), driving sales of disposable lancets, at-home lancing devices, and homecare kits.

Demand for Safety and Pain-Free Devices: Patients, especially elderly and pediatric, prefer lancets designed for minimal pain (e.g., retractable safety lancets, nano‑lancets, adjustable-depth lancets).

Regulatory Approvals & Certifications: New products obtaining CE mark or regulatory clearances (e.g., for over-the-counter (OTC) and home-use blood sampling) are accelerating market acceptance.

Mergers & Acquisitions Boosting Capacity: Consolidation (e.g., acquisitions by larger players) helps scale production, improve distribution networks, and reduce per-unit cost — making lancets more accessible globally.

Technological Innovation — Nano‑Lancets & Smart Devices: Adoption of nanotechnology in lancets for finer needles and less pain; future direction toward integrating sensors and smart blood analyzers.

Rise in Safety Concerns & Infection Control: Growing awareness of needlestick injuries, bloodborne infections (Hepatitis, HIV) encourages safety-lancets over conventional ones.

Cost-Effectiveness Pressure in Developing Regions: In price-sensitive emerging markets, standard lancets dominate because of lower cost, balancing growth vs advanced-lancet adoption.

Growth of Ambulatory Surgical Centers (ASCs) and Homecare Diagnostics: As more diagnostics shift from hospitals to ASCs and homecare, demand patterns evolve — pushing for portable, safe, user-friendly lancets.

Public Health & Preventive Care Emphasis: Increased preventive health check-ups and chronic‑disease screening programs worldwide fuel routine blood testing, supporting steady growth in lancet demand.

AI’s Potential Impact / Role in the Lancets Market

Demand Forecasting & Inventory Optimization: AI-driven analytics can model disease prevalence, demographic shifts, and healthcare trends to better forecast regional lancet demand, reducing shortages or overproduction.

Smart Lancing Devices with Adaptive Sampling: AI-enabled lancing devices could adjust needle depth, pressure, and timing based on real-time feedback (skin thickness, blood flow), minimizing pain and improving sample quality.

Integration with Telehealth & Remote Diagnostics: AI platforms can analyse data from lancet-based blood samplings (e.g., glucose, HbA1c, lipid profile) remotely — enabling chronic disease monitoring without clinic visits.

Quality Control in Manufacturing: AI-powered vision systems or sensors can ensure sterility, needle integrity, and compliance with safety standards during mass production of lancets.

Predictive Patient Compliance & Usage Patterns: AI can analyze patient history (age, diabetes severity, frequency of testing) to recommend optimal lancet type (gauge, safety vs standard), reducing waste and improving compliance.

Personalized Lancet Recommendations: AI tools (e.g., mobile apps) can suggest lancet size/type based on user demographics (skin thickness, age, sensitivity), reducing trial-and-error and enhancing comfort.

Smart Waste Management: AI-enabled tracking of used lancets to ensure safe disposal, avoid re-use, and monitor compliance — reducing risk of infection and needlestick injuries.

Market Expansion Analytics: AI-driven market intelligence can highlight emerging high-growth regions (e.g., parts of Asia, Africa) by analyzing demographic, disease, and healthcare infrastructure data — guiding companies where to invest.

Integration into Wearable or Continuous Monitoring Ecosystems: AI could help merge lancet sampling data with continuous glucose monitors or other wearable health devices — providing holistic, real-time health insights.

R&D Acceleration & Lancet Innovation: AI-driven simulation and design can help develop new lancet types (e.g., nano‑lancets, painless retractable, sensor‑embedded), optimizing safety, patient comfort, and manufacturing efficiency before physical prototypes.

Regional Insights

North America:

Market leadership (≈ 42%) — due to high chronic disease burden and well-established healthcare infrastructure.

Advanced homecare & diagnostics adoption — high demand for at-home blood testing (diabetes management, cholesterol, etc.).

Favorable regulatory environment & insurance coverage — supports frequent blood testing and lancet usage.

Asia-Pacific:

Fastest growth trajectory — driven by aging populations, rising chronic disease rates, improved healthcare access.

Emerging markets (e.g. China, India) — large diabetic populations and growing awareness of regular health monitoring.

Cost sensitivity driving mixed adoption — while developed urban areas may adopt safety/nano lancets, rural or low-income regions may continue using standard, lower-cost lancets.

India (Subregion Insight):

From ~USD 120 million (2024) to projected ~USD 414.35 million (2034).

High growth due to rising diabetes prevalence (millions of affected adults), increasing health awareness, and expansion of homecare diagnostics.

Potential for leapfrogging to safety / advanced lancets as affordability and awareness improve.

Europe:

Moderate growth driven by chronic disease prevalence, aging population, and governmental support for preventive screening.

Adoption of improved lancets due to higher safety and regulatory standards.

Other Regions (Latin America, MEA):

Emerging demand as healthcare infrastructure improves; growth may be uneven due to cost and access constraints.

Opportunity for low-cost standard lancets to dominate initially, with gradual shift toward safety/advanced types if health awareness and affordability increase.

Market Dynamics

Key Drivers:

Rising global burden of diabetes and chronic diseases → regular blood sampling demand.

Growth in at-home diagnostics and self-monitoring.

Innovation in lancet technology: safety, pain-free, nano‑lancets.

Aging populations worldwide — more frequent diagnostics, chronic disease monitoring.

Healthcare infrastructure expansion and regulatory acceptance of home-use lancets.

Restraints / Challenges:

Risk of needlestick injuries and associated bloodborne infections (Hepatitis, HIV).

Pain and discomfort associated with traditional lancets — may discourage frequent use.

Cost constraints, especially in low-income or developing regions — limiting adoption of advanced lancets.

Regulatory and compliance barriers for safety/advanced lancets and disposal standards across regions.

Opportunities:

Rising demand for safety-lancets and pain-free nano‑lancets especially in homecare and pediatric/geriatric use.

Growth of ambulatory surgical centers (ASCs) and home-testing kits expanding user base beyond hospitals.

Mergers, acquisitions, and collaborations enabling improved production, distribution, and innovation.

Integration with telemedicine and smart health ecosystems — broadening market beyond diabetes to general chronic disease monitoring and preventive health.

Top 10 Lancet Companies

Abbott Laboratories

Products: Standard and safety lancets, lancet devices, and integrated glucose-monitoring systems.

Strengths:

Global distribution network ensures availability across hospitals, clinics, and homecare markets.

Robust R&D enables development of new lancet designs compatible with their glucose-monitoring devices.

Strong brand trust and long-standing presence in the healthcare sector, making it a preferred choice in clinical settings.

Integration of lancets with monitoring devices ensures seamless blood sampling and data management.

BioCare Corporation

Products: Safety lancets, retractable lancets, and pain-reduction-focused designs.

Strengths:

Market leader in safety-oriented lancets, minimizing risk of accidental needle sticks.

Focus on patient comfort and reducing pain, targeting pediatric and geriatric populations.

Continuous innovation in safety-first devices positions BioCare as a go-to for high-risk settings.

Bioland Technology Ltd.

Products: Standard lancets, advanced lancets for home and clinical use.

Strengths:

Large-scale manufacturing capacity, particularly in Asia, supporting both domestic and export markets.

Competitive pricing allows broad market reach, especially in emerging markets.

Ability to produce high volumes ensures consistent supply for hospitals, clinics, and at-home testing.

Braun SE

Products: Hospital-grade lancing and blood-sampling devices.

Strengths:

Long-standing reputation in precision medical devices; trusted in hospital environments.

Devices designed for reliability and repeated clinical use, adhering to strict hospital standards.

Focus on durability and accuracy makes Braun a preferred brand for medical professionals.

Drawbridge Health

Products: OTC and at-home lancets, including advanced NanoDrop lancet devices.

Strengths:

Innovator in consumer-friendly home-use lancets, enabling at-home blood testing.

Early regulatory approvals for home-use devices expand market access beyond hospitals.

Focus on ease-of-use and pain reduction aligns with growing at-home testing trends.

ForaCare

Products: Homecare lancets and complete blood-testing kits.

Strengths:

Integrates lancets with telemedicine and remote monitoring solutions for chronic diseases.

Emphasis on user-friendly kits ensures accessibility for non-professional users.

Expertise in chronic disease monitoring (diabetes, cholesterol) drives recurring demand.

Genteel

Products: Pain-free lancing systems, comfort-oriented lancets.

Strengths:

Focus on reducing needle phobia, particularly for children and the elderly.

Unique device designs hide needles and use gentle activation, improving patient compliance.

Strong positioning in the “comfort-first” segment of the market.

Haiden Technology Pvt. Ltd.

Products: Safety lancets, automatic and semi-automatic lancets.

Strengths:

Emerging company with innovative automated lancet designs for hospitals and homecare.

Focused on modernizing lancet technology for safety, pain reduction, and ease of use.

Growing presence in developing markets gives it expansion potential.

HemoCue

Products: Diagnostic devices and lancets compatible with lab and hospital equipment.

Strengths:

Strong presence in diagnostic labs and hospital networks.

Offers integrated solutions combining device and lancet, improving efficiency and workflow.

Reputation for accuracy and reliability supports adoption in clinical environments.

Hoffman-La Roche Ltd.

Products: Biotech and diagnostic products including lancets and glucose-monitoring devices.

Strengths:

Financial and R&D power enables innovation in next-generation lancets.

Integration with diagnostic systems provides end-to-end solutions for hospitals and labs.

Established brand credibility enhances acceptance in professional healthcare sectors.

Latest Announcements

Thriva + Tasso (April 2025): Collaboration for needle-free blood collection, reducing needle phobia and enabling remote testing.

Drawbridge Health (April 2024): FDA 510(k) clearance for OTC NanoDrop lancet for at-home use, opening the homecare market.

Thorne Healthcare (June 2023): CE Mark for NanoDrop device using dual nano-lancet technology for painless blood sampling.

MTD acquisition of Ypsomed (Aug 2024): Expansion of pen-needles and lancet production in Europe, indicating consolidation and increased manufacturing scale.

Recent Developments

Nano-Lancet Technology: Regulatory approvals (CE, FDA) enable less painful sampling for children, elderly, and needle-phobic users.

OTC / Home-Use Device Approvals: Devices like Drawbridge Health’s NanoDrop are expanding access beyond hospitals.

Needle-Free Sampling Shift: Partnerships like Thriva + Tasso promote needle-free methods, potentially reshaping the market.

M&A Driven Scale-Up: Consolidations (e.g., MTD + Ypsomed) increase production capacity and global distribution.

Export Growth from Asia: China and India expanding lancet exports globally, affecting pricing and availability.

Segments Covered

By Type:

Standard Lancets — basic, cost-effective, widely used.

Safety Lancets — designed for minimal injury, retractable needles, preferred for safety.

Manually Activated Lancets — traditional lancets requiring manual activation; low-cost and simple.

Automatically Activated Lancets — modern devices activating at touch/press, offering ease & less pain.

By Needle Size (Gauge):

23G–33G — standard, versatile; dominant segment due to general-use suitability (blood glucose, cholesterol, HbA1c).

22G and Below — thicker needles, for cases needing larger blood volume or for patients with thicker skin. Growing fastest due to demand where standard sizes don’t suffice.

Above 33G — ultra‑fine needles, for pediatric use or patients with sensitive skin; limited but niche requirement.

By End-Use / User Setting:

Hospitals — historically the largest users due to frequent diagnostics and trained personnel.

Ambulatory Surgical Centers (ASCs) — fastest-growing usage location as minor procedures and diagnostics shift out of hospital settings.

Clinics & Diagnostic Labs — steady demand for routine blood tests and diagnostic panels.

Homecare / At-Home Testing — growing segment due to consumer demand for remote self-testing and chronic disease monitoring.

By Region:

North America — largest share, mature market.

Asia-Pacific (notably China, India, Japan) — fastest growth potential because of population size, rising chronic diseases, improving healthcare infrastructure.

Europe — moderate growth, driven by preventive healthcare and regulatory support.

Other Regions (Latin America, MEA) — emerging demand as healthcare access improves and cost-effective lancets become available.

Top 5 FAQs

-

What is the projected size and growth of the global lancets market by 2035?

It is expected to grow from USD 1.59 billion in 2025 to USD 2.65 billion by 2035, at a CAGR of 4.77%. -

Which needle size and type dominate currently?

Lancets in the 23G–33G range dominate, and standard lancets lead in overall volume due to simplicity and cost‑effectiveness. -

Which region currently holds the largest share, and which region is growing fastest?

North America holds the largest share (~42% in 2024); Asia‑Pacific — especially countries like India and China — is the fastest-growing region. -

What trends are driving future growth in lancet demand?

Key trends include rising diabetes and chronic disease prevalence, growing demand for at-home and preventive testing, innovations toward pain-free and safety lancets, and regulatory approvals for home-use devices. -

Which companies lead the lancet market and what distinguishes them?

Leading companies include Abbott Laboratories, BioCare Corporation, Bioland Technology Ltd., Braun SE, Drawbridge Health, ForaCare, Genteel, Haiden Technology Pvt. Ltd., HemoCue, and Hoffman‑La Roche Ltd. They stand out through global distribution, innovation (safety/nano/at-home lancets), reliability, integration with diagnostic systems, and strong manufacturing capabilities.

Access our exclusive, data-rich dashboard dedicated to the medical devices industry – built specifically for decision-makers, strategists, and industry leaders. The dashboard features comprehensive statistical data, segment-wise market breakdowns, regional performance shares, detailed company profiles, annual updates, and much more. From market sizing to competitive intelligence, this powerful tool is one-stop solution to your gateway.

Access the Dashboard: https://www.towardshealthcare.com/access-dashboard

Checkout Lancets Market Report Now at: https://www.towardshealthcare.com/checkout/5251

Become a valued research partner with us – https://www.towardshealthcare.com/schedule-meeting

You can place an order or ask any questions, please feel free to contact us at sales@towardshealthcare.com

Powering Healthcare Leaders with Real-Time Insights: https://www.towardshealthcare.com/healthcare-intelligence-platform

Europe Region – +44 778 256 0738

North America Region – +1 8044 4193 44

APAC Region: +91 9356 9282 04

Visit Our Website: https://www.towardshealthcare.com

Find us on social platforms: LinkedIn | Twitter | Instagram | Medium | Pinterest