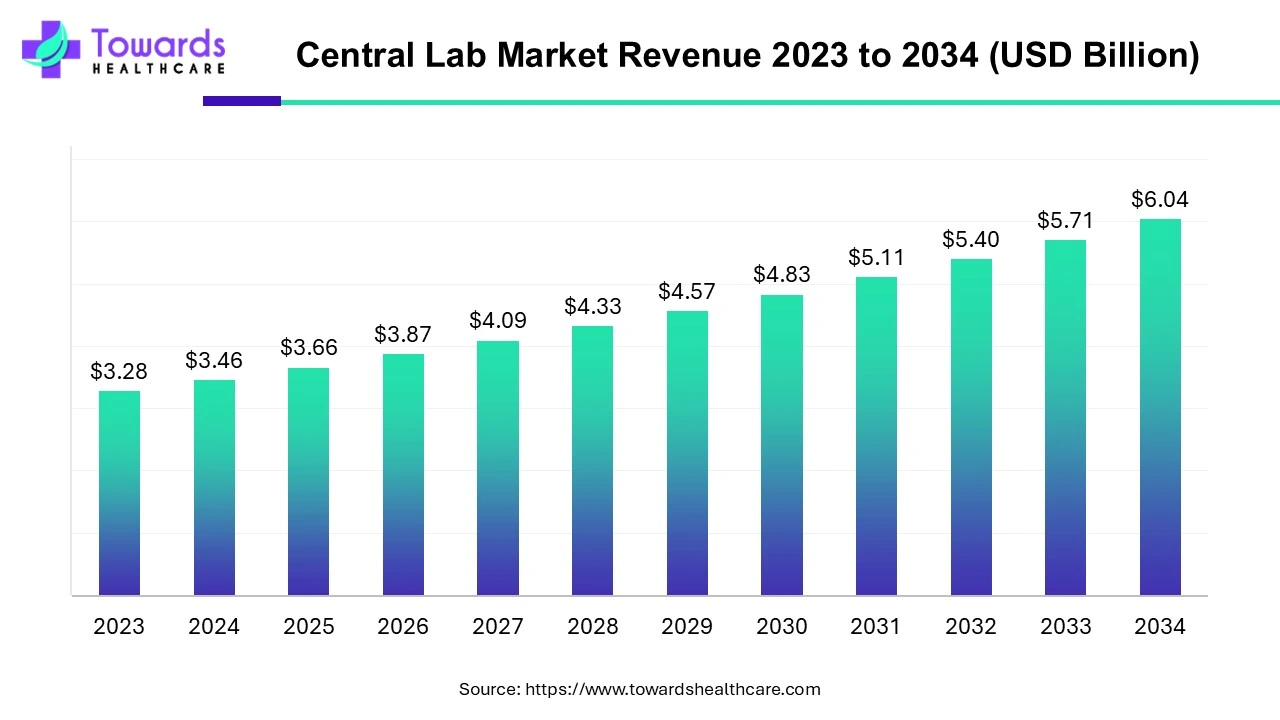

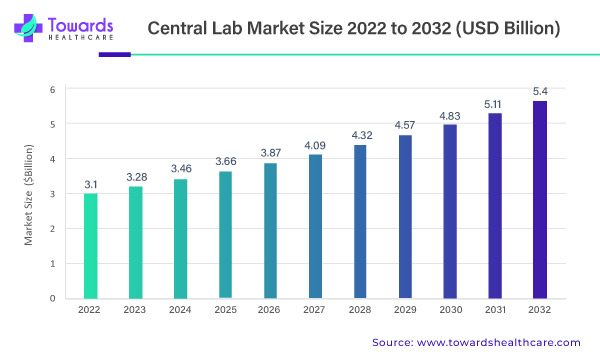

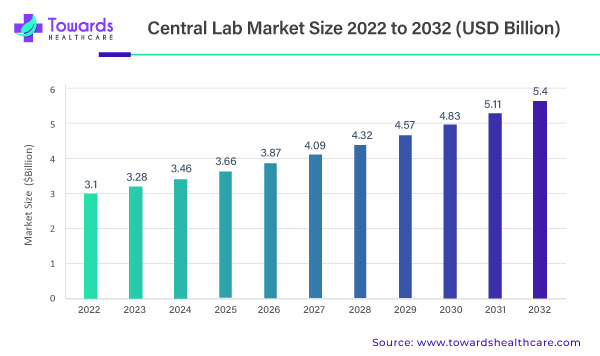

The global Central Lab market was valued at USD 3.46 billion in 2024 and is forecast to reach USD 6.04 billion by 2034 (CAGR 5.71%), driven by rising clinical trial activity, higher R&D investment and ongoing demand for standardized, centralized testing across multi-site studies.

Market-size

Base figure & forecast — 2024 revenue: USD 3.46B; 2034 projection: USD 6.04B; implied absolute increase ≈ USD 2.58B over 10 years at a 5.71% CAGR.

Revenue growth composition — growth is a mix of increased test volumes from expanding clinical trials, higher per-test complexity (genetic/biomarker assays), and value-added digital services (automation, e-requisition, analytics).

Volume drivers — more trials per sponsor and more multi-regional trials increase sample throughput and recurring revenue for central labs (outsourcing trend >50% of trials use central labs).

Price/mix drivers — shift toward expensive genetic and biomarker assays raises average revenue per sample versus routine chemistry tests.

Capacity & capex — forecasted growth requires investment in larger, digitally instrumented facilities (e.g., new CRLs such as Apollo Diagnostics’ Digi-Smart CRL) and in automation to keep TAT competitive.

Margins — economies of scale from centralized operations and digital workflow automation improve gross margins relative to decentralized testing, but margin gains can be offset by high equipment amortization (genomics platforms).

Service bundling — revenue increasingly from bundled offerings (PK/PD, biomarker, e-requisition, data reporting), improving client stickiness and lifetime value.

Geographic mix & currency effects — North America remains the largest revenue source; APAC growing fastest, shifting revenue mix and investment flows.

Consolidation impact — M&A among CROs/central labs (major providers listed in the market) concentrates revenue and customer relationships, accelerating standardized pricing and cross-sell.

Regulatory & quality costs — compliance, accreditation and data integrity investments are significant operating cost items that scale with market growth.

Market trends

Outsourcing intensification — pharmaceutical and biopharma companies continue to outsource central lab services rather than maintain in-house labs; over 50% of trials now use central labs.

Shift to complex testing — growth in biomarker and genetic services (genetic services fastest CAGR) as precision medicine and targeted therapies proliferate.

Digitalization of workflows — e-requisition solutions (IQVIA Site Lab Navigator) and digital sample tracking reduce administrative burden and errors.

Faster turnaround time (TAT) emphasis — clients demand lower TAT; new facilities (Apollo Diagnostics’ Digi-Smart CRL) claim significant TAT reductions (e.g., 60%).

Global footprint expansion — collaborations (Teddy Laboratory + LabConnect) and regional partnerships drive cross-border service delivery and access to new trial geographies.

Cost pressure & efficiency push — sponsors seek affordable solutions as trial costs climb, pushing labs to automate and centralize to reduce per-sample costs.

Regulatory scrutiny & standardization — regulators and sponsors emphasize data integrity and standardized lab processes across sites.

Integration with CRO ecosystem — central labs become part of end-to-end clinical service stacks, offering complementary clinical trial services (e.g., partnering with CROs like Simbec-Orion + Avance Clinical).

Technology adoption — next-gen flow cytometry reporting automation, AI protocol reading and sample consent tracking are becoming competitive differentiators.

Regional trial cost arbitrage — clinical trial growth in APAC (China, India, SEA) driven by lower per-patient costs and increasing local R&D investment.

AI roles & impacts for the Central Lab market

Protocol ingestion & mapping — AI reads trial protocols and auto-maps required tests/assays to lab workflows, reducing manual setup time and errors.

Impact: faster study onboarding, fewer requisition mistakes.

Automated e-requisition validation — ML models flag anomalies, missing fields or incompatible test combinations before sample shipment.

Impact: fewer rejected samples, lower administrative workload.

Sample logistics optimization — AI optimizes routing, batching and cold-chain scheduling across sites and courier networks.

Impact: reduced TAT, lower shipping costs, improved sample integrity.

Assay QC & anomaly detection — AI analyzes instrument output streams to detect drift, contamination or unusual patterns in real-time.

Impact: earlier fault detection, higher data reliability.

Predictive capacity planning — demand forecasting models predict assay volumes, allowing labs to allocate instruments and staff efficiently.

Impact: optimized capex utilization and reduced overtime.

Automated report generation & interpretation — natural-language systems draft standardized reports and flag clinically relevant biomarker changes.

Impact: faster reporting to sponsors, improved clinician readability.

AI-assisted biomarker discovery pipelines — combining lab assay data with other datasets to identify candidate biomarkers for trials.

Impact: new service lines and higher value contracts.

Consent & compliance monitoring — ML tracks consent metadata, links consents to samples, and alerts on compliance gaps.

Impact: reduced regulatory risk and audit readiness.

Image and cytometry analysis — deep-learning algorithms process high-content images and flow cytometry data faster than manual review.

Impact: scalability of complex assays (immunophenotyping, cell-based assays).

Clinical trial matching & site selection — AI uses lab capacity, regional disease prevalence and TAT metrics to suggest optimal site networks for trials.

Impact: higher trial efficiency and participant recruitment rates.

Regional insights

North America (dominant revenue share)

Regulatory & quality leadership — strong regulatory frameworks and high adoption of quality controls drive demand for accredited central labs.

R&D concentration — large pharma/biotech R&D budgets and sponsor HQs are here → more trials and high-value complex assays.

Technology adoption — rapid uptake of e-requisition and digital reporting (e.g., IQVIA tools), improving operational efficiency and client satisfaction.

Asia-Pacific (fastest growth)

Cost advantage & trial volume — lower per-patient trial costs attract sponsors to run large, multi-site studies here (China as major contributor).

Capacity expansion — local labs expanding to capture CRO and sponsor demand; partnerships (Teddy + LabConnect) facilitate global service access.

Talent & infrastructure — growing skilled workforce and investments in lab infrastructure make APAC attractive for complex testing.

Europe

Personalized medicine & rare disease focus — high prevalence of rare disease initiatives and personalized medicine funding increase demand for genetic and biomarker services.

Public health testing volumes — dense healthcare systems with high test volumes support sophisticated central lab service models.

Latin America

Emerging trial destination — growing trial activity driven by cost and patient populations; however, infrastructure variability requires central lab partnerships to ensure standardization.

Opportunity for regional hubs — major labs can build regional processing hubs to serve multiple countries, lowering TAT and costs.

Middle East & Africa (MEA)

Under-penetrated but growing — lower current share but opportunities for centralized services supporting regional clinical research and public health testing.

Infrastructure & regulatory maturation required — investments needed in cold chain, accreditation and digital connectivity.

Market dynamics

Key drivers

Rising clinical trials & R&D spending — more studies and higher complexity increase demand for centralized standardized testing.

Shift to precision medicine — biomarker and genetic testing growth drives premium services.

Cost & efficiency pressures on sponsors — central labs reduce duplicative testing, lower unit costs and improve comparability.

Digital workflow demand — sponsors demand integrated digital solutions (e-requisition, sample tracking).

Major restraints

Turnaround-time concerns — shipping samples to central labs can delay time-sensitive decisions (dosing, randomization).

High up-front equipment and compliance costs — genomics platforms and accreditation carry heavy capital and operational cost.

Sample integrity & cold chain logistics — cross-border transfers increase risk and cost.

Opportunities

AI & automation — process acceleration, error reduction and new product offerings.

Expansion into emerging markets — APAC and LATAM provide volume and cost advantages.

Bundled CRO partnerships — offering integrated trial services improves customer retention and upsell.

New assays & companion diagnostics — co-development with pharma offers higher margin services.

Challenges to resolve

Balancing centralization with TAT — build regional hubs and faster courier networks.

Maintaining data integrity across regions — invest in standardized LIMS and e-requisition systems.

Regulatory and privacy compliance across jurisdictions — harmonize SOPs and consent handling.

Top 10 companies

IQVIA / IQVIA Laboratories

Product/Service: Central lab services + digital solutions (Site Lab Navigator, e-requisition).

Overview: Integrated clinical data and lab services within a global CRO platform.

Strength: Strong digital offerings that reduce administrative burden and enhance data integrity; recognized leader in workflow automation.

LabCorp (including Central Laboratory services)

Product/Service: Large-scale central lab testing and clinical trial support.

Overview: Major diagnostics company offering extensive lab capabilities.

Strength: Massive testing capacity and logistics network; recognized brand and broad assay menu.

Eurofins Central Laboratory

Product/Service: Central lab testing across multiple disciplines.

Overview: Global testing provider with wide geographic reach.

Strength: Broad service portfolio and international footprint enabling multi-region trials.

ICON / ICON Central Labs

Product/Service: Central lab services integrated with CRO operations.

Overview: CRO with embedded lab capabilities.

Strength: CRO integration enables end-to-end trial services and streamlined sponsor interactions.

PPD (now part of Thermo/Freestanding in some markets)

Product/Service: Central lab & clinical trial services.

Overview: Large CRO network offering lab solutions.

Strength: Global reach, established sponsor relationships and large sample throughput.

Cerba Research / Barc Lab

Product/Service: Centralized testing with biomarker capabilities.

Overview: Specialized central lab services focused on sophisticated assays.

Strength: Deep biomarker and specialized testing expertise.

Frontage Laboratories, Inc.

Product/Service: Lab services supporting clinical trials.

Overview: Full-service central lab provider with emphasis on pharmacology and specialized testing.

Strength: Technical depth and client focus on complex studies.

Celerion

Product/Service: Central lab components for early-phase and specialized trials.

Overview: Early-phase CRO with lab support.

Strength: Expertise in early clinical pharmacology and tightly integrated lab support.

LabConnect

Product/Service: Central lab network services and connectivity solutions.

Overview: Facilitates lab partnerships and expands global operations through collaborations.

Strength: Ability to scale clients’ lab presence globally through partnerships (e.g., Teddy Laboratory).

Apollo Diagnostics / Clinical Reference Laboratory / Bioscientia (Sonic Healthcare)

Product/Service: Regional CRLs and centralized diagnostics (Apollo launched Digi-Smart CRL).

Overview: Growing regional players investing in digital CRLs and reduced TAT.

Strength: Regional expansion, digital integration and TAT improvement claims.

Latest announcement

Teddy Laboratory + LabConnect (May 2025)

What: Collaboration to build a full-chain laboratory service system covering China and international markets.

Why it matters: Enables Teddy to scale international operations and lets LabConnect expand into North America and Europe — this is a strategic cross-border capacity expansion that can shorten TAT for China-origin trials and offer sponsors a single connected lab partner.

Implication: Accelerates commercialization pathways for innovative drugs by improving global sample flow and centralized reporting.

Simbec-Orion + Avance Clinical (Feb 2025)

What: Partnership to offer comprehensive clinical research services, including Central Lab services.

Why it matters: Leverages complementary regional strengths to serve sponsors more holistically; improves regional coverage and client value proposition.

IQVIA — Site Lab Navigator launch (Mar 2025)

What: An e-requisition platform automating lab workflows between sponsors and investigator sites.

Why it matters: Reduces administrative burden, improves data integrity and streamlines specimen handling — directly addresses one of the market’s major pain points.

Apollo Diagnostics — Digi-Smart Central Reference Laboratory (May 2025)

What: New 45,000 sq. ft. facility in Chennai integrating five disciplines with digital monitoring; claims to reduce sample turnaround by 60%.

Why it matters: Demonstrates investment in large, digitally enabled regional CRLs to compete on speed and integrated services — an example of APAC capacity build-out.

Recent developments

Digital platforms deployed by major labs (IQVIA) — automation of lab requisitions and specimen management to improve quality and reduce administrative errors.

Regional digital CRL launches (Apollo Diagnostics) — investment in large, multi-discipline digital labs to reduce TAT substantially and serve local/regional trial volume.

Cross-border partnerships (Teddy + LabConnect) — strategic alliances aimed at connecting regional lab capacity into global networks, enabling sponsors to run multi-region studies more smoothly.

CRO + central lab collaborations (Simbec-Orion + Avance Clinical) — trend of integrated service offerings to meet end-to-end sponsor needs.

Growing adoption of complex assays — continued shift toward biomarker and genetic services, increasing per-sample revenue and technical staffing needs.

Segments covered

By Services

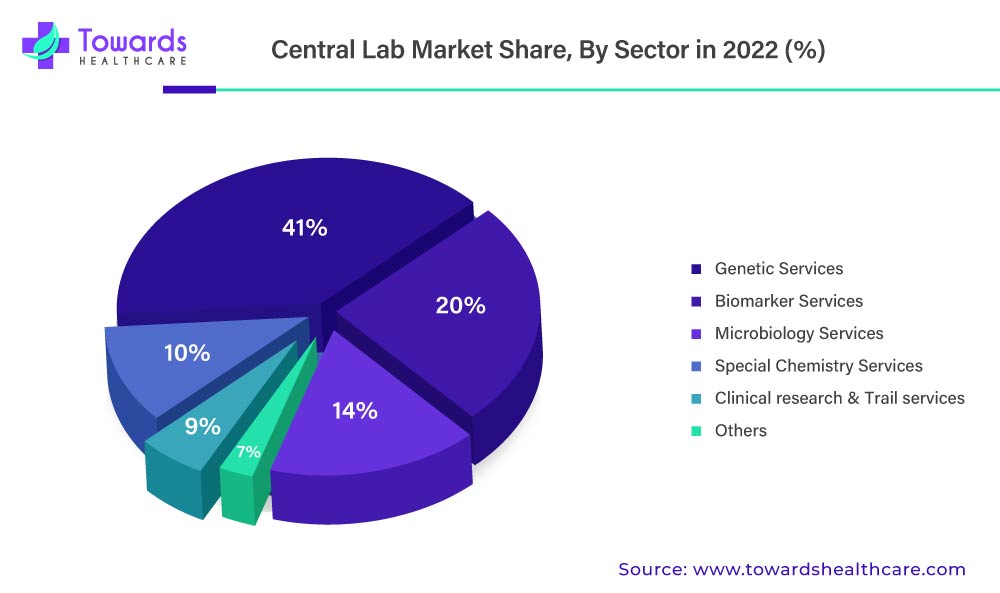

Genetic Services — high-complexity assays (NGS, targeted panels); rapid growth due to precision medicine and rare disease research. Requires specialized infrastructure and drives higher per-test revenue.

Biomarker Services — assay development, validation and deployment for pharmacodynamic/target engagement and companion diagnostics; currently the largest revenue contributor because of co-development trends.

Microbiology Services — pathogen testing, serology and infectious disease assays; intensified by pandemic preparedness and vaccine trials.

Special Chemistry Services — specialized analytes and high-sensitivity assays (toxicity markers, immunoassays).

Clinical Research & Trial Services — integrated lab testing services tied to CRO/clinical trial support, often bundled with logistics and data reporting.

Others — niche services such as flow cytometry, immunophenotyping, PK/PD analytics.

By End-User

Pharmaceutical Companies — largest revenue source; they require broad testing portfolios for drug development and safety/PK studies.

Biotechnology Companies — fastest growth segment; biologics and gene therapies demand complex, high-specialty lab work.

Academic & Research Institutes — often use central labs for standardized assays in multi-site research consortia.

Others — public health agencies, diagnostics developers and CROs.

By Geography

North America — largest share; regulatory, R&D concentration.

Europe — strong rare disease and personalized medicine demand.

Asia-Pacific — fastest growth; cost advantages and trial volume.

Latin America & MEA — emerging hubs with regional opportunity.

Top 5 FAQs

-

Q: What is the current size and forecast for the Central Lab market?

A: The market was USD 3.46 billion in 2024 and is projected to reach USD 6.04 billion by 2034, expanding at a 5.71% CAGR (2024–2034). -

Q: Which service segments lead and which will grow fastest?

A: Biomarker services held the largest revenue share in 2024; genetic services are expected to grow at the highest CAGR over the forecast period due to precision medicine and rising genetic testing demand. -

Q: Which end-user dominates the market?

A: Pharmaceutical companies contributed the largest revenue share in 2024; biotechnology companies are expected to grow fastest as biologics and gene therapies expand. -

Q: Which regions are most important for the Central Lab market?

A: North America currently dominates due to R&D concentration and regulatory environment; Asia-Pacific is forecast to grow the fastest, driven by lower trial costs, expanding local R&D and capacity growth. -

Q: What are the main challenges central labs must solve?

A: Key challenges include turnaround-time delays when shipping samples to central labs, high capital and compliance costs for complex assays, and maintaining data integrity and regulatory compliance across multi-regional operations.

Access our exclusive, data-rich dashboard dedicated to the diagnostics sector – built specifically for decision-makers, strategists, and industry leaders. The dashboard features comprehensive statistical data, segment-wise market breakdowns, regional performance shares, detailed company profiles, annual updates, and much more. From market sizing to competitive intelligence, this powerful tool is one-stop solution to your gateway.

Access the Dashboard: https://www.towardshealthcare.com/access-dashboard

Immediate Delivery Available | Buy This Premium Research @ https://www.towardshealthcare.com/price/5038

Become a valued research partner with us – https://www.towardshealthcare.com/schedule-meeting

You can place an order or ask any questions, please feel free to contact us at sales@towardshealthcare.com

Powering Healthcare Leaders with Real-Time Insights: https://www.towardshealthcare.com/healthcare-intelligence-platform

Europe Region – +44 778 256 0738

North America Region – +1 8044 4193 44

APAC Region: +91 9356 9282 04

Web: https://www.towardshealthcare.com

Find us on social platforms: LinkedIn | Twitter | Instagram | Medium | Pinterest

")

")

")