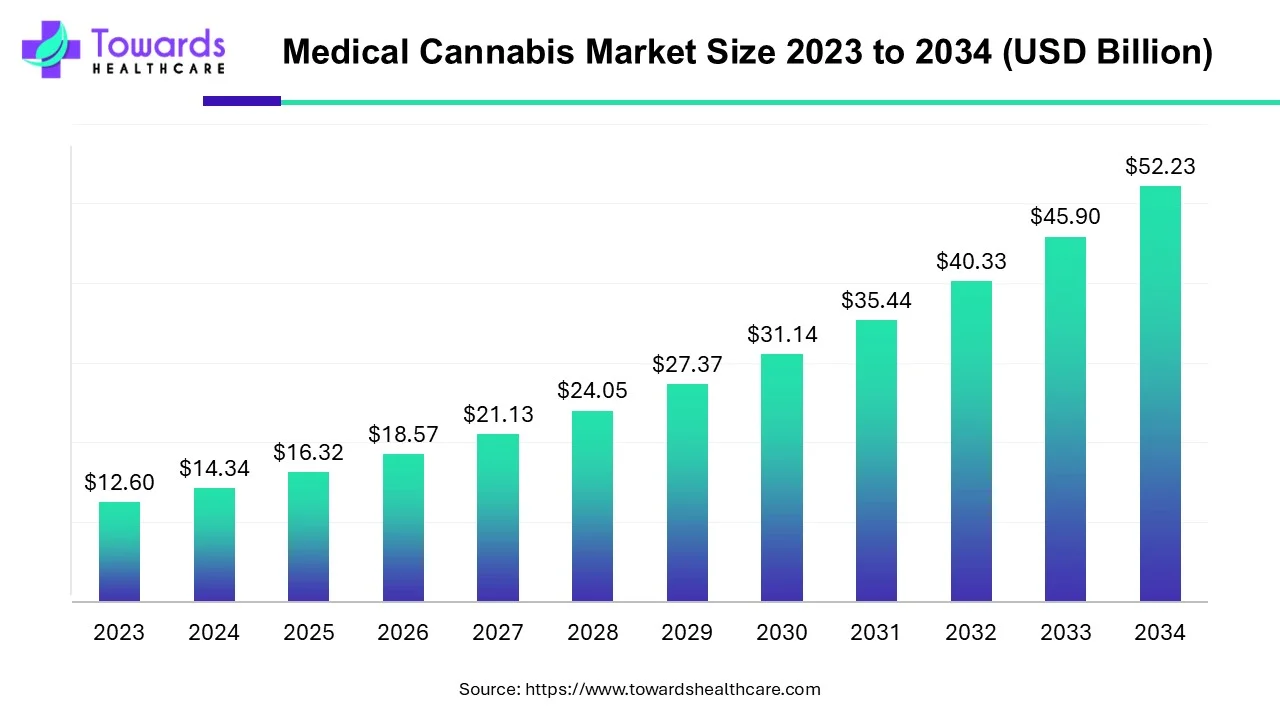

The global medical cannabis market is projected to expand from USD 16.32 billion in 2025 (USD 14.34B in 2024) to USD 52.23 billion by 2034, representing a CAGR of 13.8% (2025–2034) — driven by rising chronic pain prevalence, growing R&D and awareness, and expanding legal access.

Download the free sample and get the complete insights and forecasts report on this market @ https://www.towardshealthcare.com/download-sample/5099

Market size

Overall global baseline & forecast

➣Market size: USD 14.34 billion (2024).

➣Forecast: USD 16.32 billion (2025) → USD 52.23 billion (2034); CAGR 13.8% (2025–2034).

Product-type trajectories

➣Dissolvable / Powders: 2024 = 5.02 → 2034 = 18.28 — dominant in 2024; fastest absolute growth and preferred for rapid oral dosing & nanoemulsion applications.

➣Oil: 2024 = 3.59 → 2034 = 13.06 — highly concentrated format; forecasted to be a major growth engine across the decade.

➣Solids: 2024 = 2.87 → 2034 = 10.45 — steady growth with patient-preference for pre-dosed formats.

➣Ointments & Creams (Topicals): 2024 = 2.87 → 2034 = 10.45 — growing adoption for localized pain & dermatological indications.

Derivative (active compound) structure

➣Cannabidiol (CBD): largest revenue share in 2024 — used especially for anticonvulsant and anti-inflammatory products (Epidiolex is cited as an approved CBD-based medicine).

➣Tetrahydrocannabinol (THC): fastest-growing derivative in forecast period — strong for indications like chemotherapy nausea, appetite stimulation, and certain neuropathic pains.

Route of administration

➣Inhalation: highest revenue share in 2024 — fastest onset, used in hospital/acute settings and where rapid effect is needed.

➣Oral: fastest-growing route — advantages: dosing adherence, ease of use, suitability for geriatric & pediatric patients, avoids respiratory risks.

Distribution channel snapshot

➣Hospital pharmacy: dominant channel in 2024 — trusted by clinicians, supports monitored dosing and inpatient use.

➣Online pharmacy: fastest growth forecast — increasing e-commerce adoption, convenience, telemedicine integrations.

➣Regional split (selected reference years)

➣North America: 2024 = 5.74 → 2034 = 20.89 (largest revenue share in 2024).

➣Europe: 2024 = 3.59 → 2034 = 13.06.

➣Asia-Pacific: 2024 = 2.87 → 2034 = 10.45 (fastest-growing region by trend).

➣Latin America: 2024 = 1.15 → 2034 = 4.18.

➣Middle East & Africa: 2024 = 1.00 → 2034 = 3.66.

Market Trends

Regulatory liberalization in select markets (North America & elsewhere)

➣Canada’s Cannabis Act now underpins both medical and recreational frameworks (noted as a mature market).

➣U.S. has a patchwork — 47 states + DC + 3 territories allow medical cannabis (14 states + 2 territories run comprehensive medical-only programs).

Shifts to regulated, clinical supply channels

➣Hospital pharmacies led distribution in 2024 due to clinical trust and infrastructure; online pharmacies are rapidly gaining share for convenience and remote access.

Product innovation & formulation advances

➣Rise of dissolvable/powders (dominant in 2024) and nanoemulsion tech to improve solubility, bioavailability and dosing precision — enabling oral fast-acting formats.

Derivative demand divergence

➣CBD holds the largest revenue share (2024) due to anticonvulsant and anti-inflammatory claims; THC poised to grow fastest as more therapeutic uses and regulated formulations expand.

Investment, M&A and partnerships accelerating market integration

➣Examples: Organigram’s €14M investment in Sanity Group (June 2024); Aurora’s distribution partnerships; acquisitions and minority stakes (High Tide acquiring stake in Purecan GmbH, Jan 2025).

Cross-industry strategic moves

➣Tobacco / Big-tobacco subsidiaries (e.g., Philip Morris’ Vectura Fertin Pharma) entering cannabinoid-based medicine R&D and commercialization (collaboration with Avicanna, Jan 2025).

Country-level reform & commercialization

➣India: reported legalization for medical use and local provider growth (Boheco revenue growth FY2024→FY2025).

➣Nepal: government announcement to legalize cultivation and medicinal consumption (budget allocations cited).

Clinical research and constrained evidence base

➣Growing R&D but clinical evidence for many applications remains limited due to regulatory constraints (federal prohibitions hinder large-scale trials in some jurisdictions).

Patient / prescriber adoption dynamics

➣Rapidly increasing public awareness and patient demand (especially for chronic pain, epilepsy), but physician comfort and clinical guidelines lag behind in many regions.

Supply chain & sourcing complexity

➣Multi-jurisdictional licensing, quality control and variable domestic production capacity (imports/exports and pharma-grade manufacturing are hot spots).

AI impacts / roles

Precision cultivation & environmental control

➣AI models ingest climate, light, humidity, CO₂ and nutrient data to recommend minute adjustments (automation of grow rooms). Result: consistent cannabinoid profiles and increased yields.

Predictive phenotype & chemotype selection

➣Machine learning on genotype/phenotype datasets helps breeders select strains that reliably express target CBD/THC ratios and terpene profiles for specific therapeutic outcomes.

Automated quality control & visual inspection

➣Computer-vision systems detect mold, pests, bud defects and post-harvest contamination in real time, reducing recalls and ensuring batch uniformity for medical use.

Process optimization for extraction & formulation

➣AI optimizes solvent choice, temperature, and throughput in extraction and distillation, increasing purity and reducing solvent residuals — critical for pharma-grade oil and powders.

Formulation design (bioavailability & stability)

➣In-silico modelling assists nanoemulsion, encapsulation and oral matrix design to maximize absorption, predict shelf life, and reduce batch failure in powders and oils.

Supply-chain forecasting & inventory optimization

➣Demand forecasting models predict hospital and pharmacy usage, optimizing batch release, reducing waste, and ensuring regulated products are available where needed.

Personalized medicine & dose titration support

➣Clinical decision support tools can integrate patient data (age, weight, comorbidity, prior response) to suggest titration schedules and formulations (oral vs inhaled), improving safety and adherence.

Clinical trial acceleration & signal detection

➣AI helps design smarter adaptive trials, identify responder subgroups and detect adverse event signals faster in post-marketing surveillance and real-world evidence studies.

Regulatory compliance & documentation automation

➣Natural language processing (NLP) automates batch records, labeling compliance checks and audit-ready traceability, which is essential in highly regulated hospital/pharmacy channels.

Market intelligence & patient insights

➣Advanced analytics of anonymized patient-reported outcomes and e-pharmacy data surfaces unmet needs (e.g., neurological subpopulations), enabling targeted R&D and product launches.

Regional insights

North America (lead: 2024 = 5.74B → 2034 = 20.89B)

➣Regulatory patchwork: State-by-state variation drives fragmentation; reimbursement & prescribing pathways differ across jurisdictions.

➣Clinical adoption & hospital channels: High hospital pharmacy share reflects clinician integration for chronic pain & palliative care.

➣Commercial sophistication: Large multi-state operators, strong private investment, and distribution networks accelerate scale.

Europe (2024 = 3.59B → 2034 = 13.06B)

➣Rapid regulatory commercialization in select countries: Germany and other markets are expanding access (Sanity Group ~10% of German medical market, Organigram investment to expand supply).

➣Pharma-style expectations: Europe demands GMP, EU-GMP certifications and pharma distribution pathways—favors vertically integrated GMP players.

Asia-Pacific (2024 = 2.87B → 2034 = 10.45B)

➣Mixed policy landscape: Australia and Thailand moving toward medical access; many countries retain strict controls.

➣China & patents: China holds substantial patent share (out of 606 cannabis-related patents, 309 are owned by China) and regulator action (NMPA notice Aug 2024 on cannabidiol and other substances) — indicates an R&D and IP play in APAC.

➣India: Noted legalization for medical use and early revenue growth from domestic players (Boheco: Rs 5.3 crore → Rs 7.5 crore FY2025, strong month-on-month growth).

Latin America (2024 = 1.15B → 2034 = 4.18B)

➣Policy momentum: Several countries exploring medical frameworks; favorable climates for cultivation and export potential.

Middle East & Africa (2024 = 1.00B → 2034 = 3.66B)

➣Emerging market opportunity: Slow but steady regulatory changes and interest in medicinal cultivation and export; hospital pharmacy channels likely to lead initial adoption.

Country highlights (selected)

➣Canada: Mature regulatory framework (Cannabis Act replaces ACMPR); household cannabis spending significant (Q2 2025 = $1.7B total; $119M medical).

➣Germany: Large pharmacy distribution networks (Sanity Group strong presence) — strategic hub for EU expansion.

Nepal: Government announced legalization for medicinal cultivation and budget allocation (fiscal 2024-25) — signals new production hubs.

Market dynamics

Primary demand drivers

➣Rising prevalence of chronic pain conditions & neurological disorders (epilepsy, MS), patient awareness, and clinician acceptance for some indications.

Supply-side enablers

➣Advances in cultivation tech, formulation (nanoemulsions, powders), pharmaceutical manufacturing (EU-GMP), and strategic M&A/partnerships to secure supply chains.

Key restraints

➣Fragmented legal/regulatory landscape; federal prohibitions in some important markets restricting large randomized trials and cross-border trade.

Quality & consistency imperatives

➣Medical use requires batch-to-batch consistency — drives demand for pharmaceutical-grade production, analytics, and traceability.

Pricing & reimbursement

➣Out-of-pocket in many places; integration into public formularies remains limited — affects adoption speed.

Channel shift

➣Hospitals and pharmacies remain dominant for clinical trust; online pharmacies are an emerging, convenience-led growth channel.

R&D & evidence base

➣Solid evidence exists for discrete uses (e.g., certain CBD drug approvals); many other indications require better trials and regulatory clarity.

M&A & vertical integration

➣Market favors vertically integrated companies controlling cultivation → processing → distribution to meet regulatory specs.

Intellectual property & patents

➣Patent activity (notably China’s share) will shape botanical extraction, formulation and process advantages.

Social & policy risk

➣Stigma, political shifts, and differing national drug policies can rapidly change market access and investment attractiveness.

Top 10 companies

Ilray Inc.

Product: Listed as a market participant (medical cannabis products).

Overview: Positioned among global operators; competes on product breadth.

Strength: Presumably vertical capabilities and product diversification (powders/oils/topicals) — typical strength of listed market players.

Canopy Growth Corporation

Product: Broad medical & consumer cannabis product portfolio.

Overview: One of the large-scale Canadian operators named as a key player.

Strength: Scale in cultivation, extensive R&D partnerships and global distribution potential.

Aurora Cannabis Inc.

Product: Medical cannabis products and brands (also distribution partnerships).

Overview: Active in international distribution — example: partnership to distribute MedReleaf Australia brands (Dec 2024).

Strength: Established international supply chain and partnership capability.

Endoca

Product: CBD-centric therapeutic and wellness products (implied by being a listed company).

Overview: Known in market lists for cannabinoid products and extracts.

Strength: Focus on high-quality extracts and consumer trust in natural product formulations.

Curaleaf Holding Inc.

Product: Medical cannabis products and dispensary networks.

Overview: Identified among key firms serving hospital & pharmacy channels.

Strength: Broad U.S. reach, retail and medical distribution synergies.

Medical Marijuana Inc.

Product: CBD/medical cannabinoid products.

Overview: One of the early listed companies in the sector.

Strength: Brand longevity and established consumer product pipelines.

Green Thumb Industry

Product: Medical & wellness cannabis products.

Overview: Multi-state operator style presence (listed as key).

Strength: Integrated retail and regional distribution strengths.

Acreage Holdings

Product: Medical cannabis production and retail.

Overview: Positioned among North American multi-state operators.

Strength: Real estate and operational footprint to scale across states.

GW Pharmaceutical Plc. (GW)

Product: Prescription cannabinoid medicines — notably Epidiolex (CBD-based medication cited in your content).

Overview: Pharma-style approach with regulatory-approved medicines for epilepsy and seizure disorders.

Strength: Clinical trial pedigree, regulatory approvals and pharma distribution channels.

Folium Europe B.V.

Product: European-focused medical cannabis products (listed).

Overview: Focus on EU markets where GMP / pharma standards matter.

Strength: Regional specialization — ability to meet EU regulatory/quality demands.

Latest announcements

Avicanna — Vectura Fertin Pharma collaboration (Jan 2025)

➣Strategic collaboration aiming to improve medical cannabis access/applications in Canada. Vectura Fertin Pharma is a PMI subsidiary focused on cannabinoid-based medicines and clinical R&D.

South Carolina Compassionate Care Act bill introduced (Dec 2024)

➣A state senator introduced legislation to legalize medical cannabis for qualifying conditions; framed as an alternative for conditions traditionally treated with opioids.

Organigram — €14 million investment in Sanity Group (June 2024)

➣Investment to expand supply agreement and strengthen presence in the German medical cannabis market (Sanity Group ~10% German share; 2,000+ pharmacy distribution).

Aurora distribution partnership with The Entourage Effect / MedReleaf Australia (Dec 2024)

➣Distribution partnership to expand access to Aurora/MR products across Australian pharmacies.

SOMAÍ exclusive manufacturing/distribution partnerships across Europe & Australia (Apr 2025)

➣SOMAÍ partners with SHERBINSKIS and BOUTIQ to manufacture/distribute products, expanding access in Europe & Australia.

High Tide — definitive agreement to acquire 51% of Purecan GmbH (Jan 2025)

➣Strategic entry into German medical cannabis market (approx. €4.8M acquisition with option on remaining interest).

Philip Morris (via Vectura Fertin Pharma) — partnership with Avicanna (Jan 2025)

➣Tobacco company enters medical cannabis R&D/commercialization via its cannabinoid medicines subsidiary.

Medcana (Software Effective Solutions Corp.) moving to acquire pharmaceutical cannabis licenses in Australia (Apr 2025)

➣Acquisition of import/distribution licenses to enter Australian market — part of global expansion plan.

Jack Herer Brand — strategic partnership with SOMAÍ (Apr 2025)

U.S.-based brand partners SOMAÍ (EU-GMP MCO) for EU distribution and manufacturing.

Nepal — Finance Minister Barsha Man Pun announces legal cultivation & medicinal use; budget allocated (FY2024–25)

➣Policy signal to develop commercial production and supportive legal frameworks.

Recent developments

Consolidation & partnerships accelerating access — companies are using investments, minority stakes and distribution deals (Organigram↔Sanity; Aurora↔MedReleaf Australia; High Tide↔Purecan) to rapidly enter key national markets (Germany, Australia) that require high regulatory compliance.

Big-industry players entering R&D — tobacco/large corporates (Philip Morris via Vectura Fertin Pharma) are moving into cannabinoid therapeutics, bringing capital and pharma R&D capabilities.

Supply & manufacturing globalization — EU-GMP certified operators and MCOs like SOMAÍ are forming cross-border partnerships for manufacturing and distribution, indicating a shift toward standardized pharmaceutical supply chains.

Policy momentum in emerging markets — India, Nepal and select U.S. states show policy reforms that create new domestic markets and local manufacturing opportunities.

Commercial channel evolution — online pharmacies plus hospital pharmacies are both strategic: hospitals for trust & oversight; online for scale, remote access, and consumer convenience.

R&D & patents shaping competitiveness — strong patent holdings (China) and targeted R&D explain why strategic investments are focused on formulation and pharma-grade outputs.

Segments covered

A. By Product Type

Dissolvable / Powders

➣Use case: Rapid oral dosing, suitable for precise titration and pediatric/geriatric dosing.

➣Tech: Nanoemulsion, solubility enhancers for fast onset.

➣Market note: Dominant in 2024; projected strong CAGR to 2034.

Oil

➣Use case: Concentrated dosing, tinctures, sublingual administration.

➣Tech: Standard extraction/distillation; pharma methodology required for medicinal oils.

➣Market note: High forecasted growth as concentrated formulations scale.

Solids (tablets/capsules)

➣Use case: Controlled dosing, easy integration into hospital formularies.

➣Regulatory note: Strong preference where prescription and dosing standardization is required.

Ointments & Creams (Topicals)

➣Use case: Localized pain and dermatologic conditions with low systemic exposure.

➣Patient benefit: Avoids systemic psychoactive effects for certain indications.

B. By Derivative

➣Cannabidiol (CBD): Largest share (2024) — critical for epilepsy and seizure-related approvals.

➣Tetrahydrocannabinol (THC): Fastest growing due to appetite, antiemetic, and certain pain indications.

C. By Route of Administration

➣Inhalation: Rapid effect — useful in acute symptomatic care.

➣Oral: Best for chronic therapy adherence, safety in vulnerable populations.

➣Topical: Local action, minimal systemic side effects.

D. By Distribution Channel

➣Hospital Pharmacy: Clinical oversight, inpatient use, stronger acceptability for prescribers.

➣Online Pharmacy: Convenience, telehealth integration, fastest growth.

➣Retail Pharmacy: Community accessibility and prescription fulfilment.

E. By Region / Country (covered earlier)

Each region shows distinct regulatory, commercial and supply characteristics — North America is largest today while APAC is a rapid growth frontier with complex legal mixes.

Top 5 Searched Queries

Q1 — What is the current market size and growth outlook for medical cannabis?

Ans — The market was USD 14.34 billion in 2024, is estimated at USD 16.32 billion in 2025, and is forecast to reach USD 52.23 billion by 2034, implying a CAGR of 13.8% (2025–2034).

Q2 — Which regions and product types lead the market?

Ans — North America held the largest revenue share in 2024 (USD 5.74B). Dissolvable/powders were the dominant product type in 2024, while oil formats and the oral route are the fastest growing segments.

Q3 — Who are the major companies and what are their strengths?

Ans — Key players listed include Canopy Growth, Aurora Cannabis, Curaleaf, GW Pharmaceuticals, Green Thumb, Medical Marijuana Inc., Acreage Holdings, Endoca, Folium Europe B.V., Ilray Inc. Strengths range from pharma-grade approvals (GW’s Epidiolex) to extensive distribution networks (Aurora, Canopy) and regional GMP capabilities (EU operators).

Q4 — How do regulation and policy affect market expansion?

Ans — Market expansion is tightly linked to legal reforms and regulatory clarity. While countries like Canada have comprehensive frameworks, many markets remain patchworks (US states) or have strict controls (various APAC countries). Policy shifts (e.g., India, Nepal, and new U.S. state bills) are unlocking new demand and supply opportunities.

Q5 — How is AI changing medical cannabis production and commercialization?

Ans — AI is being used to optimize cultivation conditions, ensure batch consistency, design formulations (nanoemulsions), automate quality control, improve supply forecasting, accelerate clinical R&D, and help meet regulatory traceability needs — all crucial for pharmaceutical-grade medical cannabis.

Access our exclusive, data-rich dashboard dedicated to the therapeutic area sector – built specifically for decision-makers, strategists, and industry leaders. The dashboard features comprehensive statistical data, segment-wise market breakdowns, regional performance shares, detailed company profiles, annual updates, and much more. From market sizing to competitive intelligence, this powerful tool is one-stop solution to your gateway.

Access the Dashboard: https://www.towardshealthcare.com/access-dashboard

Immediate Delivery Available | Buy This Premium Research @ https://www.towardshealthcare.com/price/5099

Become a valued research partner with us – https://www.towardshealthcare.com/schedule-meeting

You can place an order or ask any questions, please feel free to contact us at sales@towardshealthcare.com

Powering Healthcare Leaders with Real-Time Insights: https://www.towardshealthcare.com/healthcare-intelligence-platform

Europe Region – +44 778 256 0738

North America Region – +1 8044 4193 44

APAC Region: +91 9356 9282 04

Web: https://www.towardshealthcare.com

Find us on social platforms: LinkedIn | Twitter | Instagram | Medium | Pinterest