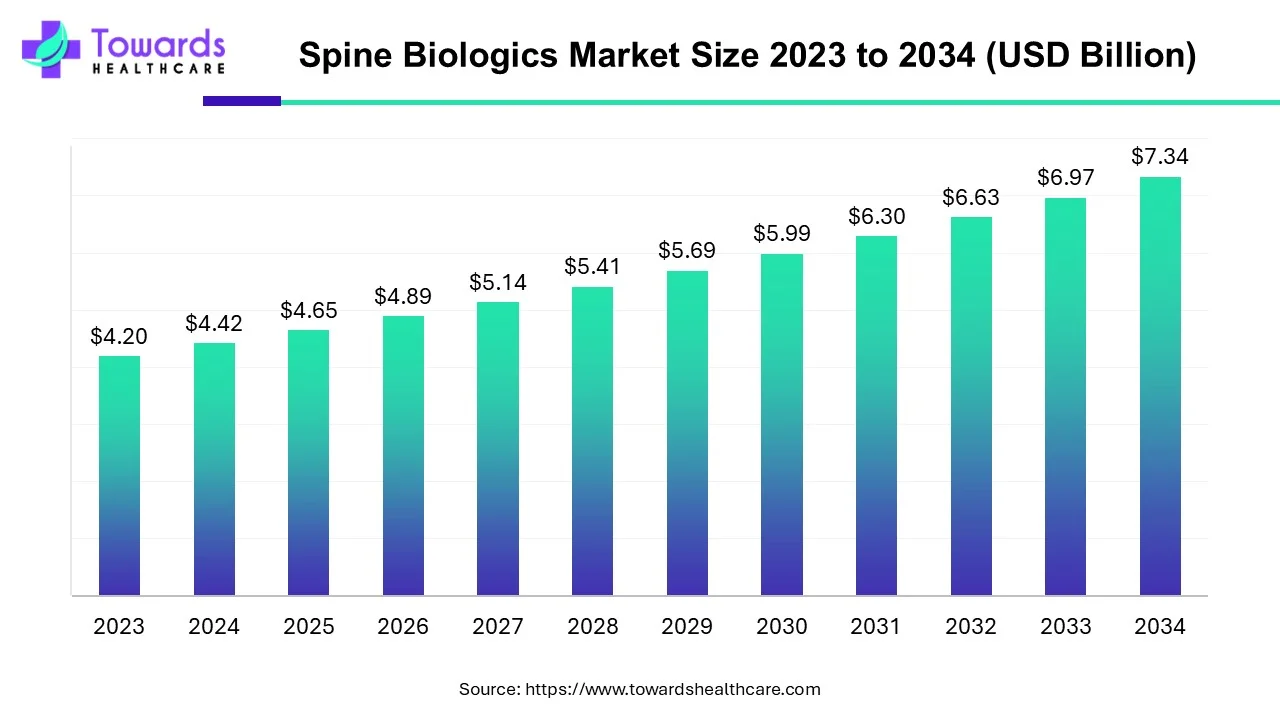

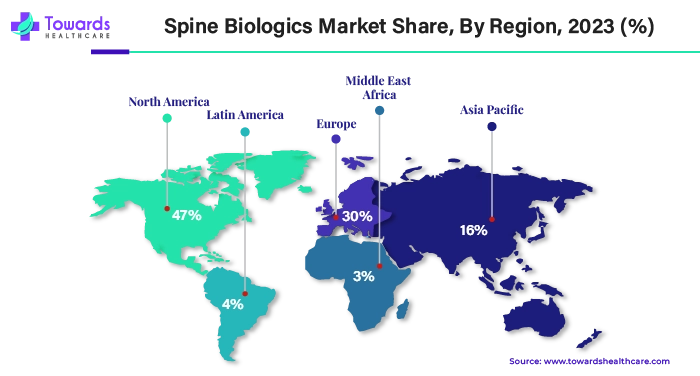

The global spine biologics market is projected to grow at a CAGR of 5.20% from USD 4.65 billion in 2025 to USD 7.34 billion by 2034. This growth is driven by increasing spinal illnesses, advancements in bone grafting technologies, and the rising demand for biologics that offer enhanced healing and recovery. North America leads the market with 47% market share in 2023, while Asia Pacific is expected to grow at the fastest rate. The spinal allografts segment dominated the market in 2023, and hospitals are the primary end-users.

Download Free Sample of Spine Biologics Market Now and Get the Complete Report Easily at: https://www.towardshealthcare.com/download-sample/5191

Market Size

2023 Market Share by Region:

North America: 47% of the market share.

Asia Pacific: Expected to grow at the fastest rate during the forecast period.

Europe, Latin America, and MEA: Show steady growth, particularly in the UK, Germany, and India.

Product Breakdown (2023):

Spinal Allografts: Dominated the market in 2023.

Bone Grafts & Substitutes, BMP, and Synthetic Bone Grafts: Holding significant shares, with strong growth expected in the coming years.

End-Use Breakdown (2023):

Hospitals: Dominated the market as the primary care setting.

Outpatient Facilities: Expected to grow rapidly from 2024-2033 due to cost-effectiveness and efficient care options.

Projected Market Growth (2025-2034):

From USD 4.65 billion in 2025 to USD 7.34 billion by 2034.

Market Trends

Rising Incidence of Spine Disorders:

The increasing prevalence of spinal disorders such as degenerative disc disease and spinal fractures is driving the demand for biologics.

Aging populations, sedentary lifestyles, and job-related risks contribute to higher incidences of spinal conditions.

Technological Advancements:

3D printing and nanotechnology are improving bone regeneration methods.

The development of bioactive materials and stem cell therapies for spine repair is transforming orthopedic surgery.

Shift Towards Minimally Invasive Surgeries (MIS):

MIS techniques are gaining traction for treating spinal disorders due to faster recovery times and reduced patient complications.

Regenerative Treatments:

There is increasing demand for spinal biologics such as stem cell therapies and growth factor treatments to support tissue regeneration.

Focus on Biologics Over Traditional Bone Grafts:

Spinal biologics offer significant advantages over traditional methods (autografts and allografts) due to better safety profiles and enhanced healing properties.

Favorable Healthcare Policies:

Government support in regions like North America and Europe, including reimbursement policies for biologic treatments, is encouraging market growth.

AI Impact or Role in Spine Biologics Market

Advanced Diagnostics:

AI-driven diagnostic tools can help in early detection of spinal conditions, leading to better-targeted biologic treatments.

Predictive Analytics for Treatment Outcomes:

AI can analyze patient data to predict the effectiveness of specific biologic treatments, leading to personalized care.

Robotic-Assisted Surgeries:

AI-powered robotic systems can assist in spinal surgeries, enhancing precision in biologic implants, especially in minimally invasive procedures.

AI in Biomaterial Development:

AI can accelerate the design of new biomaterials for spine regeneration by simulating and testing the effectiveness of different materials.

AI in Drug Discovery:

AI is playing a role in discovering and optimizing new biologic drugs, including growth factors, that target spinal repair.

Smart Implants and Devices:

AI-enabled implants that monitor healing and adjust biologic drug delivery to enhance recovery are emerging in the market.

AI in Rehabilitation:

AI-based rehabilitation tools can assess patient recovery and recommend adjustments to biologic treatment plans based on real-time data.

Supply Chain Optimization:

AI helps in forecasting demand, improving production logistics, and ensuring the timely delivery of biologic implants and materials.

AI in Research & Development:

AI algorithms analyze vast amounts of data from clinical trials and scientific literature, accelerating the R&D process for new biologic therapies.

AI-Powered Patient Monitoring:

Wearable AI devices can monitor patients’ recovery post-surgery and track biologic treatment progress, offering real-time updates to healthcare providers.

Regional Insights

North America:

North America:

Market Share: 47% (2023).

Key Drivers: High patient base, advanced healthcare infrastructure, rapid adoption of new technologies.

Growing Prevalence: Increasing incidence of spinal cord injuries (SCI) and degenerative spine conditions.

Example: The U.S. has about 335 million people and sees approximately 18,000 new traumatic spinal cord injury cases annually.

Asia Pacific:

Fastest Growing Region: Driven by a large patient population and improving healthcare systems.

Key Growth Factors: Rising spinal injuries from accidents, increasing awareness of biologics, growing healthcare infrastructure, and rising obesity rates due to sedentary lifestyles.

Key Countries: India shows the highest growth, with more than 200,000 spinal injury cases annually.

Europe:

Market Growth: Germany and the UK are leading due to rising demand for biologic treatments and strong healthcare R&D investments.

Key Trend: Germany’s aging population and high spinal injury rates are pushing the demand for spine biologics.

Market Dynamics

Drivers:

Increasing spinal diseases and degenerative conditions.

Advancements in regenerative medicine (e.g., stem cells, 3D printing).

Growth in the adoption of minimally invasive surgical procedures.

Restraints:

Allograft Limitations: Risk of infection (HBV, HCV) and loss of osteogenic potential due to sterilization.

Opportunities:

3D Printing & Nanotechnology: Opportunities to create more effective and safer biologics.

Rising Demand in Emerging Markets: Rapidly developing healthcare sectors in regions like APAC are creating new growth opportunities.

Threats:

Regulatory challenges and complexities in biologic approval.

High cost and complex production of biologics compared to traditional treatments.

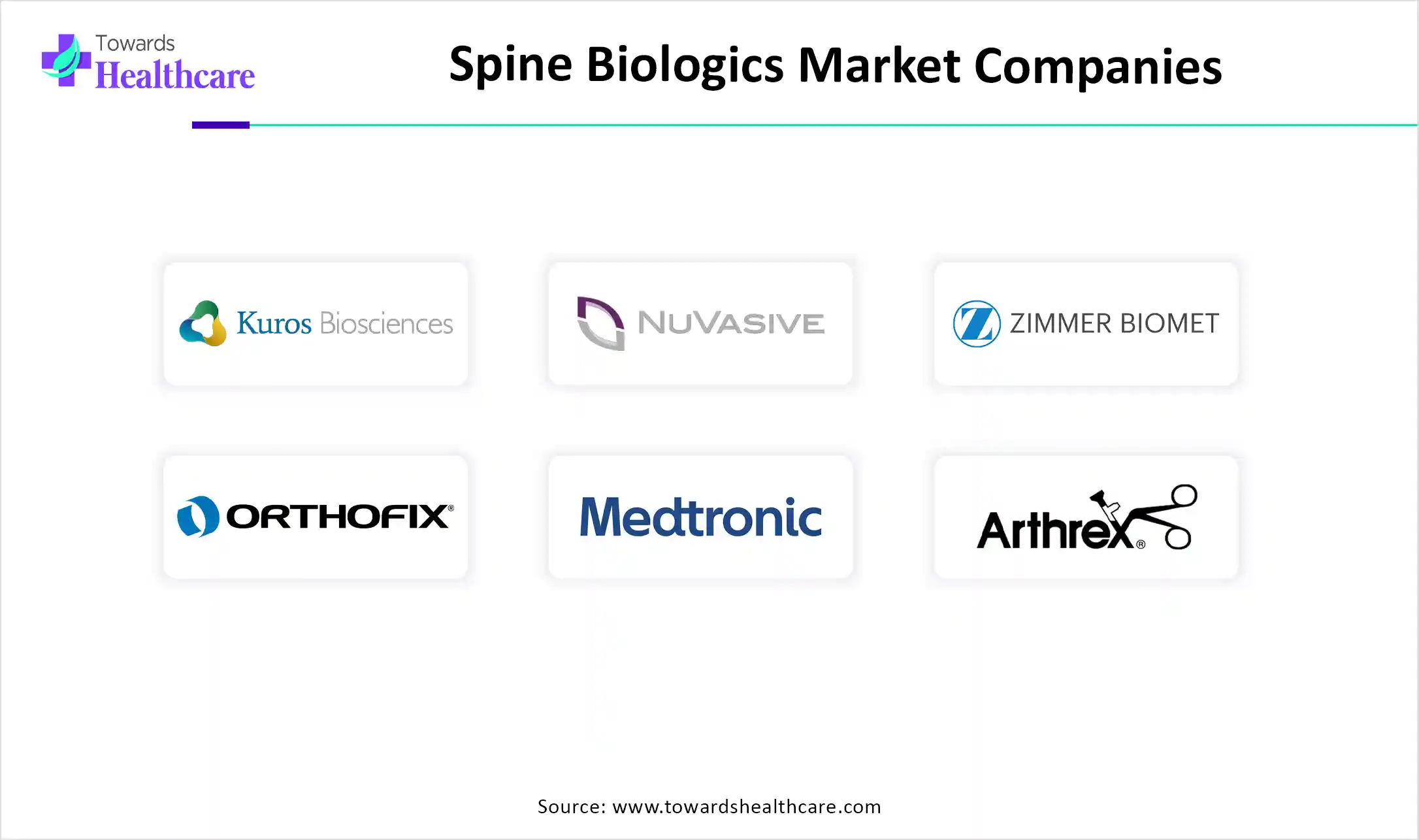

Top 10 Companies in Spine Biologics Market

Kuros Biosciences:

Product: Biologics for bone healing.

Strength: Innovative biomaterial products for regenerative medicine.

NuVasive, Inc.:

Product: Spine biologics and surgical products.

Strength: Advanced technology in spine surgeries.

Zimmer Biomet:

Product: Spine fusion devices and biologics.

Strength: Strong product portfolio and R&D.

Orthofix:

Product: Bone grafting solutions and biologics.

Strength: Strong focus on regenerative medicine.

DePuy Synthes (Johnson & Johnson):

Product: Bone grafting substitutes, biologics.

Strength: Market leader with extensive global reach.

Medtronic:

Product: Spine biologics and fusion technologies.

Strength: Extensive R&D, including acquisitions like Nanovis.

Arthrex, Inc.:

Product: Spine biologics and minimally invasive surgical instruments.

Strength: Innovative orthobiologic products.

Exactech, Inc.:

Product: Bone biologics for spine treatments.

Strength: Advanced technology in orthopedic devices.

Biocomposites:

Product: Bone regeneration products.

Strength: Focus on cutting-edge biologics.

Organogenesis Inc.:

Product: Regenerative biologic solutions for spine and other orthopedic treatments.

Strength: Focus on tissue regeneration.

Recent Developments

Bone Biologics (March 2024): Launched a $2 million initial public offering to fund clinical studies and R&D.

Biocomposites (January 2024): Renovos Biologics’ BMP-2 received FDA Breakthrough Device Designation.

Medtronic (February 2025): Acquired Nanovis’ Adaptix PEEK interbody system, enhancing spine biologic options.

Orthofix (October 2023): Launched OsteoCoveTM, an innovative bioactive synthetic graft for spinal surgeries.

Segments Covered in the Spine Biologics Market

By Product:

Spinal Allografts:

Definition: Spinal allografts are bone grafts sourced from donors (living or deceased) and are processed to maintain sterility. They are often used in spinal fusion surgeries, where they provide support and promote healing.

Sub-segments:

Machined Bones Allograft: These are bone grafts that have been processed and shaped for use in surgeries.

Demineralized Bone Matrix (DBM): A processed form of bone that has undergone demineralization, leaving behind a matrix that can promote bone growth and repair. DBMs are often used for spinal fusion and regeneration.

Advantages:

Readily available from donors.

No need for additional surgery to harvest the graft from the patient’s own bone (autograft).

Osteoconductive, helping bone to grow and repair.

Challenges:

Limited osteogenic potential due to the sterilization process.

Risk of infections (e.g., HBV, HCV) due to the donor origin.

Lower effectiveness in promoting bone regeneration compared to autografts.

Market Share: In 2023, spinal allografts held the largest share of the market, owing to their long-standing use in spinal surgeries and relatively easy availability.

Bone Morphogenetic Proteins (BMPs):

Definition: BMPs are proteins that play a key role in bone formation and healing. They are used to stimulate bone growth and are often employed in spinal fusion surgeries where bone regeneration is needed.

Types:

Recombinant BMPs (e.g., BMP-2, BMP-7) are used for spinal applications and have been found to improve healing rates.

Advantages:

Strong osteoinductive properties, encouraging new bone formation.

Can help achieve spinal fusion without the need for additional bone grafting.

Challenges:

High cost compared to traditional bone grafts.

Potential for side effects, such as unwanted tissue growth.

Market Trends: BMPs are gaining traction in spinal surgeries due to their superior healing properties and have seen increased approval in the U.S. and European markets.

Synthetic Bone Grafts:

Definition: Synthetic bone grafts are man-made materials designed to mimic the function of natural bone in spinal fusion surgeries. They are often made from materials such as hydroxyapatite, calcium phosphate, and bioactive glass.

Types:

Hydroxyapatite: A naturally occurring mineral form of calcium apatite.

Calcium Phosphate: A material with similar properties to human bone.

Bioactive Glass: A material that can bond to bone and stimulate new bone formation.

Advantages:

Biocompatible and osteoconductive, supporting bone healing and growth.

No need for donor tissue, eliminating the risk of rejection or infection.

Challenges:

May not be as effective in promoting bone regeneration as autografts or BMPs.

Some synthetic grafts may not fully integrate with the surrounding bone.

Market Trends: Synthetic bone grafts are growing in popularity due to their cost-effectiveness and reduced risk of complications compared to autografts and allografts.

Cell-based Matrices:

Definition: These are biologic scaffolds made from natural or synthetic materials that contain live cells to promote bone regeneration and healing. These matrices are used to support the growth of new bone tissue.

Types:

Stem Cell-Based Matrices: Matrices that incorporate stem cells to help regenerate bone tissue.

Collagen-based Matrices: Typically derived from natural sources and used as a scaffold for cells to grow.

Advantages:

Support both osteoconductive and osteoinductive properties, promoting bone growth and healing.

Can be customized to suit individual patient needs.

Challenges:

High manufacturing cost.

Ethical and regulatory concerns regarding the use of stem cells.

Market Trends: Cell-based matrices are on the rise due to their ability to promote faster and more effective healing, making them a valuable tool in spinal biologics.

By End-Use:

Hospitals:

Definition: Hospitals are the primary settings where complex spinal surgeries, including those requiring biologics for bone healing, are performed.

Market Share: The hospital segment dominated the spine biologics market in 2023.

Trends:

Increasing preference for biologic solutions in complex surgeries.

High demand for cutting-edge technologies and treatments, such as stem cell therapies and advanced bone grafting materials.

Growth Drivers:

Hospitals are the centers of advanced care and have the infrastructure for specialized surgeries like spinal fusion.

Surgeons prefer hospitals for complicated procedures due to the availability of specialized tools, surgical teams, and intensive care units.

Ambulatory Surgical Centers (ASCs):

Definition: ASCs are outpatient facilities that provide same-day surgical care. These centers handle less complex spinal surgeries compared to hospitals.

Growth Trends:

The ASC segment is expected to grow rapidly from 2024 to 2033 due to the increasing demand for minimally invasive surgeries (MIS) and outpatient care.

ASCs offer a cost-effective alternative to hospital stays, leading to their increasing adoption.

Market Dynamics:

ASCs are becoming popular for patients seeking quicker recovery times and lower costs for less complicated spinal procedures.

As the preference for minimally invasive spinal surgeries rises, ASCs are expected to capture a larger share of the biologics market.

Outpatient Facilities:

Definition: These are facilities where patients can receive treatment and be discharged on the same day. They include specialized orthopedic and spine clinics.

Market Trends:

The outpatient facilities segment is anticipated to grow rapidly from 2024 to 2033 due to an increasing focus on non-invasive treatments and cost-effective care.

Advantages:

Outpatient treatments are often faster, less expensive, and involve shorter recovery times compared to traditional hospital procedures.

Challenges:

Some spine surgeries require more advanced care, which may not be available in outpatient settings.

By Region:

North America:

Market Share: North America accounted for 47% of the global market in 2023, making it the dominant region.

Key Drivers:

High incidence of spinal cord injuries (SCI) and degenerative spinal conditions.

Strong healthcare infrastructure, with a wide adoption of new technologies.

Well-established reimbursement policies for biologic treatments.

Market Trends:

Increased adoption of minimally invasive spinal fusion techniques.

Rapid advancements in stem cell therapy and 3D printing technologies.

Example: The U.S. is expected to see approximately 18,000 new traumatic spinal cord injury cases annually.

Europe:

Key Markets: Germany, UK, France, and Italy are leading in the European spine biologics market.

Growth Drivers:

An aging population leading to higher incidences of degenerative spinal diseases.

Government policies favoring the use of biologics for spine treatment.

Trends:

Research and development activities related to spinal biologics are prominent in Europe, with significant investments in biotechnology.

Asia Pacific (APAC):

Market Growth: The APAC region is expected to grow at the fastest rate due to an expanding healthcare market and increasing awareness about spinal biologics.

Key Drivers:

Rapid urbanization, leading to a higher incidence of lifestyle-related diseases, including obesity and sedentary lifestyles, which are contributing to spinal injuries.

Growing healthcare infrastructure and improving access to advanced medical technologies.

Market Trends:

Surge in demand for biologics due to rising awareness among surgeons and patients about their benefits in spine treatments.

Example: India has a significant rise in spinal injuries, with over 200,000 cases reported annually.

Latin America:

Market Growth: Latin America is experiencing steady growth due to improvements in healthcare infrastructure and rising incidences of spinal disorders.

Key Markets: Brazil and Mexico.

Challenges:

High cost of biologics may limit accessibility in some parts of the region.

Middle East & Africa (MEA):

Market Growth: The MEA region is seeing gradual growth, primarily driven by healthcare advancements and a growing awareness of spinal disorders.

Key Trends:

Increasing use of biologics for spine surgeries in countries with developing healthcare systems, such as the UAE and Saudi Arabia.

Top 5 FAQs

1 What are the main drivers of growth in the spine biologics market?

Increasing spinal disorders, advanced regenerative technologies, and demand for minimally invasive surgeries.

2 Which region is dominating the spine biologics market?

North America, with a market share of 47% in 2023.

3 What are the key challenges in the spine biologics market?

High cost of biologic treatments, regulatory hurdles, and limited clinical data for certain biologic therapies.

4 What is the role of 3D printing in spine biologics?

It allows the creation of customizable and bioactive materials for bone regeneration.

5 Which companies are leading the spine biologics market?

Medtronic, Zimmer Biomet, DePuy Synthes, Orthofix, and NuVasive are some of the leading companies.

Access our exclusive, data-rich dashboard dedicated to the therapeutic area sector – built specifically for decision-makers, strategists, and industry leaders. The dashboard features comprehensive statistical data, segment-wise market breakdowns, regional performance shares, detailed company profiles, annual updates, and much more. From market sizing to competitive intelligence, this powerful tool is one-stop solution to your gateway.

Access the Dashboard: https://www.towardshealthcare.com/access-dashboard

Checkout Spine Biologics Market Report Now at: https://www.towardshealthcare.com/checkout/5191

Become a valued research partner with us – https://www.towardshealthcare.com/schedule-meeting

You can place an order or ask any questions, please feel free to contact us at sales@towardshealthcare.com

Powering Healthcare Leaders with Real-Time Insights: https://www.towardshealthcare.com/healthcare-intelligence-platform

Europe Region – +44 778 256 0738

North America Region – +1 8044 4193 44

APAC Region: +91 9356 9282 04

Visit Our Website: https://www.towardshealthcare.com

Find us on social platforms: LinkedIn | Twitter | Instagram | Medium | Pinterest