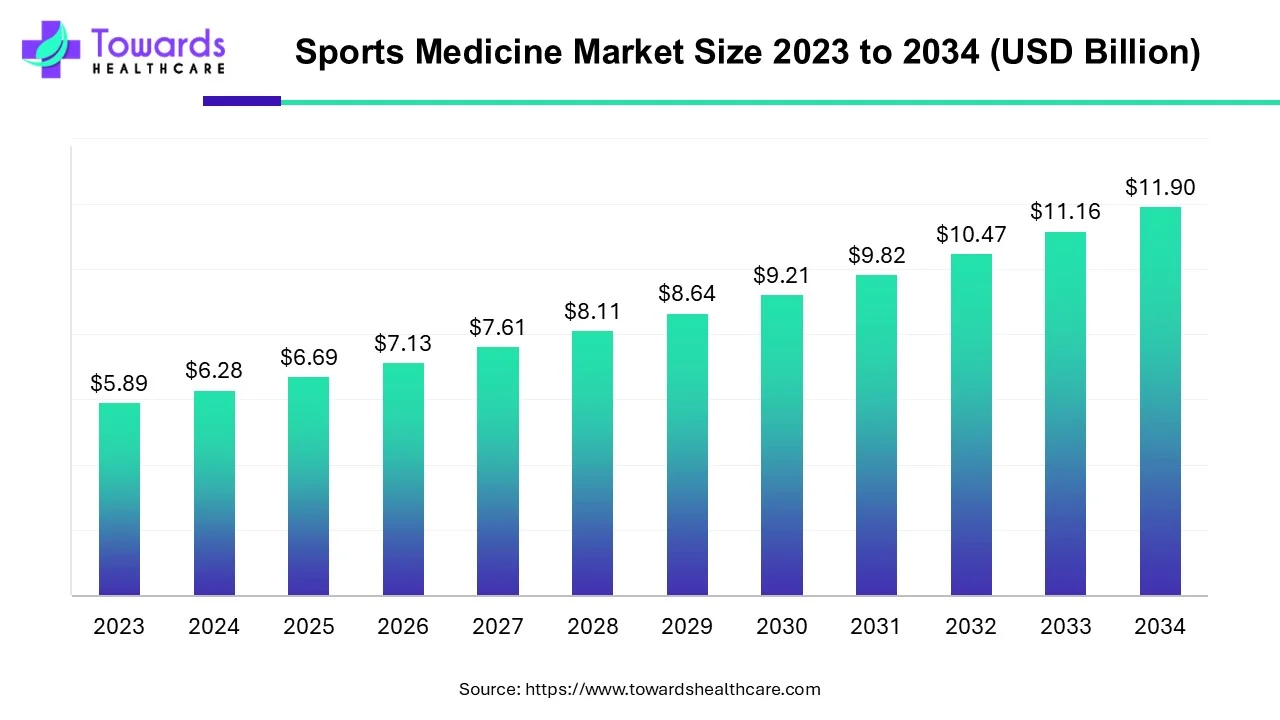

The global sports medicine market is set to expand from USD 6.69 billion in 2025 to USD 11.90 billion by 2034 (CAGR 6.6%), propelled by high injury incidence (e.g., 3.5 million U.S. injuries/year; 725 injuries and 1,119 illnesses at Beijing 2022) and strong demand for body reconstruction solutions (41% share in 2023) and knee-injury care (32% share in 2023), with North America at 42% share (2023).

Download the free sample and get the complete insights and forecasts report on this market @ https://www.towardshealthcare.com/download-sample/5107

Market size (deep, point-wise)

Baseline & horizon

➣2025: USD 6.69 B (model base year provided).

➣2034: USD 11.90 B at 6.6% CAGR.

Year-by-year trajectory (CAGR 6.6%)

➣2025: 6.69 B

➣2026: 7.13 B

➣2027: 7.60 B

➣2028: 8.10 B

➣2029: 8.64 B

➣2030: 9.21 B

➣2031: 9.82 B

➣2032: 10.46 B

➣2033: 11.16 B

➣2034: 11.90 B

Incremental value creation

➣Absolute addition 2025→2034: USD 5.21 B.

➣Mid-horizon (2029–2031) adds USD 1.18 B as installed robotics, orthobiologics, and rehab tech scaling kicks in.

Volume drivers mapped to value

➣Injury burden: U.S. 3.5 M injuries/year; Johns Hopkins notes >3.5 M injuries in under-14s with 775k ER visits—sustains high utilization of braces, arthroscopy, and ligament repair.

➣Elite events & surveillance data: Beijing 2022 reported 2.4% injuries and 3.1% illnesses among participants—evidence base pushing prevention & rapid-return protocols.

➣Participation tailwinds: U.S. 242 M people (80% aged ≥6) engaged in sport/fitness in 2023; EU sports employment 1.55 M (0.76% of total) supports service capacity growth.

Market trends

Shift to reconstruction & minimally invasive

➣Body reconstruction products led with 41% share (2023); continued mix-shift to arthroscopy, soft-tissue repair (e.g., ACL repair kits) and patient-specific implants.

Knee remains the epicenter

➣32% of market tied to knee injuries (2023); adoption of robotic-assisted TKA (e.g., Mako), advanced ACL repair systems, and AI-guided rehab pathways.

Robotics & navigation scaling

➣>1,000 Mako robots deployed by 2021 enabling >500k procedures; 2023 launch of Mako Total Knee 2.0 adds analytics + haptics; accelerates premium procedure mix.

Wearables & continuous monitoring mainstream

➣WHOOP Strap 4.0 (2023) and smart textiles inform load management, return-to-play decisions, and payer-acceptable outcomes tracking.

Orthobiologics & regenerative medicine

➣Rising use of PRP and stem-cell-based protocols to complement surgical repair, shortening recovery windows for tendons/ligaments.

Tele-sports-medicine & hybrid rehab

➣Remote consults, app-based PT, and AI triage widen access—critical for youth and community athletics with high injury incidence.

Pediatric & adolescent focus

➣FDA-cleared pediatric solutions (e.g., Arthrex TightRope for kid ACLs) mirror high injury rates in <14 cohort; tailored protocols growing.

Institutional expansion

➣New centers (e.g., Ochsner Andrews Institute 2024; Delhi Sports Injury Center 2024) expand multidisciplinary capacity.

Policy & programs fueling activity

➣U.S. President’s Council on Sports, Fitness & Nutrition renewed through Sept-2025; Canada’s Sport Canada investments; China’s Healthy China 2030 ISM strategy; India athlete welfare funds—all stoke participation and care demand.

Cost pressure & affordability innovation

➣With doctor visits USD 100–200, imaging USD 500–2,000, surgeries USD 5k–50k+, providers push value-based bundles, outpatient ASC shift, and digital-first rehab to contain OOP spend.

AI’s role & impact

➣Injury risk prediction: Models blend workload (GPS, wearables), biomechanics, sleep, and prior injuries to calculate individual risk; flags overtraining before tissue failure.

➣Imaging triage & precision diagnosis: AI on MRI/CT/US detects meniscal tears, rotator-cuff pathology, stress fractures; reduces reading times and variability; speeds surgical planning.

➣Robotics optimization: Intra-op AI refines implant alignment and soft-tissue balance (e.g., haptic envelopes + analytics in robotic TKA) → better function, fewer revisions.

➣Personalized rehab: Computer-vision verifies home-exercise form; adaptive protocols adjust intensity; digital twins simulate healing trajectories.

➣Return-to-play decision support: Multivariate thresholds (strength symmetry, hop tests, proprioception, GPS metrics) algorithmically scored to reduce re-injury risk.

➣Tele-PT automation: Chat- and voice-based “PT copilots” deliver cues, adherence nudges, pain-flare routing; lowers therapist load and expands access.

➣Surgical workflow analytics: OR video + instrument telemetry mined to benchmark steps, reduce operative time, and standardize training.

➣Orthobiologics response modeling: Predicts which patients benefit from PRP vs. grafts; optimizes injection timing and dosing windows.

➣Population health & prevention: School and club data lakes surface hot spots (e.g., turf injuries); guide rule changes, gear mandates, and targeted prehab.

➣Revenue cycle & value proof: Auto-extracted outcomes (PROMs, activity data) support payer authorization and bundled-payment justification; reduces denials.

Regional insights

North America (42% share in 2023)

Subpoints

➣Infrastructure density: High concentration of sports medicine institutes, ASCs, and team-affiliated clinics enables rapid referral and advanced care (robotics, arthroscopy).

➣Procedure premiumization: Strong uptake of robotic TKA/THA, advanced ACL repairs, and orthobiologics increases ASPs and case complexity.

➣Participation base: 242 M active participants (2023) sustain steady injury-driven demand; youth sports a major funnel.

➣Implication: Largest revenue pool; payers drive outcomes-based models and remote rehab to manage costs.

Europe

Subpoints

➣Workforce scale: 1.55 M employed in sports sector (2023) underpins multidisciplinary services.

➣Elite club integration: Pro leagues embed on-site imaging/rehab, pushing fast-track protocols into community care.

➣Access parity focus: Public systems emphasize prevention and post-op rehab adherence to reduce re-injury rates.

➣Implication: Stable demand with strong prevention budgets and structured rehab pathways.

Asia Pacific

Subpoints

➣Participation surge: Urbanization + mega-events expand amateur sport; culturally diverse needs (cricket, martial arts) diversify injury patterns.

➣Policy catalysts: China’s ISM / Healthy China 2030 integrates sport & medicine; India’s welfare funds provide pensions and medical support for sportspersons.

➣Capacity build-out: New centers and tele-rehab platforms scale access across metros and tier-2 cities.

➣Implication: Fastest relative growth; significant upside in wearables, tele-PT, and cost-effective implants.

Latin America

Subpoints

➣Grassroots growth: Football-led participation with rising private clinic chains.

➣Cost sensitivity: Strong demand for durable, lower-cost braces/supports and outpatient arthroscopy.

➣Implication: Value-tier products and remote coaching models win.

Middle East & Africa

Subpoints

➣Event-driven investment: Sports cities and elite academies spur top-end facilities.

➣Workforce training gap: Partnerships with global brands to upskill PT and ATC staff.

➣Implication: Early-stage but premium niches (elite rehab tourism) emerging.

Market dynamics

Drivers

➣High and rising injury incidence: U.S. 3.5 M/yr injuries; >3.5 M injuries in under-14s (775k ER visits) sustain procedure + rehab volumes.

➣Technology adoption: Robotics (Mako), AI imaging, and wearables enhance outcomes and throughput.

➣Participation boom: U.S. 242 M active; EU sports employment base; APAC policy pushes.

Restraints

➣Cost barriers: Visits USD 100–200, imaging USD 500–2,000, surgeries USD 5k–50k+; delays care (Commonwealth Fund noted 41% adults deferred care over cost).

➣Stigma & delayed presentation: Athletes fearing bench time postpone treatment, complicating cases.

➣Workforce variability: Shortages of pediatric sports specialists in many regions.

Opportunities

➣ASC shift & same-day surgery: Lowers cost, increases capacity.

➣Tele-sports-medicine: Extends specialist reach; payer-friendly remote rehab.

➣Regenerative protocols & pediatric solutions: Address large unmet need cohorts (youth ACL, tendinopathy).

Contextual evidence

➣Beijing 2022 surveillance and WHOOP/robotics adoption illustrate tech-enabled prevention and faster recovery.

➣Institutional expansions in 2024 (U.S., India) increase addressable capacity.

Top 10 Key Players and Company Profile

Stryker Corporation

Products: Mako SmartRobotics (incl. Total Knee 2.0), arthroscopy tools, soft-tissue and ligament repair, trauma systems.

Overview: Ortho and med-tech leader with installed robotic base >1,000 by 2021; expanding analytics-driven joint workflows.

Strengths: Robotics leadership, haptic guidance, data analytics ecosystem, ASC penetration.

Smith & Nephew

Products: Arthroscopy (shoulder/knee), ligament repair implants, sports biologics, negative pressure wound therapy.

Overview: Strong sports medicine franchise across soft-tissue and arthroscopy with education platforms.

Strengths: Surgeon training depth, broad soft-tissue portfolio, global reach.

Zimmer Biomet

Products: Identity Shoulder System (FDA-cleared 2022), knee/hip systems, sports medicine accessories.

Overview: Recon powerhouse diversifying into shoulder and sports indications.

Strengths: Recon brand trust, shoulder platform innovation, distribution.

Johnson & Johnson MedTech (DePuy Synthes)

Products: Extremities, fixation, soft-tissue repair; expanded via CrossRoads Extremity Systems acquisition (2022).

Overview: Full-line ortho with growing foot/ankle presence.

Strengths: Scale, M&A integration, comprehensive hospital relationships.

Arthrex

Products: ACL Repair TightRope & SwiveLock ACL Repair Kit (FDA 2023), extensive arthroscopy and sports implants.

Overview: Sports medicine pure-play renowned for rapid innovation and surgeon education.

Strengths: First-to-market pediatric ACL approvals, broad procedure sets, KOL engagement.

Enovis (DJO Global)

Products: Bracing/supports, PT equipment; DynaClip bone staples (2023) for foot & ankle.

Overview: Bracing to surgical solutions with strong rehab footprint.

Strengths: End-to-end continuum (support → surgery → rehab), ASC-friendly economics.

Performance Health Holding Inc.

Products: Rehabilitation equipment, therapeutic modalities, tape, and clinical supplies.

Overview: Core supplier to PT/ATC settings across collegiate and community sports.

Strengths: Wide catalog, recurring consumables, training-room penetration.

Bauerfeind AG

Products: High-end braces, compression, orthoses for knee/ankle/back.

Overview: Premium support & recovery brand used by elite athletes.

Strengths: Product quality, athlete endorsements, clinical efficacy credentials.

Mueller Sports Medicine

Products: Braces, tapes, supports, and accessories.

Overview: Value-to-mid market focus with broad retail visibility.

Strengths: Affordability, breadth, grassroots reach.

Ochsner Andrews Orthopedics & Sports Medicine (provider)

Products/Services: Multidisciplinary surgical, PT, and performance services; new Acadiana facility (2024).

Overview: Integrated care model linking elite protocols to community access.

Strengths: Clinical brand equity, comprehensive continuum, regional expansion model.

Latest announcements

2025 | Modern Sports Medicine & Wellness (MSMW) × NeuralCure AI

➣What: Strategic partnership to embed AI (predictive analytics, diagnostics enhancement, treatment simulations).

➣Why it matters: Operationalizes AI across triage→plan→rehab, improving throughput and personalization, especially for non-surgical orthobiologics and telehealth.

2024 | Ochsner Andrews Institute – Acadiana

➣What: 14,000-sq-ft dedicated physical therapy & sports medicine facility.

➣Impact: Adds capacity for multidisciplinary rehab; supports ASC-linked care pathways.

2024 | India Center for Sports Injury (South Delhi)

➣What: 20-bed tertiary center with advanced ortho & rehab tech.

➣Impact: Strengthens APAC access; platform for youth-injury protocols.

Recent developments

Arthrex (2023): FDA clearance for TightRope implant; first pediatric ACL repair tools approved—expands addressable pediatric segment.

Stryker (2023): Mako Total Knee 2.0 with 3D CT planning, haptics, analytics—elevates outcomes vs. manual surgery.

Enovis/DJO (2023): DynaClip Quattro/Delta bone staples—efficiency in foot/ankle fixation.

Zimmer Biomet (2022): Identity Shoulder System—modularity across shoulder arthroplasty indications.

DePuy Synthes (2022): Acquired CrossRoads Extremity Systems—strengthens foot/ankle solutions.

Stryker (2021): >1,000 Mako robots in hospitals; >500k procedures—proof of robotic scale.

WHOOP (2023): Strap 4.0—personalized training insights for prevention/return-to-play.

WOA × FIMS (2021): Joint projects for Olympian long-term health; global health study infrastructure.

Segments Covered

By Product

1. Body Reconstruction

➣Scope: Orthopedic implants, fracture/ligament repair products, arthroscopy devices, soft-tissue repair systems, prosthetics, and orthobiologics.

In-depth analysis:

Market dominance:

➣Accounted for 41% of the total market in 2023, making it the largest product category.

➣Growth driven by rising incidence of ACL/MCL tears, rotator cuff injuries, and shoulder dislocations among both professional and amateur athletes.

Technological advancements:

➣Adoption of robotic-assisted surgical systems such as Stryker’s Mako SmartRobotics and AI-based preoperative planning enhances surgical precision.

➣Arthrex’s TightRope ACL Repair Kit and SwiveLock system offer minimally invasive repair options, reducing rehabilitation time.

➣Increasing use of biologics (PRP, stem cells) to improve healing and tissue regeneration post-surgery.

Growth drivers:

➣Growing participation in sports (242 million U.S. participants aged 6+ in 2023).

➣Expanding orthopedic surgery centers and ambulatory surgical facilities.

➣Rising acceptance of prosthetics and custom-fit implants using 3D printing and bioresorbable materials.

Outlook (2025–2034):

➣Expected to maintain its lead with high-single-digit growth, supported by continuous innovation, shorter hospital stays, and value-based surgical care models.

2. Body Support & Recovery

➣Scope: Braces, supports, compression wear, physiotherapy (PT) equipment, thermal therapy systems, electrostimulation, and other recovery aids.

In-depth analysis:

Market share:

➣Second-largest segment, projected for steady mid-single-digit CAGR through 2034.

➣Driven by increased focus on injury prevention and rehabilitation-based therapies post-surgery.

Technological progress:

➣Smart braces with embedded sensors monitor patient mobility, load, and progress.

➣Electrostimulation and cryotherapy devices used for faster recovery post-surgery or muscle fatigue.

➣Compression wear increasingly used by professional athletes for circulation enhancement and fatigue reduction.

Market dynamics:

➣Rising number of physiotherapy centers and home-based rehab solutions.

➣Growing demand among non-professional and fitness enthusiasts, not just elite athletes.

Digital physiotherapy tools integrating AI and telehealth for remote guidance and recovery tracking.

Outlook:

➣Key growth area due to affordability, accessibility, and expansion of preventive sports medicine programs in schools, universities, and community fitness centers.

3. Accessories & Other Products

➣Scope: Bandages, tapes, disinfectants, wraps, and other sports accessories.

In-depth analysis:

Role in market:

➣Essential low-cost consumables ensuring continuity of care in training rooms, physiotherapy centers, and field-side medical setups.

➣High-volume, recurring demand due to daily use and disposable nature.

Innovation trends:

➣Development of eco-friendly and hypoallergenic tapes, biodegradable wraps, and anti-microbial disinfectant sprays.

➣Digital inventory management systems used by sports clubs to maintain continuous stock.

Market characteristics:

➣Low-margin, high-volume business model.

➣Dominated by Mueller Sports Medicine, Performance Health, and Bauerfeind.

➣Increasing penetration through online retail and subscription-based supply chains.

Outlook:

➣Stable market growth; sustainability and hygiene-based innovations will strengthen this segment’s position.

By Injury Type

1. Knee Injuries (32% in 2023)

In-depth analysis:

Dominant category representing one-third of global revenue.

➣Rising prevalence of ACL/MCL tears and meniscal damage due to intense physical activities and professional sports.

Technological landscape:

Robot-assisted total knee arthroplasty (TKA) systems like Mako 2.0 enable precision and faster recovery.

➣Pediatric ACL repair tools (Arthrex TightRope) now FDA-approved, expanding patient demographics.

➣Use of orthobiologics such as PRP for cartilage repair and joint preservation.

Market implication:

➣Knee reconstruction continues to dominate due to its frequency, clinical complexity, and need for post-surgical rehabilitation programs.

2. Shoulder Injuries

In-depth analysis:

➣Growing category led by sports like baseball, swimming, and weightlifting.

➣Common injuries include rotator cuff tears, labral injuries, and dislocations.

Technological enhancements:

➣Arthroscopic procedures replacing open surgeries, ensuring faster return-to-play.

➣Development of modular shoulder implants (e.g., Zimmer Biomet’s Identity Shoulder System).

➣Regenerative solutions—tissue patches, biologic scaffolds—speed tendon healing.

Outlook:

➣Expected to grow steadily, supported by increased awareness among aging athletes and postural correction programs.

3. Foot & Ankle, Back & Spine, Hip & Groin, and Others

In-depth analysis:

Foot & Ankle:

➣Rising due to overuse injuries and sprains; DJO/Enovis’ DynaClip bone staples simplify fixation and recovery.

➣Growing podiatric clinics and outpatient care models in developed countries.

Back & Spine:

➣Sports-related lower back pain and disc injuries drive demand for non-invasive therapies, electrostimulation, and physiotherapy.

➣PT-based conservative management dominates.

Hip & Groin:

➣Increasing arthroscopy for femoroacetabular impingement (FAI) and labral tears.

➣Rehabilitation tools and targeted training to restore mobility.

Other injuries:

➣Include elbow (tennis elbow), wrist (carpal strains), and head trauma management (protective gear).

By End User

1. Hospitals

In-depth analysis:

Role:

➣Handle complex reconstruction surgeries and multi-injury trauma cases.

➣Equipped with integrated imaging, surgical robotics, and intensive post-surgery rehabilitation departments.

Trends:

➣Partnerships with sports clubs and federations for exclusive athlete care.

➣Shift towards value-based care and bundled payment models.

➣Hospitals integrating AI diagnostics and tele-rehabilitation platforms.

Outlook:

➣Stable but premium segment; focus on multi-specialty collaboration and advanced surgical systems.

2. Ambulatory Surgical Centers (ASCs)

In-depth analysis:

Role:

➣Ideal for same-day arthroscopy, ligament repair, and minimally invasive surgeries.

➣Offer cost-efficient operations with shorter recovery periods.

Market influence:

➣Preferred by insurers for lower overhead costs compared to hospitals.

➣Adoption of modular surgical trays and compact robotics systems for efficiency.

➣Surge in private equity investments in ASC networks.

Outlook:

➣Fastest-growing end-user segment due to the global push for outpatient and same-day surgery models.

3. Physiotherapy Centers & Others

In-depth analysis:

Role:

➣Core of post-injury rehabilitation and long-term conditioning.

➣Integration of digital PT apps, motion-tracking systems, and AI-guided exercise regimens.

Trends:

➣Expansion of tele-physiotherapy and home-based recovery services post-COVID.

➣Wearable tech (WHOOP, smart garments) used for continuous performance monitoring.

➣Increasing collaboration between physiotherapists, orthopedic surgeons, and sports trainers for holistic care.

Outlook:

➣Expected to witness high growth with expansion of preventive healthcare programs and remote rehabilitation technology.

By Geography

1. North America (42% share in 2023)

In-depth analysis:

Market leader with advanced healthcare infrastructure, high sports participation, and widespread insurance coverage.

Key drivers:

➣242 million people actively involved in sports/fitness.

➣High rate of sports injuries (~3.5 million/year).

➣Presence of top players like Stryker, Zimmer Biomet, Arthrex, and DJO Global.

Outlook:

➣Maintains dominance due to strong R&D investments and adoption of robotics and telemedicine.

2. Europe

In-depth analysis:

➣Strong sports culture and public healthcare integration.

➣1.55 million people employed in the sports sector (0.76% of total EU employment).

➣Collaboration with sports federations enhances preventive programs.

➣Increasing use of rehabilitation technologies and orthopedic implants supported by public insurance systems.

Outlook:

➣Moderate but steady growth, driven by rising investments in athletic injury prevention and recovery programs.

3. Asia Pacific

In-depth analysis:

➣Fastest-growing region, supported by urbanization, government sports initiatives, and growing middle-class interest in fitness.

Country specifics:

➣China: “Healthy China 2030” integrates medicine and sports (ISM program).

➣India: National funds provide pensions and medical support for sportspersons; new centers like the 2024 Sports Injury Center in Delhi.

Trends:

➣Surge in local manufacturing of braces and PT equipment.

➣Telemedicine and wearable diagnostics adoption to bridge rural-urban gaps.

Outlook:

➣Double-digit CAGR potential; strong opportunities in affordable rehabilitation and orthobiologics.

4. Latin America

In-depth analysis:

➣Emerging market with growing sports participation and rising sports medicine awareness.

➣Demand driven by football-related injuries and a rise in fitness clubs.

➣Focus on low-cost braces, bandages, and outpatient physiotherapy setups.

Outlook:

➣Value-based growth driven by affordability and regional manufacturing partnerships.

5. Middle East & Africa

In-depth analysis:

➣Early-stage but promising due to sports tourism, high-profile events, and government funding for elite athlete care.

➣Gulf countries investing in sports cities and orthopedic centers.

➣Partnerships with U.S. and European healthcare providers for skill transfer and training.

Outlook:

➣High growth potential in premium rehabilitation services and specialized orthopedic care.

Top 5 FAQs

-

What is the market size and growth?

USD 6.69 B (2025) → USD 11.90 B (2034), 6.6% CAGR; cumulative addition ~USD 5.21 B. -

Which products lead the market?

Body reconstruction products led with 41% share (2023); arthroscopy and soft-tissue repair are key. -

What injury type dominates demand?

Knee injuries at 32% (2023); ACL/meniscus care and robotic-assisted knee procedures are major growth drivers. -

Which region is largest today?

North America with 42% (2023), supported by high participation (242 M active) and advanced facilities. -

What forces are accelerating demand?

High injury incidence (e.g., U.S. ~3.5 M/yr; children >3.5 M injuries with 775k ER visits), technology adoption (robotics, wearables, AI), and expanding specialized centers; tempered by cost barriers (visits USD 100–200, imaging USD 500–2,000, surgeries USD 5k–50k+).

Access our exclusive, data-rich dashboard dedicated to the therapeutic area sector – built specifically for decision-makers, strategists, and industry leaders. The dashboard features comprehensive statistical data, segment-wise market breakdowns, regional performance shares, detailed company profiles, annual updates, and much more. From market sizing to competitive intelligence, this powerful tool is one-stop solution to your gateway.

Access the Dashboard: https://www.towardshealthcare.com/access-dashboard

Immediate Delivery Available | Checkout this Premium Research Report @ https://www.towardshealthcare.com/checkout/5107

Become a valued research partner with us – https://www.towardshealthcare.com/schedule-meeting

You can place an order or ask any questions, please feel free to contact us at sales@towardshealthcare.com

Powering Healthcare Leaders with Real-Time Insights: https://www.towardshealthcare.com/healthcare-intelligence-platform

Europe Region – +44 778 256 0738

North America Region – +1 8044 4193 44

APAC Region: +91 9356 9282 04

Web: https://www.towardshealthcare.com

Find us on social platforms: LinkedIn | Twitter | Instagram | Medium | Pinterest