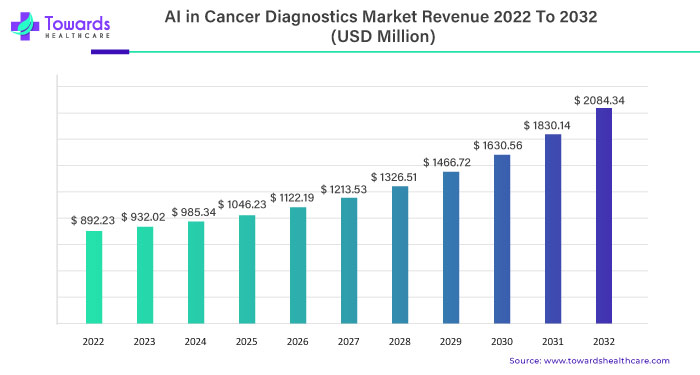

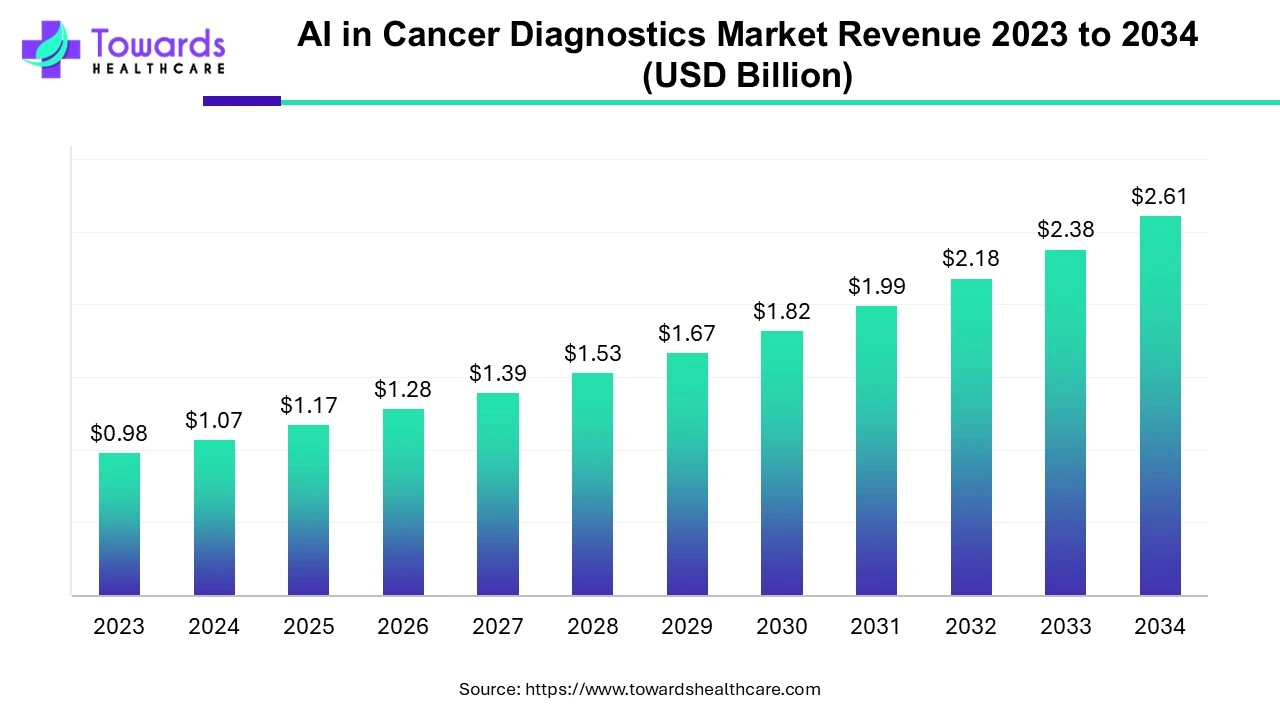

The global AI in cancer diagnostics market was USD 1.07 billion in 2024 and is forecast to reach USD 2.61 billion by 2034 (CAGR 9.35%), propelled by rising cancer incidence, expanding software solutions, and rapid adoption in hospitals and imaging workflows.

Download this Free Sample Now and Get the Complete Report and Insights of this Market Easily @ https://www.towardshealthcare.com/download-sample/5044

Market size in AI in Cancer Diagnostics Market

●Current baseline (2024): Global market revenue USD 1.07B — this is the measured commercial value of AI products and services applied to cancer diagnostics in 2024 (software, hardware, services).

●Forecast (2034): Projected market value USD 2.61B by 2034, implying a cumulative expansion driven mainly by recurring software licensing, platform subscriptions, and growing deployments in clinical sites.

●Compound growth: Implied CAGR 9.35% (2024–2034) — steady, mid-single-digit to low-double-digit growth consistent with regulated medtech adoption cycles.

●Revenue composition (structural view): Software solutions dominate revenue share (largest contributor in 2024) with higher gross margins; hardware and services make up the remainder — hardware is capital-intensive with slower replacement cycles; services (integration, validation, maintenance) grow as deployments scale.

●Addressable market drivers: Increasing digital imaging volumes, digitization of pathology, federated data platforms (e.g., NHS Cancer 360) and new diagnostic modalities (AI-native liquid biopsies, prognostic tests) expand the addressable spend beyond imaging into multimodal diagnostics.

●Commercial cadence: Early adopter hospitals and diagnostic chains drive initial sales; widespread adoption depends on regulatory clearances, reimbursement pathways, and workflow integration.

●Price / value dynamics: Value propositions focus on time saved per case, improved sensitivity/specificity, and downstream cost avoidance (earlier staging → lower treatment cost); pricing mixes include per-case, per-study, subscription and enterprise licensing.

●Geographic weighting: North America (largest share in 2024) contributes disproportionately to revenue today; fastest CAGR expected in Asia-Pacific.

●Investment signal: Recent VC exits and series rounds (e.g., Ataraxis $4M seed/series) indicate investor appetite for AI-native diagnostics, particularly prognostic/predictive tests.

●Market maturity outlook: Market transitions from point solutions to platforms over 2024–2034 — consolidation likely as incumbents (big diagnostics and imaging vendors) scale software stacks and add regulatory-backed products.

Market trends

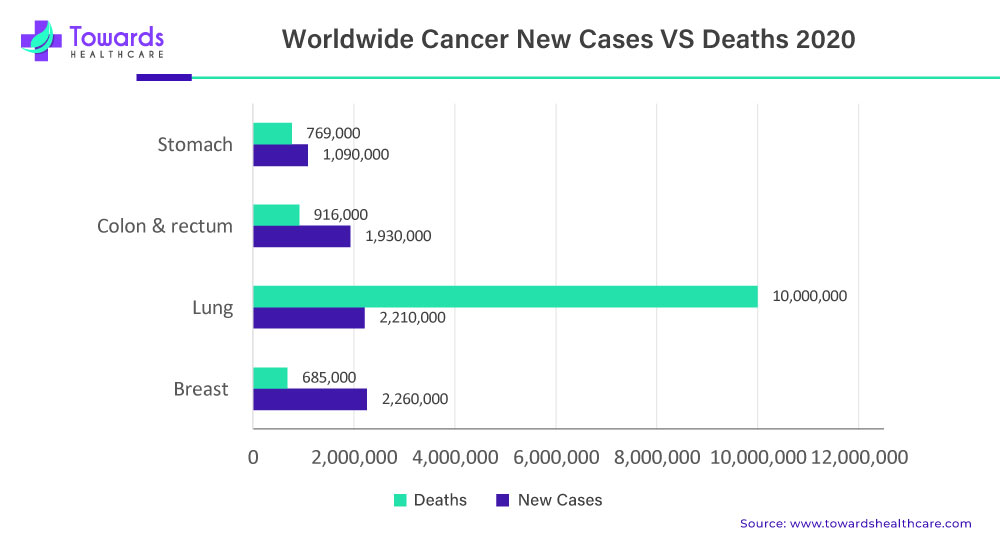

●Rising cancer incidence fuels demand: WHO data cited — ~20 million new cancer cases in 2022 and projection to 35 million by 2050; higher case volumes create urgent demand for scalable diagnostic tools.

●Software solutions dominance: In 2024 the software solutions segment held the dominant market presence; trend continues as software enables rapid algorithm updates, cloud analytics, and federated learning.

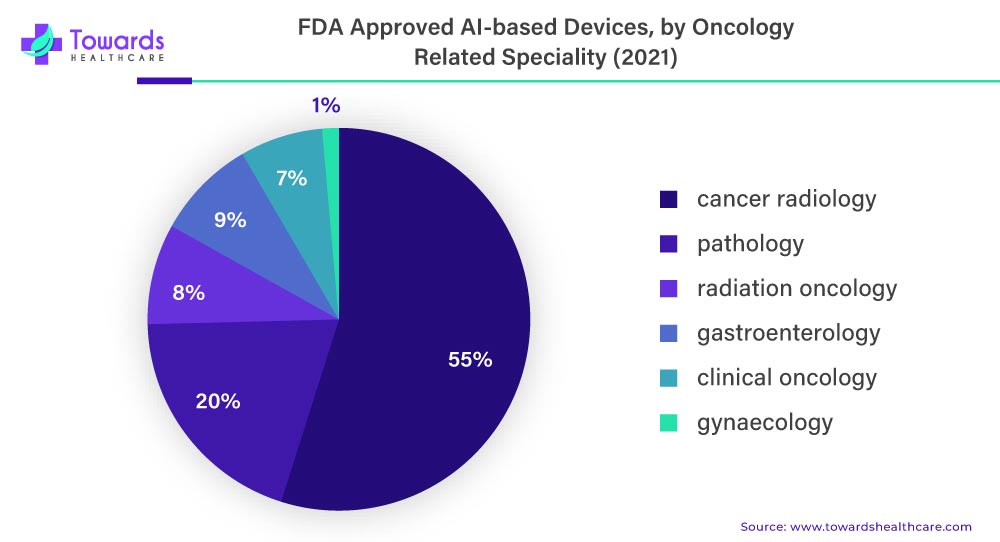

●Imaging remains primary revenue source: >75% of FDA-listed AI devices (as of July 2022 update) are used in radiology — imaging continues to generate the largest share of clinical AI deployments.

●Shift toward multimodal diagnostics: Beyond imaging, genomics and liquid biopsy AI tools are emerging (e.g., prognostic tests like Ataraxis Breast), broadening the clinical use cases and revenue channels.

●Regulatory acceleration and designations: Breakthrough Device Designations (example: Roche VENTANA TROP 2 RxDx, April 2025) speed clinical adoption and payer conversations, increasing commercial potential.

●Health system integration: Federated data platforms and integrated dashboards (e.g., NHS Cancer 360 announced May 2025) enable real-time clinician workflows and scalable rollouts across networks.

●Regional policy support: Asia-Pacific national initiatives (China R&D emphasis; India’s Ayushman Bharat digital push) and Europe’s research funding drive faster adoption in those regions.

●Investment and commercialization activity: VC funding and company launches (Ataraxis, Nov/Oct 2024 funding events) indicate active commercialization and productization cycles.

●Data availability & standardization focus: The market trend is toward pooled, standardized digital pathology and imaging datasets to improve model generalizability and fairness.

●Clinical economics emphasis: Vendors increasingly provide health-economic evidence (time saved, diagnostic yield, treatment pathway optimization) to secure procurement and reimbursement.

AI impacts / roles in AI in Cancer Diagnostics Market

Augmented image interpretation (detection & triage)

●AI pre-screens CT/MRI/mammograms to flag likely positives, prioritizing workloads for radiologists and reducing time-to-diagnosis.

●Result: faster cascade to confirmatory tests and treatment planning; improves throughput in high-volume centers.

Quantitative imaging and volumetrics

●Automated lesion segmentation, volumetric tracking and measurement reduce inter-reader variability and enable objective progression metrics.

●Result: consistent staging, better monitoring of therapy response, and improved trial endpoints.

Digital pathology & slide analysis

●Deep learning models analyze whole-slide images to detect cancer patterns, grade tumors, and quantify biomarkers.

●Result: speeds pathology workflows, surfaces subtle features unseen by the eye, and enables computational biomarkers.

Prognostic and predictive modeling

●AI integrates imaging, histology, and clinical data to predict recurrence risk, survival probabilities, or therapy response (e.g., first AI-native prognostic breast test claims).

●Result: personalized treatment triage, better patient stratification for trials and targeted therapies.

Biomarker discovery from multimodal data

●Machine learning uncovers novel radiomic/genomic signatures correlated with outcomes or therapy sensitivity.

●Result: new companion diagnostics and targets for drug development.

Workflow orchestration and decision support

●AI-driven dashboards (e.g., Cancer 360) synthesize appointments, tests, and analytics to guide clinician actions.

●Result: reduces administrative friction, closes care gaps, and shortens diagnostic timelines.

Automated report generation & structured outputs

●Natural language processing converts findings into structured reports with standardized staging and recommendations.

●Result: reduces documentation burden and improves clarity for multidisciplinary teams.

Radiation dose optimization and image enhancement

●AI algorithms reconstruct high-quality images from lower radiation/contrast exposures (e.g., PET-CT with 60% lower radiation claim), improving patient safety.

●Result: safer serial imaging and expanded screening potential.

Federated learning for cross-institutional model training

●Models train on decentralized data without sharing raw protected health information, improving generalizability while protecting privacy.

●Result: better performance across diverse populations and faster regulatory confidence.

Operational analytics and capacity planning

●AI forecasts case loads, identifies bottlenecks and predicts resource needs across cancer care pathways.

●Result: optimized staffing, faster throughput, and improved access in constrained systems.

Regional insights

North America — market leader (2024):

●Drivers: High imaging volumes, favorable reimbursement approaches, regulatory approvals (numerous FDA-cleared AI tools).

●Clinical adoption: Hospitals and large diagnostic chains are early enterprise buyers; research collaborations between tech firms and academic centers accelerate validation.

●Economic impact: Higher per-unit spend on enterprise software and services drives larger revenue share.

Asia-Pacific — fastest growth trajectory:

●Drivers: Large patient base, national AI / digital health programs (China, India), and rising private investment.

●Opportunity: Leapfrog adoption in high-throughput centers and diagnostic chains; lower per-unit price points but massive volume potential.

●Challenges: Data heterogeneity, regulatory fragmentation, and local validation requirements.

Europe — regulatory and research hub:

●Drivers: Strong government research funding, integrated health systems enabling cross-site pilots.

●Adoption pattern: Cautious but evidence-driven; emphasis on CE marking, clinical effectiveness and data privacy.

●Commercialization: Partnerships between medtech incumbents and AI startups are common.

India — diagnostics scaling & early detection need:

●Epidemiology: Low detection rates (overall 29%; 15% for breast cancer; 33% for lung cancer) underscore unmet screening and diagnostic needs.

●Initiatives: Technology-driven labs (e.g., Gurugram PET-CT with AI, May 2025) show targeted investments in high-value diagnostic capability.

●Business model: Cost-sensitive, with emphasis on point-of-care integration and public-private partnerships.

Japan — mature market with high burden:

●Epidemiology: Estimated ~979,300 cancer cases and ~393,100 deaths in 2024; high economic burden (cost > 1,024,006 million JPY), incentivizing productivity gains via AI.

●Adoption: High-quality data and established healthcare infrastructure enable rigorous clinical validation of AI tools.

Latin America, MEA — growing but fragmented:

●Drivers: Increasing awareness, regional centers of excellence; constrained budgets slow commoditized uptake.

●Strategy: Cloud-delivered, subscription models and staged pilots with major private hospitals.

Clinical specialty skew — lung & brain focus:

●Lung: Largest cancer-type revenue contributor in 2024 (WHO estimate ~2.5M new lung cancer cases annually; 12.4% of all cases).

●Brain: Fastest growth in AI interest due to diagnostic complexity and high unmet need for accurate characterization.

Market dynamics

Supply side: Vendor consolidation vs. specialization

●Major incumbents (Roche, GE, Siemens) expand via diagnostics + digital solutions; startups focus on niche prognostic or AI-native tests — consolidation pressure expected.

Demand side: Hospital procurement cycles & proof-of-value

●Buyers require clinical validation, workflow fit and health-economic justification; Cancer 360-type platforms enable system-level rollouts that simplify procurement.

Regulation & reimbursement as gating factors

●Regulatory designations (Breakthrough Device) accelerate market access; reimbursement policies determine large-scale adoption.

Data access & quality constraints

●Data standardization and federated approaches are essential to overcome privacy/legal barriers and to improve model robustness.

Capital flows & commercialization timing

●Early VC rounds (e.g., Ataraxis $4M) support product development; commercialization timelines hinge on clinical trials and regulatory clearance.

Technology maturation & product evolution

●From single-task classifiers to multimodal, explainable AI platforms — customers demand interpretability and integration into clinical decision support.

Pricing pressure & outcomes focus

●As competition grows, vendors must show measurable outcome improvements (earlier detection, reduced false positives, cost savings) to sustain pricing.

Workforce impact & task shifting

●AI reallocates human effort — radiologists/pathologists will focus on complex cases; training and change management are needed.

Interoperability & integration requirements

●Seamless EHR/PACS/ LIS integration and standard APIs become competitive differentiators.

Geopolitical & regional policy influence

●National AI strategies and data sovereignty rules shape deployment models and vendor market entry.

Top 10 companies

Roche Diagnostics

●Product/Offering: Diagnostics, tests, platforms and digital solutions (VENTANA TROP 2 RxDx example).

●Overview: Large integrated diagnostics and pharma player with broad portfolio across tests and platforms; reported CHF 60.5B total sales in 2024.

●Strength: Scale, regulatory experience (Breakthrough Device designation, April 2025), global commercial reach and integrated diagnostic pipeline.

GE Healthcare

●Product/Offering: AI-powered imaging systems and advanced therapy support for oncology diagnosis.

●Overview: Major medical technology vendor with global installed base; Q2 2025 revenue reported $5B (growth in U.S., Europe, MENA).

●Strength: Large equipment footprint enabling deep integration of AI tools into imaging hardware and enterprise service contracts.

Siemens Healthineers

●Product/Offering: Imaging platforms and digital health solutions with integrated AI modules.

●Overview: Established medtech leader positioned to bundle AI into imaging and diagnostics offerings.

●Strength: Strong hospital relationships, robust regulatory & service infrastructure, ability to scale enterprise deployments.

Paige AI

●Product/Offering: Digital pathology AI and computational biomarkers (collaboration example with Microsoft in 2023).

●Overview: Pathology-focused AI company advancing digital pathology interpretation and biomarker development.

●Strength: Domain specialization in pathology, partnerships with major tech companies for cloud and analytics scale.

PathAI

●Product/Offering: AI pathology tools for diagnosis and biomarker discovery.

●Overview: Focused on improving pathology accuracy and enabling companion diagnostics.

●Strength: Research collaborations, emphasis on model validation and clinical utility.

Ibex AI

●Product/Offering: AI diagnostics solutions for cancer detection in histology and imaging.

●Overview: Niche vendor delivering pathology and image analysis solutions for clinical workflows.

●Strength: Tailored clinical products and focused customer success for pathology labs.

Indica Labs

●Product/Offering: Digital pathology/slide analysis platforms.

●Overview: Provides tools enabling morphometric and biomarker quantitation for research and clinical use.

●Strength: Strong in analytics tooling and research partnerships.

Enlitic

●Product/Offering: Imaging AI solutions for radiology and oncology detection tasks.

●Overview: Early imaging AI company evolving into enterprise imaging analytics.

●Strength: Imaging-first expertise and ML model deployment experience in clinical settings.

Owkin

●Product/Offering: AI for biomarker discovery and predictive modeling across multimodal datasets.

●Overview: Combines clinical and molecular data science to create predictive models.

●Strength: Strong emphasis on multimodal R&D and translational biomarker footprints.

Mindpeak GmbH / SkinVision / iCAD / others

●Product/Offering: Varied — SkinVision (skin cancer screening tools), iCAD (diagnostic solutions), Mindpeak (pathology AI).

●Overview: A mix of specialty vendors focused on single-cancer types or modality niches.

●Strength: Targeted solutions, fast product iterations and focused clinical validation in their niches.

Latest announcements

India — Gurugram AI-driven PET-CT lab inauguration (May 2025)

●What: India’s first technology-driven cancer diagnostic laboratory inaugurated by Union Minister Jitendra Singh.

●Why it matters: The lab claims 60% lower radiation exposure and high-resolution AI-powered imaging (Mahajan Imaging & Labs), demonstrating an on-the-ground shift toward safer, AI-enhanced imaging in India.

●Impact: Sets a local benchmark for imaging safety and may accelerate adoption across private diagnostic chains.

NHS Cancer 360 tool announcement (May 2025)

●What: A diagnostic/clinical dashboard integrated into the NHS federated data platform (FDP) to reduce delays and present appointments, treatments and test data to clinicians.

●Why it matters: System-level integration that can rapidly accelerate AI adoption across a national health system by making AI outputs operationally useful.

●Impact: Could materially shorten time-to-treatment and increase survival rates through better care coordination.

Roche VENTANA TROP 2 RxDx — Breakthrough Device Designation (April 2025)

●What: FDA Breakthrough Device Designation for a diagnostic linked to non-small cell lung cancer (NSCLC).

●Why it matters: Regulatory recognition shortens path to market and supports clinical uptake and payer discussions.

●Impact: Strengthens Roche’s position in AI-enabled companion diagnostics for lung cancer.

Ataraxis AI — funding & product launches (Oct/Nov 2024)

●What: Came out of stealth with $4M in venture funding and launched Ataraxis Breast (AI-native prognostic/predictive test).

●Why it matters: Example of AI-native company focusing on prognostic tests rather than only detection, signaling product diversification in the market.

●Impact: Introduces new comparator for prognostic commercial tests and intensifies competition in AI-powered personalized diagnostics.

Recent developments

New AI-native prognostic tests entering clinical market: Ataraxis Breast represents first-mover AI-native prognostic/predictive offerings, shifting market value from pure detection to prognostication.

Rising regulatory approvals/designations: Roche’s designation for TROP 2 RxDx highlights a maturing regulatory pathway for AI-linked companion diagnostics.

National program integrations: NHS Cancer 360 demonstrates how federated platforms are becoming the vehicle for clinical AI scale.

Investment activity in startups: Seed/early rounds (Ataraxis $4M) show continued funding into diagnostic AI, especially for clinically differentiated, validated tests.

Local infrastructure upgrades in emerging markets: India’s AI PET-CT lab shows hardware + software integration approaches are being adopted outside traditional high-income markets.

Segments covered

By Component — Software Solutions

●Explanation: Core AI models, analytic platforms, interpretive software and reporting tools; highest revenue share due to recurring licensing and cloud services.

By Component — Hardware

●Explanation: Imaging hardware with embedded AI (PET-CT, MRI upgrades) and dedicated AI appliances; capital investment and slower refresh cadence.

By Component — Services

●Explanation: Implementation, validation, model retraining, integration and maintenance; critical for safe clinical rollouts and ongoing revenue streams.

By Cancer Type — Breast Cancer

●Explanation: High clinical and commercial interest for earlier detection and prognostic testing (e.g., Ataraxis Breast).

By Cancer Type — Lung Cancer

●Explanation: Largest revenue contributor in 2024 due to high incidence and imaging reliance (CT screening, nodule detection).

By Cancer Type — Prostate Cancer

●Explanation: AI assists MRI interpretation and biopsy targeting.

By Cancer Type — Colorectal Cancer

●Explanation: Imaging and pathology AI for polyp detection and histologic grading.

By Cancer Type — Brain Tumor

●Explanation: Fastest growth area due to diagnostic complexity and need for advanced segmentation/characterization.

By End-User — Hospital

●Explanation: Largest revenue share; hospitals possess capital, patient volumes and integration capabilities needed for enterprise AI.

By End-User — Surgical Centers & Medical Institutes

●Explanation: Fastest CAGR — growing adoption as centers invest in intraoperative imaging and diagnostics to improve surgical outcomes.

By Region — North America, Asia Pacific, Europe, Latin America, MEA

●Explanation: Regionally segmented by readiness, funding, and regulatory landscapes; North America leads, Asia-Pacific fastest growing.

Top 5 FAQs

-

Q: What is the current size and expected growth of the AI in cancer diagnostics market?

A: The market was USD 1.07B in 2024 and is forecast to reach USD 2.61B by 2034, growing at a CAGR of 9.35% (2024–2034). -

Q: Which component drives most revenue today?

A: Software solutions were the dominant component in 2024 and are expected to remain the fastest-growing segment due to subscription licensing and platform economics. -

Q: Which cancer types are most influential commercially?

A: Lung cancer contributed the largest revenue share in 2024; brain tumor AI solutions are projected to grow fastest during the forecast period. -

Q: Which region holds the largest share and which is growing fastest?

A: North America held the largest market share in 2024; Asia-Pacific is expected to register the fastest CAGR during the forecast period. -

Q: What recent regulatory and industry signals show market maturation?

A: Examples include Roche’s Breakthrough Device Designation (April 2025) for a lung cancer diagnostic and the NHS’s Cancer 360 tool (May 2025) integrated into a federated data platform — both signal accelerating regulatory and system-level adoption.

Access our exclusive, data-rich dashboard dedicated to the diagnostics sector – built specifically for decision-makers, strategists, and industry leaders. The dashboard features comprehensive statistical data, segment-wise market breakdowns, regional performance shares, detailed company profiles, annual updates, and much more. From market sizing to competitive intelligence, this powerful tool is one-stop solution to your gateway.

Access the Dashboard: https://www.towardshealthcare.com/access-dashboard

Immediate Delivery Available | Buy This Premium Research @ https://www.towardshealthcare.com/price/5044

Become a valued research partner with us – https://www.towardshealthcare.com/schedule-meeting

You can place an order or ask any questions, please feel free to contact us at sales@towardshealthcare.com

Powering Healthcare Leaders with Real-Time Insights: https://www.towardshealthcare.com/healthcare-intelligence-platform

Europe Region – +44 778 256 0738

North America Region – +1 8044 4193 44

APAC Region: +91 9356 9282 04

Web: https://www.towardshealthcare.com

Find us on social platforms: LinkedIn | Twitter | Instagram | Medium | Pinterest