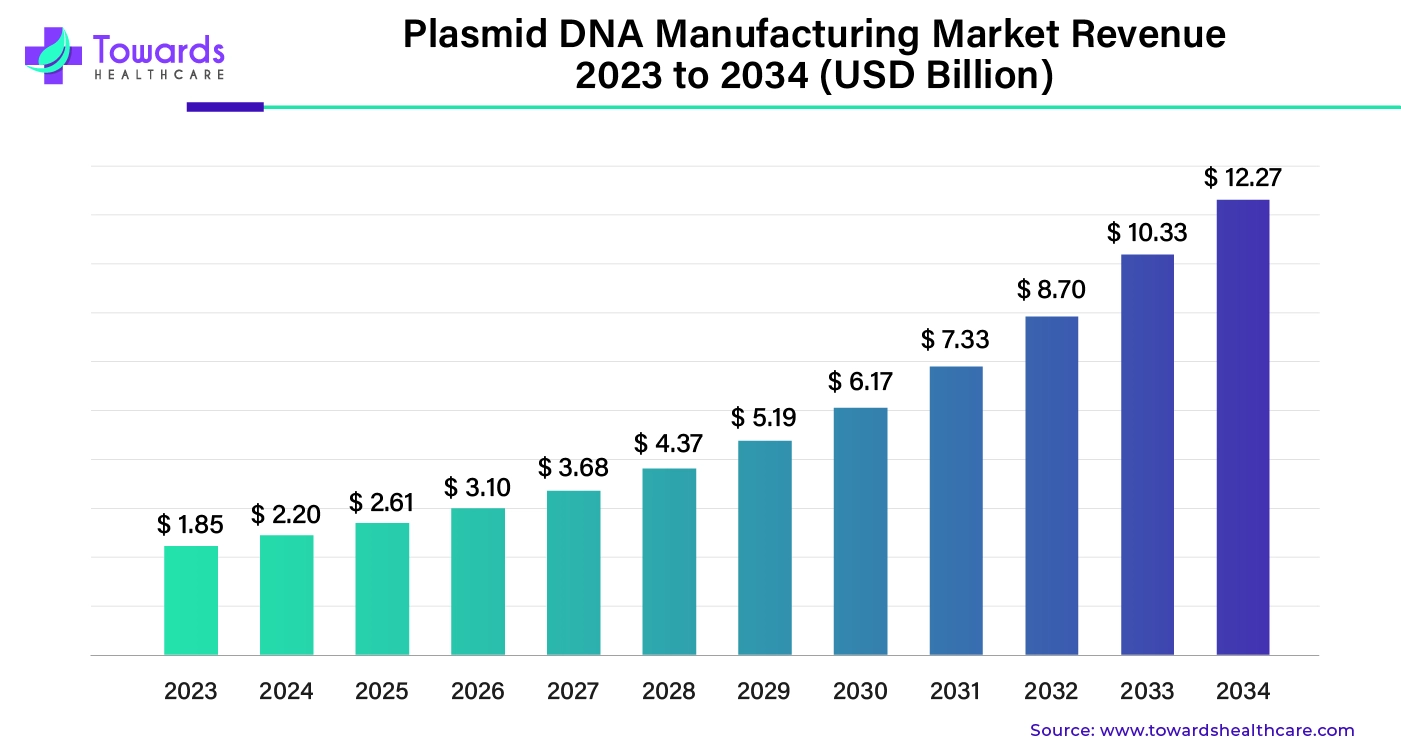

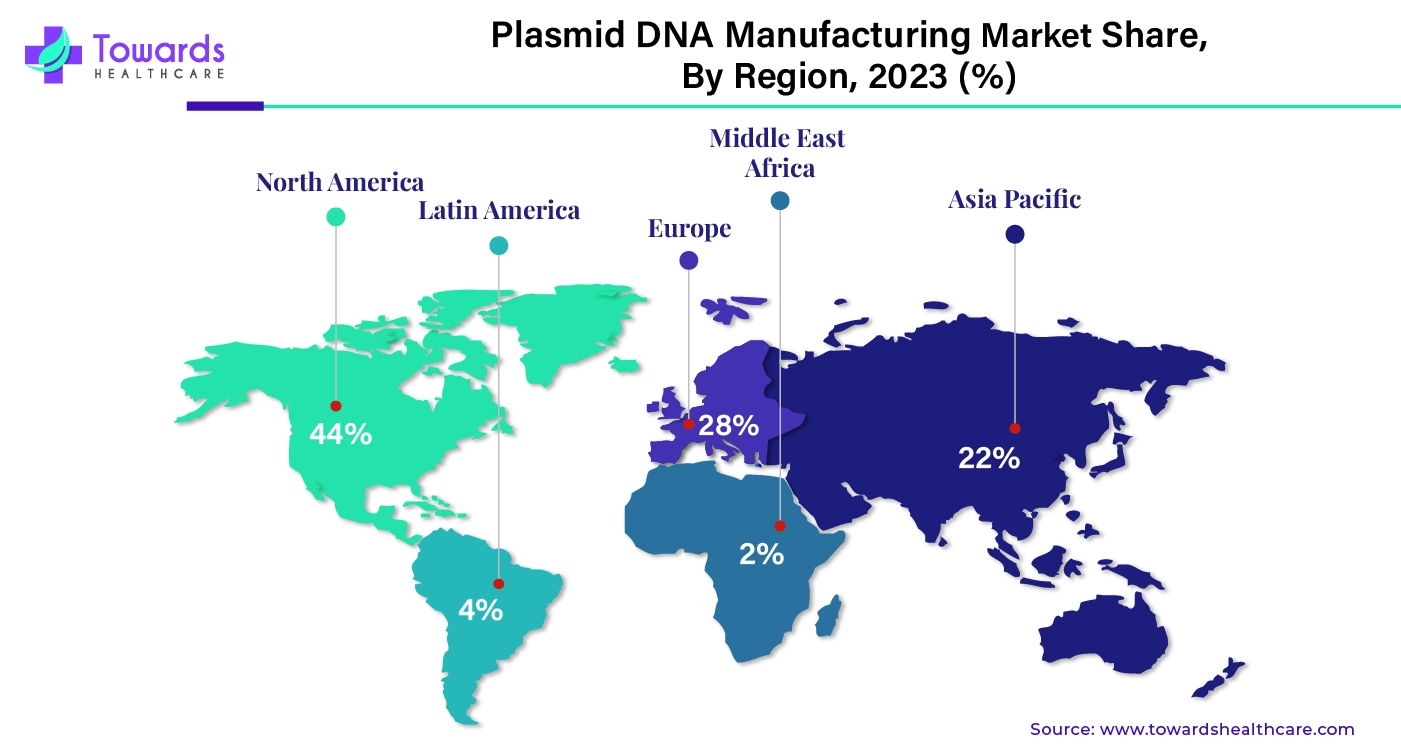

The global plasmid DNA manufacturing market was valued at US$ 1.85 billion in 2023 and is projected to grow to US$ 12.27 billion by 2034, at a CAGR of 18.77% (2024–2034). North America held the largest share (44%) in 2023, while Asia Pacific is projected to grow fastest. Viral vectors dominated by product type, gene therapy led applications, and infectious diseases led disease-based usage. Rising demand in vaccines, gene therapies, and oncology treatments is driving the market.

Download the free sample and get the complete insights and forecasts report on this market @ https://www.towardshealthcare.com/download-sample/5239

Market Size

2023 – US$ 1.85 Billion

◉Market foundation driven by COVID-19 vaccine momentum, early-stage adoption of plasmid DNA in clinical trials, and demand for infectious disease treatments.

◉Viral vectors and plasmids accounted for the bulk of consumption.

2025 – US$ 2.63 Billion

◉Growth driven by expansion of GMP manufacturing facilities such as ProBio’s New Jersey hub and BioNTech’s plasmid DNA plant in Germany.

◉Increased adoption of plasmid-based therapies in oncology and rare disease segments.

2030 – US$ 6.04 Billion

◉Major inflection point: widespread use of plasmid DNA in personalized medicine.

◉Expansion of AI-designed plasmids for higher yield and stability.

◉Strong demand for plasmid-based monoclonal antibodies in cancer treatment.

2034 – US$ 12.27 Billion

◉Plasmid DNA manufacturing becomes a core biomanufacturing industry.

◉Scaling breakthroughs like Kaneka Eurogentec’s 1 kg single-batch production pave the way for industrial-level output.

◉Gene therapy adoption becomes mainstream with over 1 million patients expected to receive plasmid-related therapies annually.

Market Trends

Cancer as a Growth Engine

◉WHO: 35M cancer cases by 2050 (+77% vs 2022).

◉Plasmid DNA enables monoclonal antibody production, personalized gene therapies, and cancer vaccines.

◉Example: NIH expects 1.09M patients in the U.S. will receive gene therapy by 2034.

Vaccine Demand & Population Growth

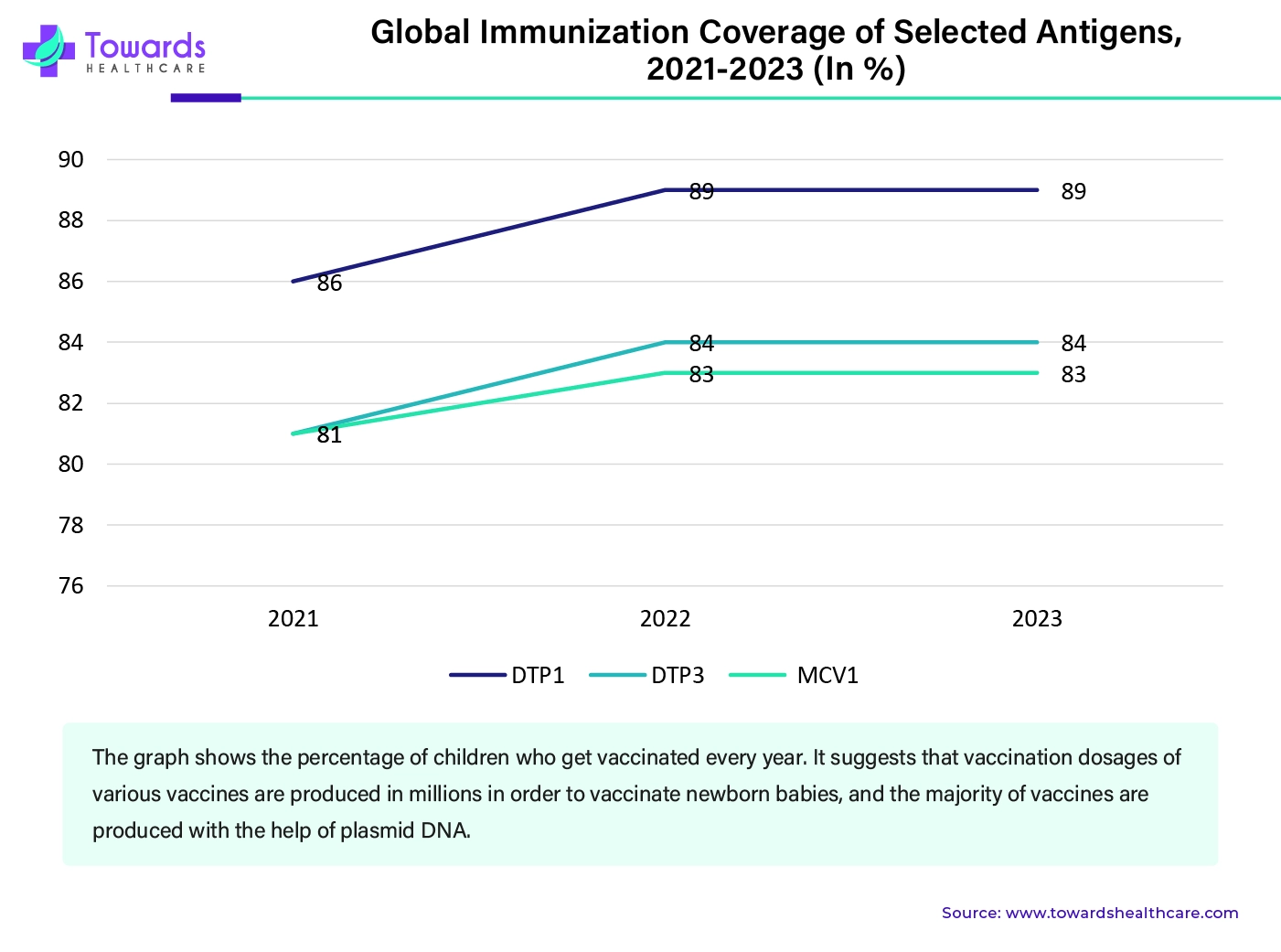

◉140M babies born annually, all requiring multiple vaccines.

◉Plasmid DNA increasingly used in DNA vaccines for diseases like influenza, Zika, and COVID-19 variants.

AI-Driven DNA Editing & Design

◉Profluent’s OpenCRISPR-1 (2024): first open-source AI gene editor, designed molecules for altering human DNA.

◉AI enhances affordability, precision, and efficiency in plasmid DNA design and production.

Viral Vector Dominance

◉Viral vectors remain the preferred method for genetic material delivery.

◉Industry needs 2–3 billion liters/year of bioreactor capacity, expected to increase further as therapies scale.

CDMO Expansion & Outsourcing

◉Outsourcing plasmid production is booming, reducing costs for pharma firms.

◉Example: Charles River & Ship of Theseus CDMO deal (2024) strengthens contract GMP plasmid DNA manufacturing.

Breakthroughs in Manufacturing Scale

◉Kaneka Eurogentec (2024): first to achieve 1 kg plasmid DNA in one fermentation run.

◉This removes bottlenecks in large-scale therapy and vaccine production.

AI’s Role in the Market

Yield Stabilization

◉Traditional plasmid production yields are inconsistent.

◉AI-driven predictive fermentation control reduces instability and improves batch reliability.

Precision Gene Editing

◉AI ensures lower off-target mutations in CRISPR and other editing methods.

◉Example: OpenCRISPR-1 highlights AI-designed editors that outperform manual processes.

Therapy Personalization

◉AI analyzes genomic and patient data to create customized therapies.

◉Enables personalized cancer vaccines and rare disease therapies, improving patient outcomes.

Optimized Drug Design & Simulation

◉AI models simulate plasmid stability under stress, storage, and transport conditions.

◉Reduces need for physical trials, saving time and cost.

Clinical Trial Data Handling

◉AI manages large genomic datasets from trials, improving regulatory compliance and accelerating drug approvals.

Next-Generation Plasmid Development

◉AI develops plasmids with improved resistance to degradation, extending shelf-life.

◉Supports mass vaccination programs in developing regions.

Regional Insights

North America (44% Share, 2023 – Market Leader)

◉North America is the dominant regional hub in the plasmid DNA and advanced therapy market, contributing nearly half of the global revenue in 2023.

Strengths:

◉The U.S. and Canada are home to leading biotechnology companies such as Charles River Laboratories, Thermo Fisher Scientific, and ProBio, which provide both in-house plasmid manufacturing and contract development services (CDMOs). The region benefits from an advanced R&D ecosystem, driven by strong collaborations between universities, private pharma, and government initiatives. Government support—particularly through the NIH, BARDA, and FDA—provides funding, regulatory guidance, and incentives for innovation.

Therapy Demand:

◉The National Institutes of Health (NIH) projects that the number of patients requiring gene therapies will reach 1.09 million by 2034, creating unprecedented demand for plasmid DNA as a core raw material for viral vectors and cell therapies.

Recent Development:

◉In April 2024, ProBio launched a GMP plasmid DNA manufacturing facility in New Jersey, strategically boosting the U.S. supply chain and reducing reliance on imports. This development enhances supply security, a critical factor given rising concerns about manufacturing bottlenecks.

Europe

◉Europe holds a strong second position, driven by robust academic research, policy initiatives, and growing biotech clusters.

Strengths:

◉Governments actively support advanced therapy medicinal products (ATMPs) through funding programs and regulatory flexibility. The European Medicines Agency (EMA) has accelerated approval pathways for gene therapies, fostering faster commercialization.

United Kingdom:

◉The UK prioritizes rare disease therapies and promotes industry–government collaborations. The NHS is increasingly integrating gene and cell therapies into its healthcare system, making it a model for structured adoption.

Germany:

◉Germany stands out as a biotech leader in Europe. In 2023, BioNTech inaugurated a plasmid DNA manufacturing plant dedicated to vaccines and oncology therapies. This investment strengthens Europe’s local supply chain and reduces dependence on U.S. and Asian suppliers.

Asia Pacific (Fastest Growth Region)

◉The Asia Pacific market is projected to experience the highest CAGR through 2034, driven by population size, rising healthcare demand, and strong biotech investments.

China:

◉With an aging population expected to surpass 400 million above the age of 60 by 2030, China faces increasing demand for treatments addressing cancer, cardiovascular diseases, and age-related disorders. The government is heavily investing in biotech innovation zones, clinical trial expansions, and local manufacturing capabilities to reduce dependency on Western suppliers.

India:

◉Ranked as the third-largest biotech hub in Asia-Pacific.

◉Successfully developed the world’s first DNA-based COVID-19 vaccine (ZyCoV-D by Zydus Cadila), showcasing innovation capacity.

◉Hosts the second-highest number of USFDA-approved manufacturing plants globally, giving it a competitive edge in low-cost, large-scale plasmid DNA and biologics manufacturing.

Japan:

◉Japan is a mature biotech market with heavy government and private-sector investment in life sciences. It boasts a strong pharmaceutical industry, a highly developed regulatory framework, and initiatives to position Japan as a global leader in gene therapies and regenerative medicine.

Latin America & Middle East & Africa (Emerging but Challenged)

◉These regions are at a nascent stage, with opportunities emerging primarily through vaccine demand and healthcare expansion programs.

Growth Factors:

◉Expanding healthcare access and national immunization programs.

◉Growing collaborations with global biotech firms to expand reach.

Challenges:

◉Limited advanced manufacturing facilities hinder local plasmid production.

◉Reliance on imports and CDMO partnerships for critical raw materials.

◉Regulatory environments are still developing, slowing adoption of ATMPs.

Market Dynamics

Drivers

Rising Cancer Incidence

◉The WHO projects a 77% increase in cancer cases by 2050. Gene and cell therapies, which rely on plasmid DNA as a starting material, are increasingly being developed for oncology applications such as CAR-T cell therapy.

Growing Vaccine Demand

◉With 140 million children born each year globally, vaccines remain a cornerstone of healthcare. DNA plasmids are central to next-generation vaccines against infectious diseases like COVID-19, influenza, and RSV.

Expansion of Gene Therapy Trials

◉Over 5,000+ gene therapy clinical trials were ongoing in 2023, highlighting the massive pipeline of therapies that depend on plasmid DNA.

AI-Driven Innovation

◉Artificial intelligence is being applied to plasmid design and optimization, improving yield, reducing production time, and increasing manufacturing efficiency.

Restraints

Regulatory Risks

◉Strict regulations due to biothreat risks and GMO leakage significantly slow approvals and increase compliance costs.

High Costs of ATMPs

◉The average cost of advanced therapies can exceed $1–2 million per patient, limiting adoption despite clinical efficacy.

Opportunities

Scalable Manufacturing

◉Kaneka Eurogentec’s record 1 kg plasmid run (2024) demonstrated a breakthrough in scalability, lowering costs and enabling commercial-scale production.

Expanding CDMO Industry

◉Outsourcing to CDMOs reduces entry barriers for pharma companies, allowing smaller biotechs to develop gene therapies without heavy CAPEX investments.

Challenges

Capacity Shortages

◉Demand for viral vectors requires 2–3 billion liters of plasmid fermentation annually, far exceeding current capacity.

Slow ATMP Adoption

◉Despite regulatory approvals, adoption is slow due to limited durability data, affordability issues, and reimbursement challenges.

Top Companies

Twist Bioscience

Product: Semiconductor-based DNA synthesis platform.

Strengths: High-throughput, precise, and scalable synthetic DNA production.

Performance: Reported $96.1M in Q3 FY2025 revenue (+18% YoY growth), reflecting strong demand in synthetic biology and gene therapy markets.

Charles River Laboratories

Product: End-to-end plasmid DNA and viral vector manufacturing services.

Strengths: Established CDMO presence, global reach, trusted by leading pharma/biotech firms.

Revenue: Achieved $4.05B in 2024, with plasmid services contributing to growth.

Thermo Fisher Scientific

Product: PlasmidPro, an automated plasmid purification solution (mini-to-maxi scale).

Strengths: A global biotech leader with automation-driven platforms reducing time-to-market for therapies.

Bionova Scientific (Asahi Kasei Group)

Product: CDMO plasmid DNA production.

Strengths: Invested $100M in a Texas facility (100,000 sq. ft.) to expand plasmid DNA production and cater to U.S. demand.

VGXI & Aldevron

Strengths: Long-standing expertise in plasmid DNA supply for both vaccines and therapeutic applications. Trusted partners for biotech firms seeking high-quality, GMP-grade plasmids.

Latest Announcements

◉ProBio (April 2025): Launched GMP plasmid DNA manufacturing facility in New Jersey, ensuring predictable delivery timelines.

◉EU Policy (May 2025): European regulators introduced reforms to increase affordability and access to ATMPs, aiming to boost adoption.

Recent Developments

◉Kaneka Eurogentec (2024): Achieved 1 kg plasmid DNA output in a single fermentation batch – a scalability milestone.

◉Charles River & Ship of Theseus (2024): Entered a CDMO partnership to expand GMP plasmid DNA services.

◉BioNTech (2023): Opened its own plasmid DNA facility in Germany, securing supply for infectious disease vaccines and oncology therapies.

Segments Covered

Top 5 FAQs

Q1. What is the size of the plasmid DNA manufacturing market?

A1. Valued at US$ 1.85B in 2023, projected to reach US$ 12.27B by 2034 at a CAGR of 18.77%.

Q2. Which region dominated in 2023?

A2. North America held 44% share due to strong biotech/pharma industry and high R&D.

Q3. Why is plasmid DNA important in vaccines?

A3. Used for DNA vaccine production – essential since 140M babies born yearly need multiple immunizations.

Q4. How does AI impact plasmid DNA manufacturing?

A4. AI improves plasmid stability, precision in editing, personalized therapies, and large-scale manufacturing efficiency.

Q5. Which company achieved a breakthrough in plasmid production?

A5. Kaneka Eurogentec (2024) produced 1 kg plasmid DNA in one fermentation run, a record-setting milestone.

Check out the details below

Access our exclusive, data-rich dashboard dedicated to the healthcare market – built specifically for decision-makers, strategists, and industry leaders. The dashboard features comprehensive statistical data, segment-wise market breakdowns, regional performance shares, detailed company profiles, annual updates, and much more. From market sizing to competitive intelligence, this powerful tool is one-stop solution to your gateway.

Access the Dashboard: https://www.towardshealthcare.com/access-dashboard

Immediate Delivery Available | Buy This Premium Research @ https://www.towardshealthcare.com/price/5239

Become a valued research partner with us – https://www.towardshealthcare.com/schedule-meeting

You can place an order or ask any questions, please feel free to contact us at sales@towardshealthcare.com

Powering Healthcare Leaders with Real-Time Insights: https://www.towardshealthcare.com/healthcare-intelligence-platform

Europe Region – +44 778 256 0738

North America Region – +1 8044 4193 44

Web: https://www.towardshealthcare.com

Find us on social platforms: LinkedIn | Twitter | Instagram | Medium | Pinterest