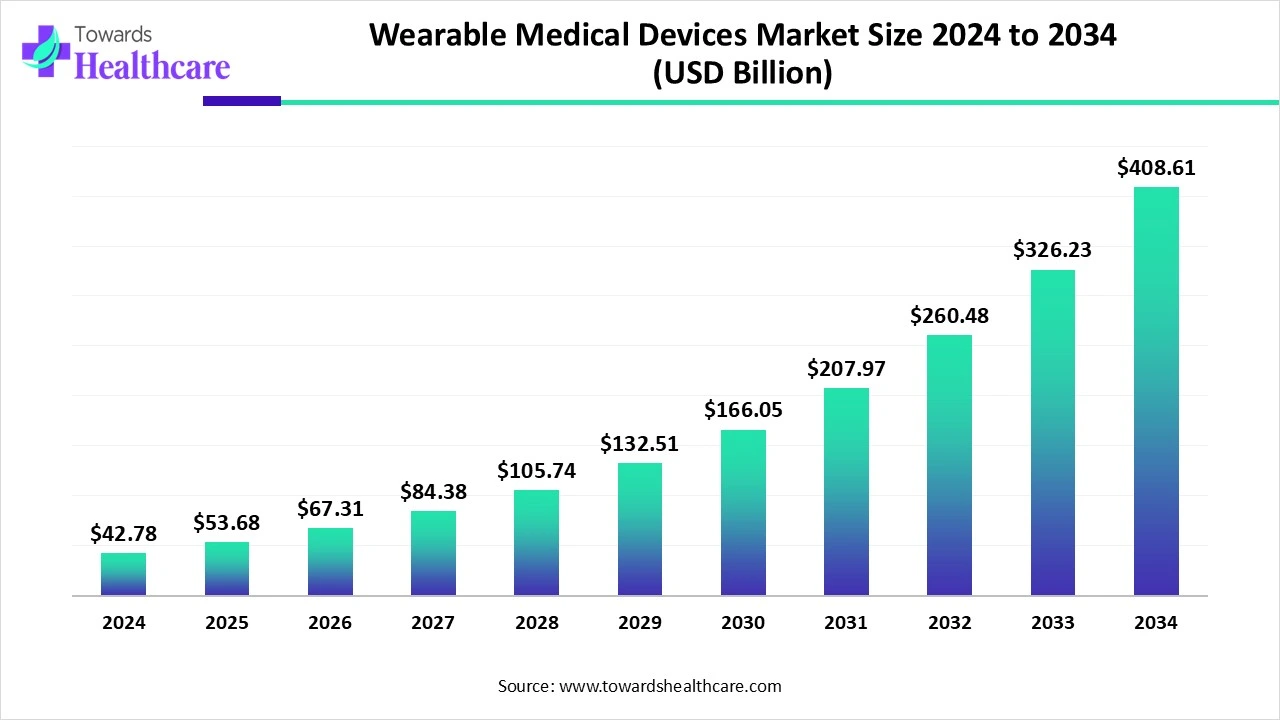

The global wearable medical devices market was USD 42.78 billion in 2024, rose to USD 53.68 billion in 2025 (≈+25.48% YoY), and is projected to reach USD 408.61 billion by 2034, a multi-billion-dollar expansion driven by tech integration, remote care and rising chronic disease burden.

Download the free sample and get the complete insights and forecasts report on this market @ https://www.towardshealthcare.com/download-sample/5613

Market size

Baseline numbers (explicit):

2024 market size: USD 42.78 Bn.

2025 market size: USD 53.68 Bn (absolute increase USD 10.90 Bn; ≈25.48% YoY).

2034 projected size: USD 408.61 Bn.

Stated CAGR vs. number-driven CAGR:

Reported CAGR (2025–2034): 25.57% (given).

Calculated CAGR using the supplied 2025 (USD 53.68B) → 2034 (USD 408.61B) over 9 years is ≈25.30%. (Small rounding/statement difference — both indicate very high compound growth.)

Magnitude of expansion (scale factor):

The market multiplies by a factor of ~7.6× from 2025 to 2034 (408.61 / 53.68 ≈ 7.61).

Absolute incremental value added between 2025 and 2034: USD 354.93 Bn (average nominal increase ≈ USD 39.44 Bn per year).

What a ~25% CAGR implies operationally:

Rapid product iteration cycles: devices and apps must update frequently to remain competitive.

Large capital inflows required into manufacturing, regulatory/human-factors testing, cloud/AI platforms, and distribution.

Market composition will shift from consumer mass gadgets to higher-value clinical & therapeutic-grade wearables (report forecasts clinical grade as fastest growing).

Value pools implied:

Device hardware (sensors, batteries, wearables) will capture significant early revenue but software, analytics, and services (remote monitoring subscriptions, data services, clinician dashboards) will become major recurring-revenue pools as usage matures.

Channel evolution impact on size:

Online channels forecast fastest growth — enabling direct-to-consumer & B2B distribution, lowering per-unit customer acquisition costs and widening addressable markets (urban + remote).

Market trends

Surge in remote patient monitoring & home healthcare acceptance

Home healthcare dominated 2024; remote monitoring is the fastest growing application area — payers, clinicians, and patients increasingly accept data collected outside clinics for chronic care and post-op monitoring.

Non-invasive sensing innovation is a rallying point

Examples: MIT wristwatch-sized device that can detect single circulating cells (April 2025); KIMS ammonia sensor enabling breath analysis. These drive clinical relevance without invasive procedures.

AI integration across the stack

AI is already used to clean sensor data, detect patterns, predict events, and improve diagnostic accuracy — transforming wearables from passive trackers into active clinical tools.

Convergence of technologies (micro/nano/ICT/biomed/materials engineering)

Multi-disciplinary R&D is enabling smaller sensors, flexible form factors, and long-duration adhesives (e.g., patches that stick for days).

Strap/clip/bracelet dominance and form-factor diversification

Strap/clip/bracelets dominated 2024 but fast growth is also happening in shoe sensors, patches, headbands — each unlocking new clinical use cases (mobility, respiration, sleep).

Consumer → Clinical march

Consumer-grade devices led 2024 by volume; clinical-grade devices are the fastest-growing segment as regulatory approvals and validation studies increase clinical acceptance.

Distribution shift: pharmacies still lead, but online channels accelerating

Pharmacies dominated in 2024 for availability and counseling; online channels are the fastest growing distribution route due to convenience and variety.

Regional investment and adoption divergence

North America led in 2024 (mature healthcare systems, capital); Asia Pacific is the fastest-growing market driven by huge populations, rising healthcare spending, and manufacturing capacity.

Regulation & standards becoming critical — sleep example

NUS call (Apr 2025) for aligned sleep measurement standards highlights a trend: manufacturers must conform to shared measurement/principle standards to increase clinical utility.

Startups & IP activity rising

Patent approvals (e.g., Wearable Devices Ltd’s gesture/voice interface, Apr 2025) and prototype announcements (LSMP) indicate active innovation and IP consolidation.

Clinical trials & validation intensifying

UCLA Health trial of gentle nerve stimulation for ADHD (Apr 2025) and Sonus-Providence collaboration show devices are moving into formal clinical validation and commercialization pathways.

AI roles in the wearable medical devices market

Signal-level denoising & artifact removal (edge + cloud):

AI models filter motion artifacts, electromagnetic noise, and physiologic cross-talk (e.g., motion vs. heart rate).

Why it matters: Increases usable data fraction, reduces false alarms, and improves clinician trust — enables clinical-grade accuracy from consumer hardware.

Sensor fusion & multimodal pattern extraction:

AI ingests ECG, PPG, accelerometer, respiration, temperature and learns combined signatures (e.g., heart-failure decompensation patterns).

Why it matters: Multimodal models raise sensitivity/specificity vs single-sensor approaches and unlock new digital biomarkers.

Personalized baselines & adaptive models:

Machine learning tailors detection thresholds and algorithms to each patient’s physiology over time (accounts for age, activity, comorbidities).

Why it matters: Reduces false alerts and improves early detection in chronic disease management.

Predictive analytics & early warning forecasting:

AI forecasts near-term clinical events (arrhythmia onset, glycemic excursions, COPD exacerbations) allowing pre-emptive interventions.

Why it matters: Can reduce hospitalizations, lower costs, and prove health economic value to payers.

On-device (edge) inference for privacy & latency:

Tiny models run on-device to process raw signals and transmit only derived alerts/summary metrics.

Why it matters: Preserves privacy, reduces bandwidth/battery use, and enables real-time responses (e.g., seizure detection).

Federated learning & privacy-preserving model improvement:

Models are trained across decentralized devices without sharing raw data, improving generalizability while protecting patient data.

Why it matters: Meets regulatory privacy expectations and accelerates model updates across manufacturer device fleets.

Regulatory compliance, explainability & model auditing:

AI pipelines include explainable modules and audit logs to satisfy regulators and clinicians (traceable decision paths, importance scores).

Why it matters: Facilitates clinical adoption and regulatory approval for diagnostic claims.

Clinical decision support & workflow integration:

AI converts wearable raw data into clinically actionable summaries and integrates into EHRs, clinician dashboards, or telehealth triage.

Why it matters: Increases clinician efficiency and creates monetizable care pathways.

Synthetic data generation and accelerated R&D:

AI creates realistic synthetic signals to augment training datasets for rare events (e.g., uncommon arrhythmias) and supports algorithm validation.

Why it matters: Reduces time/cost for model development and helps satisfy statistical validation requirements.

Optimization of power, sampling, and form factor (ML for hardware):

AI estimates when to sample at high frequency or downsample based on user state, optimizing battery life. Also helps map sensor placements to signal yield.

Why it matters: Extends device lifetime and improves wearability — crucial for patch/adhesive multi-day devices.

Regional insights

North America (U.S. + Canada)

Market status: Dominated global market in 2024.

Why dominant: high per-capita healthcare spending, strong reimbursement infrastructure, early payer support for RPM (remote patient monitoring), mature venture and corporate funding.

Clinical validation & regulatory pathway: FDA approvals and clinical trials create credible clinical-grade devices. Strong academic-industry collaborations (UCLA trial example).

Opportunity: Integration into hospital systems and chronic care pathways (diabetes, cardiac).

Challenge: Higher cost expectations; payers demand clear evidence of economic and clinical value.

Asia Pacific (China, India, Japan, South Korea, others)

Growth engine: Fastest-growing region due to rising healthcare spending, large addressable populations, and manufacturing capabilities.

China: Massive scale potential and local manufacturing; regulatory modernization encourages device approvals.

India: Growing healthcare access, government pushes for affordable devices; price sensitivity encourages low-cost innovations and online distribution.

Korea & Japan: Strong materials/science base (KIMS ammonia sensor; LSMP research), rapid technology adoption.

Opportunity: Volume market for consumer-grade wearables and rapid uptake of telehealth; production scale-ups reduce global device costs.

Europe (Germany, UK, France, Nordics)

Investment & standards: Europe is driven by increasing healthcare & private investments plus strong medtech clusters (Germany).

Regulatory landscape: CE-marking and evolving EU medical device regulations — makes market access rigorous but stable. NUS-style calls for measurement standards (sleep trackers) resonate in Europe’s standards culture.

Opportunity: Clinical collaborations and precision chronic care programs; strong rehabilitation & neurostimulation research ecosystems.

Latin America

Adoption profile: Slower relative adoption but high need for remote monitoring in underserved regions.

Challenge: Reimbursement limitations and distribution gaps.

Opportunity: Telehealth + low-cost wearables with local partnerships to expand reach.

Middle East & Africa (MEA)

Current profile: Small but growing; niche demand in private healthcare centers and expatriate populations.

Opportunity: Mobile-first remote care models; workplace health programs.

Regional cross-cutting considerations

Manufacturing vs. clinical validation split: Asia will likely supply hardware at scale; North America & Europe will drive clinical validation and regulatory leadership.

Distribution nuance: Pharmacies lead in places with retailized medical supply culture; online channels accelerate reach in countries with strong e-commerce infrastructure.

Market dynamics

Drivers

Rising incidence of chronic diseases (cardiovascular disease, diabetes, asthma, etc.):

Drives need for continuous monitoring and early detection; wearables reduce clinic visits and enable preventive care.

Shift to home healthcare & remote patient monitoring:

Home healthcare dominated 2024; RPM is fastest growing — aligns with aging populations and desire to cut hospital readmissions.

Technological convergence (AI, materials, sensors, microelectronics):

Enables smaller, more accurate, longer-life devices and new diagnostic capabilities (e.g., single-cell detection).

Consumer health awareness & wellness adoption funneling into medical use:

Wearables starting in fitness segment are being upgraded to clinical-grade use cases.

Distribution and digital channels:

Online channels lower friction of purchase and enable software updates/subscription monetization.

Restraints

High device and system costs:

Limits adoption in resource-constrained settings, and across public health systems without clear cost-effectiveness data.

Regulatory and reimbursement barriers:

Clinical claims require trials, increasing time and cost to market. Payer reimbursement lags for many RPM benefits.

Data privacy and interoperability concerns:

Fragmented data formats and privacy regulations slow wide clinical integration.

Opportunities

Non-invasive device boom:

Devices offering diagnostic value without invasive procedures (breath sensors, multi-day patches) have strong patient compliance and wide use cases.

Clinical-grade device market expansion:

As clinical acceptance grows, higher-value devices & subscription services will expand margins and MRR models.

AI + data services monetization:

Analytics, prediction engines, clinician dashboards, and care-management subscriptions are high-value revenue adjacencies.

Emerging markets & online channels:

Low-cost, scalable devices for India/China and telehealth bundles can expand addressable market.

Ten top companies

Medtronic

Representative products: implantable cardiac devices, insulin delivery systems, neurostimulation devices.

Overview: Large global medtech with deep clinical footprint across cardiology, diabetes, and neurostimulation.

Strengths: Strong regulatory expertise, clinician relationships, proven device reliability, scale manufacturing and service networks.

Google (incl. Verily & Fitbit ecosystem)

Representative products: health-oriented wearables via Fitbit; Verily research projects on biosensing & data platforms.

Overview: Tech giant with data/cloud strength and wearable hardware/software assets.

Strengths: Massive data/AI infrastructure, platform integration, consumer reach (Fitbit), and cross-discipline R&D resources.

Abbott

Representative products: continuous glucose monitoring (CGM) systems, cardiac sensors.

Overview: Large diagnostics and devices company with strong presence in chronic disease monitoring.

Strengths: Established clinical evidence base, global distribution, payer engagement for chronic care devices.

OMRON Healthcare, Inc.

Representative products: blood pressure monitors, consumer-clinician connected vitals devices.

Overview: Known for accurate, consumer-validated vitals monitors and home diagnostics.

Strengths: Trust in clinical accuracy for home devices, wide pharmacy distribution, strong brand equity.

Koninklijke Philips N.V. (Philips)

Representative products: connected patient monitoring, sleep & respiratory wearables, clinical systems.

Overview: Integrated health tech and health informatics capabilities with hospital and home solutions.

Strengths: Strong hospital relationships, integrated care platforms, and deep clinical validation capabilities.

Garmin Ltd.

Representative products: advanced activity/heart-rate watches with growing health metrics.

Overview: Consumer wearables leader moving into more clinically relevant monitoring via partnerships and sensor upgrades.

Strengths: Robust hardware engineering, consumer brand, long battery life & durability design.

GE HealthCare

Representative products: clinical monitoring systems, imaging + connected device integrations.

Overview: Large provider of clinical diagnostic equipment; bringing scale and integration to wearable data pipelines.

Strengths: Hospital procurement channels, systems integration, and clinician trust.

Dexcom, Inc.

Representative products: continuous glucose monitoring (CGM) systems widely used by diabetes patients.

Overview: Leader in CGM — established real-world clinical efficacy and growing remote monitoring integrations.

Strengths: Device accuracy/validation, strong clinical adoption, partnerships for insulin pump ecosystems.

Insulet Corporation

Representative products: tubeless insulin pumps (Omnipod) and integrated diabetes care systems.

Overview: Innovator in wearable insulin delivery with strong patient adoption.

Strengths: Seamless user experience, clinical focus, and strong market positioning in diabetes wearable therapy.

Withings

Representative products: consumer-to-medical hybrid wearables (BP monitors, smartwatches) with health tracking features.

Overview: European brand bridging consumer design and medical measurement accuracy.

Strengths: Design/UX, hybrid consumer-medical positioning, and pharmacy/retail distribution relationships.

Latest announcements

UCLA Health — clinical trial for gentle nerve stimulation for ADHD (Apr 2025)

What happened: First clinical trial testing wearable gentle nerve stimulation during sleep to reduce ADHD symptoms in children exposed to alcohol before birth; funded by NIAAA with $350,000 grant.

Why it matters: Demonstrates movement of neurostimulation wearables into pediatric neurotherapeutics with federal funding; success would expand therapeutic wearable use cases and reimbursement potential.

Sonus Microsystems + Providence Health Care Ventures collaboration (Apr 2025)

What happened: Collaboration to develop Sonus’ wearable ultrasound platform for cardiac monitoring and commercialization via PHCV Innovation Program.

Why it matters: Wearable ultrasound is a disruptive sensing modality; if validated, it enables richer imaging-like information in wearables (beyond vitals).

NUS Prof. Michael Chee (Apr 2025) — call for standardization of sleep measurement

What happened: Academic recommendation that manufacturers align common standards & principles for sleep measurement to improve utility of consumer trackers.

Why it matters: Standardization accelerates clinical adoption and cross-device comparability (critical for large-scale sleep studies and reimbursement).

KIMS ammonia sensor (Apr 2025)

What happened: Researchers at KIMS developed ammonia sensor usable for breath analysis and indoor air quality monitoring; potential for disease-diagnosis applications.

Why it matters: Breath sensors enlarge non-invasive diagnostic possibilities (e.g., metabolic or infection monitoring).

Wearable Devices Ltd — USPTO patent allowed (Apr 2025)

What happened: Patent titled “Gesture and Voice-Controlled Interface Device” allowed — AI-powered touchless sensing wearables.

Why it matters: Highlights IP activity in human-device interfaces that will improve hands-free operation and accessibility for clinical populations.

Lung-Sound-Monitoring-Patch (LSMP) prototype (KIST)

What happened: Prototype patch that can adhere for 5 days to monitor lung sounds.

Why it matters: Long-duration adherence and respiratory monitoring enable continuous pulmonary monitoring for COPD, post-op care, and infectious disease surveillance.

MIT single-cell detection wristwatch-sized device (Apr 2025)

What happened: Small, wristwatch-sized non-invasive monitor reported to detect single cells in blood vessels.

Why it matters: If validated clinically, it opens an entirely new class of wearables for early cancer detection, circulating tumor cells, and immune monitoring.

Recent developments

From prototypes to trials — validation pipeline accelerates:

Multiple research prototypes (LSMP, MIT device) and clinical trials (UCLA) show industry movement from lab proof-of-concept to clinical validation — the critical step for clinical-grade commercialization.

New sensing modalities increase clinical reach:

Breath ammonia sensors and wearable ultrasound extend beyond vitals to biochemical and imaging-like data — expanding diagnostic scope and potential reimbursement codes.

Standards & interoperability becoming business-critical:

Academic/regulatory calls for measurement harmonization (sleep metrics) mean manufacturers who align early will gain clinician trust and platform partnerships.

IP & HCI (human-computer interaction) patents emphasize usability:

Gesture/voice patents show that usability and accessibility are strategic differentiators — enabling caregivers and patients with limited mobility to interact with devices.

Edge of consumer/clinical boundary erodes:

Consumer devices evolving to clinical grade (and vice versa) create hybrid business models (hardware sale + SaaS analytics + clinician licenses).

Commercialization partnerships accelerate market entry:

Collaborations like Sonus + Providence demonstrate access to clinical validation and distribution channels, shortening time-to-market.

Segments covered

By Product — Diagnostic Devices (umbrella)

Vital sign monitoring devices (heart rate, SpO₂, BP, respiration):

Value: Continuous vitals enable early decompensation detection.

Challenges: Motion artifacts, cuffless BP accuracy, regulatory thresholds.

Growth drivers: Remote care, chronic disease monitoring.

Electrocardiographs (ECG) & rhythm detection:

Value: Atrial fibrillation detection, rhythm monitoring, arrhythmia screening.

Challenges: Short vs continuous monitoring accuracy, skin contact quality.

Players: Patch ECG specialists, mobile ECG apps.

Pulse oximeters & spirometers:

Value: Respiratory disease monitoring and triage.

Challenges: Peripheral perfusion effects for SpO₂, calibration for spirometry.

Use cases: COVID/post-COVID respiratory follow up, COPD.

Sleep monitoring devices (trackers, wrist actigraphs, polysomnographs):

Value: Sleep disorder screening, therapy efficacy.

Challenge: Aligning measurement standards (NUS recommendation), validation vs PSG (polysomnography).

Neuromonitoring & EEG/EMG wearables:

Value: Seizure detection, neurorehabilitation, brain-state monitoring.

Challenges: Low-noise surface EEG acquisition, wearable comfort for long use.

Sensing devices (accelerometers, biosensors, ultrasound platforms):

Value: Activity measurement, gait analysis, imaging proxies.

Challenges: Data fusion and clinical interpretation.

By Product — Therapeutic Devices

Pain management & neurostimulation devices:

Value: Non-pharmacologic chronic pain therapies, neuromodulation for depression/ADHD.

Challenge: Proving durable clinical outcomes, device tolerance in daily life.

Insulin/glucose monitoring & pumps:

Value: Closed-loop glycemic control; major chronic disease impact.

Challenge: Accuracy, integration, reimbursement.

Rehabilitation devices (accelerometer-based, exoskeleton adjuncts):

Value: Objective mobility tracking, therapy adherence.

Challenge: Translating data into actionable therapy adjustments.

By Site — Form factors

Strap/clip/bracelet: dominant (comfort, consumer familiarity).

Patches (multi-day): improved continuous monitoring and adherence (LSMP example).

Shoe sensors: mobility and gait analytics for orthopedics & fall risk.

Headbands & handhelds: sleep EEG and handheld diagnostics (ultrasound probes).

By Grade Type

Consumer-grade: high volume, lower per-unit price, gateway to clinical adoption.

Clinical-grade: higher accuracy, regulatory burden, greater revenue per unit and services.

By Distribution Channel

Pharmacies: in-person counseling, medical advice at point of sale (2024 leader).

Online: fastest growing — direct access, subscriptions, software updates.

Top 5 FAQs

Q1: How large is the wearable medical devices market today, and how fast is it growing?

A: In 2024 the market was USD 42.78B, rose to USD 53.68B in 2025 (≈+25.5% YoY), and is projected to reach USD 408.61B by 2034 — implying 25.3–25.6% CAGR (2025–2034) and a 7.6× expansion from 2025 to 2034.

Q2: Which region currently leads and which region is fastest-growing?

A: North America dominated in 2024 (mature healthcare systems, high spending). Asia Pacific is projected to be the fastest-growing region during the forecast, driven by population scale, rising healthcare spending, and manufacturing strength.

Q3: Which product segments are most important for investors?

A: Diagnostic devices led 2024 by value; therapeutic devices and clinical-grade wearables are forecasted as the fastest-growing value segments — they carry higher per-unit revenues and subscription/service potential.

Q4: How will AI change device value and business models?

A: AI turns raw sensor streams into predictive, clinically actionable insights — enabling subscription analytics, reduced false alarms, edge inference for privacy, and scalable personalization. This drives higher lifetime revenues (device + software + services).

Q5: What are the main market restraints and where are the biggest opportunities?

A: Restraints: high costs, regulatory and reimbursement hurdles, privacy/interoperability issues. Opportunities: non-invasive diagnostics (breath, single-cell detection), clinical-grade wearables, and service/AI monetization (remote patient monitoring subscriptions).

Access our exclusive, data-rich dashboard dedicated to the medical devices – built specifically for decision-makers, strategists, and industry leaders. The dashboard features comprehensive statistical data, segment-wise market breakdowns, regional performance shares, detailed company profiles, annual updates, and much more. From market sizing to competitive intelligence, this powerful tool is one-stop solution to your gateway.

Access the Dashboard: https://www.towardshealthcare.com/access-dashboard

Immediate Delivery Available | Buy This Premium Research @ https://www.towardshealthcare.com/price/5613

Become a valued research partner with us – https://www.towardshealthcare.com/schedule-meeting

You can place an order or ask any questions, please feel free to contact us at sales@towardshealthcare.com

Powering Healthcare Leaders with Real-Time Insights: https://www.towardshealthcare.com/healthcare-intelligence-platform

Europe Region – +44 778 256 0738

North America Region – +1 8044 4193 44

APAC Region: +91 9356 9282 04

Web: https://www.towardshealthcare.com

Find us on social platforms: LinkedIn | Twitter | Instagram | Medium | Pinterest