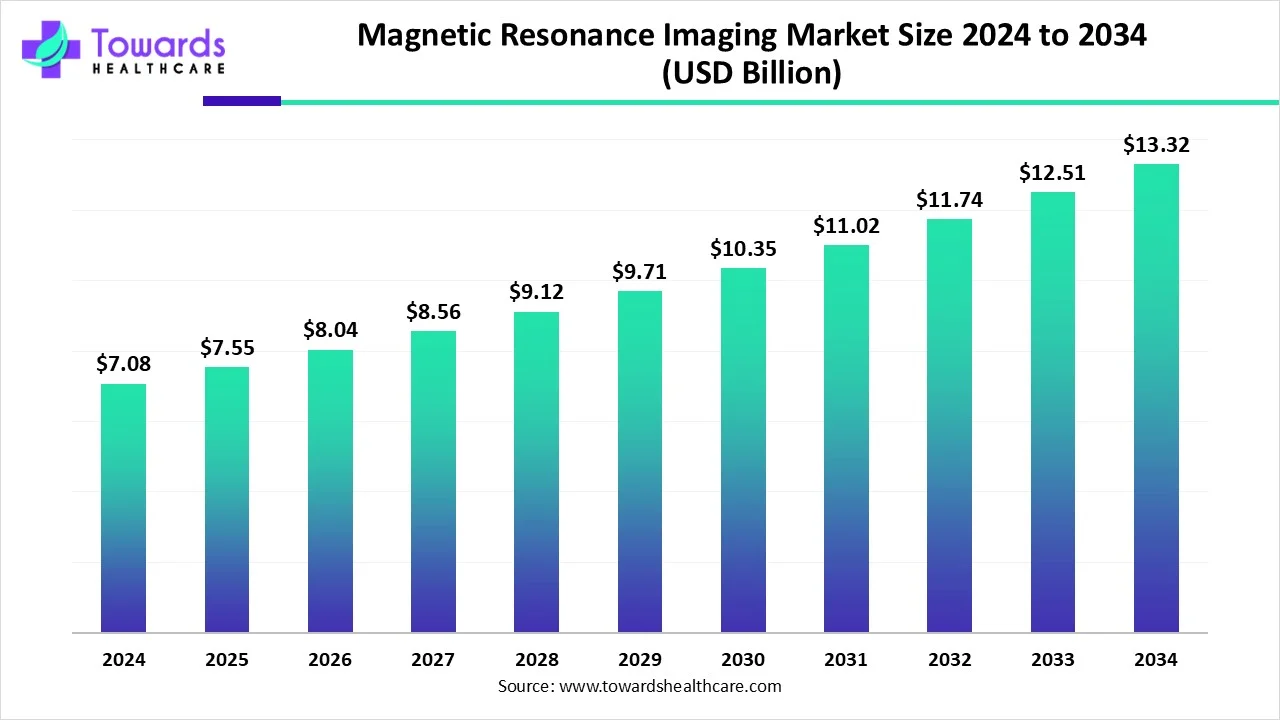

The global MRI market is projected to grow from USD 7.55 billion (2025) to USD 13.32 billion (2034) — a CAGR of 6.52% (2025–2034) — driven by rising diagnostic demand, regional expansion (North America 38% share in 2023; fastest APAC growth), and technology advances that are reducing cost, scan time and improving accessibility.

Market size

Base & forecast figures

Market value: USD 7.55 billion in 2025 → USD 13.32 billion by 2034.

Forecast CAGR: 6.52% for 2025–2034.

Historic / reference year shares (2023)

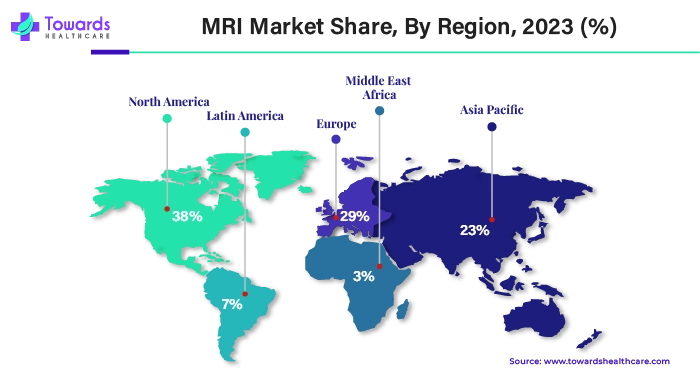

North America: 38% revenue share (2023) — largest regional contributor.

Architecture (2023): Closed MRI systems = 77% revenue share.

Field strength (2023): Mid-field strength = >49% revenue share.

Application (2023): Brain & neurological = 24% revenue share.

End-use (2023): Hospitals = >40% revenue share.

Regional growth rates used in sizing

Asia Pacific noted as fastest regional CAGR (example figure given: 7.4%).

Open MRI systems expected to grow at ~7.72% CAGR (architecture sub-growth).

Unit intensity example (country level)

Germany: ~1.39 MRI units per 100,000 people (2024) projected to 1.47 (2025) — indicates capacity increases in developed markets.

Market drivers embedded in size

Rising prevalence of cancer and chronic diseases, improved hospital imaging budgets, and technology (mid-field portability, open MRI, AI speedups) expand addressable demand and capacity — reflected in the above growth numbers.

Market trends

Shift to mid-field & portable systems

Mid-field (>49% share in 2023) is valued for lower energy, smaller footprint and easier deployment (including mobile units).

Open MRI adoption rising

Open systems reduce claustrophobia and support larger patients; open MRI segment growing faster (projected ~7.72% CAGR) even though closed systems held 77% revenue in 2023.

High-field imaging gaining ground

High-field (1.5T–3.0T) is the fastest growing field‐strength segment for higher resolution diagnostic work; complements mid-field expansion for different use cases.

Hospitals remain primary buyers

40% revenue from hospitals (2023) — due to capital budgets, integrated care and the need for specialist staffing and follow-up services.

Asia-Pacific infrastructure expansion

APAC fastest regional CAGR (noted 7.4%) driven by healthcare investment, domestic manufacturing initiatives (e.g., FMVL in Chennai, Voxelgrids in India).

Clinical demand driven by oncology & neurology

Brain & neurological imaging largest application (24% in 2023); growing cancer screening and follow-up imaging use cases support MRI volume growth.

Cost pressure & affordability challenge

High capital and setup costs (equipment USD 150k–3M; facility/setup up to ~USD 5M cited) limit deployment in lower-income settings.

Scan time reduction as a service engine

AI methods (example: Monash McSTRA) and ultra-powerful scanners (CEA example) are enabling multi-minute or under-5-minute scans, improving throughput and access.

Helium-independence & sustainability

Innovations (e.g., Siemens DryCool, Voxelgrids using liquid nitrogen) reduce reliance on helium and operating constraints — lowers lifecycle costs and supply risk.

Software & therapy integration

MRI integration into therapy planning (e.g., MRI-based HDR brachytherapy planning, GE MIM Symphony HDR updates) expands MRI’s role beyond diagnostics into treatment planning.

AI roles/impacts in the MRI market

Radical scan-time reduction (through reconstruction & inference)

Example from the provided content: Monash University’s McSTRA AI produced clinically useful images in a fraction of the time vs. traditional methods — enabling 5-minute full-body or multi-region exams and 10x throughput gains. Faster scans increase patient throughput and reduce per-scan cost.

Image quality enhancement (super-resolution & denoising)

AI reconstructs higher quality images from undersampled k-space data; this lets lower-field or faster protocols emulate higher-field clarity, narrowing the gap between mid-field and high-field for many clinical tasks.

Protocol optimization & automated exam tailoring

AI can recommend tailored sequences based on clinical question, patient morphology and prior images — saving scanner time and standardizing exam quality across technicians and sites.

Automated segmentation and quantification

AI automates lesion segmentation (brain tumors, breast lesions), volumetrics and biomarkers — accelerating radiologist workflows and supporting objective longitudinal tracking.

AI-assisted triage & workflow prioritization

Embedded models flag urgent findings (hemorrhage, large mass) enabling faster radiology response and better resource allocation in high-volume hospitals.

Synthesizing sequences to reduce contrast use

AI can synthesize contrast-enhanced-like images or generate missing sequences, reducing gadolinium usage and scan steps for some indications.

Cross-modality registration and treatment planning

AI aligns MRI with CT/US for therapy planning (example: MRI-HDR brachytherapy planning improvements) enabling more precise radiation dosing and interventional guidance.

Operational analytics for capacity & maintenance

Predictive maintenance models forecast downtime, optimize service schedules and extend magnet uptime — lowering total cost of ownership for hospitals and imaging centers.

Enabling lower-cost hardware to reach clinical thresholds

AI improves diagnostic performance of low-field or mid-field systems, making them clinically acceptable for many indications and expanding access in resource-limited regions.

Regulatory & validation accelerators (model-driven evidence)

AI can automate performance evaluation across multi-site datasets, helping vendors gather validation evidence faster for new sequences, workflows or hardware integrations — speeding market introduction of innovations.

Regional insights

North America (dominant — 38% revenue share, 2023)

a. High installed base & reimbursement environment: Established hospital budgets and reimbursement mechanisms support high per-unit utilization.

b. Innovation & manufacturing anchor: Major players (Siemens, GE, Philips) have deep R&D and local presence; investment in hybrid systems and advanced magnets (e.g., Siemens DryCool UK investment) influences global supply chains.

c. Clinical demand concentration: High levels of cancer detection, neurological care and cardiac imaging maintain steady MRI utilization.

Asia Pacific (fastest CAGR — 7.4%)

a. Capacity expansion & domestic manufacturing: Initiatives like FMVL (Chennai) and Voxelgrids (India) reduce import dependence and lower local prices.

b. Diverse market segments: Large unmet demand in tier-2/3 cities supports adoption of mid-field and open MRIs that are cheaper and easier to deploy.

c. Policy & infrastructure upgrades: Healthcare reforms and hospital modernization programs accelerate purchases.

Europe

a. Screening & early detection programs: Country programs and favorable regulatory support increase MRI usage for chronic disease monitoring.

b. Per capita saturation differences: Germany’s MRI units per 100k (1.39 → 1.47) show incremental growth rather than leaps, indicating replacement/upgrade cycles and higher per-scanner utilization.

UK

a. High throughput & investment: NHS investments (e.g., £2.3 billion in MRI/CT capacity) and community diagnostic centers drive volumes (0.37 million MRI scans in May 2024).

b. Centralized purchasing & capacity planning: Public health models create large procurement cycles and opportunities for scalable vendors.

Latin America & MEA

a. Variable penetration & opportunity: Lower per-capita MRI units create greenfield opportunities for portable/mid-field systems and mobile imaging solutions.

b. Cost sensitivity: Preference for lower capital, lower operating cost systems; AI-enhanced mid-field systems are attractive.

Country examples illustrating tech diffusion

a. India: domestic production initiatives (FMVL; Voxelgrids) + first clinical MRI rollout reduce import bills and create localized price competition.

b. Jammu & Kashmir (India) example: Hexamed introduced a 48-channel MRI (July 2024) — shows regional centers upgrading to high-channel systems for better throughput/resolution.

Market dynamics

Demand growth driven by disease burden

Rising cancer incidence and neurological disease (WHO estimates cited) increases MRI utilization for diagnosis, staging and treatment planning.

Supply constraints & capital intensity

High purchase price (USD 150k–3M) and facility setup (up to USD 5M) slow installations in low-resource settings; financing & leasing structures become important.

Technology substitution & segmentation

Mid-field and open MRIs expand accessible service points; high-field remains necessary for complex diagnostics — market segments coexist rather than fully replace one another.

Throughput economics as a competitive lever

AI and fast scanners reduce per-scan time, improving return on investment and enabling operators to lower prices or increase margins.

Service, software & ecosystem revenue

Maintenance, software upgrades (e.g., MIM Symphony HDR Prostate) and advanced sequences create recurring revenue streams beyond hardware sale.

Supply-chain & resource risk (helium dependence)

Helium scarcity and cost push vendors toward helium-saving or helium-free technologies (Siemens DryCool; liquid nitrogen approaches) to de-risk operations.

Regulatory & reimbursement environment

Public health investments (e.g., NHS spending) and screening recommendations directly affect market uptake; reimbursement parity for MRI vs alternative imaging influences modality choice.

Local manufacturing & price competition

Domestic players (FMVL, Voxelgrids) can lower entry costs and accelerate adoption in price-sensitive markets, pressuring global vendors to offer lower-cost models.

Consolidation & partnerships

Large vendors’ investments in production facilities and partnerships with software firms indicate vertical integration to control cost and feature set.

Clinical expansion into therapy

MRI’s role expands from diagnosis to treatment planning (e.g., brachytherapy), creating demand for integrated software and MRI-compatible interventional suites.

Top 10 companies

Siemens Healthineers

Product/overview: Full range of MRI scanners; investing in magnet production (North Oxfordshire DryCool plant).

Strength: Large R&D footprint, verticalizing magnet production, sustainability focus (DryCool reduces helium from ~1,500 L to <1 L), strong global reach.

GE Healthcare

Product/overview: MRI systems + software ecosystem (MIM Software subsidiary updates for HDR brachytherapy).

Strength: Broad modality portfolio and software integration for therapy planning — strong clinical workflows.

Philips (Koninklijke Philips N.V.)

Product/overview: Comprehensive MRI platforms (high- and mid-field); emphasis on patient comfort and integrated imaging solutions.

Strength: Strength in cross-modal integration and hospital enterprise solutions.

Canon Medical Systems (incl. Toshiba legacy)

Product/overview: MRI systems and service solutions (Toshiba Medical Systems contribution cited).

Strength: Service & maintenance capabilities and long heritage in imaging tech.

Hitachi Healthcare

Product/overview: Known for open MRI systems and alternative designs that improve patient comfort.

Strength: Open MRI expertise — helps address claustrophobia and large-patient needs.

Fujifilm Holdings Corporation

Product/overview: Imaging systems; launched Echelon Synergy MRI (CT & MRI User Conclave, March 2024).

Strength: Strong imaging portfolio and regional market activity (India product introductions and user conclaves).

Shimadzu Corporation

Product/overview: Precision instruments and medical equipment; growing sales (net sales 2024 = ¥384 billion, targeting ¥540 billion FY 2025 per your data).

Strength: Manufacturing scale and precision instrument heritage.

Bruker Corporation

Product/overview: Specialty MRI/physics and research imaging systems.

Strength: Strong in research and specialized imaging niches; appeals to academic market.

Esaote SPA

Product/overview: Compact MRI systems and specialized scanners (often for extremity or dedicated applications).

Strength: Niche, cost-sensitive devices targeted at clinics and smaller centers.

Hologic Inc.

Product/overview: Breast imaging and related technologies — relevant as breast MRI demand grows.

Strength: Specialty focus on women’s imaging and diagnostic ecosystems.

Latest announcements

Siemens Healthineers — DryCool magnet plant (May 2024)

Detail: $250 million investment in a North Oxfordshire production facility to manufacture superconducting magnets. DryCool technology reduces helium usage dramatically (from ~1,500 L to <1 L). Expected to create >1,300 jobs and produce the first UK-made MRI scanner. Impact: lowers supply-chain vulnerability, reduces long-term operating costs and improves sustainability.

Fujifilm — Echelon Synergy MRI (March 2–3, 2024)

Detail: Launched Echelon Synergy MRI at a CT & MRI User Conclave in Mumbai. Impact: strengthens Fujifilm India’s product lineup and supports regional user education.

Voxelgrids (Bangalore) — helium-independent MRI (Aug/Oct 2023 → clinical launch Oct 2023)

Detail: First made-in-India scanner designed to use liquid nitrogen rather than liquid helium; slated for clinical launch in October. Impact: localizes advanced tech and reduces operating constraints and import dependence.

FMVL (Fischer Medical Ventures, Chennai) — domestic MRI production (May 2024)

Detail: Claimed to be first domestically producing MRI systems in India to reduce dependency on imports and expand product offerings via acquisitions/investments. Impact: price pressure and improved access in India.

Hexamed Diagnostics — 48-channel MRI (July 2024)

Detail: Introduced first 48-channel MRI in Jammu & Kashmir, delivering higher channel counts for faster imaging and better resolution. Impact: Regional upgrading of imaging capability and throughput.

GE HealthCare / MIM Software — HDR brachytherapy planning update (July 2024)

Detail: MIM Symphony HDR Prostate now matches MRI contours with real-time ultrasound for HDR planning. Impact: advances MRI role in therapy planning and interventional workflows.

Sir H.N. Reliance Foundation Hospital — open MRI installation (June 2024)

Detail: Deployed open MRI to reduce claustrophobia and provide patient-friendly imaging with high detail. Impact: local example of open MRI adoption for patient comfort and specialized needs.

Regional policy & capacity investments (UK / NHS data)

Detail: NHS invested £2.3 billion into MRI/CT capacity; England reported 0.37 million MRI scans in May 2024. Impact: public capital injections expand capacity and scanning volumes.

Recent developments

Faster clinical scanners & AI reconstruction — McSTRA and ultra-powerful scanners allow sub-5-minute brain scans and markedly shorter full exams.

Domestic manufacturing pushes — India examples (FMVL, Voxelgrids) aiming to lower import dependence and costs.

Higher channel & advanced systems — 48-channel systems deployed regionally for higher throughput/resolution.

MRI in therapy planning — Software updates enabling MRI-based HDR brachytherapy planning increase MRI’s therapeutic role.

Sustainability & helium-saving tech — Siemens DryCool and liquid nitrogen approaches reduce helium reliance.

Segments covered

1. By Architecture

Open System MRI

Design & Patient Experience: Open MRIs feature a more accessible, open design with magnets positioned above and below, rather than in a tight cylindrical capsule. This reduces claustrophobia and panic in patients, including children, obese individuals, or those with anxiety disorders.

Clinical Adoption Trend: Growing rapidly due to patient-friendly design and increasing demand in hospitals and diagnostic centers where patient comfort is prioritized.

Diagnostic Capability: While slightly lower magnetic field strength than closed systems, modern open MRIs provide sufficient resolution for many routine diagnostic tasks.

Strategic Impact: As awareness grows around patient comfort and scan compliance, open MRIs expand MRI accessibility in underserved markets.

Closed System MRI

Design & Imaging Advantage: Capsule-like design enables higher magnetic field strengths (often high-field 1.5–3.0T), producing superior image clarity for complex diagnostics.

Revenue Dominance: Represented 77% of market revenue in 2023 due to widespread use in high-end hospital settings.

Clinical Use: Preferred for neurology, oncology, and other applications requiring high-resolution imaging; supports advanced sequences and contrast-enhanced imaging.

Limitations: Claustrophobia and size constraints can limit patient throughput; not ideal for all patient populations.

By Field Strength

Low Field Strength MRI

Use Case & Advantages: Operates at <1.0T; offers lower capital and operational costs and consumes less energy.

Niche Applications: Suitable for screening, extremity imaging, and point-of-care settings (mobile units or smaller clinics).

Trade-off: Lower image quality compared to mid- and high-field systems; not ideal for complex diagnostics.

Mid Field Strength MRI

Market Share & Adoption: Dominated >49% of revenue in 2023, reflecting balance of cost, quality, and accessibility.

Operational Advantage: Smaller footprint enables deployment in hospital wings, outpatient imaging centers, and even mobile units.

Clinical Impact: Adequate for general diagnostics, spine, musculoskeletal, and many neurological applications without requiring high-field infrastructure.

High Field Strength MRI

Technology & Capabilities: 1.5–3.0T systems; gold standard for high-resolution imaging.

Growth: Fastest-growing field-strength category due to rising demand for advanced diagnostics and oncology imaging.

Clinical Use: Critical for brain, breast, cardiac, and cancer imaging where detailed structural information is necessary.

Infrastructure Requirement: Larger space, higher energy consumption, specialized shielding, and trained personnel.

By End-use

Hospitals

Revenue Contribution: Largest share >40% in 2023.

Reason: Hospitals can invest in full-size MRI systems, manage operating costs, and provide comprehensive care, including follow-up and multi-disciplinary consultation.

Strategic Advantage: High patient volume, trained radiologists, and integrated software allow efficient use of high-field MRI systems.

Imaging Centers

Role: Drive outpatient access, offer cost-efficient alternatives to hospitals, and cater to routine scans.

Trend: Increasing adoption of mid-field and open MRI systems to reduce costs and improve patient throughput.

Ambulatory Surgical Centers (ASCs)

Function: Provide targeted imaging support for procedural or pre-operative diagnostics.

Adoption Drivers: Require mid-field or portable MRIs that balance space, cost, and efficiency.

Others

Scope: Includes research institutes, specialty clinics, and mobile imaging providers.

Importance: Support niche applications (e.g., veterinary imaging, extremity-focused MRI, clinical trials), expanding the overall market ecosystem.

By Region

North America

Revenue Share: 38% in 2023; largest market globally.

Drivers: Reimbursement systems, high adoption of high-field MRI, and hospital investment capacity.

Europe

Drivers: Government-backed chronic disease screening, increasing chronic care infrastructure, moderate growth due to relatively high saturation of MRI units.

Asia Pacific

Growth: Fastest CAGR (~7.4%); driven by domestic manufacturing (FMVL, Voxelgrids), healthcare reforms, and infrastructure expansion.

Trend: Mid-field and open MRI adoption to meet large population demand.

Latin America & MEA

Trend: Lower per-capita MRI units; opportunity for cost-effective, mid-field, or portable MRI systems.

Drivers: Price sensitivity and emerging healthcare infrastructure.

By Clinical Application

Neurology/Brain

Revenue Share: Largest segment at 24% in 2023.

Clinical Advantage: MRI is most sensitive modality for detecting brain tumors, metastases, and neurological abnormalities.

Spine & Musculoskeletal

Usage: Imaging structural disorders, trauma, and orthopedic follow-ups; mid-field systems often sufficient.

Cardiac & Vascular

Requirement: High-field MRI preferred for detailed imaging of heart chambers, coronary arteries, and vascular anomalies.

Abdominal

Use Case: Liver, kidney, and soft tissue imaging; requires high-quality sequences but can use mid-field MRI for many routine cases.

Breast

Trend: Growing adoption due to high sensitivity in detecting small lesions; often combined with mammography/ultrasound.

OSA (Obstructive Sleep Apnea)

Usage: MRI applied for anatomical airway assessment; niche but growing in research and clinical diagnostics.

Other Applications

Scope: Includes extremity MRI, pediatric imaging, functional MRI (fMRI), and research-focused studies.

Top 5 FAQs

-

Q: How big is the MRI market and how fast is it growing?

A: Projected from USD 7.55 billion (2025) to USD 13.32 billion (2034) — CAGR 6.52% (2025–2034). -

Q: Which region currently leads the MRI market?

A: North America with 38% revenue share in 2023; Asia-Pacific is the fastest growing region (approx 7.4% CAGR). -

Q: Which MRI architectures and field strengths dominate today?

A: Closed MRI systems generated 77% of revenue in 2023; mid-field strength systems held >49% share in 2023, while high-field systems are the fastest growing field-strength category. -

Q: What are the main restraints to wider MRI adoption?

A: High capital cost (equipment USD 150k–3M), expensive facility setup (up to USD 5M), and operating costs — these limit deployment in resource-constrained settings. -

Q: How is technology changing MRI economics and accessibility?

A: AI reconstruction (e.g., McSTRA) and faster scanners reduce scan time (potentially under 5 minutes), increasing throughput and lowering per-scan costs; helium-saving technologies (DryCool, liquid nitrogen designs) reduce operating constraints and lifecycle costs.

Access our exclusive, data-rich dashboard dedicated to the diagnostics industries– built specifically for decision-makers, strategists, and industry leaders. The dashboard features comprehensive statistical data, segment-wise market breakdowns, regional performance shares, detailed company profiles, annual updates, and much more. From market sizing to competitive intelligence, this powerful tool is one-stop solution to your gateway.

Access the Dashboard: https://www.towardshealthcare.com/access-dashboard

Immediate Delivery Available | Buy This Premium Research @ https://www.towardshealthcare.com/price/5181

Become a valued research partner with us – https://www.towardshealthcare.com/schedule-meeting

You can place an order or ask any questions, please feel free to contact us at [email protected]

Powering Healthcare Leaders with Real-Time Insights: https://www.towardshealthcare.com/healthcare-intelligence-platform

Europe Region – +44 778 256 0738

North America Region – +1 8044 4193 44

APAC Region: +91 9356 9282 04

Web: https://www.towardshealthcare.com

Find us on social platforms: LinkedIn | Twitter | Instagram | Medium | Pinterest