Is Liquid Biopsy Changing How Cancer Is Diagnosed and Treated in the U.S 2026.?

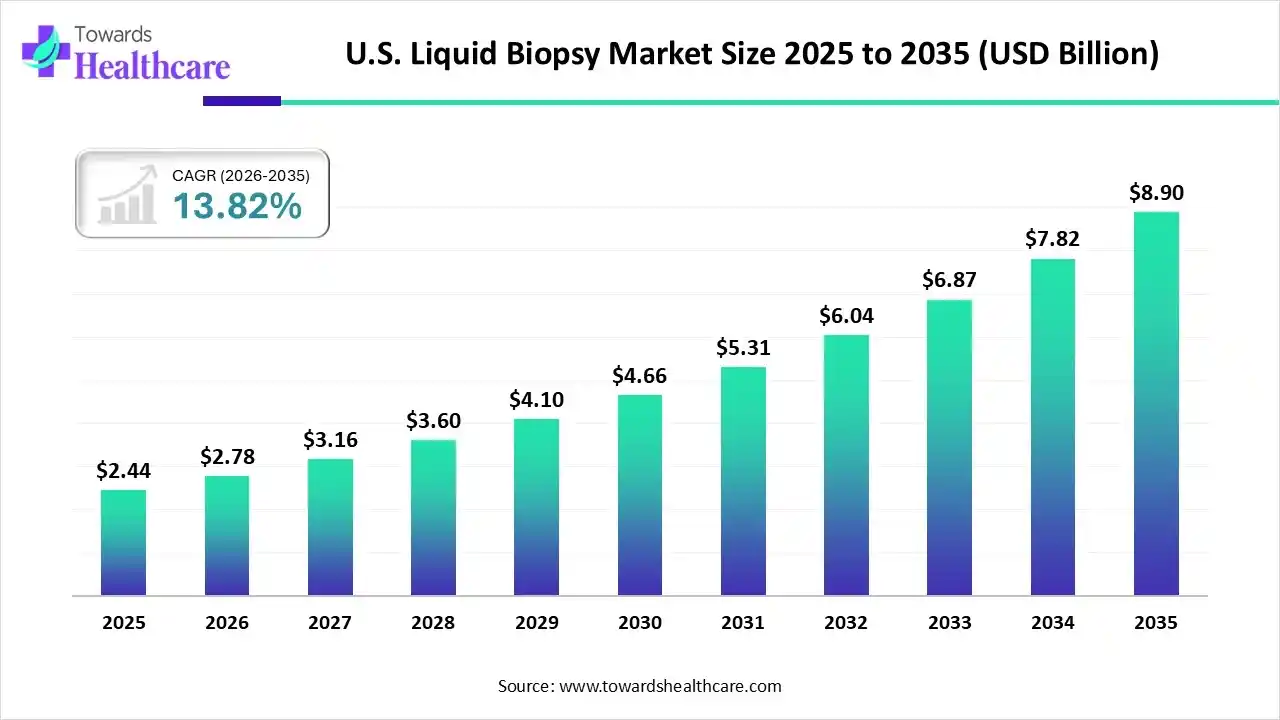

For more than a decade, the U.S. healthcare ecosystem has searched for diagnostic solutions that are faster, safer, and more precise. Liquid biopsy has steadily moved from being an experimental concept discussed in research conferences to a clinically relevant diagnostic approach that is reshaping how cancer is detected, monitored, and treated. As of 2025, the U.S. liquid biopsy market stood at USD 2.44 billion, reflecting not only technological progress but also a deeper shift in clinical philosophy. Physicians, researchers, and patients are increasingly favoring methods that minimize physical burden while maximizing diagnostic insight. With projections showing the market reaching approximately USD 8.90 billion by 2035 at a CAGR of 13.82 percent, liquid biopsy is no longer a peripheral innovation. It has become a central pillar of precision oncology in the United States.

𝐃𝐨𝐰𝐧𝐥𝐨𝐚𝐝 𝐅𝐫𝐞𝐞 𝐒𝐚𝐦𝐩𝐥𝐞:

https://www.towardshealthcare.com/download-sample/6572

This growth does not emerge from hype alone. It is the result of converging forces: rising cancer incidence, advances in genomics, improved sequencing platforms, and a healthcare system that now recognizes the value of early and continuous disease monitoring. Liquid biopsy addresses some of the most persistent limitations of traditional tissue biopsy, including invasiveness, sampling bias, and inability to capture tumor heterogeneity over time. By accessing cancer-derived material circulating in blood or other biofluids, clinicians gain a dynamic and more comprehensive view of disease biology.

Why Non-Invasive Diagnostics Are No Longer Optional

Cancer care in the U.S. is under pressure from multiple directions. An aging population, increasing prevalence of chronic diseases, and rising treatment costs have exposed inefficiencies in conventional diagnostic pathways. Tissue biopsy, while still essential, often fails to meet the demands of modern oncology. It requires surgical intervention, carries procedural risks, and provides only a snapshot of a tumor at a single moment in time.

Liquid biopsy changes this paradigm by offering repeatable, non-invasive testing that can track disease progression in real time. This capability aligns directly with the growing emphasis on precision medicine, where treatment decisions depend on molecular profiles rather than anatomical location alone. As awareness of early cancer detection benefits increases among clinicians and patients alike, liquid biopsy has gained acceptance not just as an alternative, but as a complementary and sometimes superior diagnostic approach.

The U.S. market reflects this transition clearly. By 2026, the market is expected to surpass USD 2.78 billion, signaling sustained confidence from healthcare providers, payers, and technology developers. The rapid adoption of liquid biopsy tests for therapy selection, minimal residual disease detection, and recurrence monitoring underscores their expanding role in standard oncology workflows.

The Science Powering Liquid Biopsy Adoption

At the heart of liquid biopsy lies the ability to detect and analyze tumor-derived biomarkers such as circulating tumor DNA, circulating tumor cells, RNA fragments, proteins, and extracellular vesicles. Among these, circulating tumor DNA has emerged as the dominant biomarker in the U.S. market. Its sensitivity, compatibility with next-generation sequencing, and proven utility in early detection and therapy guidance have positioned it as the backbone of most liquid biopsy assays.

However, the field is not static. RNA-based biomarkers, including microRNA and messenger RNA, are gaining attention due to their stability in blood and their ability to reflect real-time gene expression changes. These biomarkers provide functional insights that DNA alone cannot offer, making them particularly valuable for prognosis and treatment response monitoring. As sequencing technologies evolve and analytical pipelines mature, RNA is expected to grow at the fastest rate among biomarker categories during the forecast period.

Technological platforms have also played a decisive role in market expansion. Next-generation sequencing currently dominates the U.S. liquid biopsy landscape because it enables simultaneous analysis of multiple genetic alterations with high accuracy. Reduced sequencing costs and faster turnaround times have made NGS more accessible across clinical settings. At the same time, epigenetic analysis is emerging as a high-growth area, driven by its ability to detect cancer-specific DNA methylation patterns that often appear early in disease development.

From Diagnosis to Disease Surveillance

One of the most defining features of the U.S. liquid biopsy market is its broad application across the cancer care continuum. In 2025, therapy selection and companion diagnostics represented the largest application segment. Oncologists increasingly rely on liquid biopsy results to identify actionable mutations, select targeted therapies, and avoid ineffective treatments. This approach not only improves clinical outcomes but also reduces unnecessary healthcare spending.

Yet the fastest growth is occurring in minimal residual disease detection. The ability to detect microscopic traces of cancer after treatment has profound implications for patient management. By identifying relapse earlier than imaging or clinical symptoms, MRD testing allows clinicians to intervene sooner, adjust therapies, and potentially improve survival outcomes. This shift toward proactive monitoring reflects a more nuanced understanding of cancer as a dynamic disease rather than a one-time event.

Liquid biopsy has also proven particularly valuable in treatment response monitoring and recurrence surveillance. Repeated blood-based testing provides insights into how tumors evolve under therapeutic pressure, enabling timely adjustments to treatment strategies. This dynamic monitoring capability is increasingly viewed as essential in an era where resistance mechanisms can emerge rapidly.

Cancer Types Driving Market Momentum

Not all cancers contribute equally to liquid biopsy adoption, and the U.S. market data reflects this reality. Lung cancer remains the dominant indication area, largely due to its high prevalence and the clinical need for molecular profiling to guide targeted therapies. Liquid biopsy has become an indispensable tool in managing non-small cell lung cancer, where tissue samples are often difficult to obtain and rapid treatment decisions are critical.

Pancreatic cancer, although less prevalent, represents the fastest-growing segment. Its typically late diagnosis and poor prognosis have driven intense research interest in early detection strategies. Liquid biopsy offers a promising solution by enabling earlier identification of disease and closer monitoring of treatment response. As clinical evidence continues to accumulate, adoption in this segment is expected to accelerate.

Breast, colorectal, prostate, and other solid tumors also contribute significantly to market growth, supported by rising cancer incidence and expanding test availability. The estimated 2,041,910 new cancer cases in the U.S. in 2025 highlight the scale of the diagnostic challenge and the urgent need for scalable, patient-friendly solutions.

Clinical Settings and Business Models Evolving Together

The dominance of reference laboratories in the U.S. liquid biopsy market reflects the complexity of testing and data interpretation. These laboratories possess the infrastructure, expertise, and quality control systems necessary to deliver reliable results at scale. Their partnerships with hospitals, oncologists, and biopharmaceutical companies have solidified their position as central players in the diagnostic ecosystem.

At the same time, biopharmaceutical and biotechnology companies represent the fastest-growing end-user segment. Their investment in biomarker-driven drug development and companion diagnostics has created a strong demand for liquid biopsy technologies that can support clinical trials and regulatory submissions. This close integration between diagnostics and therapeutics underscores the strategic importance of liquid biopsy in modern drug development.

Business models are also evolving. Centralized testing labs continue to dominate due to regulatory requirements and the need for specialized expertise. However, direct-to-consumer testing models are gaining traction as consumer awareness increases and at-home diagnostic solutions become more sophisticated. While DTC testing raises questions around data interpretation and clinical follow-up, its rapid growth signals a broader shift toward patient-centric healthcare.

The Role of Software, Bioinformatics, and AI

As liquid biopsy generates vast amounts of genomic and molecular data, software and bioinformatics tools have become indispensable. This segment is projected to grow at the fastest rate, driven by the need for accurate data interpretation, integration with electronic health records, and real-time clinical decision support. Advanced analytics platforms now translate complex sequencing outputs into actionable insights for clinicians.

Artificial intelligence further amplifies this capability. Machine learning algorithms can identify subtle patterns in ctDNA and CTC data that may escape traditional analysis. AI-driven tools enable predictive modeling of disease progression, treatment response, and relapse risk. By automating data interpretation, AI reduces variability, accelerates decision-making, and supports scalable deployment of liquid biopsy solutions across diverse clinical settings.

The integration of AI does not replace clinical expertise; rather, it augments it. Experienced oncologists and pathologists increasingly rely on AI-powered insights to inform complex treatment decisions. This collaboration between human judgment and machine intelligence represents one of the most promising frontiers in precision oncology.

Government Support and Regulatory Momentum

Government initiatives have played a critical role in advancing the U.S. liquid biopsy market. Continued investment from federal agencies in 2025 reinforced the strategic importance of early cancer detection and precision oncology. Research consortia supported by national institutions have accelerated biomarker validation and fostered collaboration between academia and industry.

Regulatory pathways, while rigorous, have become more defined as liquid biopsy technologies mature. FDA authorizations for pan-solid tumor assays and companion diagnostics signal growing regulatory confidence. At the same time, initiatives aimed at precompetitive collaboration have reduced duplication of effort and accelerated innovation. These developments create a more predictable environment for technology developers and investors alike.

Competitive Landscape Shaped by Innovation

The U.S. liquid biopsy market features a mix of established diagnostics companies and specialized innovators. Organizations such as Guardant Health, Foundation Medicine, Exact Sciences, Illumina, and Thermo Fisher Scientific have built strong portfolios that span assay development, sequencing platforms, and clinical services. Their continued investment in research and clinical validation reinforces market confidence.

Competition in this space centers not only on test accuracy but also on turnaround time, scalability, and clinical utility. Companies that can demonstrate clear impact on patient outcomes are best positioned to succeed. Recent product launches and research presentations highlight an industry that continues to push technical and clinical boundaries.

Challenges That Demand Attention

Despite its promise, liquid biopsy faces challenges that cannot be ignored. High testing costs remain a barrier to widespread adoption, particularly in smaller healthcare settings. Variability in assay performance and lack of standardization across laboratories complicate result interpretation. Reimbursement policies also lag behind technological progress, creating uncertainty for providers and patients.

Data privacy and ethical considerations add another layer of complexity. As genomic data becomes more central to diagnosis and treatment, safeguarding patient information is paramount. Addressing these challenges requires coordinated efforts from regulators, industry stakeholders, and healthcare providers.

Looking Ahead with Measured Confidence

The future of the U.S. liquid biopsy market appears robust, but its success will depend on disciplined execution rather than unchecked optimism. Continued technological innovation must align with clinical needs and regulatory expectations. Education efforts targeting physicians and patients will play a crucial role in driving informed adoption.

As liquid biopsy expands beyond oncology into areas such as cardiovascular and infectious disease diagnostics, its broader healthcare impact will become clearer. For now, its role in cancer care alone justifies the attention and investment it continues to receive. With strong growth projections, expanding clinical applications, and sustained government support, liquid biopsy stands poised to redefine how cancer is detected and managed in the United States.

From the perspective of a market observer with more than a decade of experience in oncology diagnostics, this evolution feels less like a sudden disruption and more like a long-anticipated correction. The healthcare system is finally aligning diagnostic capability with the biological complexity of cancer. Liquid biopsy is not a distant future concept. It is already reshaping the present, and its influence will only deepen in the years ahead.

Access our exclusive, data-rich dashboard dedicated to the diagnostics sector – built specifically for decision-makers, strategists, and industry leaders. The dashboard features comprehensive statistical data, segment-wise market breakdowns, regional performance shares, detailed company profiles, annual updates, and much more. From market sizing to competitive intelligence, this powerful tool is one-stop solution to your gateway.

Access the Dashboard: https://www.towardshealthcare.com/access-dashboard

Checkout U.S. Liquid Biopsy Market Report Now at: https://www.towardshealthcare.com/checkout/6572

Become a valued research partner with us – https://www.towardshealthcare.com/schedule-meeting

You can place an order or ask any questions, please feel free to contact us at sales@towardshealthcare.com

Powering Healthcare Leaders with Real-Time Insights: https://www.towardshealthcare.com/healthcare-intelligence-platform

Europe Region – +44 778 256 0738

North America Region – +1 8044 4193 44

APAC Region: +91 9356 9282 04

Visit Our Website: https://www.towardshealthcare.com

Find us on social platforms: LinkedIn | Twitter | Instagram | Medium | Pinterest

Table of Contents

Toggle