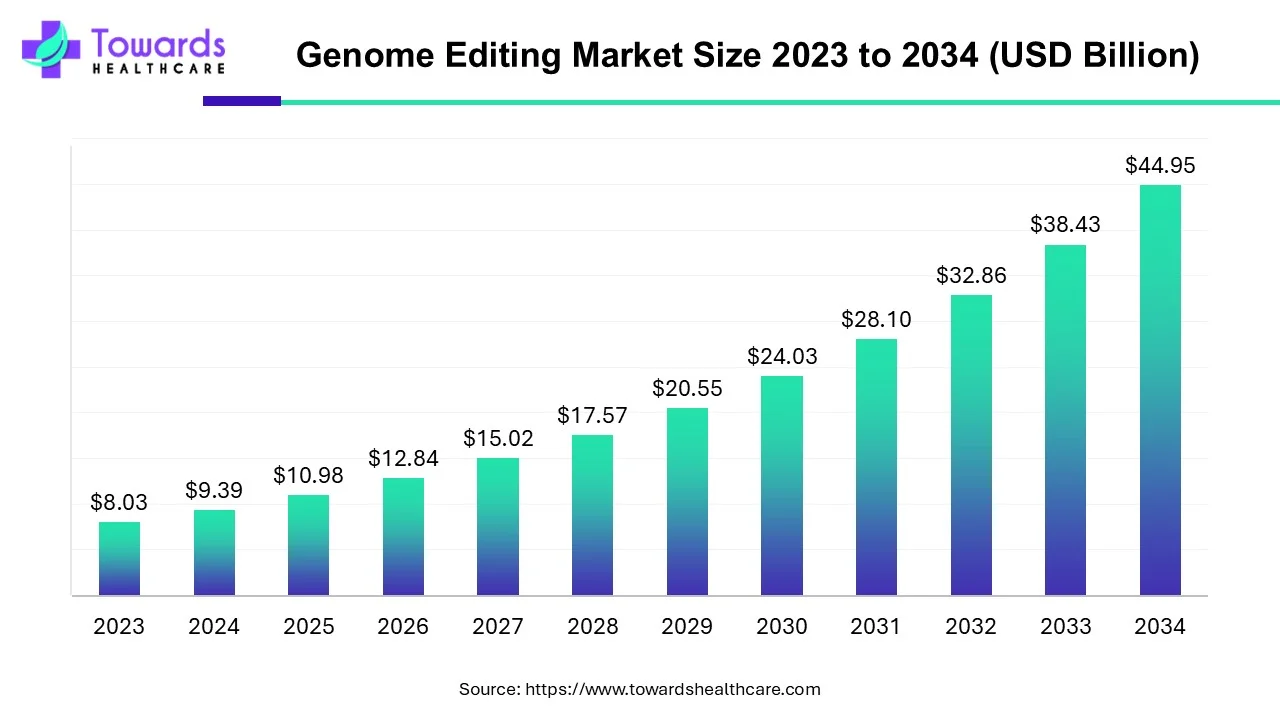

The global genome editing market is forecast to grow from USD 10.98 billion in 2025 to USD 44.95 billion by 2034, representing a CAGR of 16.95% from 2025–2034 — powered by rapid clinical translation, expanding commercial products, stronger regional investments (North America 48% revenue share in 2023), and accelerating tech & delivery improvements.

Download the free sample and get the complete insights and forecasts report on this market @ https://www.towardshealthcare.com/download-sample/5161

Market-size analysis

Base numbers & horizon

● 2025: USD 10.98B (report baseline).

● 2034 forecast: USD 44.95B.

● Compound Annual Growth Rate (2025–2034): 16.95% — indicating multi-fold expansion over ~9 years.

Absolute scale-up implied

● The market is expected to increase by USD 33.97B over the forecast period (44.95 − 10.98 = 33.97B), reflecting both product commercialization and platform scale.

Revenue concentration vs. growth pockets

● North America held 48% of revenue in 2023 — a mature commercial nucleus (large pharma, deep VC, clinical-stage programs).

● Asia-Pacific is the fastest growth region (projected CAGR 18.77%) — indicating catch-up in capability, manufacturing, and clinical adoption.

Technology mix contributes to value

● CRISPR/Cas9 accounted for >44% of 2023 revenue — the dominant value driver due to low cost and broad adoption, while alternative platforms (ZFN, TALENs) remain valuable niche or specialized revenue contributors.

Delivery method skew

● Ex-vivo delivery generated >52% revenue in 2023 (controlled manufacturing workflows, cell therapy commercialization).

● In-vivo shows much faster projected growth (CAGR ~19.95%) — signaling important future revenue shifts as delivery barriers are solved.

End-use concentration

● Biotechnology & pharma companies captured >52% share in 2023 — they are the primary buyers (R&D tools, therapeutic programs), while academic & research institutions show the fastest growth (CAGR ~19.24%) as research scales.

Market depth vs. breadth

● Depth: Established clinical assets (exa-cel, CAR-T programs) concentrate high per-asset revenue and reimbursement potential.

● Breadth: Toolkits, reagents, services, sequencing/analytics, and contract services expand TAM substantially.

Capital intensity & commercial timing

● Large near-term revenue inflections come from a handful of clinical approvals / reimbursements (gene-edited therapeutics). Tool/reagent sales provide recurring, lower-ticket revenue supporting overall market stability.

Regulatory & ethics effect on market size

● Regulatory clarity (e.g., country-level guidance) accelerates commercialization; uncertainty delays market capture, creating step-wise jumps rather than smooth growth.

Downstream impact on adjacent markets

● Growth lifts related markets: delivery technologies, GMP manufacturing, cell-therapy infrastructure, genomic diagnostics, and AI design tools — increasing the effective addressable market beyond the raw genome-editing spend.

Market trends

Clinical translation accelerating to the clinic

● Examples: VERVE-101 (base editing program dosing in 2022) and the first personalized CRISPR therapy treated at Children’s Hospital of Philadelphia (May 2025) — demonstrating clinical momentum and de-risking therapeutic models.

Platform consolidation around CRISPR + next-gen editors

● CRISPR/Cas9 dominated 2023 (>44% revenue). The market trend is to combine CRISPR with base and prime editors for precision and reduced off-target effects.

Shift from ex-vivo dominance to rapid in-vivo adoption

● Ex-vivo generated >52% revenue in 2023; however in-vivo growth CAGR (~19.95%) indicates an upcoming balance as delivery solutions mature (AAV, LNPs, novel viral/non-viral vectors).

AI integration into design & discovery

● AI-driven design (e.g., OpenCRISPR / AI-generated editors, April 2024) is moving from proof-of-concept to productization, improving guide selection, off-target prediction, and novel nuclease design.

Commercialization of off-the-shelf reagents & GMP enzyme supply

● Increasing availability of GMP Cas9 and standardized reagents (e.g., commercial Cas9 launch in 2025) reduces entry friction for clinical programs.

Expanded non-therapeutic markets — agriculture, industrial biotech

● Field trials (Italy, April 2024, genetically altered rice) and agricultural applications broaden market demand beyond human therapeutics.

Multi-stakeholder funding & national genomic strategies

● National strategies (e.g., Canada’s CAD 175.1M genomics plan starting 2024–25; India’s DBT efforts; UK 10-year health/genomics plan announced July 2025) funnel funds into genomics and genome editing capabilities.

Increased M&A and strategic alliances

● Partnerships like Regeneron + Mammoth (April 2025) highlight strategic scaling of in-house gene editing capabilities by larger pharma.

Growing focus on ethical, regulatory frameworks

● Countries publishing ethics guidance (China) and programmatic newborn genomics studies (Genomics England) reflect parallel growth in regulatory oversight — shaping adoption timelines.

Service and CRO expansion to support scalable development

● The growth of contract research and manufacturing organizations supports the surge in ex-vivo programs and will increasingly service in-vivo product pipelines.

AI impact / role in the genome-editing market

AI-driven nuclease & editor design (de novo proteins)

● What it does: Designs novel Cas-like proteins and engineered nucleases from sequence and structure predictions.

● Why it matters: Enables editors with altered PAM recognition, compact size for in-vivo delivery, or higher fidelity. Example: OpenCRISPR (April 2024) — AI-generated gene editor demonstrates feasibility.

Guide RNA (gRNA) optimization and off-target avoidance

● What it does: ML models rank candidate guides by predicted on-target efficacy and off-target risk.

● Why it matters: Minimizes safety risks, increases editing precision — accelerates clinical candidate selection and reduces wet-lab cycles.

Off-target prediction and safety scoring

● What it does: Predicts genome-wide unintended cleavage sites using ensemble models integrating chromatin state, sequence context, and repair signatures.

● Why it matters: Critical regulatory evidence and risk mitigation to satisfy regulators; directly combats the key restraint “off-target effects.”

AI-assisted delivery vehicle selection & payload optimization

● What it does: Predicts the best vector/particle design (AAV capsid variants, LNP formulations) for tissue tropism and immune evasion.

● Why it matters: Accelerates in-vivo program feasibility, reducing formulation experimentation and time-to-clinic.

Automated experimental design & active learning

● What it does: Uses active learning loops to propose the next most informative experiments, minimizing required runs.

● Why it matters: Faster iteration, lower cost per lead; especially powerful for high-throughput screens and base/prime editing optimization.

Patient stratification & response prediction

● What it does: Integrates genomic, clinical, and biomarker data to predict which patients will benefit from a given edit/therapy.

● Why it matters: Improves trial design, increases effect sizes, and supports precision enrollment — increasing the chance of successful clinical outcomes.

Manufacturing process optimization (GMP scale)

● What it does: Predictive models optimize culture conditions, vector yields, and QC thresholds.

● Why it matters: Reduces cost-of-goods, improves batch consistency for ex-vivo cell-therapy manufacturing where >52% revenue currently sits.

Regulatory dossier support & in silico evidence

● What it does: AI generates predictive safety assessments and interpretable reports to support IND/CTA filings.

● Why it matters: Strengthens regulatory submissions and can shorten preclinical requirements by providing high-quality in silico evidence.

Design of multi-modal therapeutics (combo strategies)

● What it does: Models interactions between edits, small molecules, and immune modulators to design synergistic regimens.

● Why it matters: Enables combination strategies (e.g., editing + immunomodulation) and refines dosing regimens—critical in complex diseases like oncology.

Enabling democratized research tools & open science

● What it does: Open AI models (OpenCRISPR style) and predictive tools lower barriers for academic labs and startups.

● Why it matters: Expands the innovation base (boosts the academic & research institutions segment growth ~19.24% CAGR), but raises ethical/governance questions that must be managed.

Regional insights

A. North America (dominant market, 48% revenue in 2023)

Clinical & commercial lead

Strong network of biotech, big pharma, deep VC, and leading academic centers (examples include Children’s Hospital of Philadelphia dosing in May 2025).

Regulatory infrastructure & reimbursement pathways

FDA, NIH, and other agencies provide relatively clear regulatory pathways for gene therapies; this reduces commercialization risk and attracts investment.

Manufacturing & services concentration

Large network of GMP facilities, CROs, and specialized cell-therapy plants supports ex-vivo program scaling — sustaining >52% ex-vivo revenue.

M&A & strategic alliances

Big pharmas forming alliances (e.g., Regeneron + Mammoth, April 2025) to integrate gene editing capabilities — consolidates technical leadership.

B. Asia-Pacific (fastest CAGR ~18.77%)

Rapid capacity build-out

China, India, Japan, and South Korea investing heavily in biotech infrastructure and startups (China: >500 genomics startups; India: DBT bioincubator growth).

Regulatory momentum & local trials

Country-specific guidance (e.g., China’s ethical guidelines) and large patient populations make APAC attractive for clinical trials and field trials in agriculture.

Cost-competitive manufacturing & scale

Lower costs and scaling potential for reagent production, contract manufacturing, and clinical trial enrollment are attractive to global players.

Policy & government funding

National genomic strategies and public funding (India’s bioeconomy targets; other governments) increase local adoption and home-grown innovation.

C. Europe

Strong research base & ethics focus

Europe provides rich academic research and public debate around ethics; government funding supports translational genomics (e.g., NHS genomics plan in the UK, July 2025).

Regulatory caution but infrastructure

Regulatory frameworks are robust and precautionary; adoption may be incremental but sustained by public health programs (newborn screening expansion).

D. Latin America & MEA

Emerging demand, slower commercialization

Smaller current market share but growing research adoption; potential in agriculture and population-specific genetic disease programs.

Dependence on imported reagents & partnerships

Growth likely to be driven by partnerships with global providers and capacity building.

Market dynamics

Drivers

Clinical progress & approvals — successful early clinical programs (e.g., VERVE-101 trials, May 2025 therapy dosing) drive investor confidence and clinical pipelines.

Lower sequencing & assay costs — cheaper genome characterization accelerates target discovery and patient identification.

Commercial reagent & enzyme availability — commercial GMP Cas9 availability (2025 announcements) reduces barriers for clinical programs.

Government funding & national strategies — Canada’s genomics strategy; India’s DBT and bioincubator expansion; UK genomics initiatives — all inject capital and infrastructure.

Broad end-use demand — biotech & pharma dominance (>52% share) provides reliable revenue; academia growth creates innovation pipeline.

Restraints

Off-target effects & safety concerns — a major structural restraint; unpredictable DNA cleavage can create harmful mutations and regulatory hurdles.

Delivery challenges for in-vivo applications — although in-vivo CAGR is high (~19.95%), safe targeted delivery to many tissues remains technically difficult.

Regulatory & ethical hurdles — germline editing concerns and varying national policies slow certain applications and create market uncertainty.

High development & manufacturing costs — especially for cell therapies (ex-vivo processes) and GMP biologics.

Opportunities

Gene therapy for rare diseases — large unmet need (millions affected; only ~5% of rare diseases have approved therapies) — high therapeutic value and willingness to pay.

AI-enabled acceleration — AI can reduce R&D time and cost, improve safety profiling, and design next-gen editors.

Agricultural and industrial applications — field trials (genetically edited rice in Italy, April 2024) and industrial strain engineering expand TAM outside human therapeutics.

Delivery platform commercialization — companies solving delivery problems capture outsized value (viral & non-viral vectors, nanoparticle design).

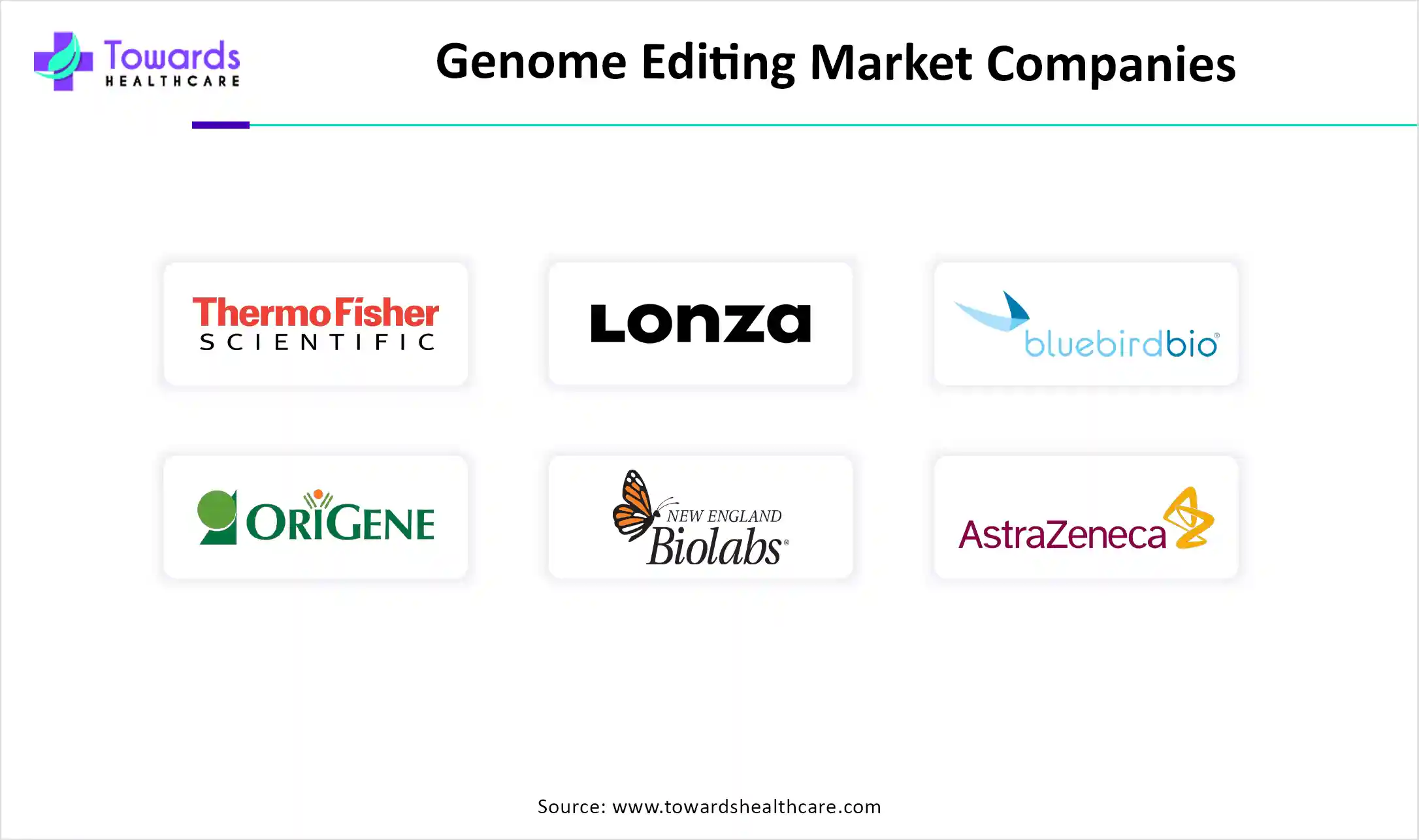

Top 10 companies

Thermo Fisher Scientific, Inc.

Overview: Global leader in life-science tools and consumables.

Product focus: Reagents, instruments, CRISPR toolkits, sequencing platforms and GMP supply chains.

Strength: Scale, distribution network, and integrated workflow offerings — enables broad market penetration across research and clinical customers.

Lonza

Overview: Contract development & manufacturing organization (CDMO) with cell & gene therapy manufacturing capability.

Product focus: GMP manufacturing, viral vector production, cell-therapy process development.

Strength: Manufacturing scale and regulatory experience critical for ex-vivo product commercialization.

Bluebird Bio, Inc.

Overview: Developer of gene therapies and engineered cell therapies.

Product focus: Gene addition and cell therapies (historically in hemoglobinopathies & oncology).

Strength: Clinical development expertise and experience navigating reimbursement and commercialization for gene products.

Revvity / Horizon Discovery (Horizon Discovery Ltd.)

Overview: Provider of engineered cell lines, reagents, and genomic services.

Product focus: CRISPR knockout/knock-in cell lines and research tools.

Strength: Deep portfolio for discovery-stage programs and translational assays.

New England Biolabs (NEB)

Overview: Enzyme manufacturer and reagent supplier.

Product focus: Nucleases, enzymes for CRISPR workflows, and molecular biology reagents.

Strength: Trusted enzyme quality, research trust, and product consistency.

Genscript Biotech Corp

Overview: Gene synthesis, CRISPR services and biologics manufacturing support.

Product focus: Custom gene services, CRISPR reagents, and protein production.

Strength: Cost-effective gene/clinically-oriented services and global footprint.

Danaher Corporation

Overview: Diversified life-science conglomerate with tools and diagnostics businesses.

Product focus: Instrumentation, sequencing, and diagnostic platforms that support genome editing R&D.

Strength: Broad product ecosystem enabling integrated workflows from discovery to QC.

Takara Bio Inc.

Overview: Provider of molecular biology reagents and single-cell genomics instruments.

Product focus: CRISPR kits, single-cell genomics and acquired spatial genomics capability (Curio Bioscience acquisition, Jan 2025).

Strength: Combined reagent & spatial genomics strengths accelerate complex biological readouts.

CRISPR Therapeutics

Overview: Clinical-stage company focused on CRISPR/Cas9-based therapeutics.

Product focus: Approved assets (exa-cel for β-thalassemia & sickle cell in some countries), and clinical programs (CTX211, CTX320, CTX310, CTX131, CTX112).

Strength: Deep therapeutic pipeline, clinical execution track record, and translational know-how.

Editas Medicine / Intellia Therapeutics / Sangamo (grouped choices depending on role) — example: Editas Medicine

Overview: Clinical pioneers in CRISPR/other editing platforms.

Product focus: In-vivo and ex-vivo edit programs across genetic diseases and ocular disorders.

Strength: Platform expertise, clinical stage candidates, and partnerships with pharma.

Latest announcements

CRISPR Therapeutics pipeline updates — multiple clinical programs advancing (CTX211 for T1DM; CTX320/Lp(a); CTX310/ANGPTL3; CTX131; CTX112). These programs represent diversity across CV, metabolic, and oncology indications.

Caribou Biosciences IND approval & GALLOP study (Apr 2024 / planned by end 2024) — FDA approved IND for CB-010 (anti-CD19 CAR-T with PD-1 KO) and anticipated multicenter GALLOP study for lupus nephritis and extrarenal lupus.

Profluent OpenCRISPR launch (Apr 2024) — release of an open-source AI-generated gene editor (OpenCRISPR-1), signaling AI’s entry into editor design.

Takara Bio acquisition of Curio Bioscience (Jan 2025) — strengthens single-cell + spatial genomics capability for genome editing readouts.

Biomay commercial availability of CRISPR/Cas9 nuclease (May 2025) — off-the-shelf GMP-grade Cas9 expands supply options for clinical programs.

Danaher + IGI research center (Jan 2024) — joint center to develop CRISPR-based gene treatments, combining industry resources with academic research.

EditCo Bio launch XDel Knockout Cells (Jan 2025) — new CRISPR knockout cell line product to streamline gene-editing workflows.

Regeneron + Mammoth alliance (Apr 2025) — Regeneron to access Mammoth’s ultracompact CRISPR platform for in-vivo programs targeting non-hepatic tissues.

Children’s Hospital of Philadelphia — personalized CRISPR therapy (May 2025) — first patient treated with personalized CRISPR gene editing therapy, a key clinical milestone.

UK 10-year genomics plan (July 2025) — expansion of NHS Genomics Medicine Service and Generation Study recruitment up to 100,000 newborns.

Recent developments

Open-source AI editors (Profluent, Apr 2024)

Significance: Demonstrates AI can design functional gene editors, accelerating discovery and potentially lowering R&D costs. Opens debate on governance and safeguards for democratized editor design.

Commercial GMP reagents (Biomay, May 2025)

Significance: Readily available GMP Cas9 reduces supply bottlenecks, smoothing the transition from preclinical to clinical manufacturing.

Spatial genomics consolidation (Takara + Curio, Jan 2025)

Significance: Merging single-cell and spatial readouts increases power to measure editing effects in tissue context — important for safety and efficacy assessment.

Academic–industry hubs (Danaher–IGI, Jan 2024)

Significance: Institutional collaborations accelerate translational pipelines and may standardize assays and regulatory approaches.

Clinical firsts & milestones (CHOP May 2025; VERVE-101 July 2022)

Significance: Clinical dosing milestones validate clinical feasibility and catalyze investor & payer interest; dosing of patients is a key inflection for valuation.

Regulatory & policy movements (China ethics guidance; UK genomics plan July 2025; Canada genomics funding)

Significance: Policy moves both enable and constrain activities — enabling by funding and structured programs; constraining when ethics tighten certain research (e.g., germline editing).

New product launches for research acceleration (EditCo XDel, Jan 2025)

Significance: Research-grade tools shorten timelines for model generation and functional studies — broadening the pipeline of translational candidates.

Segments covered

By Application

Genetic Engineering: Creation of GMOs, research models, and engineered cell lines — core revenue from research reagents and services.

Cell Line Engineering: Custom cell lines for drug discovery, toxicity screening, and functional genomics.

Animal Genetic Engineering: Preclinical models, disease modeling, and translational studies for therapeutic insight.

Plant Genetic Engineering: Crop trait improvement (disease resistance, yield), regulatory and field-trial adoption.

Others: Industrial strains, microbes for biomanufacturing, and synthetic biology applications.

Clinical Applications: Diagnostics, therapy development, and therapeutics — where major near-term revenue and payer dynamics appear.

By Technology

(CRISPR)/Cas9: Broadest adoption — cost-efficient and scalable; dominates revenue.

TALENs / MegaTALs: More precise for some targets; used when CRISPR not ideal.

ZFN: Established footprint in certain therapeutic programs; projected for significant CAGR (e.g., 16.58% indicated).

Meganuclease & Others: Specialized tools for niche applications.

By Delivery Method

Ex-vivo: Cells removed, edited, QC’d, and reintroduced — presently dominant (>52%), best for hematological conditions and many cell therapies.

In-vivo: Direct editing inside the body — fastest growing (CAGR ~19.95%), key to treating organ-specific diseases but faces delivery hurdles.

By End-use

Biotech & Pharma Companies: Primary commercial consumers (discovery, therapeutic development).

Academic & Government Research Institutes: Rapidest growth segment (CAGR ~19.24%); source of innovation and preclinical pipeline.

Contract Research Organizations (CROs): Provide outsourced services for trials, manufacturing, and scale-up.

By Region

North America, Europe, Asia Pacific, Latin America, MEA — regional differences in maturity, funding, regulatory approach, and adoption speed.

Top 5 FAQs

-

Q: What is the expected market size and growth of the genome editing market?

A: The market is expected to grow from USD 10.98 billion in 2025 to USD 44.95 billion by 2034, at a CAGR of 16.95% for 2025–2034. -

Q: Which region currently leads the genome editing market and which will grow fastest?

A: North America led in 2023 with approximately 48% revenue share. Asia-Pacific is projected to grow the fastest with a CAGR of ~18.77% during the forecast period. -

Q: What technology and delivery methods dominate the market today?

A: CRISPR/Cas9 contributed >44% of revenue in 2023, making it the dominant technology. Ex-vivo delivery generated >52% of revenue in 2023, though in-vivo methods are the fastest growing (CAGR ~19.95%). -

Q: What are the principal market restraints?

A: Major restraints include off-target effects (safety risks from unintended DNA changes), delivery challenges for in-vivo treatments, regulatory and ethical hurdles, and high development/manufacturing costs. -

Q: How is AI impacting the genome editing market?

A: AI is influencing editor design (AI-generated editors like OpenCRISPR, Apr 2024), gRNA optimization, off-target prediction, delivery vehicle selection, trial/patient stratification, and manufacturing optimization — collectively reducing timelines, improving safety predictions, and expanding the innovation base.

Access our exclusive, data-rich dashboard dedicated to the biotechnology industries – built specifically for decision-makers, strategists, and industry leaders. The dashboard features comprehensive statistical data, segment-wise market breakdowns, regional performance shares, detailed company profiles, annual updates, and much more. From market sizing to competitive intelligence, this powerful tool is one-stop solution to your gateway.

Access the Dashboard: https://www.towardshealthcare.com/access-dashboard

Immediate Delivery Available | Buy This Premium Research @ https://www.towardshealthcare.com/price/5161

Become a valued research partner with us – https://www.towardshealthcare.com/schedule-meeting

You can place an order or ask any questions, please feel free to contact us at [email protected]

Powering Healthcare Leaders with Real-Time Insights: https://www.towardshealthcare.com/healthcare-intelligence-platform

Europe Region – +44 778 256 0738

North America Region – +1 8044 4193 44

APAC Region: +91 9356 9282 04

Web: https://www.towardshealthcare.com

Find us on social platforms: LinkedIn | Twitter | Instagram | Medium | Pinterest