The Asia-Pacific Women’s Digital Health Market — valued at USD 724.17M in 2024 and USD 889.14M in 2025 — is projected to reach USD 5,691.42M by 2034 (a 22.74% CAGR, 2025–2034), driven by smartphone penetration, telehealth demand, government initiatives and rapid AI/IoT adoption.

Download the free sample and get the complete insights and forecasts report on this market @ https://www.towardshealthcare.com/download-sample/5808

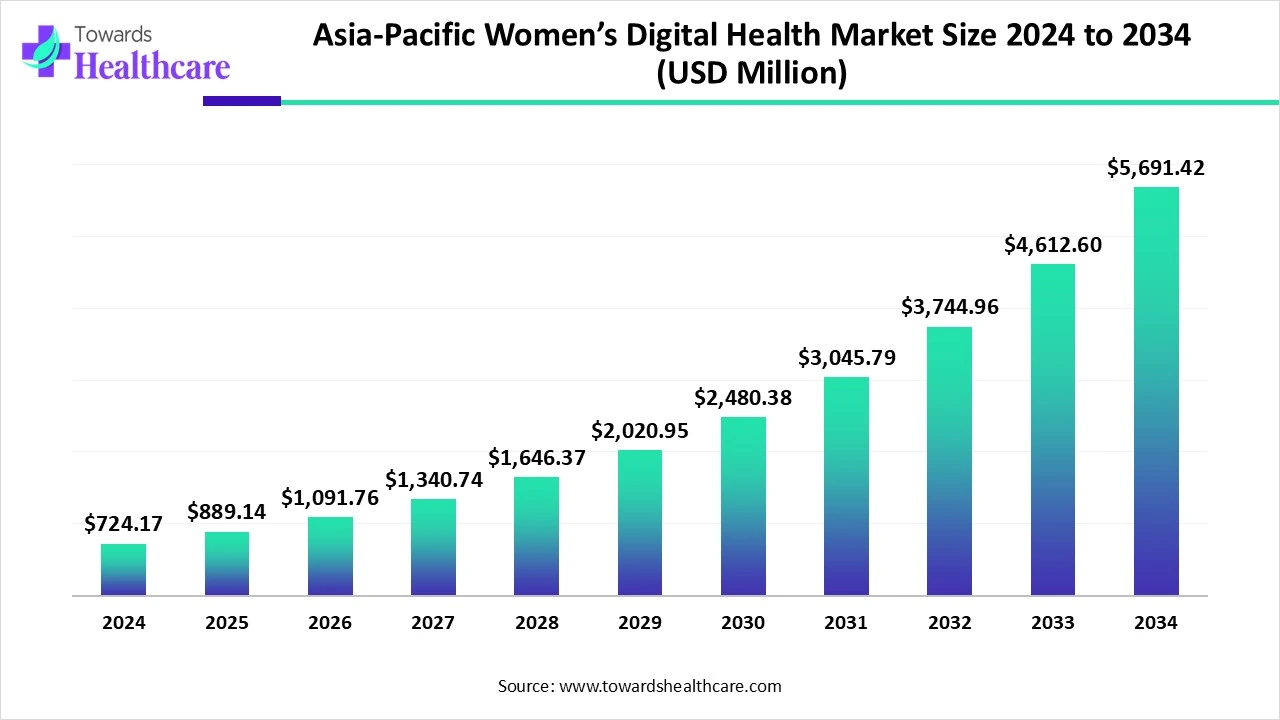

Market-size

Baseline figures (anchor points).

➤2024: USD 724.17 million (APAC).

➤2025: USD 889.14 million (APAC).

➤2034 projection: USD 5,691.42 million (APAC).

These are the official anchors for sizing, forecasting and strategy.

CAGR and scale of change.

➤Reported CAGR (2025–2034): 22.74%.

➤Growth multiple (2025 → 2034): 6.40× (i.e., market grows more than sixfold).

➤Absolute increase: ~USD 4.80 billion added market value between 2025 and 2034.

APAC vs. global context.

➤Global women’s digital health market: USD 3.82B (2025) → USD 20.92B (2034).

➤APAC share in 2025 ≈ 23.3% of the global 2025 market (889.14M / 3.82B).

➤Interpretation: APAC is already a material share (~one-quarter) of the global opportunity and is expected to remain a strategic growth region.

Acceleration from 2024 → 2025 (momentum signal).

➤Year-on-year jump from USD 724.17M → USD 889.14M (22.8% YoY).

➤Indicates strong near-term investor/consumer traction and validating signals for product-market fit.

Market depth vs breadth.

➤Depth: high-value clinical tools, cloud platforms and enterprise telemedicine (hospitals, providers).

➤Breadth: mass consumer adoption through mobile apps & wearables (individual consumers constitute ~50% share of end-use in 2024).

➤Strategic implication: winners will have dual playbooks — consumer acquisition + provider integration.

Capital intensity & monetization windows.

➤Mobile apps and cloud platforms enable rapid scale at lower capex; diagnostic devices and regulated medtech require more capital and longer commercialization cycles — both will contribute to the aggregate size but on different timelines.

Market trends

Mobile health apps dominate (2024 40% share of APAC product mix).

➤Reason: smartphone ubiquity + faster user onboarding, privacy control and direct consumer monetization (subscriptions, in-app services).

Wearables are the fastest-growing product type.

➤Drivers: AI sensors, fertility and pregnancy monitoring, non-invasive continuous monitoring. Wearables convert episodic care into continuous data streams.

Fertility & pregnancy management lead application revenue (35% in 2024).

➤Why it leads: high demand for monitoring and guidance during pregnancy, fertility planning, rising infertility awareness, and government interest in maternal outcomes.

Mental health & wellness show the fastest application CAGR.

➤Factors: Gen-Z and younger women’s mental health needs, remote counseling, and scalable digital therapy/CBT modules.

Individual consumers dominate end-use (50% in 2024).

➤Consequence: consumer marketing funnels, community & social features, and D2C data collection are central to product roadmaps.

Telemedicine providers are the fastest-growing end-use segment.

➤Telemedicine scales care delivery, reduces visit friction for pregnancy, chronic conditions and mental health — providers will increasingly white-label tools or partner with app makers.

Cloud-based platforms are the backbone (45% share in 2024).

➤Implication: interoperable EHR integration, data portability, multi-tenant SaaS commercialization and faster product updates.

AI/ML is the fastest-growing technology lever.

➤Use cases: risk stratification, ultrasound interpretation, predictive fertility windows, personalization.

Mobile delivery leads (55% share) while web platforms rise fastest.

➤Mobile apps win for engagement and device access; web platforms scale multi-user, multi-stakeholder workflows (providers, admin panels).

Policy & funding momentum in APAC.

➤Examples from supplied data: government digital health missions, corporate funding (eKincare), public-private initiatives (AlgoBharat), and corporate programs (Roche’s awareness campaigns).

Convergence of medtech + consumer tech.

➤Devices (wearables, diagnostics) tightly integrated with app ecosystems and provider portals, blurring lines between consumer health and regulated medical devices.

Localization is critical.

➤Language, cultural norms around women’s health, payment models, and urban-rural access shape product adoption differently across APAC markets.

AI impacts for APAC women’s digital health

Personalized fertility windows & ovulation forecasting (AI time-series modelling).

➤What: Combine cycle history, wearable vitals and symptom logs to model individual ovulation/fertility windows.

➤Why: Personalized forecasts increase conception success and reduce noise from population-level calendars.

➤Scale: Improves value of fertility apps/wearables and lifts subscription retention.

Automated remote pregnancy risk stratification (ML risk scores).

➤What: ML models ingest vitals, ultrasound metrics and patient history to flag high-risk pregnancies.

➤Why: Enables early interventions and prioritizes scarce clinical resources in low-access areas.

➤Scale: Reduces maternal complications and improves clinical outcomes at scale when paired with telemedicine.

AI-assisted ultrasound & imaging interpretation.

➤What: Edge or cloud AI to detect gestational age, fetal abnormalities, and placental issues.

➤Why: Fills imaging expertise gaps in remote hospitals and reduces time to clinical decision.

➤Scale: Makes portable ultrasound devices more actionable for frontline clinics.

Continuous sensor analytics from wearables (trend detection & alerts).

➤What: Detect subtle changes (e.g., hr variability, sleep, temperature) linked to PCOS, pregnancy complications or stress.

➤Why: Moves care from episodic to continuous monitoring; alerts trigger timely teleconsults.

➤Scale: Drives device stickiness and enables outcome-based pricing.

Personalized mental-health interventions via NLP & recommendation engines.

➤What: Conversational agents triage mood, recommend CBT modules and escalate to human counselors.

➤Why: Lowers barrier to seeking help; matches scale of demand for younger women.

➤Scale: Reduces cost per intervention and increases service reach across languages.

Clinical decision support for providers (explainable AI).

➤What: Suggest treatment pathways, drug interactions and follow-up schedules tailored to female physiology.

➤Why: Improves quality and reduces guideline variability across clinics.

➤Scale: Improves outcomes and fosters provider trust in digital tools.

Predictive population health & resource planning (big-data ML).

➤What: Forecast hot spots (e.g., maternal complications by district) using aggregated, de-identified data.

➤Why: Governments and NGOs can allocate resources proactively (screening camps, mobile clinics).

➤Scale: Strengthens national programs and justifies public funding.

AI for automated regulatory/compliance monitoring & anomaly detection.

➤What: Monitor data flows for privacy breaches, anomalous model drift, or biased outputs by subgroup.

➤Why: Ensures safety and reduces legal/regulatory risk in fragmented APAC regulatory environments.

➤Scale: Essential for enterprise customers (hospitals, insurers).

Federated learning & privacy-preserving AI across providers.

➤What: Train models across hospital datasets without centralized data pooling.

➤Why: Solves data-sharing and privacy constraints while improving model generalizability across APAC populations.

➤Scale: Enables pan-country models respecting local laws.

Operational AI — demand forecasting, chatflows, and automated billing.

➤What: Optimize appointment scheduling, teleconsult capacity, and payment reconciliation.

➤Why: Lowers operational cost for telemedicine providers and improves patient experience.

➤Scale: Enhances unit economics and accelerates provider uptake.

Regional insights

A. China — scale, institutional adoption, device penetration

Market character: Large urban tech adoption; high hospital digitization (apps widely used for scheduling).

Strengths: Massive smartphone user base, robust local device OEMs and cloud adoption.

Strategic moves: Focus on integrated hospital-app ecosystems; enterprise partnerships matter.

Barrier: Regulatory scrutiny on health AI and data localization norms; rural access gaps despite scale.

B. India — policy push, telehealth scale, cost sensitivity

Market character: Rapid policy momentum (digital health missions), high unmet maternal needs, price-sensitive consumers.

Strengths: Large developer ecosystem, strong telemedicine and aggregator players, government programs (ABDM, Tele MANAS).

Subpoints:

Urban vs rural: Urban consumers adopt apps fast; rural needs affordable offline-first solutions.

Payment models: Mix of freemium, telco partnerships and minimal direct pay; value-based models possible with government ties.

C. Japan — aging population, clinical rigor, selective consumer uptake

Market character: High geriatric proportion, conservative adoption of health IoT among women (usage stats show many non-users).

Strengths: Strong clinical infrastructure, emphasis on sex/gender-specific diagnostics (e.g., WaiSE).

Barriers: Cultural norms and conservative tech uptake for certain women’s health topics.

D. Southeast Asia (Indonesia, Philippines, Thailand, Vietnam) — mobile first, fragmented markets

Market character: Mobile-first users, rapid adoption of telemedicine aggregators (e.g., Halodoc, Alodokter).

Strengths: Localized apps that fit language & cultural contexts; fast partner adoption among insurers.

Barriers: Payment fragmentation, variable regulation and uneven provider quality.

E. Australia & New Zealand — high per-capita spend, strong regulatory frameworks

Market character: Mature markets with higher willingness to pay for health tech.

Strengths: Clear reimbursement pathways, high trust in digital health players.

Implication: Good testbeds for premium features and clinical trials.

F. Emerging APAC (Nepal, Bangladesh, smaller island nations) — access gaps, high impact potential

Market character: Low baseline digital health adoption but high impact per intervention (e.g., maternal mortality reduction).

Strategy: Low-cost point-of-care diagnostics, SMS-enabled care models and NGO + government partnerships.

Market dynamics

Drivers

Telehealth demand — remote consultations reduce travel, crucial for pregnancy and mental health care.

Smartphone & 5G buildup — faster, more reliable connectivity enables richer telemedicine and remote imaging (GSMA projection in supplied data: large increase in 5G by 2030).

Consumer health awareness — women increasingly track cycles, fertility and wellness, fueling D2C app growth.

Government initiatives & funding — national digital health missions hasten provider integrations and reimbursement frameworks.

Restraints

Rural digital divide — device ownership, connectivity, literacy and cost barriers reduce reach.

Regulatory fragmentation — different countries with distinct rules on health data, device approvals, and AI use slow pan-regional scale.

Trust & cultural stigma — menstrual, fertility and sexual health topics may face social resistance in parts of APAC.

Opportunities

Point-of-care diagnostics & home testing — self-collected tests (HPV, pregnancy) extend reach.

Wearables & continuous monitoring — non-invasive sensors unlocking high-frequency women’s health signals.

AI-enabled provider decision support — reduces specialist load and improves rural care quality.

Public–private collaboration — governments partnering with startups for screening weeks and helpline integrations.

Threats & risks

Data privacy & breaches — women’s health data is sensitive; breaches cause reputational and regulatory risk.

Algorithmic bias — models trained on non-representative datasets may underperform for some APAC subgroups.

Commercial viability — monetization depends on willingness to pay or coverage by payers/insurers.

Structural forces & enablers

Cloud platforms & interoperability — enable multi-stakeholder workflows (consumer → provider → insurer → researcher).

Capital flow & M&A — funding rounds (example: eKincare) and strategic deals accelerate scale.

Localization & partnerships — partnerships with local providers and NGOs are required for deep rural penetration.

Top 10 companies

Clue (Bayer AG)

Product/Overview: Consumer menstrual-cycle tracking app with data insights for female reproductive health.

Strength: Strong scientific brand association (Bayer), data-driven cycle analytics and credibility for partnerships with providers and research programs.

Flo Health Inc.

Product/Overview: Period, ovulation and women’s health tracking app with content and symptom logging.

Strength: Large consumer reach; strong user engagement patterns and potential for premium subscription & telehealth add-ons.

Elvie

Product/Overview: Femtech hardware + apps (pelvic-floor trainers, wearable pumps and trackers).

Strength: Device-plus-software approach yields high-value unit economics and differentiated IP in women’s devices.

Ava Science Inc.

Product/Overview: Fertility and sleep monitoring wearable that tracks physiological signals relevant to conception.

Strength: Wearable focus for continuous fertility data, attractive for couples seeking conception optimization.

Ovia Health (Eden Health Group)

Product/Overview: Digital maternal & family health platform offering pregnancy management and care pathways.

Strength: Comprehensive maternal care playbook — a natural enterprise play for employers and providers.

Natural Cycles

Product/Overview: Algorithm-driven fertility planning app (contraception & conception use cases).

Strength: Scientific/algorithmic positioning that appeals to users seeking non-hormonal fertility guidance.

Maven Clinic

Product/Overview: Virtual clinic for women and family health — telemedicine + care navigation.

Strength: Employer and payer partnerships, end-to-end care coordination for fertility and maternity benefits.

Medtronic

Product/Overview: Large medtech company with device & diagnostic portfolio applicable to women’s chronic disease and monitoring.

Strength: Institutional relationships with hospitals, regulatory know-how and scale manufacturing.

Philips Healthcare

Product/Overview: Imaging, monitoring and software solutions with enterprise health platform reach.

Strength: End-to-end hospital integration, trusted imaging and cloud platform presence.

Xiaomi (Mi Health & Wearables)

Product/Overview: Consumer wearables and health tracking integrated with mobile ecosystems.

Strength: Low-cost hardware scale and massive distribution channels across APAC, enabling rapid wearable penetration.

(Honourable mentions: Practo, 1mg, Halodoc, Alodokter, Glow, Babyscripts — these local/regional players strengthen telemedicine, pharmacy and maternal-care orchestration in APAC.)

Latest announcements

Noha Salem (Organon) — fertility as a policy priority

What she said: Governments should recognize infertility as a disease and integrate fertility care into national healthcare strategies.

Impact: If adopted, this reframes fertility from a consumer expense to a covered public health priority, expanding reimbursement and public program funding — a major growth lever for fertility digital tools.

eKincare (May 2025) — investment from MSD IDEA Studio APAC

What: eKincare raised strategic investment to expand AI-driven integrated digital health gateway capabilities.

Implication: Capital for AI, data analytics and telemedicine scale; signals investor appetite in APAC femtech & enterprise health platforms.

Lupin Digital Health (March 2025) — post-procedure home-based care guide

What: Launch of guidance for home recovery after interventional cardiology procedures.

Relevance to women: Demonstrates pharma/healthcare players moving into digital post-op care — a model that can be extended to postpartum recovery and maternal follow-up.

Roche (May 2024) — National Women’s Check-up Week (Singapore)

What: Public awareness campaign and survey across APAC markets; collaboration with patient orgs for screening.

Implication: Pharma/diagnostics firms can drive demand generation and local outreach with public health partners.

AlgoBharat + SEWA Shakti Kendras (July 2024) — Digital Health Passport (blockchain solution)

What: Secure, immutable credentialing to access health benefits and social programs.

Implication: Demonstrates interest in secure, portable health identity solutions that can benefit marginalized women.

Recent developments

Funding + enterprise investments (eKincare) — signals capital availability for scale and AI productization in APAC; expect M&A / partnerships.

Public awareness & screening campaigns (Roche) — corporate programs can catalyze user acquisition and screening funnel for digital products.

Operational digital tools from pharma (Lupin) — demonstrates nontraditional entrants expanding digital care beyond classical therapeutics.

Blockchain health identity pilots (AlgoBharat + SEWA) — points to experimentation with secure health IDs for access to benefits; powerful for female populations needing portability of maternal records.

Regulatory & policy commentary (Organon leader) — pushes fertility into policy conversations; such influence can change payer/reimbursement dynamics.

Strategic takeaway: capital + policy + corporate programs are aligning to create both demand and supply-side scaffolding for long-term APAC women’s digital health scale.

Segments covered

By Product Type

Mobile Health Applications

➤Role: Primary consumer touchpoint for tracking, teleconsults and content.

➤Value props: Low friction, rapid iteration, subscription and ad models.

Wearable Devices

➤Role: Continuous physiological monitoring (temperature, HRV, sleep).

➤Challenges: Sensor accuracy, regulatory classification if clinical claims made.

Telehealth Platforms

➤Role: Provider-patient virtual visits, remote monitoring feeds to clinicians.

➤Value props: Access extension, appointment efficiency and triage.

Diagnostic Devices

➤Role: Home tests (HPV, pregnancy), point-of-care devices for clinics.

➤Implication: High regulatory bar but high value per unit.

Software & Analytics Tools

➤Role: Clinical dashboards, EHR integration, AI analytics for population health.

➤Customers: Hospitals, telemedicine providers, payers.

By Application

Fertility & Pregnancy Management: prenatal monitoring apps, remote checklists, tele-OB consults.

Mental Health & Wellness: chatbots, therapy modules, remote counseling.

Menstrual Health & Cycle Tracking: data for symptom management and long-term care.

Menopause Management: symptom tracking, hormone care pathways.

Chronic Disease Management: PCOS, osteoporosis and breast cancer monitoring via digital pathways.

Sexual & Reproductive Health: STI education, contraceptive management.

Preventive Health & Screening: campaigns, reminders and test scheduling.

By End Use

Individual Consumers: D2C subscriptions, self-monitoring and community features.

Telemedicine Providers: White-label or integrated platforms for scaling consultations.

Hospitals & Clinics: Clinical grade devices, EHR integrations and provider dashboards.

Diagnostic Centers: Lab reporting and integration workflows.

Research & Academic Institutes: De-identified datasets for large-scale studies.

By Technology

Cloud Platforms: Multi-tenant SaaS, scalability and data centralization.

AI & ML: Personalization and decision support.

IoT-enabled Devices: Continuous data ingestion from wearables and sensors.

Big Data Analytics: Population insights, cohort analysis.

Blockchain: Secure credentialing and immutable patient records (pilot stage).

By Delivery Mode

Mobile-based Platforms: Highest engagement, device feature access (sensors).

Web-based Platforms: Provider portals, multi-user admin panels and accessibility.

On-premise Solutions: For hospitals needing data control and compliance.

Top 5 FAQs

Q1 — How fast will APAC women’s digital health grow?

A: From USD 889.14M in 2025 to USD 5.691B by 2034 — a 22.74% CAGR (2025–2034), implying ~6.4× growth in that window.

Q2 — Which product types and delivery modes matter most today?

A: Mobile health applications held the largest product share in 2024 (40%), and mobile-based delivery led with 55% share. Wearables are the fastest-growing product segment.

Q3 — Which applications will drive future growth?

A: Fertility & pregnancy management was the largest application (35% share in 2024), while mental health & wellness is forecast to grow fastest.

Q4 — How important is AI and cloud tech?

A: Very; cloud platforms held 45% share in 2024 and AI/ML is the fastest-growing technology — central to predictive care, imaging assistance and personalization.

Q5 — What are the biggest constraints to scaling?

A: The critical restraints are access in rural areas, regulatory fragmentation across APAC and data privacy/trust issues — all of which require policy, product and partnership solutions.

Access our exclusive, data-rich dashboard dedicated to the healthcare market – built specifically for decision-makers, strategists, and industry leaders. The dashboard features comprehensive statistical data, segment-wise market breakdowns, regional performance shares, detailed company profiles, annual updates, and much more. From market sizing to competitive intelligence, this powerful tool is one-stop solution to your gateway.

Access the Dashboard: https://www.towardshealthcare.com/access-dashboard

Immediate Delivery Available | Buy This Premium Research @ https://www.towardshealthcare.com/price/5808

Become a valued research partner with us – https://www.towardshealthcare.com/schedule-meeting

You can place an order or ask any questions, please feel free to contact us at [email protected]

Powering Healthcare Leaders with Real-Time Insights: https://www.towardshealthcare.com/healthcare-intelligence-platform

Europe Region – +44 778 256 0738

North America Region – +1 8044 4193 44

APAC Region: +91 9356 9282 04

Web: https://www.towardshealthcare.com

Find us on social platforms: LinkedIn | Twitter | Instagram | Medium | Pinterest