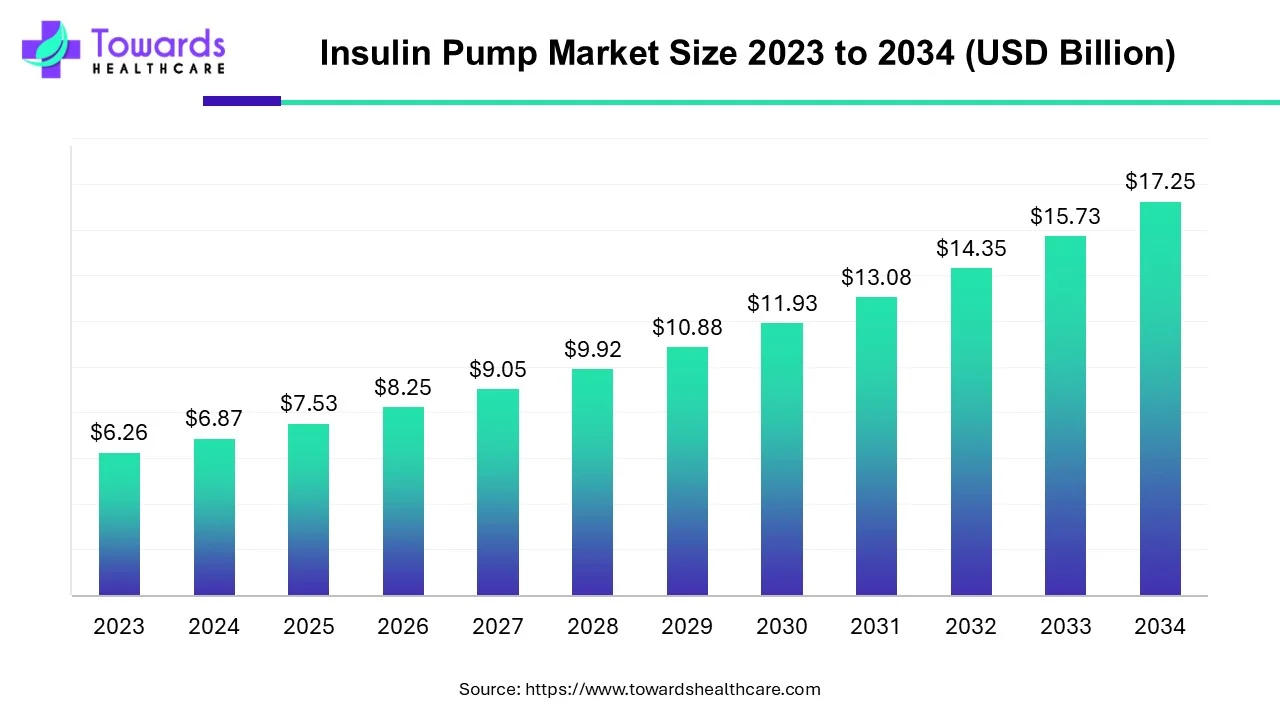

The global Insulin Pump Market is projected to grow from USD 6.87 billion in 2024 to USD 17.25 billion by 2034, expanding at a CAGR of 9.65%, driven by rising diabetes prevalence and continuous innovation in AI-enabled and CGM-integrated insulin pumps.

Download Free Sample of Insulin Pump Market Now and Get the Complete Report Easily at: https://www.towardshealthcare.com/download-sample/5025

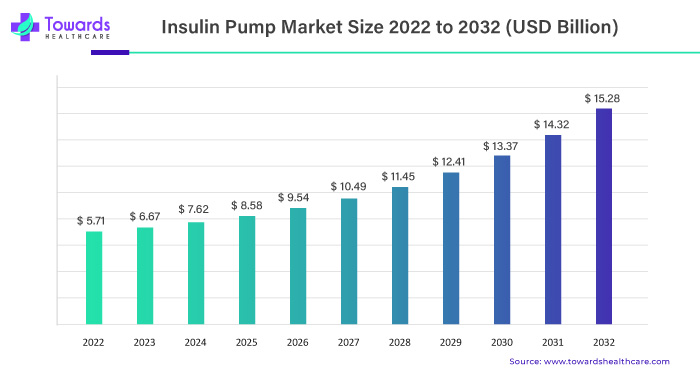

Market Size

Market Value Growth:

2024: USD 6.87 billion

2034: USD 17.25 billion

CAGR: 9.65% (2025–2034)

Strong growth led by AI integration, wearable technologies, and automation of insulin delivery.

Volume Expansion:

Over 12 million active insulin pump users globally in 2024.

Expected to surpass 25 million by 2034, with North America and Europe accounting for over 60% of users.

Revenue Distribution by Region (2024):

North America: ~42%

Europe: ~28%

Asia Pacific: ~22%

Rest of World (Latin America + MEA): ~8%

Forecast Drivers:

Increasing diabetic population—projected to reach 783 million globally by 2045 (IDF).

Higher adoption of closed-loop systems and tubeless pumps.

Profit Margins:

Insulin pump manufacturers enjoy EBITDA margins of 25–30%, especially those offering CGM-integrated smart pumps.

End-Use Contribution:

Hospitals: ~55% of revenue (2024)

Homecare: fastest growth at CAGR >10% due to remote management and geriatric population.

Technological Investment:

Over USD 1.2 billion invested globally (2024–2025) in R&D for AI, CGM, and wireless insulin systems.

Long-Term Growth Catalyst:

Digital health ecosystem integration (AI + mobile app + CGM sensors).

Government support for diabetic care reimbursement (Medicare, NHS, Health Canada).

Market Trends

Integration of CGM and Insulin Pumps:

Tandem and Medtronic integrating continuous glucose monitoring for automated insulin adjustment.

In August 2024, Medtronic partnered with Abbott to integrate FreeStyle Libre technology with its smart insulin systems.

Rise of Patch Pumps:

Compact, tubeless patch pumps gaining preference for convenience and reduced infection risk.

Expected to grow fastest through 2034.

AI-Driven Automation:

AI enabling predictive dose delivery and error reduction, supporting closed-loop insulin systems.

Miniaturization & Portability:

Tandem’s Tandem Mobi, world’s smallest automated insulin pump, launched Feb 2024.

Regulatory Support & Reimbursement Policies:

Medicare and Health Canada support 80%–100% cost reimbursement for qualified devices.

Collaborative Ecosystems:

Tandem’s long-term R&D partnership with University of Virginia (2025) accelerates automated insulin systems.

Shift Toward Homecare Usage:

Increasing geriatric population driving self-administration and remote monitoring.

Personalized Insulin Delivery:

AI algorithms enable adaptive insulin dosing based on patient’s daily glucose trends.

Hybrid Closed-Loop System Approvals:

Health Canada approved Omnipod 5 (April 2024), integrating Dexcom G6 CGM sensor.

Expansion in Emerging Economies:

India and China showing rapid insulin pump adoption due to rising diabetes prevalence and government screening initiatives.

10 Deep AI Impacts / Roles in Insulin Pump Market

Automated Insulin Delivery:

AI regulates insulin release based on CGM data, maintaining glucose levels automatically without manual intervention.

Predictive Dose Adjustment:

Algorithms forecast glucose spikes, adjusting insulin proactively—reducing hypo- and hyperglycemia risks.

Personalized Therapy:

AI tailors insulin doses according to patient’s food intake, activity level, and body metabolism patterns.

Continuous Learning Models:

Machine learning improves accuracy over time by analyzing patient-specific glucose variations.

Integration with Wearables:

Smart AI-enabled devices provide 24×7 health tracking via Bluetooth or smartphone apps.

Remote Monitoring & Telehealth:

AI analytics allow doctors to review data remotely and adjust therapies in real time.

Error Reduction in Dosing:

AI minimizes human error by eliminating manual calculations of insulin bolus doses.

Early Detection of Complications:

AI identifies abnormal glucose fluctuations, predicting diabetic ketoacidosis (DKA) risk early.

Enhanced User Experience:

Voice-assisted or app-based AI interfaces help elderly patients manage pumps easily.

Clinical Research Acceleration:

AI-driven data from millions of users assists in faster clinical trials and new product validation for insulin technologies.

Regional Insights

1. North America (Dominant Region – 42% Market Share in 2024)

Key Drivers:

High obesity and diabetes prevalence (1 in 10 Americans diabetic).

Strong regulatory approval system (FDA).

Major players like Medtronic, Tandem, and Insulet based here.

Reimbursement Advantage:

Medicare Parts A & B cover up to 80% of pump costs.

Adoption Rate:

Over 500,000 Americans on insulin pump therapy.

Growth Catalyst:

Technological integration and automation fueling rapid device replacement cycles.

2. Europe (Second-Largest Region – 28% Market Share)

Drivers:

Aging population and rising diabetes prevalence.

EU “Blueprint for Action on Diabetes 2030” promoting insulin pump adoption.

Key Countries: Germany, U.K., France, Italy, Spain.

Technology Adoption:

Strong preference for MiniMed and Accu-Chek due to CE-certified reliability.

3. Asia Pacific (Fastest-Growing Region – CAGR >10%)

High Disease Burden:

India and China together account for over 230 million diabetics.

Market Trends:

Shift to proactive diabetes management through portable pumps.

Healthcare Transformation:

Urbanization, awareness campaigns, and telemedicine adoption.

4. Latin America & MEA (Emerging Regions)

Latin America: Brazil and Mexico driving growth through public diabetes programs.

MEA: Adoption still limited but improving due to growing healthcare infrastructure in the UAE and Saudi Arabia.

Market Dynamics

Drivers:

Rising Diabetes Prevalence: 783 million projected cases by 2045 (IDF).

Technological Advancement: AI-based closed-loop systems improving therapy precision.

Favorable Reimbursement: Medicare and EU health initiatives boost affordability.

Miniaturization and Comfort: Lightweight, wireless designs improving user compliance.

Restraints:

High Device Cost: Average pump system USD 4,000–6,000 limits adoption in low-income regions.

Training & Skill Requirements: Need for professional guidance in usage.

Hospital Contraindications: Not suitable for unconscious or critical patients.

Opportunities:

Emerging Markets: India and China’s massive diabetic base.

AI and IoT Integration: Data-driven smart diabetes management.

Portable Homecare Devices: Catering to elderly population.

Leaders You Should Know in Insulin Pump Market

Medtronic Plc

Product: MiniMed Series

Overview: Global leader in insulin automation.

Strength: Advanced hybrid closed-loop technology; strong distribution in North America & Europe.

Insulet Corporation

Product: Omnipod 5

Overview: Pioneer of tubeless insulin pumps.

Strength: Compact wireless design, integrated CGM with Dexcom sensors.

Tandem Diabetes Care, Inc.

Product: Tandem Mobi

Overview: Specializes in small automated insulin delivery systems.

Strength: Smartphone-controlled AI insulin pump.

F. Hoffmann-La Roche AG (Accu-Chek)

Product: Accu-Chek Combo

Strength: Strong presence in European healthcare systems.

Ypsomed AG

Product: MyLife Omnipod

Strength: Swiss precision engineering, modular pump systems.

Terumo Corporation

Overview: Focused on infusion technology.

Strength: Expertise in precision needles and tubing.

MicroPort Scientific

Overview: China-based firm in medtech solutions.

Strength: R&D in digital insulin pumps for Asia-Pacific.

Debiotech S.A.

Overview: Swiss company developing microfluidic insulin systems.

Strength: Advanced microneedle technology.

Eoflow Co. Ltd.

Product: EOPatch

Strength: Wireless patch pump technology gaining global traction.

Cequr SA

Product: PaQ Insulin Delivery

Strength: Focus on wearable, discrete insulin devices.

Latest Announcement

Tandem Diabetes Care (Jan 2025):

Collaboration with University of Virginia for research in fully automated closed-loop insulin systems.

Medtronic & Abbott (Aug 2024):

Strategic alliance to integrate FreeStyle Libre with Medtronic insulin delivery systems.

Novo Nordisk (Mar 2024):

Acquired Cardior Pharmaceuticals (EUR 1.025 billion) to expand cardiovascular and diabetic disease synergy.

Recent Developments

Health Canada Approval (Apr 2024):

Approved Omnipod 5, integrated with Dexcom G6, to launch in mid-2025.

Tandem Mobi Launch (Feb 2024):

World’s smallest automated pump predicting and preventing hypo/hyperglycemia.

Medtronic Financial Update (2024):

Reported USD 32.4 billion annual revenue, up 3.6% YoY—diabetes care segment growing fastest.

AI Integration R&D:

Companies investing heavily in algorithmic dosing systems for precision insulin control.

Segments Covered

1. By Type

1.1. Tethered Pumps (Dominant Segment, 2024)

Overview:

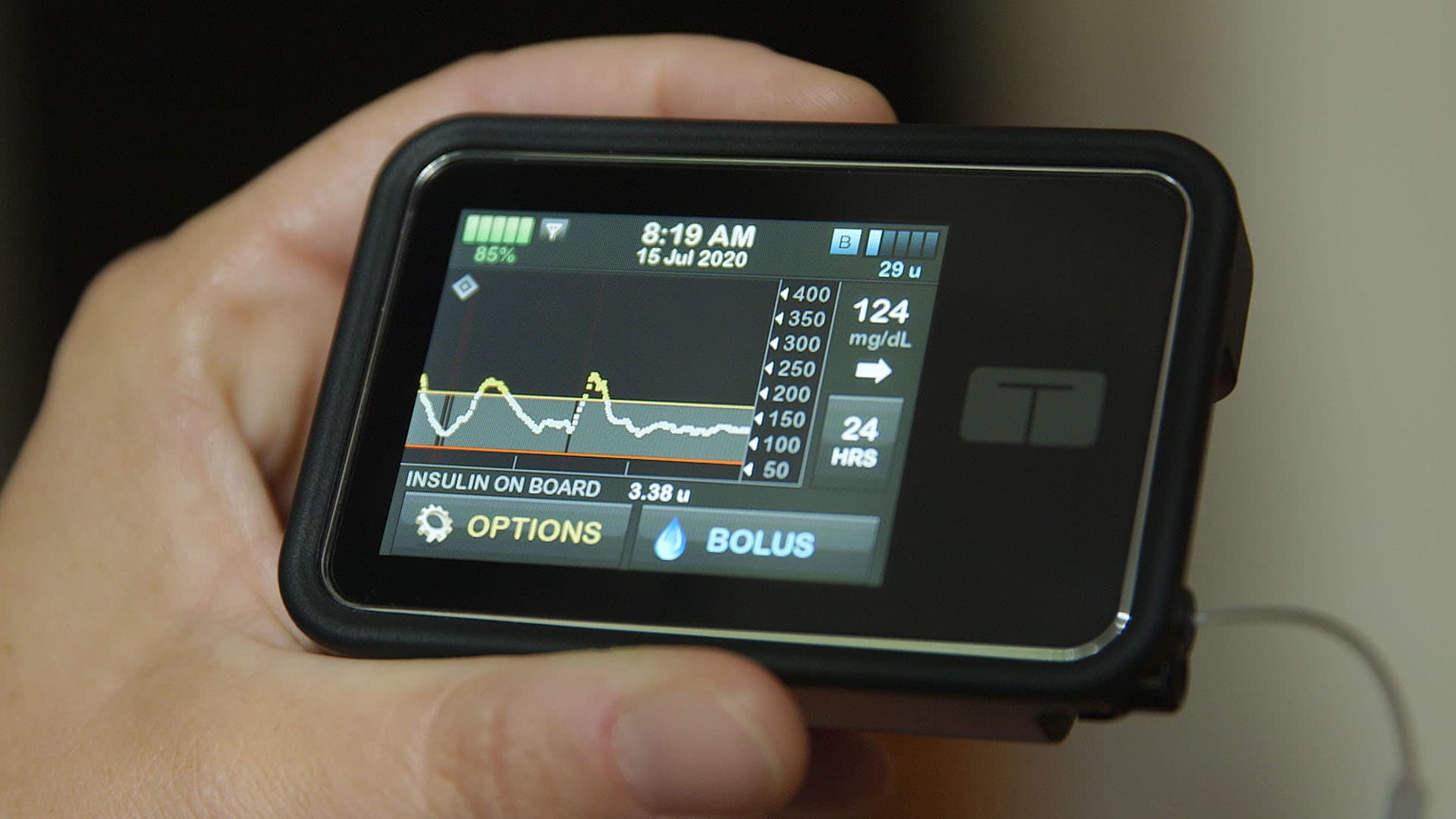

Tethered pumps are traditional insulin pumps attached to the body via a thin plastic tube (infusion set) that delivers insulin from the pump to a cannula inserted under the skin.

Reasons for Dominance:

Affordability: These pumps are cost-effective compared to newer patch or tubeless models.

Display Interface: They feature LCD screens or smartphone-linked displays that allow real-time monitoring of insulin levels.

Custom Dosing: Users can manually program basal and bolus insulin rates depending on their needs.

Reliability: Proven accuracy and fewer insulin delivery errors compared to early-generation patch pumps.

Technological Integration:

Integration with Continuous Glucose Monitoring (CGM) systems to automate dose adjustments.

Example: Medtronic’s MiniMed 780G—a tethered hybrid closed-loop pump that automatically corrects glucose every 5 minutes.

Growth Prospects:

Expected steady growth due to advanced hybrid-loop designs and increased use in hospital settings where physician supervision is preferred.

1.2. Patch Pumps (Fastest-Growing Segment, 2025–2034)

Overview:

Patch pumps are tubeless, adhesive-based devices worn directly on the skin. They deliver insulin through a short cannula inserted under the skin.

Key Features:

Wireless Operation: Controlled via a remote or mobile app (no tubing).

Discreet and Lightweight: Designed for mobility, especially for children and working adults.

Reduced Risk of Infection: Eliminates tubing-related contamination or disconnection.

Growth Drivers:

Ease of Use: Especially suitable for elderly and pediatric patients.

Integration with AI: Many patch pumps feature predictive algorithms to prevent hypo/hyperglycemia.

Example: Insulet’s Omnipod 5, approved in 2024, offers wireless insulin delivery integrated with Dexcom G6 CGM sensors.

Market Potential:

Expected CAGR >12% (2025–2034).

Rising acceptance in homecare and outpatient diabetes management.

2. By Product

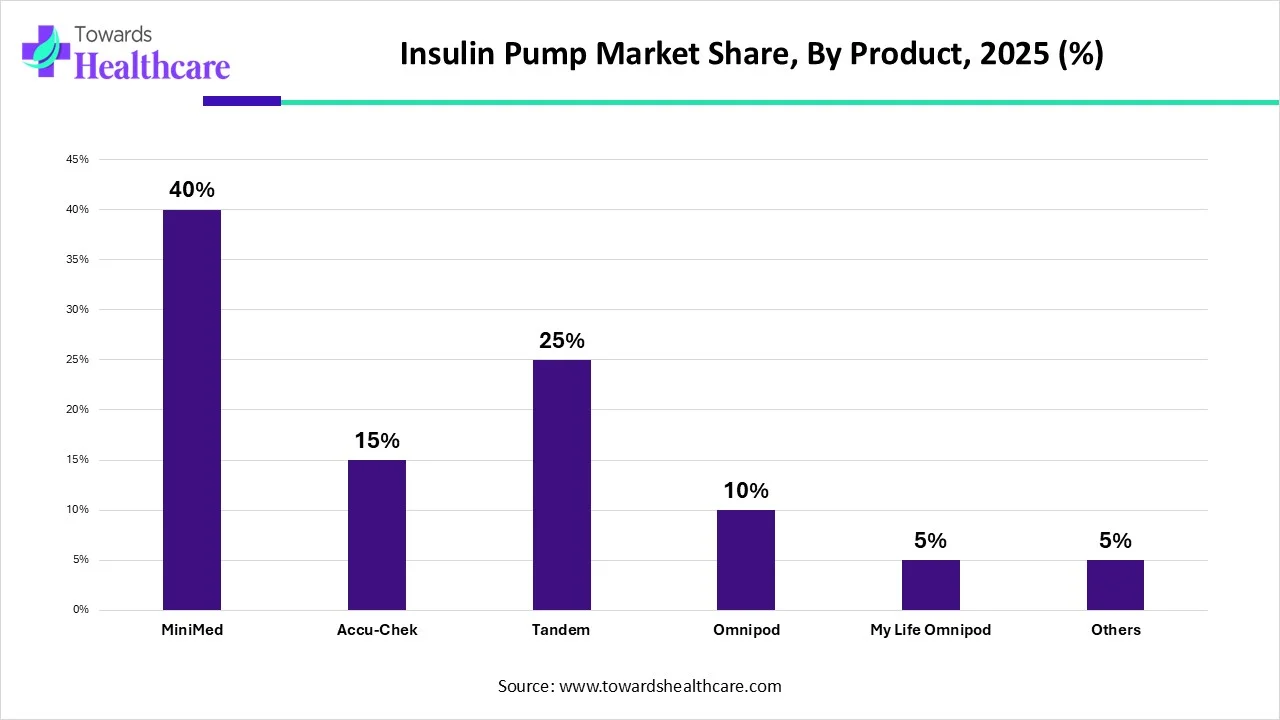

2.1. MiniMed (Largest Market Share, 2024)

Manufacturer: Medtronic Plc

Overview:

MiniMed insulin pumps dominate the market due to their AI-powered automation and strong brand credibility.

Advantages:

Delivers continuous basal insulin and correction boluses automatically.

Integrated with Guardian Sensor 3 CGM system.

Operates 24×7 without fingerpricks, reducing patient burden.

Adoption:

Popular in North America and Europe; used in both Type 1 and Type 2 diabetes.

Market Strength:

Long-standing clinical validation, global distribution, and Medicare reimbursement coverage.

2.2. Tandem (Fastest-Growing Product Segment)

Manufacturer: Tandem Diabetes Care, Inc.

Overview:

Specializes in miniaturized, app-controlled insulin pumps.

Product Highlight: Tandem Mobi – World’s smallest automated insulin delivery system (launched Feb 2024).

Key Features:

Controlled via smartphone (iOS and Android).

Watertight aluminum casing and portable design.

Uses AI algorithms to predict and prevent glycemic events.

Growth Outlook:

Partnership with University of Virginia (2025) to develop fully automated closed-loop systems.

CAGR expected to exceed 13% (2025–2034).

2.3. Accu-Chek, Omnipod, MyLife, Others

Accu-Chek (Roche):

Reliable wired pumps with integrated glucose meters.

Popular in European countries due to established hospital networks.

Omnipod (Insulet):

Tubeless, waterproof patch pumps gaining traction in homecare settings.

MyLife (Ypsomed):

Modular insulin system compatible with multiple infusion sets and cartridges.

3. By Accessories

3.1. Insulin Set Insertion Devices (Leading in 2024)

Function:

Enable precise, consistent placement of cannulas under the skin for insulin delivery.

Advantages:

Simplifies insertion, reducing pain and user error.

Minimizes infection risk through sterile, single-use design.

Enhances consistent insulin absorption.

Market Insights:

Accounts for over 45% of accessory revenue (2024).

Commonly used in both hospital and homecare environments.

Future Outlook:

R&D towards automated insertion devices with disposable integrated sensors.

3.2. Insulin Reservoirs or Cartridges (Fastest-Growing Accessory Segment)

Function:

Store and deliver insulin within the pump; prefilled cartridges are convenient and reduce waste.

Trends:

Lightweight, leak-proof polymer materials enhancing portability.

Integration of safety-lock mechanisms to prevent accidental overdelivery.

Drivers:

Growing patient preference for replaceable cartridges over refillable reservoirs.

Innovation Example:

Medtronic’s Quick-set infusion reservoirs designed for easy attachment and detachment.

4. By Disease Indication

4.1. Type 1 Diabetes (Dominant Segment)

Nature: Autoimmune disorder where the pancreas produces little or no insulin.

Market Share:

Accounts for ~65% of insulin pump users globally (2024).

Reasons for Dominance:

Insulin therapy is a lifelong requirement.

Improved quality of life and glucose control with pump usage.

Technological Impact:

AI-controlled closed-loop systems mimic pancreatic function, reducing glycemic variability.

Integration with smartphone apps allows remote parental monitoring in pediatric cases.

Example:

Medtronic’s MiniMed 780G—FDA approved for patients aged 7+ years with Type 1 diabetes.

4.2. Type 2 Diabetes (Fastest-Growing Segment)

Overview:

Type 2 diabetes patients are increasingly adopting insulin pumps due to uncontrolled glucose levels and insulin resistance.

Growth Factors:

Rising obesity and sedentary lifestyles.

Growing acceptance among healthcare providers for pump therapy in complex cases.

Technology Influence:

Use of automated insulin delivery (AID) systems enhances glycemic control without manual intervention.

Recent Finding:

AI-based systems improved blood glucose control by 25% among Type 2 users in clinical studies.

Market Forecast:

Expected CAGR: 10.5% (2025–2034).

5. By End-Use

5.1. Hospitals & Clinics (Dominant in 2024)

Overview:

Primary site for insulin pump administration, patient training, and clinical supervision.

Key Growth Drivers:

Availability of skilled healthcare professionals and diabetes educators.

Access to advanced medical technologies for continuous glucose monitoring and automated insulin delivery.

Increasing hospitalizations due to diabetes-related complications (e.g., DKA, hyperglycemia).

Adoption in Inpatient Care:

Used for short-term management in surgical or intensive care patients under supervision.

Challenges:

Contraindications include impaired consciousness, psychiatric illness, or lack of trained staff.

5.2. Homecare (Fastest-Growing End-Use Segment)

Overview:

Driven by the rising geriatric population and shift toward self-care.

Market Drivers:

Portable, user-friendly, and tubeless insulin pumps suited for home use.

Integration with mobile apps allows remote monitoring by healthcare providers.

Reimbursement policies cover home-based devices (e.g., Medicare in the U.S.).

Example:

Insulet’s Omnipod 5 allows insulin adjustment via mobile devices, ideal for remote usage.

Outlook:

Expected CAGR: >11% (2025–2034), fastest among end-use categories.

Supported by AI-driven glucose tracking and real-time alerts.

6. Additional Subsegment Insights

Battery Accessories:

Rechargeable or disposable batteries powering pump operation.

Trend toward USB-C rechargeable units for sustainability.

Laboratory Use (Emerging Niche):

Used in clinical trials for insulin delivery efficiency testing and algorithm calibration.

Accounts for small market share (3%) but vital for R&D activities.

Top 5 FAQs

1. What is the projected market size of the insulin pump market by 2034?

The global insulin pump market is expected to reach USD 17.25 billion by 2034, from USD 6.87 billion in 2024, at a CAGR of 9.65%.

2. Which region leads the insulin pump market?

North America dominates the market, supported by strong reimbursement systems and high diabetes prevalence.

3. Which product segment holds the largest share?

MiniMed (Medtronic) segment leads due to advanced automation and continuous insulin delivery systems.

4. What are the key factors driving the market growth?

Rising global diabetes prevalence, AI integration, portable device demand, and supportive reimbursement policies.

5. Which company has the fastest-growing product innovation?

Tandem Diabetes Care with its AI-powered Tandem Mobi insulin pump, launched in 2024, shows the highest growth trajectory.

Access our exclusive, data-rich dashboard dedicated to the medical devices sector – built specifically for decision-makers, strategists, and industry leaders. The dashboard features comprehensive statistical data, segment-wise market breakdowns, regional performance shares, detailed company profiles, annual updates, and much more. From market sizing to competitive intelligence, this powerful tool is one-stop solution to your gateway.

Access the Dashboard: https://www.towardshealthcare.com/access-dashboard

Checkout Insulin Pump Market Report Now at: https://www.towardshealthcare.com/checkout/5025

Become a valued research partner with us – https://www.towardshealthcare.com/schedule-meeting

You can place an order or ask any questions, please feel free to contact us at sales@towardshealthcare.com

Powering Healthcare Leaders with Real-Time Insights: https://www.towardshealthcare.com/healthcare-intelligence-platform

Europe Region – +44 778 256 0738

North America Region – +1 8044 4193 44

APAC Region: +91 9356 9282 04

Visit Our Website: https://www.towardshealthcare.com

Find us on social platforms: LinkedIn | Twitter | Instagram | Medium | Pinterest

")