Is the Multiple Myeloma Market on Track for a $50 Billion Boom in 2025 and Beyond?

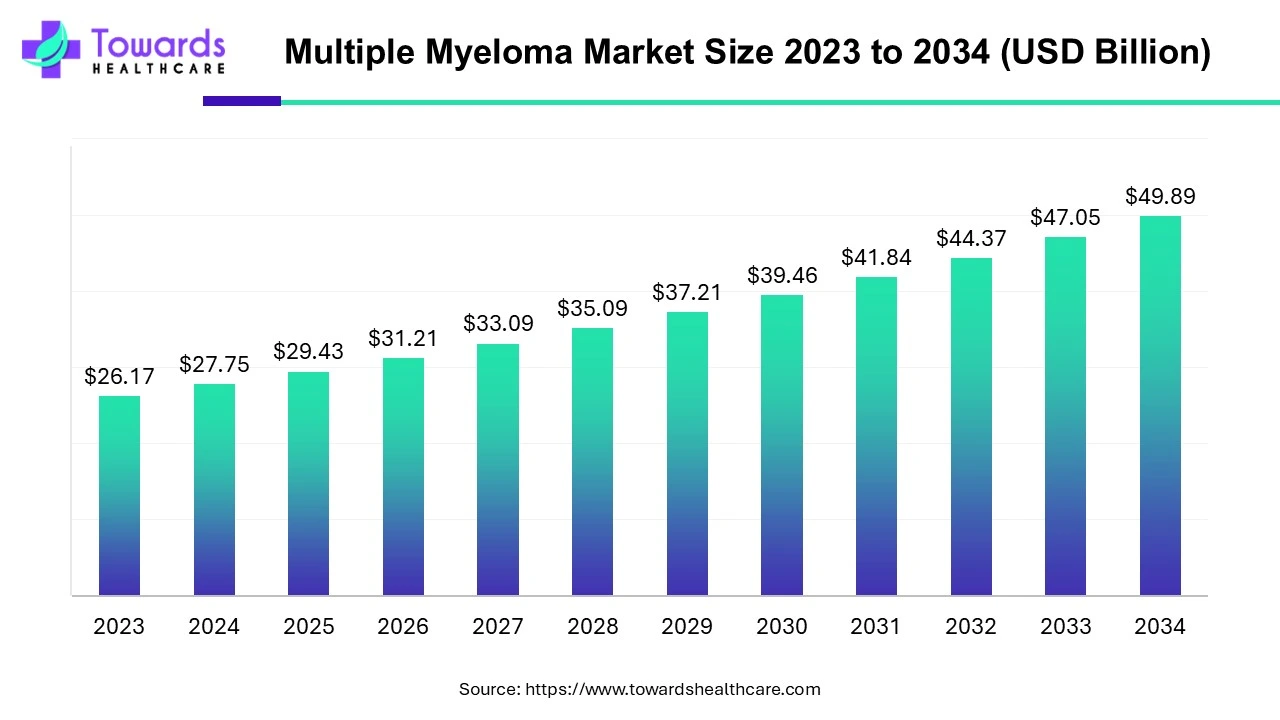

The global multiple myeloma market is valued at USD 27.75 billion in 2024, projected to rise to USD 29.43 billion in 2025, and expected to reach USD 49.89 billion by 2034, expanding at a CAGR of 6.04% (2025–2034). Growth is driven by the rising prevalence of multiple myeloma (176,404 cases globally in 2023), increasing demand for treatments such as immunotherapies, proteasome inhibitors, CAR-T therapies, radiation therapy, and stem cell transplants, coupled with growing elderly populations.

Download the free sample and get the complete insights and forecasts report on this market @ https://www.towardshealthcare.com/download-sample/5489

Table of Contents

ToggleMarket Size

Global Baseline & Case Load (Context for size)

➤2023 global incidence reported: 176,404 cases.

➤Prevalence growth fuels demand for long-term therapies and supportive care; prevalence > incidence because myeloma is being managed chronically.

2024 Market Value Composition (USD 27.75B)

➤Therapeutic revenue (largest share): immunomodulators (maintenance & first line), proteasome inhibitors, monoclonal antibodies, CAR-T.

➤Support services & procedures: autologous stem cell transplant procedures, plasmapheresis, radiation therapy revenue lines included.

➤Diagnostics & monitoring: costs from imaging, bone marrow tests, MRD (minimal residual disease) assays factor into total market.

2025 Short-Term Projection (USD 29.43B)

➤Incremental growth due to near-term approvals and expanded label uses (e.g., sarclisa approvals in Japan & China).

➤Uptick also from hospital purchase contracts and scaling of subcutaneous formulations reducing administration cost/time.

2034 Long-Term Forecast (USD 49.89B; CAGR 6.04%)

➤Drivers that compound growth over decade: more indications for existing biologics, wider CAR-T adoption (geographic expansion), oral therapy penetration, biosimilar launches, and AI-enabled efficiencies in care and drug development.

Channel & Product Mix Effects on Size

➤Hospital pharmacy share: heavy due to complex therapies (CAR-T, IV monoclonals) — high-priced but lower volume vs oral agents.

➤Retail & online share: rising with long-term oral maintenance therapies (Revlimid, Ninlaro) and generics — higher volume, lower per-unit price but major aggregate contribution to recurring revenues.

Price vs Volume Dynamics

➤High-value, low-volume products (CAR-T, novel biologics) anchor headline market value.

➤Higher volume, lower price generic/outpatient drugs (immunomodulator generics, oral proteasome inhibitors) expand patient access and contribute to sustainable recurring revenue.

Payer & Reimbursement Influence

➤Market size sensitive to reimbursement policy changes (e.g., national formularies in Europe, Medicare/insurer policies in U.S., public programs in APAC).

➤Expanded coverage for CAR-T and first-line biologics materially increases addressable market.

Clinical Trial to Commercial Lag

➤Large clinical pipeline (1,500+ trials) implies consistent new entrants over decade — this steady pipeline sustains long-term market growth assumptions in the forecast.

Market Trends

Regulatory Momentum & Label Expansion

➤Recent approvals: Abecma (ide-cel) approval and multiple Sarclisa approvals broaden indications from relapsed/refractory to newly diagnosed or transplant-ineligible patients.

➤Explanation: Label expansions move therapies earlier in treatment lines — increases treated patient population per product and extends treatment duration, raising lifetime revenue per patient.

Shift from Acute to Chronic Disease Management

➤Myeloma increasingly seen as chronic, managed disease with long maintenance phases.

➤Consequence: sustained recurring revenue models (monthly maintenance drugs) and long-term monitoring services (MRD testing, follow-up imaging).

Rise of CAR-T & Cell Therapies (Geographic Spread)

➤CAR-T (e.g., ide-cel, other BCMA-directed therapies) matured from US-centric to approvals/NDAs beyond Mainland China (Macau, HK, Singapore) — enabling global roll-out.

➤Impact: Hospitals expand infrastructure (cell processing, apheresis), increasing capital and service revenue within hospitals.

Subcutaneous & More Convenient Formulations

➤Darzalex Faspro (subcutaneous daratumumab) increases outpatient throughput, reduces infusion time, and can lower administration costs — boosts adoption.

➤Subcut formulations improve patient convenience and hospital resource optimization.

Immunomodulator Dominance with Proteasome Inhibitor Growth

➤2024: immunomodulators dominate (lenalidomide widely used).

➤Proteasome inhibitors accelerating due to newer oral agents (ixazomib) & combination regimens — improving adherence and shifting dispensing patterns toward retail.

Growing APAC Demand due to Ageing & Infrastructure

➤China: 6.7% annual rise in incidence; India: rising cases and awareness — together increase patient pool and local R&D/market opportunities.

➤Increasing investments in oncology infrastructure accelerate uptake of advanced therapies.

Cost Pressure & Biosimilar Entry

➤Soaring costs (CAR-T > USD 350k; Revlimid USD 16k–20k/month) create incentive for biosimilars and generics — downward pricing pressure but larger volume adoption.

Public-Private Funding & Strategic Alliances

➤Blackstone–Sanofi EUR 300M risk-sharing for subcutaneous Sarclisa — indicates trend to de-risk big launches and accelerate development/commercial rollout.

➤Such alliances mobilize capital for trials and market access programs.

AI & Data-Driven Care Adoption

➤Use cases include predictive treatment response, trial recruitment optimization, and patient monitoring — shown to reduce unnecessary maintenance therapy in ~30% of patients per one study (Hospital 12 de Octubre-CNIO & California Hospital).

➤Immediate effect: better resource allocation and potential cost reduction.

Heightened Clinical Trial Activity

➤1,500+ active trials worldwide (2023) covering immunotherapies, bispecifics, CAR-T — ensuring a robust pipeline and continual new approvals over coming years.

AI’s Role in Multiple Myeloma Market

Early & More Accurate Diagnosis

Subpoints:

➤AI models analyze imaging (MRI, PET/CT) and lab trends to flag early bone lesions and M-protein changes.

➤Enables earlier intervention and staging refinement (smoldering vs active disease).

➤Implication: earlier therapy initiation may prolong progression-free survival and increase lifetime therapy revenues.

Predictive Response Modeling (Precision Therapy)

Subpoints:

➤Algorithms integrate genomic, cytogenetic, and baseline health data to predict responders vs non-responders to specific drugs (e.g., proteasome inhibitors).

➤Can stratify patients for maintenance vs observation.

➤Implication: improves clinical outcomes, reduces unnecessary drug exposure (study showed potential to remove maintenance in 30% of patients), optimizes drug spend.

Optimized Clinical Trial Design & Recruitment

Subpoints:

➤ML identifies eligible patients faster from EHRs, matching molecular profiles to trials.

➤Simulated trial arms and adaptive trial design accelerate go/no-go decisions.

➤Implication: reduces trial timelines and costs; increases success rate of targeted therapies.

Real-Time Treatment Monitoring & Dose Adjustment

Subpoints:

➤Continuous data from labs and wearable devices fed into AI for adverse event early-warning.

➤AI recommends dose adjustments to minimize toxicity (e.g., for CAR-T or chemo combos).

➤Implication: lowers hospital readmissions, improves safety profile and patient throughput.

Prognostic Modeling & MRD Interpretation

Subpoints:

➤Advanced models distinguish clinically meaningful minimal residual disease (MRD) signals vs noise.

➤Helps determine treatment cessation or escalation decisions.

➤Implication: personalizes treatment length, potentially reducing long-term drug exposure and side effects.

Drug Discovery & Repurposing

Subpoints:

➤AI screens molecular libraries to discover small molecules, bispecific constructs, or repurpose drugs impacting myeloma pathways (e.g., EP300/CBP inhibitors like OPN-6602 concept).

➤Prioritizes candidates with higher predicted safety/efficacy profiles.

➤Implication: shortens preclinical cycles and de-risks clinical candidates.

Cost Optimization & Payer Analytics

Subpoints:

➤Health-economic models powered by AI forecast long-term cost-effectiveness of new regimens for payers.

➤Helps pharma design value-based pricing and risk-sharing agreements (e.g., Blackstone–Sanofi style deals).

➤Implication: increases access by aligning price to outcomes.

Workflow Automation for Cell Therapy Manufacturing

Subpoints:

➤ML optimizes manufacturing parameters for autologous CAR-T (cell expansion, viability checks).

➤Reduces batch failures and turnaround time from apheresis to infusion.

➤Implication: increases CAR-T scalability and lowers per-patient manufacturing cost.

Adverse Event Prediction for High-Risk Therapies

Subpoints:

➤Predict cytokine release syndrome (CRS) and neurotoxicity risk in CAR-T recipients using baseline biomarker signatures.

➤Guides preemptive supportive care and ICU resource allocation.

➤Implication: reduces severe toxicity incidence and improves safety data for regulators/payers.

Patient Engagement & Remote Care

Subpoints:

➤AI chatbots for adherence reminders, triage for side effects, and remote symptom tracking (fatigue, bone pain).

➤Aggregated data feeds clinician dashboards to prioritize interventions.

➤Implication: improves adherence to maintenance regimens, reduces dropouts from long treatment courses.

Regional Insights in Multiple Myeloma Market

A. North America — Market Leader (Detailed)

United States

Subpoints:

➤Incidence: 35,780 new cases (2024 data cited).

➤Infrastructure: Rapid adoption of CAR-T and novel biologics; major clinical trial centers.

➤Reimbursement: Medicare/private payers shape access; value-based contracts emerging for expensive therapies.

➤Explanation: High per-patient spend + large patient base = dominant revenue share.

Canada

Subpoints:

➤Conditional approvals (e.g., Abecma) speed adoption.

➤Public healthcare increases bargaining power but may slow uptake due to cost containment and HTA reviews.

➤Explanation: Universal coverage can facilitate equitable access but requires robust pharmacoeconomic justification.

B. Asia-Pacific — Fastest Growing & Heterogeneous

China

Subpoints:

➤Incidence rising at ~6.7% per year; aging population.

➤Growing local R&D and manufacturing; regulatory accelerations.

➤Explanation: Large patient pool + investments → major growth potential.

India

Subpoints:

➤Incidence estimated 2–3 per 100,000; regional hotspots in South & West.

➤Challenges: affordability, oncology infrastructure gaps in rural areas.

➤Explanation: Market growth dependent on awareness, diagnostics expansion and cost-effective therapies.

Japan

Subpoints:

➤MOH approval of Sarclisa+VRd marks stronger frontline options.

➤High average age at diagnosis supports demand for easy-to-administer regimens.

➤Explanation: Rapid uptake of approved therapies due to strong health system and reimbursement.

C. Europe — Mature Market with Strong Reimbursement

Germany

Subpoints:

➤Robust public funding of oncology R&D (BMBF).

➤Reimbursement environment supports high access for innovative therapies.

➤Explanation: High per-capita spend and clinical trial activity sustain market value.

France & UK

Subpoints:

➤France: 5,400 new cases/year; strong INCa programs.

➤UK: NICE evaluation critical for access timing.

➤Explanation: Health technology assessments (HTAs) determine timing & scale of market uptake.

D. Latin America — Emerging but Fragmented

Brazil

Subpoints:

➤Growing trial hubs (INCA) and public/private investments.

➤Reimbursement disparities across regions.

➤Explanation: Market expansion possible with public-private partnerships.

Mexico

Subpoints:

➤Cancer policies aim to reduce economic burden; room for improved screening and access initiatives.

➤Explanation: Policy shifts can accelerate market growth.

E. Middle East & Africa (MEA) — Selective Growth

Gulf States (UAE/Saudi Arabia)

Subpoints:

➤Investment in oncology centers enables access to advanced therapies.

➤Smaller patient pools but high per-patient spend.

➤Explanation: Potential for premium market segments (medical tourism).

South Africa

Subpoints:

➤Advanced centers in metro areas; access limited regionally.

➤Public health constraints limit widespread adoption of ultra-expensive therapies.

Market Dynamics

Drivers

Increasing Prevalence & Ageing

➤Aging populations in North America, Europe, APAC raise incidence and prevalence → more patients needing chronic care.

Therapeutic Innovation

➤Novel modalities (CAR-T, bispecifics, new monoclonals) create new treatment lines and indications.

Orphan & Accelerated Approvals

➤Regulatory incentives (ODD) accelerate development and commercialization for rare cancer therapies.

Clinical Trial Proliferation

➤1,500+ active trials keep pipeline robust and continuous approvals likely.

Convenience & Oral Agent Expansion

➤Oral proteasome inhibitors & oral small molecules shift treatment to outpatient settings, increasing adherence.

Restraints

Extreme Treatment Costs

➤CAR-T > USD 350k; monthly maintenance like Revlimid USD 16k–20k; creates access barriers and budget shocks for payers.

Complex Administration Requirements

➤CAR-T and many biologics require specialized infrastructure, trained staff, and monitoring — limits rapid scale-up in emerging markets.

Regulatory/HTA Hurdles

➤Stringent health economics reviews can delay reimbursement and market entry in cost-sensitive markets.

Side-Effect Burden

➤Toxicities (CRS, infections) increase supportive care costs and resource utilization.

Opportunities

Biosimilars & Generics

➤Reduce cost burden and expand affordability, particularly for maintenance therapies.

AI & Personalized Medicine

➤Targeted treatment reduces wasted spend and can support outcomes-based pricing.

Emerging Market Penetration

➤APAC & LATAM present large, underpenetrated patient pools; infrastructure investments open new revenue streams.

Value-Based Contracts & Risk Sharing

➤Innovative payer-pharma agreements can align pricing with real outcomes, fostering adoption.

Threats & Challenges

Price Regulation & Cost Containment

➤Governments may impose price controls or restrict access to high-cost therapies.

Manufacturing & Supply Chain Risks

➤Autologous cell therapies depend on complex supply chains; disruptions can limit patient treatment.

Competition & Rapid Obsolescence

➤New entrants and faster, cheaper alternatives may rapidly erode incumbent revenue streams.

Top 10 Companies

Bristol Myers Squibb (BMS)

➤Key product(s): Abecma (ide-cel) (BCMA CAR-T).

➤Overview: Leader in CAR-T commercialization and oncology R&D.

Strengths:

➤Strong CAR-T manufacturing and distribution capabilities.

➤Deep clinical pipeline and trial network.

Strategic notes:

➤Early mover advantage in BCMA space; success depends on scaling manufacturing and lowering cost per infusion.

Janssen Pharmaceuticals (Johnson & Johnson)

➤Key product(s): Daratumumab (Darzalex Faspro) (subcutaneous daratumumab).

➤Overview: Established hematology oncology portfolio with broad clinical adoption.

Strengths:

➤First subcutaneous daratumumab formulation increases outpatient reach.

➤Global commercial footprint and payer relationships.

Strategic notes:

➤Subcut format reduces infusion burden; competitive edge in convenience-driven adoption.

Sanofi SA

➤Key product(s): Isatuximab (Sarclisa).

➤Overview: Anti-CD38 therapy with multiple approved regimens and global ambitions.

Strengths:

➤Strong global clinical development and partnerships (e.g., Blackstone financing).

➤Rapid label expansions (frontline approvals in Asia).

Strategic notes:

➤Risk-sharing partnerships (Blackstone) signal willingness to innovate commercial models to scale access.

Novartis

➤Key product(s): CAR-T portfolio (Kymriah historically).

➤Overview: Large oncology R&D engine with CAR-T experience.

Strengths:

➤Established manufacturing know-how; global regulatory relationships.

Strategic notes:

➤Focus on next-gen cell therapies and combination regimens.

Amgen Inc.

➤Key product(s): Kyprolis (carfilzomib) (proteasome inhibitor).

➤Overview: Strong proteasome inhibitor expertise and oncology sales force.

Strengths:

➤Well-established molecules, experience in combination regimens.

Strategic notes:

➤Proteasome inhibitor leadership positions Amgen to capture growth as that class expands.

Takeda Pharmaceutical

➤Key product(s): Velcade (bortezomib), Ninlaro (ixazomib).

➤Overview: Core strengths in proteasome inhibitors; global reach.

Strengths:

➤First mover in proteasome inhibitors; strong hospital relationships.

Strategic notes:

➤Oral Ninlaro supports retail channel growth and long-term maintenance revenue.

AbbVie

➤Overview: Growing hematology oncology portfolio and biologics capability.

Strengths:

➤Large commercial organization and experience with monoclonal antibodies.

Strategic notes:

➤Potential to leverage immunology expertise into myeloma space.

AstraZeneca

➤Overview: Expanding into hematology via immuno-oncology and collaborations.

Strengths:

➤R&D scale, strong alliance capabilities.

Strategic notes:

➤Likely to partner or acquire niche players to accelerate presence.

Pfizer

➤Overview: Broad oncology footprint and strategic R&D collaborations.

Strengths:

➤Large global reach and commercialization muscle.

Strategic notes:

➤Potential to launch combination regimens leveraging partner pipelines.

Johnson & Johnson (Parent)

➤Overview: Janssen operates hematology offerings; parent company provides scale.

Strengths:

➤Strong clinical data, manufacturing and global distribution networks.

Strategic notes:

➤Cross-company synergies between oncology divisions give competitive advantages.

Latest Announcements

July 30, 2024 — Darzalex Faspro Approval (with VRd)

➤Context: Injectable daratumumab (subcutaneous) authorized with bortezomib, lenalidomide, dexamethasone for patients who qualify for autologous stem cell transplantation.

Impact:

➤Reduces infusion time versus IV daratumumab; improves patient throughput.

➤Drives adoption in frontline and peri-transplant settings.

Downstream effects:

➤Hospitals optimize infusion center schedules; payer contracts adjust to regimen cost/benefit.

Sept 20, 2024 — Sarclisa (Isatuximab) Approval (with VRd)

➤Context: Approval for non-transplant eligible patients in a frontline combination.

Impact:

➤Expands anti-CD38 class into a broader first-line population.

➤May compete with daratumumab-based regimens — fosters pricing and outcomes comparisons.

Downstream effects:

➤Potential head-to-head real-world data studies; accelerated planning for subcutaneous formulations.

2025 Regulatory Notices & Orphan Designations

➤FDA untitled letter to Edenbridge/Dexcel Pharma (Hemady promotion issues) — indicates regulatory vigilance on promotional claims.

➤Opna Bio’s OPN-6602 orphan designation — signals new small molecule entrants targeting epigenetic regulators (EP300/CBP).

Impact:

➤Regulatory enforcement can affect commercial messaging and market trust; ODDs attract investment and fast development paths.

Recent Developments

March 2025 — FDA Untitled Letter to Edenbridge/Dexcel

➤Issue: Promotional deficiencies for Hemady (oral dexamethasone formulation).

Explanation:

➤Compliance lapses may delay market penetration and invite scrutiny; demonstrates FDA oversight even for established compounds in new formulations.

February 2025 — OPN-6602 Orphan Designation

➤Issue: Orphan Drug status for EP300/CBP inhibitor indicates interest in epigenetic targets in myeloma.

Explanation:

➤Orphan designation can facilitate expedited development and potential exclusivity periods — attractive for investors and can shape competitive pipeline.

Geographic NDA Approvals

➤Equecabtagene Autoleucel NDA acceptance in Macau (and approvals in HK & Singapore).

Explanation:

➤Shows CAR-T commercialization beyond Mainland China — accelerating global availability and adoption in Asia.

Strategic Financing & Risk Sharing

➤Blackstone–Sanofi EUR 300M for subcutaneous Sarclisa development underscores financial innovation to spread development risk and speed commercialization.

Segments Covered

By Drug Class

Immunomodulators

➤Examples: Lenalidomide (Revlimid), Thalidomide.

➤Role: First-line, maintenance; strong evidence base and long-term usage.

➤Economic note: High maintenance spend due to chronic use.

Proteasome Inhibitors

➤Examples: Bortezomib (Velcade), Carfilzomib (Kyprolis), Ixazomib (Ninlaro).

➤Role: Backbone in combination regimens; shifting to oral options (ixazomib) increases outpatient management.

➤Clinical note: Effective in bortezomib-sensitive disease; next-gen agents targeting resistance emerging.

Anti-CD38 Monoclonal Antibodies

➤Examples: Daratumumab (Darzalex), Isatuximab (Sarclisa).

➤Role: Broad utility in frontline and relapsed settings; subcutaneous formulations enhancing uptake.

➤Economic note: High per-dose cost but strong clinical efficacy.

Alkylating Agents

➤Role: Often used in conditioning for stem cell transplant and in older regimens; lower cost but important in certain protocols.

CAR-T & Cell Therapies

➤Role: High-value, indication for relapsed/refractory patients; expanding into earlier lines with new data.

➤Economic/operational note: Requires specialized manufacturing and hospital infrastructure.

Others

➤Small molecules (e.g., EP300/CBP inhibitors), bispecific antibodies, and adjunctive supportive care (bisphosphonates).

By Distribution

Hospital Pharmacies

➤Role: Administer high-complexity therapies, supportive infusions, and inpatient monitoring.

➤Advantage: Controlled environment for safety & complex logistics.

Retail Pharmacies & Drug Stores

➤Role: Dispense oral therapies, maintenance medications; closer to patients for adherence initiatives.

➤Trend: Fastest growing due to oral agent expansion.

Online Pharmacies

➤Role: Home delivery for maintenance therapies and generics; convenience factor increasing for chronic myeloma population.

Top 5 FAQs

Q1. What is the market size of multiple myeloma in 2024 and forecast for 2034?

-

2024: USD 27.75 billion → 2034: USD 49.89 billion (CAGR 6.04%).

Q2. Which region dominates the multiple myeloma market?

-

North America in 2024; Asia-Pacific fastest growth.

Q3. Which drug class segment dominates the market?

-

Immunomodulators dominated in 2024; proteasome inhibitors growing fastest.

Q4. What is the biggest challenge in the multiple myeloma market?

-

High treatment cost (CAR-T > USD 350k, Revlimid USD 16k–20k/month).

Q5. How is AI transforming multiple myeloma care?

-

AI enables early diagnosis, personalized therapy, clinical trial efficiency, and cost reduction

Access our exclusive, data-rich dashboard dedicated to the healthcare market – built specifically for decision-makers, strategists, and industry leaders. The dashboard features comprehensive statistical data, segment-wise market breakdowns, regional performance shares, detailed company profiles, annual updates, and much more. From market sizing to competitive intelligence, this powerful tool is one-stop solution to your gateway.

Access the Dashboard: https://www.towardshealthcare.com/access-dashboard

Immediate Delivery Available | Buy This Premium Research @ https://www.towardshealthcare.com/price/5489

About Us

Towards Healthcare is a leading global provider of technological solutions, clinical research services, and advanced analytics, with a strong emphasis on life science research. Dedicated to advancing innovation in the life sciences sector, we build strategic partnerships that generate actionable insights and transformative breakthroughs. As a global strategy consulting firm, we empower life science leaders to gain a competitive edge, drive research excellence, and accelerate sustainable growth.

Become a valued research partner with us – https://www.towardshealthcare.com/schedule-meeting

You can place an order or ask any questions, please feel free to contact us at sales@towardshealthcare.com

Powering Healthcare Leaders with Real-Time Insights: https://www.towardshealthcare.com/healthcare-intelligence-platform

Europe Region – +44 778 256 0738

North America Region – +1 8044 4193 44

APAC Region: +91 9356 9282 04

Web: https://www.towardshealthcare.com

Find us on social platforms: LinkedIn | Twitter | Instagram | Medium | Pinterest