Medical Devices 2035: The $1,083 Billion Healthcare Shift!

The global medical devices industry is no longer just a backbone of healthcare; it has become its nervous system. From simple diagnostic kits to AI-powered surgical robots, medical devices now shape how doctors detect disease, treat patients, and monitor recovery.

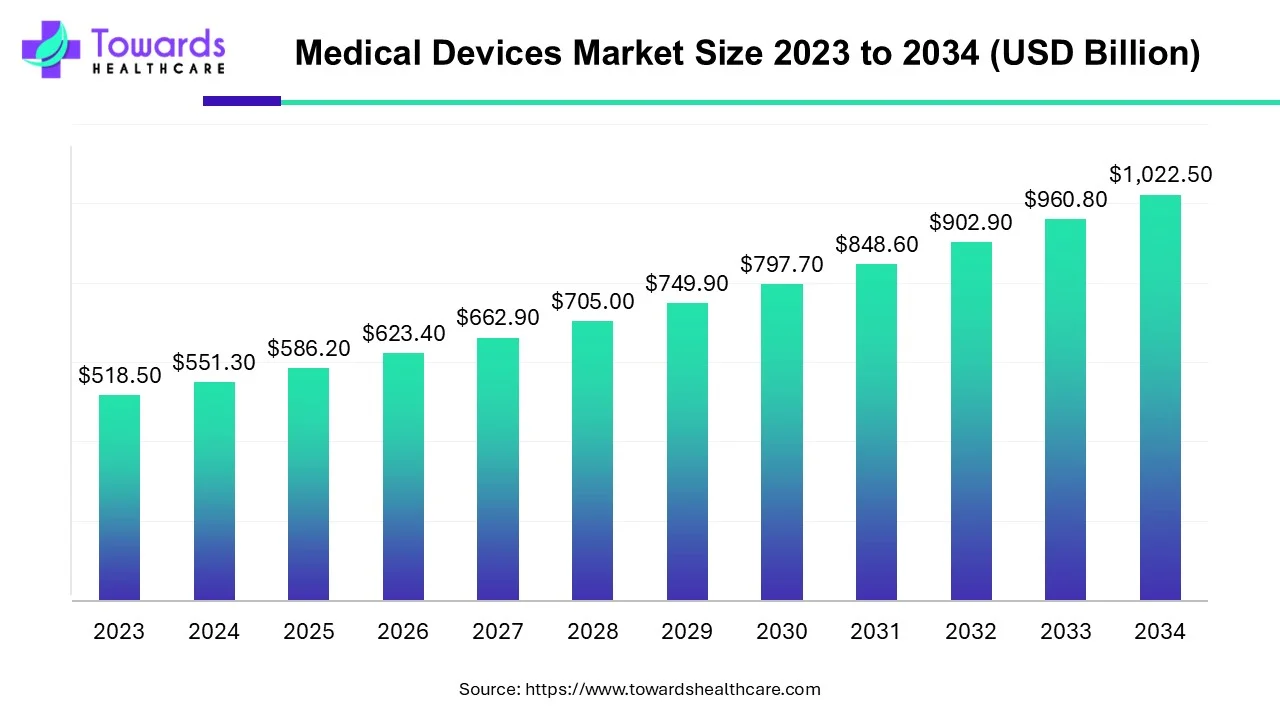

In 2025, the global medical devices market stands at USD 586.20 billion. It is expected to grow to USD 623.37 billion in 2026 and surge to USD 1,083.96 billion by 2035, expanding at a steady CAGR of 6.34% between 2026 and 2035. Behind these numbers lies a powerful transformation driven by technology, accessibility, and changing patient expectations.

Download Free Sample: https://www.towardshealthcare.com/download-sample/5487

This is not just market expansion. It is a MedTech revolution.

Table of Contents

ToggleHealthcare Is No Longer Reactive—It Is Intelligent

Medical devices today do more than support treatment. They predict complications, guide surgeons in real time, and continuously monitor chronic conditions.

Organizations such as the World Health Organization define medical devices broadly—from tongue depressors to programmable pacemakers and in vitro diagnostic kits. Globally, there are nearly 2 million medical devices, grouped into more than 7,000 categories.

The shift from traditional equipment to connected, data-driven devices has redefined care delivery. Hospitals no longer rely solely on physician expertise; they increasingly depend on precision tools that reduce error margins and improve clinical outcomes.

The AI Surge That Changed Everything

Artificial intelligence has moved from pilot projects to core infrastructure within medical devices.

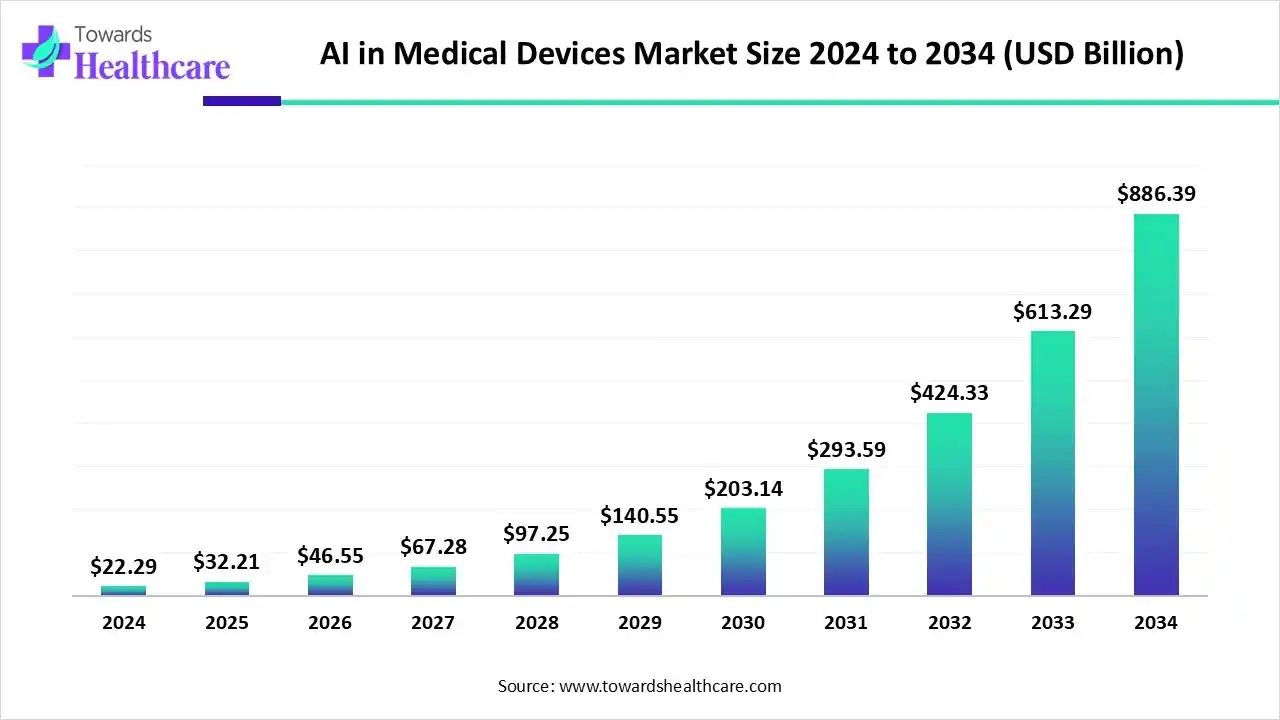

The global AI in medical devices market jumped from USD 22.29 billion in 2024 to USD 32.21 billion in 2025. By 2034, projections suggest it could approach USD 886.39 billion, expanding at a striking CAGR of 44.53%.

This surge is not accidental.

AI-enabled imaging systems detect tumors with greater sensitivity. Machine learning algorithms flag irregular heart rhythms. Smart insulin pumps adjust dosages automatically. Surgical robots enhance dexterity during complex procedures.

The U.S. Food and Drug Administration has approved nearly 1,000 AI-powered medical devices between 1995 and August 2024, signaling strong regulatory momentum behind intelligent MedTech.

AI no longer assists healthcare; it actively participates in decision-making.

In Vitro Diagnostics Lead the Charge

Among all device categories, In Vitro Diagnostics (IVD) dominate the market.

In 2024, the IVD segment reached USD 88.0 billion and continues to expand steadily through 2034. These devices detect infections, chronic conditions, and genetic markers outside the human body using blood, tissue, or other samples.

Governments encourage early disease detection programs. Screening initiatives and point-of-care diagnostics increase demand. Clinicians depend on IVD results for the majority of medical decisions.

Simply put, diagnostics drive modern medicine; and diagnostics drive this market.

Diabetes Care Is Accelerating Faster Than Ever

While IVD leads in size, diabetes care devices are growing at the fastest pace.

Glucose monitors, continuous glucose monitoring (CGM) systems, insulin pumps, and smart pens allow patients to manage their conditions independently. Rising diabetes prevalence across Asia-Pacific, the Middle East, and North America fuels adoption.

Insurance coverage expansion and improved device affordability further strengthen growth.

Patients no longer visit labs daily. They manage their health in real time.

Hospitals Still Dominate; but Clinics Are Catching Up

Hospitals and Ambulatory Surgical Centers (ASCs) remain the largest end-users of medical devices. Strong capital investment, reimbursement structures, and access to specialized professionals explain their dominance.

Between 2011 and 2014, hospital spending on implantable devices rose from USD 12.1 billion to USD 13.8 billion, growing at 4.7% annually. Medical supply expenses also increased steadily. Together, these costs consumed a rising share of hospital budgets.

However, clinics are emerging as powerful growth hubs.

Specialized oncology centers, diagnostic labs, and outpatient facilities increasingly deploy advanced imaging and monitoring tools. In the United States alone, there are 72 NCI-Designated Cancer Centers, accelerating high-end device utilization outside traditional hospital settings.

Healthcare decentralization is underway.

North America Sets the Pace

North America held the largest market share in 2024. Strong regulatory systems, innovation ecosystems, and advanced R&D infrastructure fuel leadership.

The United States remains a global export powerhouse, shipping USD 34.8 billion worth of medical instruments in 2023. Trade policies and startup activity strengthen its position.

Canada also demonstrates momentum, with healthcare spending reaching approximately USD 344 billion in 2023, representing 12.1% of GDP. More than 70% of this spending is publicly funded, supporting stable device procurement.

Innovation thrives in structured ecosystems.

Asia-Pacific Manufactures the Future

Asia-Pacific is projected to host the fastest-growing medical devices market in the coming years.

China exports billions of dollars’ worth of medical instruments annually and has simplified regulatory processes to attract foreign manufacturers. The country exported USD 11.6 billion in medical instruments between March 2024 and February 2025.

India continues to expand exports, rising from USD 1,868.05 million in 2017-18 to USD 2,923.16 million in 2021-22. Government policies such as the Production Linked Incentive (PLI) Scheme and 100% FDI allowance accelerate domestic manufacturing.

Japan, regulated by the Pharmaceuticals and Medical Devices Agency, faces a rapidly aging population—over 36 million citizens aged 65 and above; creating consistent demand for advanced devices.

Asia-Pacific does not just consume devices; it manufactures and innovates.

Europe Balances Innovation and Regulation

Europe maintains steady growth supported by established players such as:

-

Siemens Healthineers

-

Medtronic

-

Fresenius Medical Care

Germany alone filed more than 15,000 patent applications in medical technology with the European Patent Office in 2023. Approximately 500,000 types of medical devices and IVDs are available in the country.

Europe combines regulatory discipline with engineering excellence.

Middle East, Africa, and Latin America Rise Steadily

Emerging regions show promising acceleration.

In the UAE, one in three people suffers from chronic conditions, increasing demand for monitoring and diagnostic tools. South Africa reports tens of millions of diabetes cases, intensifying device imports.

Brazil announced investments of nearly USD 480 million for procurement of over 10,000 medical devices. Latin American governments increasingly prioritize domestic production to reduce import dependence.

Healthcare expansion in these regions creates structural long-term demand.

Investment Momentum Strengthens the Ecosystem

Global investments reflect confidence in MedTech’s future.

-

Shanghai Kohope Medical Devices invested USD 2.5 million to expand syringe manufacturing.

-

The South Korean government committed over USD 622 million to next-generation diagnostic tools and robotics.

-

Philips invested USD 150 million to expand AI-based ultrasound and imaging manufacturing in Pennsylvania.

-

Micro Life Sciences raised USD 200 million from the Abu Dhabi Investment Authority.

Capital inflow enables R&D acceleration, scale manufacturing, and geographic expansion.

Regulation: The Double-Edged Sword

While strong regulatory frameworks in the U.S., Europe, and Japan enhance safety and trust, many developing nations lack structured oversight. Several African countries depend on European or U.S. approvals due to limited regulatory capacity.

This dependence increases compliance costs for local manufacturers and restricts customization for regional health needs.

Balancing safety with accessibility remains a central policy challenge.

Technology Expands the Definition of a Device

Modern medical devices integrate:

-

Telemedicine platforms

-

Wearable monitoring systems

-

Robotics

-

3D printing

-

Nanotechnology

-

Augmented and virtual reality

These technologies increase precision and personalize care pathways. Manufacturers now compete not only on hardware but on data intelligence, interoperability, and connectivity.

A pacemaker is no longer just an implant. It is a connected data platform.

The Human Side of MedTech

Behind every billion-dollar projection lies a patient.

A diabetic child checks glucose levels without pain.

An elderly cardiac patient receives remote monitoring alerts.

A surgeon completes a minimally invasive procedure with robotic guidance.

Medical devices do not simply generate revenue; they extend life expectancy, improve recovery rates, and reduce healthcare system burdens.

Corporate Leadership and Market Influence

Leading companies continue to shape global MedTech trends.

Medtronic reported FY2024 revenue of USD 32.4 billion, with USD 11.8 billion from cardiovascular products and USD 9.4 billion from neuroscience.

Stryker Corporation recorded USD 22.6 billion in annual net sales, marking double-digit growth.

Innovation also emerges from regional firms like Dr Morepan, which expands into wellness products while building long-term healthcare brands.

Competition drives advancement.

The Road to 2035: What Lies Ahead?

As the industry approaches the trillion-dollar milestone, several forces will shape the next decade:

-

AI-driven predictive diagnostics

-

Personalized implantable technologies

-

Home-based remote monitoring

-

Expanding reimbursement ecosystems

-

Localized manufacturing in emerging economies

The global market’s rise to USD 1,083.96 billion by 2035 reflects more than financial growth—it reflects healthcare system transformation.

Final Perspective: A Market That Mirrors Humanity

The medical devices market grows because healthcare challenges grow. Chronic diseases rise. Populations age. Expectations evolve.

Technology answers these demands.

Governments invest. Companies innovate. Regulators adapt. Clinicians learn. Patients engage.

The result is a healthcare environment where machines enhance human expertise rather than replace it.

Medical devices have moved from supportive tools to central pillars of modern medicine. As the world advances toward 2035, this industry will not merely expand; it will redefine how healthcare operates across continents.

The trillion-dollar horizon is not the destination. It is the beginning of a smarter, more connected era in global healthcare.

Access our exclusive, data-rich dashboard dedicated to the medical devices market – built specifically for decision-makers, strategists, and industry leaders. The dashboard features comprehensive statistical data, segment-wise market breakdowns, regional performance shares, detailed company profiles, annual updates, and much more. From market sizing to competitive intelligence, this powerful tool is one-stop solution to your gateway.

Access the Dashboard: https://www.towardshealthcare.com/access-dashboard

Checkout Medical Devices Market Report Now at: https://www.towardshealthcare.com/checkout/5487

You can place an order or ask any questions, please feel free to contact us at sales@towardshealthcare.com

Europe Region – +44 778 256 0738

North America Region – +1 8044 4193 44

APAC Region: +91 9356 9282 04

Visit Our Website: https://www.towardshealthcare.com

Find us on social platforms: LinkedIn | Twitter | Instagram | Medium | Pinterest