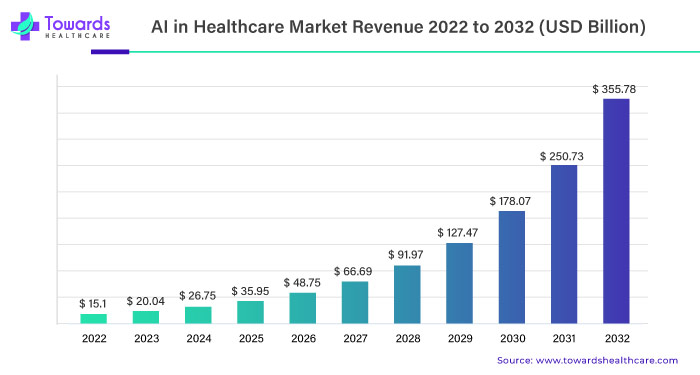

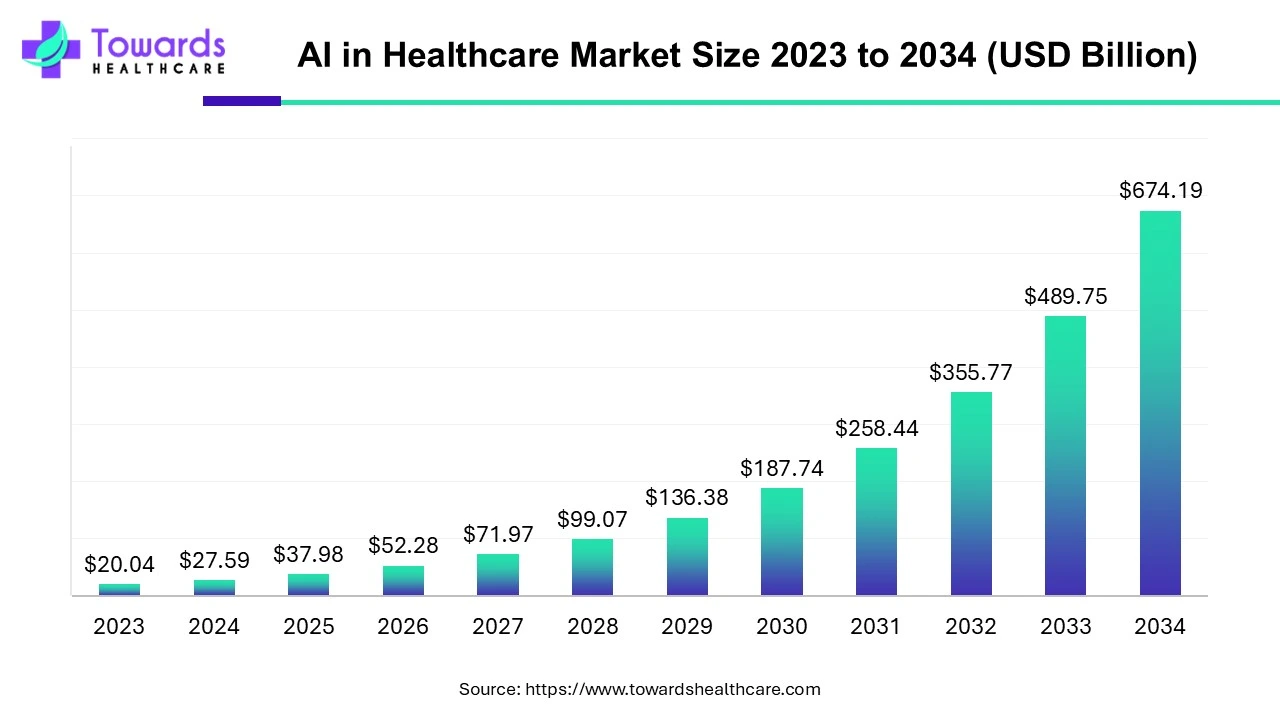

AI in Healthcare Market is projected to grow from USD 37.98 billion in 2025 to USD 674.19 billion by 2034 (a CAGR ≈ 37.66%), driven by rapid adoption of AI software, scaling services, major industry collaborations, and advances in imaging/early detection.

Download the free sample and get the complete insights and forecasts report on this market @ https://www.towardshealthcare.com/download-sample/5073

Market-size

Global headline numbers (base & forecast)

●Base: USD 37.98 billion (2025).

●Forecast: USD 674.19 billion (2034).

●Absolute growth (2025 → 2034): +USD 636.21 billion (674.19 − 37.98).

●Growth multiple: the market is expected to be ~17.75× larger in 2034 versus 2025.

●Implied CAGR (9 years): ≈ 37.66% (matches the provided CAGR).

U.S. market

●2024: USD 8.45 billion (value given).

●2025: USD 11.57 billion.

●2034: USD 194.88 billion.

●Absolute growth (2025→2034): +USD 183.31 billion.

●Growth multiple (2025→2034): ~16.84×.

●Implied CAGR (2025→2034): ≈ 36.9% (close to the stated 36.97%).

●U.S. share of the projected global 2034 market: ≈ 28.9% (194.88 / 674.19).

Segment-level size posture (high-level)

●Software is stated to have held a dominant presence in 2024 — meaning a large share of current value is software (platforms, APIs, ML frameworks, AI solutions).

●Services (deployment, integration, support) are forecast to grow significantly — implying increasing services revenue as deployments scale and more integration/customization is required.

Geography & velocity

●North America dominated in 2024 (largest revenue base and early adopter concentration).

●Asia-Pacific is forecast to be the fastest growth region during the period (driven by population, digital adoption, government initiatives).

Summary implication for investors / leaders

●The market is both large and hyper-growth: the expected ~17–18× expansion in <10 years implies mass re-wiring of healthcare IT, heavy capital flows to AI platforms & services, and a sustained opportunity for companies that can scale data pipelines, clinical validation, and regulatory compliance.

Market trends

Big-tech & ecosystem collaborations scaling AI models

●Example: Nvidia + Mayo Clinic + Illumina + IQVIA + Arc Institute (Jan 2025) — collaborative focus: scale clinical and genomics models across institutions.

●Implication: federated/enterprise model scaling, accelerated model training on medical data, more validated large clinical models.

Major funding rounds fueling expansion & developer ecosystems

Innovaccer Series F ($275M, Jan 2025) to expand AI + cloud capabilities and scale developer ecosystem.

●Implication: funding enables productization of population-health AI & commercial scale deployments (ops + analytics).

Regional policy & national strategy encouraging AI adoption

●India projection: AI in healthcare projected to add USD 25–30 billion to India’s GDP by 2025 per the cited “Digital Healthcare – Top 10 Myths Debunked” report; supportive acts like IndiaAI and Digital Personal Data Protection Act (2023).

●Implication: policy + regulation + national programs accelerate adoption and local market creation.

Rise of AI-powered medical devices and diagnostics

●Multiple novel devices and diagnostic tools (e.g., earlier detection of neurodegenerative disease, ultrasound + electromagnetic tracking for breast cancer treatment).

●Implication: device manufacturers and software vendors converge; regulatory clearance path becomes central.

Shift from point solutions to integrated care-workflow AI

●Products like Innovaccer’s “Agents of Care” and HelloCareAI’s virtual platform show trend toward AI assistants that remove administrative burden (billing, notes, scheduling, nurse-assist).

●Implication: operational ROI becomes as persuasive as clinical accuracy.

Clinical validation & accuracy claims shaping market momentum

●Example in text: NIH newsletter: 99% accuracy in evaluating mammograms (leading to faster breast cancer diagnosis).

●Implication: high-profile accuracy claims speed adoption but also invite scrutiny on dataset representativeness and generalizability.

Generative AI & medical imaging alliances

●Microsoft partnerships with Mass General Brigham and UW-Madison (Jul 2024) to develop imaging models for thousands of conditions; Google/Vertex AI expansion (Oct 2024) shows platformization of clinical AI.

●Implication: large cloud vendors continue to provide layers (compute, MLOps, model hosting) that enable healthcare AI deployments.

Local/regional digital health initiatives

●Andhra Pradesh’s Janani Mitra app (Dec 2024) for pregnant women — state level AI/tech solutions for public health.

●Implication: government-led apps drive scale and data availability in emerging markets.

Startups receiving targeted pre-seed/seed support for autonomous clinical decision tools

●Example: MedMitra AI raised ₹3 crore (Feb 2025) to develop autonomous AI solutions for clinical decision gaps.

●Implication: new entrants focused on clinical workflows will proliferate; specialization remains attractive.

Workforce & burnout mitigation as a major trend

●Tools to reduce clinician burnout (automating documentation, admin tasks) are moving from “nice to have” to “must have” for staffing constrained systems (e.g., Innovaccer agents).

●Implication: buyer willingness to pay grows where ROI = reduced staff time + faster throughput.

Roles / impacts of AI in this market

Early disease detection (imaging + biomarkers)

●Mechanism: deep learning+radiomics extract sub-visual imaging features; genomics + proteomics AI discover early signatures.

●Benefit: earlier diagnosis (e.g., mammography accuracy gains → faster breast cancer diagnosis), improved staging and treatment planning.

●Caveat: needs large, representative labelled datasets; external validation across devices/populations mandatory.

Precision medicine & biomarker-driven therapy selection

●Mechanism: ML models correlate genomic/proteomic signatures with drug response to identify targets.

●Benefit: better matching of patients to targeted therapies (oncology, neurodegeneration), reducing ineffective treatments.

●Caveat: translational pipeline (discovery → clinical validation → approval) remains long and costly.

Clinical decision support at point of care

●Mechanism: models ingest EHR, images, labs; provide differential diagnoses, risk scores, treatment suggestions.

●Benefit: improved diagnostic accuracy, earlier interventions, standardized protocol adherence.

●Caveat: “explainability” and medicolegal responsibility issues; clinician acceptance critical.

Operational automation & clinician workload reduction

●Mechanism: NLP for documentation, AI agents for administrative workflows (scheduling, coding, prior auth).

●Benefit: potential to reclaim clinician time — content cites ~$150B yearly potential operational savings and Harvard-derived claims of up to 50% treatment cost reductions when diagnosis is improved.

●Caveat: change management, integration complexity; ROI depends on scale.

Accelerated drug discovery & clinical trials

●Mechanism: AI screens molecules, predicts pharmacokinetics, optimizes trial cohorts and endpoints.

●Benefit: shorter timelines, reduced R&D costs, higher hit rates.

●Caveat: model predictions still require experimental/clinical confirmation.

Augmented and robot-assisted surgery

●Mechanism: AI guides instruments, enhances imaging fusion, offers intraoperative decision support.

●Benefit: higher precision, fewer complications, increased throughput (robot-assisted surgery was a leading application in 2024).

●Caveat: high capex, steep training curve, regulatory pathway for autonomy.

Remote patient monitoring & chronic care management

●Mechanism: AI analyzes wearables, home sensors, and telehealth streams to detect deterioration and personalize care.

●Benefit: prevents admissions, personalizes interventions for chronic disease management.

●Caveat: data connectivity/privacy; reimbursement frameworks vary.

Medical imaging scale & triage

●Mechanism: AI triages scans (urgent flagging), automates measurements, quantifies changes over time.

●Benefit: faster radiologist workflows, improved sensitivity/specificity in high-volume settings.

●Caveat: reliance on AI can create downstream false positives/negatives if not tuned.

NLP & unstructured data extraction (EHR intelligence)

●Mechanism: NLP extracts structured insights from notes, pathology reports, discharge summaries.

●Benefit: unlocks longitudinal data for analytics, cohort building, and improved coding.

●Caveat: clinical language complexity and inter-pathology variability limit out-of-the-box accuracy.

Cybersecurity & fraud detection

●Mechanism: anomaly detection on access patterns, claims, and device telemetry.

●Benefit: protects patient data, reduces fraudulent billing, secures networked medical devices.

●Caveat: adversarial attacks on AI and need for continual model retraining.

Regional insights

North America (leadership & scale)

●Market posture: Dominant revenue base in 2024; U.S. is the single largest market.

●Drivers: strong healthcare IT infrastructure, deep venture & private equity funding, concentration of leading academic medical centers, high per-capita healthcare spend.

●Implications: Rapid adoption of enterprise AI platforms, early commercial reimbursement pilots, centralized data partnerships (e.g., Mayo Clinic collaborations).

United States — micro view

●Rapid year-on-year expansion: US market rose from USD 8.45B (2024) to USD 11.57B (2025) and is forecast to reach USD 194.88B (2034).

●Drivers: payers & providers seek cost savings + outcome improvements; cloud & big-tech partnerships (e.g., Microsoft, Google) accelerate deployment.

Asia-Pacific (fastest growth)

●Market posture: projected fastest CAGR across regions.

●Drivers: large population, expanding geriatric base, digital penetration (smartphones), government investments in “smart hospitals”, rising private healthcare spend, and medical tourism.

●Country focus: India — strong growth due to national initiatives (IndiaAI) and projected GDP impact (USD 25–30B by 2025 per included report).

●Implications: opportunity to scale low-cost AI solutions and public health apps (e.g., Janani Mitra).

Europe (regulated innovation)

●Market posture: growth driven by regulatory frameworks that both constrain and encourage responsible AI (AI Act, European Health Data Space).

●Drivers: ageing population, public funding (Horizon Europe), strong collaborations between research institutes and industry.

●Implications: Europe will emphasize explainability, privacy, and compliance; solutions there may be more conservative but highly validated.

Latin America & Middle East/Africa (emerging adoption)

●Market posture: trailing in absolute dollars but high upside for targeted solutions (telemedicine, remote monitoring).

●Drivers: public health needs, paucity of specialists (making triage AI attractive), and rising smartphone coverage.

●Implications: success often depends on low-cost, mobile-first AI and strong public-private partnerships.

Cross-regional dynamics

●Data flows vs. sovereignty: growth depends on harmonizing cross-border data access with local privacy laws.

●Vendor strategy: global vendors supply cloud & models; regional vendors localize models and workflows (language, disease prevalence).

Market dynamics

Primary growth drivers

●Massive unmet clinical needs (early detection, diagnostics, chronic disease burden).

●Technology enablers: increased compute, cloud MLOps, pretrained models, and cheaper GPUs/ASICs.

●Business drivers: proven operational ROI (reduced admin costs, faster throughput) and payer interest.

Key restraints

●Data access & quality: fragmented, messy healthcare data reduces generalizability.

●Implementation cost: high integration, validation, and clinician training costs slow adoption at smaller providers.

●Regulatory uncertainty: varying approvals and standards across regions.

Strategic enablers

●Public-private collaborations (e.g., Nvidia + Mayo Clinic) that create data consortiums and validated model sets.

●Funding and developer ecosystem investment (e.g., Innovaccer’s $275M) for scalability.

Competitive dynamics

●Platform providers (cloud + model infra) vs vertical specialist vendors (imaging AI, genomics).

●New entrants focused on narrow clinical use-cases (specialists) can be acquired by platform players to expand portfolios.

Technology dynamics

●Shift from rule-based CAD to deep learning/radiomics and now to large, multi-modal clinical models.

●Increased emphasis on NLP, computer vision, and federated learning for privacy-respecting model training.

Regulatory & reimbursement dynamics

●Reimbursement remains a gating variable for many clinical use cases; early wins tied to demonstrable clinical and economic outcomes.

Workforce & operational dynamics

●AI as an augmentation strategy to relieve clinician burnout and administrative overload — solutions will be measured by clinician adoption metrics, not just accuracy.

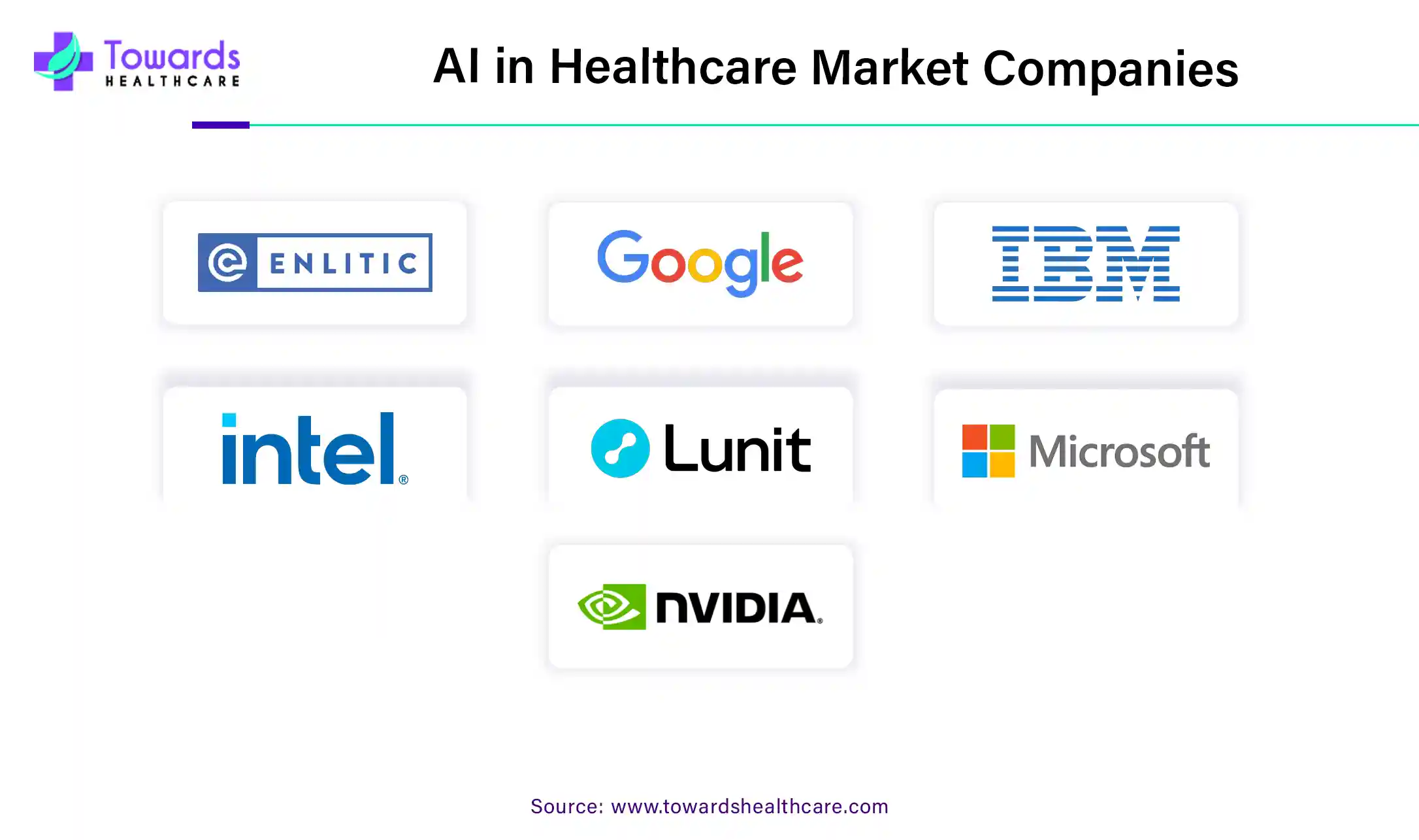

Top 10 companies

Google (Google Health / Vertex AI)

Product/overview: Cloud AI platforms (Vertex AI), imaging & clinical research collaborations.

Strength: Massive cloud infrastructure, ML research depth, clinical partnerships — platformization of model deployment and data analytics.

Microsoft (Health & Life Sciences)

Product/overview: Healthcare cloud offerings, partnerships for imaging models (e.g., Mass General Brigham), and productivity/clinical workflow integration.

Strength: Enterprise reach with clinician productivity tools, strong compliance posture, and healthcare partner network.

Nvidia

Product/overview: GPU/accelerator hardware and healthcare AI stacks (model toolkits, inferencing platforms); active clinical collaborations (e.g., Jan 2025 consortium).

Strength: Market leader in compute for AI; ecosystem for model training/validation at scale.

IBM (Watson & Health initiatives)

Product/overview: AI/analytics for clinical decision support, life-sciences data analytics.

Strength: Enterprise healthcare customers, deep experience in complex deployments, and strong regulatory/government relationships.

Siemens Healthineers

Product/overview: Medical devices + AI integration layers; collaborations to make generative AI available in their dev stacks.

Strength: Clinical device portfolio and hospital integration expertise; trusted brand in imaging.

Philips

Product/overview: Imaging, monitoring, and informatics with AI modules for diagnostics and workflow.

Strength: Broad hospital footprint, integrated hardware+software approach.

Intel

Product/overview: Hardware (processors, accelerators) and edge computing solutions for medical devices.

Strength: Supply chain & hardware optimization for inference at the edge and in-hospital compute.

Johnson & Johnson

Product/overview: Medical devices and surgical technologies, increasingly integrating AI into surgical assistance.

Strength: Strong device commercialization channels and clinical relationships with surgeons/hospitals.

Medtronic

Product/overview: Devices and therapies with data-driven device support and surgical tech.

Strength: Large installed base of devices and long sales cycles that favour deep integration of AI features.

Lunit

Product/overview: AI-first medical imaging company focused on oncology and imaging diagnostics.

Strength: Specialized imaging algorithms, rapid clinical validation in imaging workflows.

Latest announcements

Nvidia collaboration with Mayo Clinic, Illumina, IQVIA, Arc Institute (Jan 2025)

What: Consortium to scale AI models in healthcare and genomics.

Why it matters: Aligns compute leader with clinical/genomics data owners — accelerates validated, deployable models for clinical use and research.

Innovaccer raises $275M (Series F, Jan 2025)

What: Capital to expand AI + cloud capabilities and grow developer ecosystem.

Why it matters: Signals investor confidence in platform-level, population-health AI and speaks to commercial expansion of enterprise clinical AI.

HelloCareAI secures $47M (Apr 2025)

What: Funding to expand AI-powered virtual healthcare for smart hospitals (nursing support, remote monitoring).

Why it matters: Direct investment in operational AI that targets nurse augmentation and hospital workflows.

Innovaccer — “Agents of Care” (Feb 2025)

What: AI tools to reduce medical staff burnout by handling administrative duties.

Why it matters: Demonstrates market prioritization of clinician workflow solutions with direct ROI.

Microsoft — imaging model collaborations (Jul 2024)

What: Partnerships with Mass General Brigham and UW-Madison to build models across >23,000 conditions.

Why it matters: Large clinically-validated model sets can power broad radiology augmentation.

Siemens + AWS integration (Jan 2024)

What: Making generative AI accessible via Siemens’ Mendix low-code platform with Amazon Bedrock.

Why it matters: Low-code model integration allows non-ML practitioners to incorporate generative AI into clinical apps.

Andhra Pradesh — Janani Mitra app (Dec 2024)

What: State AI app for pregnant women’s delivery parameters and nutrition guidance.

Why it matters: Example of public health AI at scale; can generate large labeled datasets for maternal health interventions.

Google Cloud — Vertex AI expansion for Healthcare Data Engine (Oct 2024)

What: Tools for faster queries of health records and advanced analytics.

Why it matters: Supports rapid analytics and portability of clinical insights across systems.

MedMitra AI pre-seed (Feb 2025)

What: ₹3 crore (~small pre-seed) to develop autonomous AI decision tools.

Why it matters: Highlights proliferation of niche startups addressing specific clinical decision gaps in India.

Recent developments

Market is maturing from pilots to scale — Funding rounds, big-tech collaborations, and state apps show movement from research proofs toward commercial/operational scale.

Operational ROI as the adoption lever — Tools that reduce clinician admin burden and demonstrably reduce costs (e.g., Innovaccer, HelloCareAI) are gaining traction.

Imaging remains a primary battleground — Microsoft, Google, and others are placing big bets on imaging models that cover thousands of conditions — imaging AI is a proven monetizable path.

Public sector & regional initiatives create demand pipelines — e.g., AP’s Janani Mitra app and India AI initiatives create datasets and deployment venues for scaled AI solutions.

Ecosystem play vs. point play — Platform vendors (cloud + compute + MLOps) and specialized vendors (imaging, genomics) are forming strategic alliances to deliver end-to-end value.

Segments covered

By Component

Hardware (processors, GPUs, FPGAs, ASICs): critical for training and inferencing speed, latency-sensitive hospital deployments, and edge inferencing inside devices.

Software (AI platforms, APIs, ML frameworks, AI solutions): enables model development, validation, MLOps, and clinical workflow integration — dominant revenue component in 2024.

Services (deployment, integration, support, consulting): grows as complexity of deployments increases; service revenue includes model validation and regulatory support.

By Deployment

On-premise: needed for privacy-sensitive hospitals and latency-critical workloads (e.g., intraoperative imaging).

Cloud-based: enables scale, continuous model updates, and easier MLOps; preferred for large model hosting and multi-institution collaborations.

By Technology

Machine Learning / Deep Learning: backbone for imaging, genomics, and predictive analytics.

NLP & Speech Analytics: unlocks unstructured EHR notes and supports dictation/clinical documentation automation.

Computer Vision & Radiomics: specialized for imaging feature extraction and tumor characterization.

By End-Use

Healthcare Providers: hospitals & clinics — primary buyers for workflow and imaging AI.

Healthcare Companies: pharma & biotech — use AI for drug discovery, trials, and R&D.

Payers / Others: interested in cost reduction and population risk stratification.

By Region

Standard geographic segmentation (North America, Europe, APAC, LATAM, MEA) each with specific needs and regulatory stance (see regional section above).

Top 5 FAQs

-

Q: What is the expected size of the AI in Healthcare market by 2034?

A: The market is projected to reach USD 674.19 billion by 2034, up from USD 37.98 billion in 2025 (implied CAGR ≈ 37.66%).

-

Q: How big is the U.S. market and what is its growth path?

A: The U.S. market was USD 8.45B in 2024, USD 11.57B in 2025, and is forecast to reach USD 194.88B by 2034 (CAGR ≈ 36.9% from 2025–2034). The U.S. is expected to represent ~29% of the 2034 global market.

-

Q: Which parts of the AI in Healthcare stack currently make most revenue?

A: Software held a dominant presence in 2024 (platforms, APIs, clinical ML solutions). Services are forecast to grow significantly as implementations scale and customization/integration needs rise.

-

Q: Is there clinical evidence that AI is already improving diagnostics?

A: The provided content references a NIH newsletter reporting 99% accuracy in evaluating mammograms, which has accelerated breast cancer diagnosis—an example of high-impact clinical performance driving adoption. (As always, clinical claims require peer review, external validation, and deployment-specific evaluation.)

-

Q: What are the main barriers to adoption?

A: Key barriers include data access & integration hurdles, high implementation costs, fragmented data quality across sites, regulatory/compliance complexity, and clinician acceptance/trust concerns.

Access our exclusive, data-rich dashboard dedicated to the healthcare market – built specifically for decision-makers, strategists, and industry leaders. The dashboard features comprehensive statistical data, segment-wise market breakdowns, regional performance shares, detailed company profiles, annual updates, and much more. From market sizing to competitive intelligence, this powerful tool is one-stop solution to your gateway.

Access the Dashboard: https://www.towardshealthcare.com/access-dashboard

Immediate Delivery Available | Buy This Premium Research @ https://www.towardshealthcare.com/price/5073

Become a valued research partner with us – https://www.towardshealthcare.com/schedule-meeting

You can place an order or ask any questions, please feel free to contact us at sales@towardshealthcare.com

Powering Healthcare Leaders with Real-Time Insights: https://www.towardshealthcare.com/healthcare-intelligence-platform

Europe Region – +44 778 256 0738

North America Region – +1 8044 4193 44

APAC Region: +91 9356 9282 04

Web: https://www.towardshealthcare.com

Find us on social platforms: LinkedIn | Twitter | Instagram | Medium | Pinterest