The global clinical trials market is undergoing a structural transformation that goes far beyond incremental growth. What was once a highly linear, time-intensive, and geographically concentrated process has evolved into a complex, technology-enabled ecosystem shaped by scientific urgency, patient-centric thinking, regulatory recalibration, and sustained capital inflows. After more than a decade of observing this market across therapeutic areas and geographies, one conclusion is clear: clinical trials are no longer just a step in drug developmen, they have become a strategic capability that determines success or failure in modern healthcare innovation.

At the core of this shift lies a convergence of forces. Rising disease burden, especially from chronic and rare conditions, has increased the demand for novel therapies. Scientific advances have expanded what is possible, pushing trials into areas such as gene therapy, cell therapy, RNA-based drugs, and personalized medicine. Governments have recognized clinical research as national infrastructure rather than optional activity. At the same time, technology has quietly but decisively re-engineered how trials are designed, conducted, monitored, and analyzed. Together, these elements are redefining both the scale and the philosophy of clinical research.

The growing incidence and prevalence of chronic disorders remain one of the most powerful drivers of clinical trial activity. Cardiovascular diseases, oncology, neurological disorders, autoimmune diseases, metabolic conditions, and rare genetic disorders now dominate research pipelines. These conditions are long-term, complex, and heterogeneous by nature, making traditional “one-size-fits-all” trial models increasingly inadequate. Sponsors must now demonstrate not only efficacy but also long-term safety, quality-of-life improvements, and real-world relevance. This has expanded the scope, duration, and sophistication of clinical trials, pushing the market toward more adaptive and data-rich designs.

Research and development spending has followed this medical reality. Pharmaceutical and biotechnology companies are investing heavily in discovery and development, not just to remain competitive but to survive in an environment where innovation cycles are accelerating. Over the last decade, R&D strategies have shifted from volume-driven pipelines to precision-driven portfolios. Instead of developing multiple broad-spectrum drugs, companies increasingly focus on targeted therapies aimed at specific patient subgroups. This approach improves success rates but also increases trial complexity, as smaller, more defined populations require careful recruitment, biomarker validation, and advanced statistical modeling.

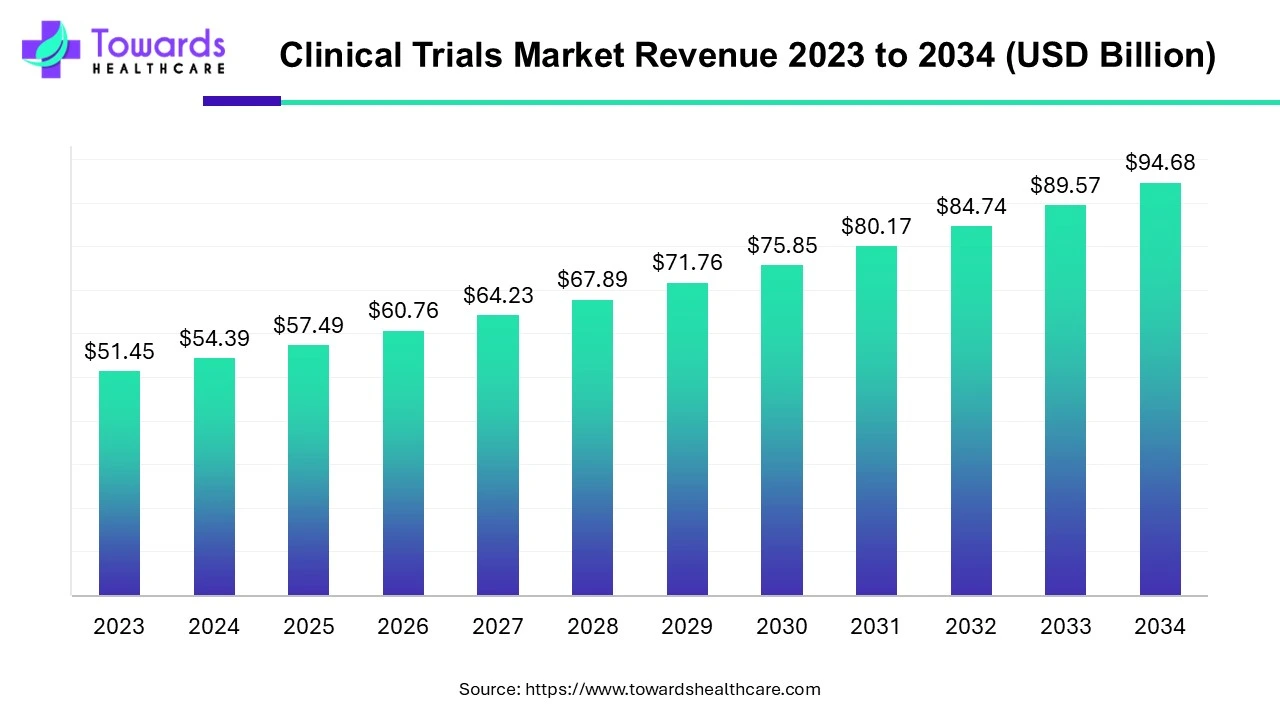

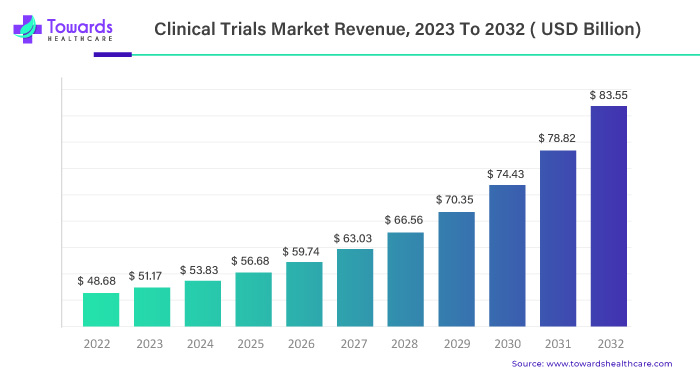

From a market valuation perspective, these structural shifts are already translating into sustained and measurable growth. The global clinical trials market is calculated at approximately USD 98.91 billion in 2026, reflecting the cumulative impact of rising R&D intensity, expanding trial volumes, and increasing operational complexity. This figure does not simply represent more studies being conducted; it reflects deeper investment per trial, broader geographic reach, and greater reliance on specialized technologies and services.

𝐃𝐨𝐰𝐧𝐥𝐨𝐚𝐝 𝐅𝐫𝐞𝐞 𝐒𝐚𝐦𝐩𝐥𝐞:

https://www.towardshealthcare.com/download-sample/5018

Looking ahead, the market is expected to reach nearly USD 174.18 billion by 2035, expanding at a compound annual growth rate of 5.7% between 2026 and 2035. This steady trajectory suggests a market driven by structural demand rather than short-term cycles. Unlike earlier phases where growth was tied closely to blockbuster drug development, future expansion will be supported by a diversified mix of therapeutic areas, trial models, and stakeholder participation. Oncology, rare diseases, neurology, and immunology are expected to remain key contributors, while emerging modalities such as gene and cell therapies will continue to push average trial costs and duration higher.

This forecast also reflects a broader redefinition of what constitutes clinical trial activity. Spending increasingly extends beyond traditional site operations to include digital infrastructure, real-world data integration, long-term follow-up studies, and patient engagement platforms. As regulators, payers, and healthcare systems demand stronger evidence of value, sponsors are investing earlier and more consistently in robust trial frameworks. The projected growth rate therefore captures not only an increase in trial numbers but a qualitative shift toward more comprehensive, data-intensive research programs.

Importantly, the expected market expansion underscores the resilience of clinical trials as a sector. Even amid economic uncertainty or shifting healthcare priorities, clinical research remains a non-negotiable foundation for medical progress. The forecasted growth through 2035 reflects confidence that innovation pipelines will remain active, policy environments will continue to support research, and technological adoption will further improve trial efficiency. In this context, the clinical trials market is positioned not as a cost center, but as a long-term investment in healthcare sustainability and scientific advancement.

Personalized medicine has played a central role in reshaping trial methodologies. Therapies tailored to genetic, molecular, or phenotypic characteristics demand trials that can identify the right patients at the right time. Companion diagnostics, genomic screening, and biomarker-based enrollment are no longer optional in many therapeutic areas. As a result, clinical trials now operate at the intersection of medicine, data science, and diagnostics. This integration has expanded the clinical trials market beyond traditional research organizations to include genomic labs, data analytics firms, and digital health providers.

Biologics, cell therapies, and gene therapies represent another defining trend. These advanced modalities have fundamentally different development pathways compared to small-molecule drugs. Manufacturing constraints, cold-chain logistics, ethical considerations, and long-term follow-up requirements all influence trial design. For example, gene therapy trials often require multi-year post-treatment monitoring to assess durability and safety. This has created demand for specialized clinical trial services, long-term patient registries, and novel regulatory frameworks, all of which contribute to sustained market expansion.

Investment patterns reflect the strategic importance of clinical trials in this new environment. Governments across developed and emerging economies are increasing funding for clinical research as part of broader healthcare and innovation agendas. Public funding supports early-stage research, academic-industry collaborations, and infrastructure development, reducing entry barriers for smaller innovators. At the same time, private investment—from venture capital, private equity, and strategic partnerships—has surged, particularly in high-risk, high-reward areas such as rare diseases and advanced therapies.

These investments are not limited to drug developers. Contract research organizations, technology providers, and site management organizations have attracted significant capital as sponsors seek to outsource complexity and improve efficiency. The rise of specialized service providers reflects a recognition that clinical trials require operational excellence as much as scientific insight. Efficient patient recruitment, regulatory compliance, data integrity, and timeline management can determine whether a promising therapy reaches the market or stalls indefinitely.

Favorable government policies have further accelerated market growth. Regulatory authorities have increasingly adopted risk-based and science-driven approaches to trial oversight. Accelerated approval pathways, conditional approvals, and adaptive trial designs have become more common, particularly in areas of high unmet medical need. These policies do not lower standards; instead, they modernize evaluation processes to reflect advances in science and data analytics. By providing clearer guidance and greater flexibility, regulators have reduced uncertainty and encouraged innovation.

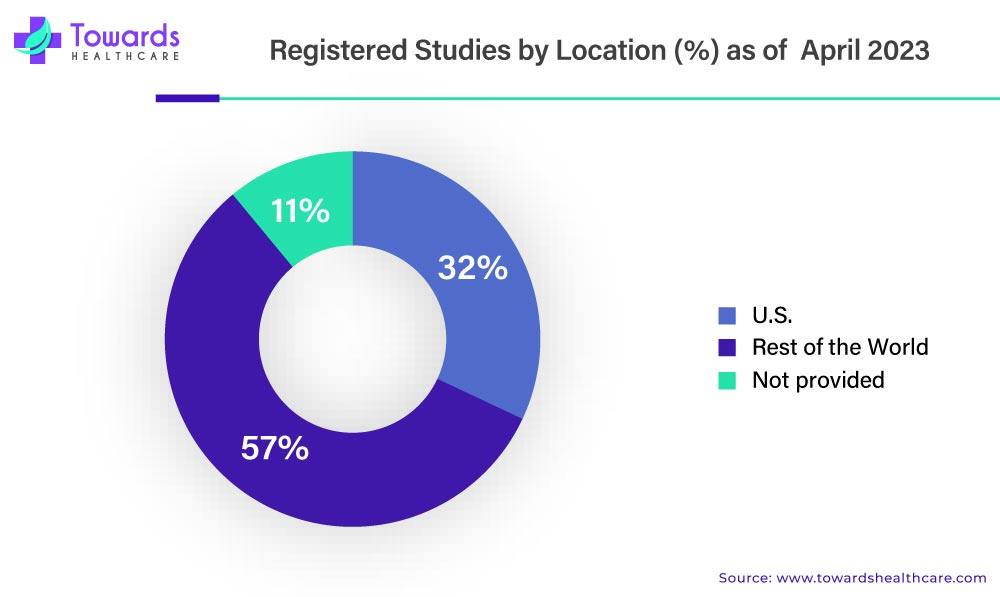

Emerging markets have benefited significantly from supportive policy environments. Countries in Asia-Pacific, Latin America, and parts of Eastern Europe have invested in clinical research infrastructure, streamlined approval processes, and promoted international collaboration. These regions offer diverse patient populations, cost efficiencies, and growing scientific capabilities, making them attractive destinations for global trials. As a result, the clinical trials market is becoming more geographically balanced, reducing overreliance on traditional research hubs.

Technology has perhaps had the most transformative impact on clinical trials, though often in subtle ways. Digital tools now touch every stage of the trial lifecycle. Electronic data capture systems have replaced paper-based records, improving accuracy and accessibility. Clinical trial management systems enable real-time oversight of timelines, budgets, and site performance. Remote monitoring tools allow sponsors to oversee trials without constant on-site visits, reducing costs and increasing flexibility.

Decentralized and hybrid trial models have emerged as practical alternatives to fully site-based studies. By incorporating telemedicine, wearable devices, and home-based data collection, these models reduce the burden on participants and expand access to underrepresented populations. This shift is particularly important for chronic disease trials, where frequent site visits can discourage participation and increase dropout rates. While decentralized trials are not suitable for all studies, their growing adoption signals a broader move toward patient-centric research.

Advanced analytics and artificial intelligence are reshaping trial design and execution. Predictive modeling helps sponsors identify potential risks, optimize site selection, and forecast enrollment challenges before they become critical issues. Machine learning algorithms can analyze large datasets to detect patterns that might otherwise go unnoticed, supporting more informed decision-making. In data-heavy areas such as oncology and genomics, these tools are becoming indispensable.

Despite these advances, the clinical trials market faces persistent challenges. Patient recruitment remains one of the most significant bottlenecks, particularly for rare diseases and narrowly defined populations. Competition for eligible participants is intense, and traditional recruitment strategies often fall short. Addressing this issue requires not only better outreach but also greater transparency, trust-building, and community engagement. Patients today are more informed and more selective, and they expect trials to respect their time, privacy, and individual needs.

Operational complexity is another ongoing concern. Global trials must navigate diverse regulatory requirements, cultural differences, and logistical constraints. Data privacy regulations, while essential, add layers of compliance that require careful management. Maintaining data quality and consistency across multiple sites and countries demands robust systems and experienced oversight. These challenges underscore the importance of skilled professionals who understand both the scientific and operational dimensions of clinical research.

Workforce dynamics also influence market evolution. The demand for experienced clinical research professionals continues to grow, but talent shortages persist in key areas such as biostatistics, data management, and regulatory affairs. Training and retaining skilled personnel has become a strategic priority for organizations across the clinical trials ecosystem. Knowledge transfer, continuous education, and cross-functional collaboration are essential to maintaining quality and innovation.

Looking ahead, the clinical trials market is likely to become even more integrated with real-world evidence generation. The boundary between clinical trials and post-market surveillance is gradually blurring, as regulators and payers seek data on long-term outcomes and real-world effectiveness. This trend will encourage more seamless data collection across the product lifecycle, further expanding the scope and value of clinical research activities.

Sustainability and ethical considerations are also gaining prominence. Sponsors are increasingly mindful of environmental impact, diversity and inclusion, and ethical trial conduct. Inclusive trial designs that reflect real-world populations are no longer aspirational goals; they are becoming regulatory and societal expectations. Addressing these issues requires intentional planning and a willingness to rethink established practices.

From a market perspective, the clinical trials sector is no longer defined solely by volume growth. Its evolution reflects deeper changes in how society approaches healthcare innovation. Trials are becoming more adaptive, more data-driven, and more patient-focused. They serve not only as regulatory requirements but as platforms for learning, collaboration, and continuous improvement.

In this context, success in the clinical trials market depends on strategic alignment rather than isolated excellence. Scientific ambition must align with operational capability. Technological adoption must align with human judgment. Regulatory compliance must align with ethical responsibility. Organizations that recognize and manage these interdependencies will shape the next phase of market development.

After years of observing cycles of hype and correction, one lesson stands out: sustainable progress in clinical trials comes from disciplined innovation. Breakthroughs matter, but so does execution. Incremental improvements in trial design, data quality, and patient engagement often deliver more value than headline-grabbing technologies alone. The market rewards those who combine experience with openness to change.

The current momentum in the clinical trials market suggests that its role in healthcare will continue to expand. As medical challenges grow more complex and expectations rise, clinical trials will remain the proving ground where science meets society. They will test not only new therapies but also new ways of working, collaborating, and thinking about health itself.

In that sense, the question is no longer whether the clinical trials market will grow. The real question is how effectively it will adapt—and who will lead that adaptation with clarity, integrity, and long-term vision.

Access our exclusive, data-rich dashboard dedicated to the healthcare market – built specifically for decision-makers, strategists, and industry leaders. The dashboard features comprehensive statistical data, segment-wise market breakdowns, regional performance shares, detailed company profiles, annual updates, and much more. From market sizing to competitive intelligence, this powerful tool is one-stop solution to your gateway.

Access the Dashboard: https://www.towardshealthcare.com/access-dashboard

Checkout Clinical Trials Market Report Now at: https://www.towardshealthcare.com/checkout/5018

Become a valued research partner with us – https://www.towardshealthcare.com/schedule-meeting

You can place an order or ask any questions, please feel free to contact us at sales@towardshealthcare.com

Powering Healthcare Leaders with Real-Time Insights: https://www.towardshealthcare.com/healthcare-intelligence-platform

Europe Region – +44 778 256 0738

North America Region – +1 8044 4193 44

APAC Region: +91 9356 9282 04

Visit Our Website: https://www.towardshealthcare.com

Find us on social platforms: LinkedIn | Twitter | Instagram | Medium | Pinterest

")

")

")