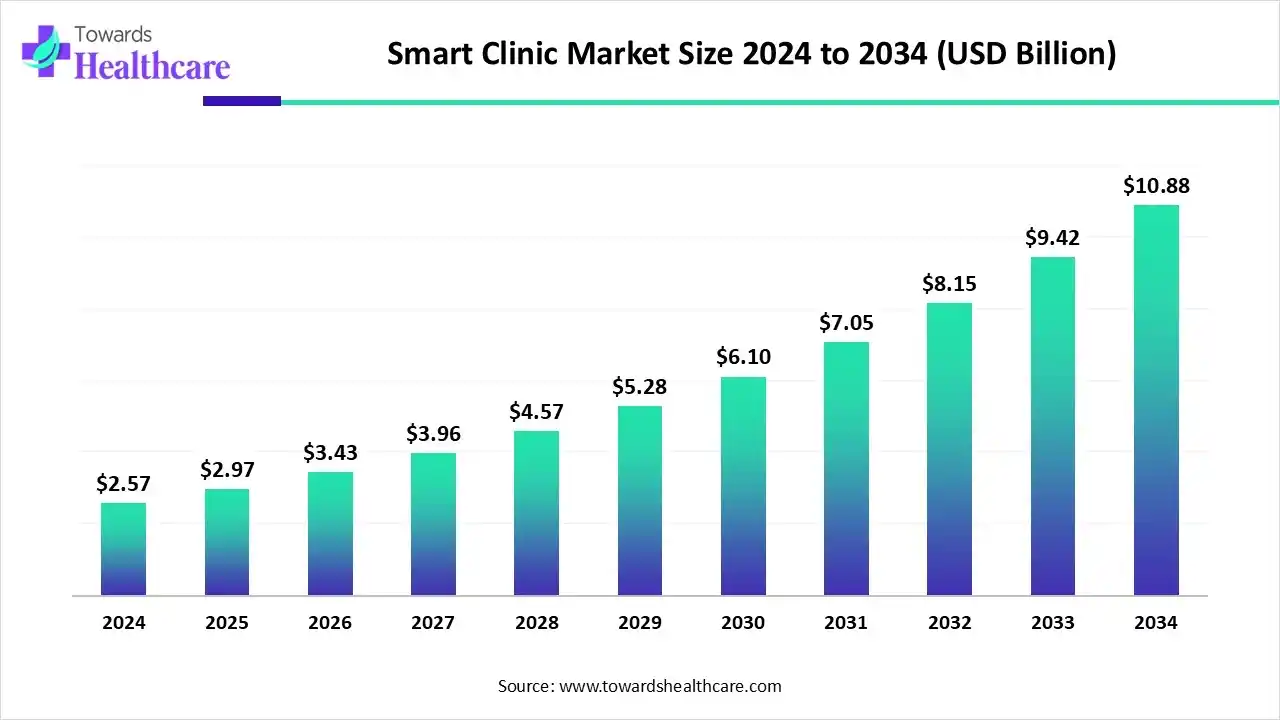

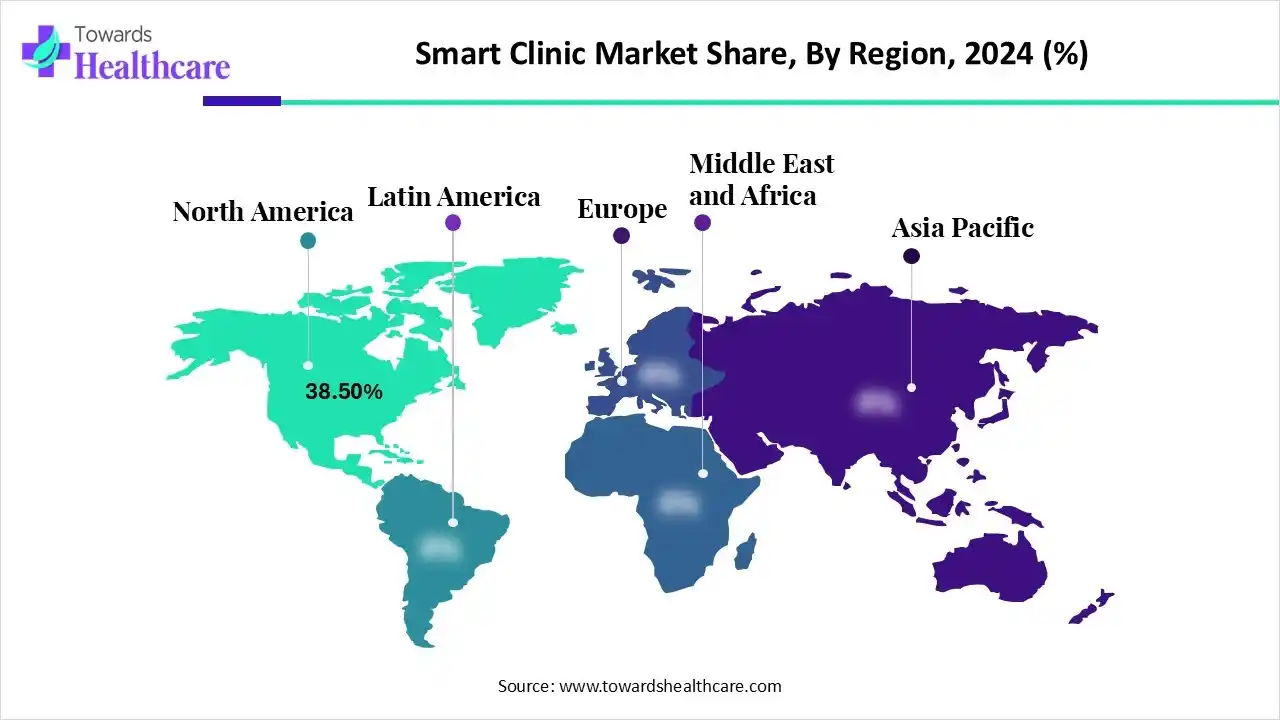

The smart clinic market grew from US$2.57B (2024) to US$2.97B (2025) and is set to exceed US$10.88B by 2034 (overall CAGR 15.47%; 2025–2034 CAGR 15.74%), propelled by AI, telemedicine, IoT, and cloud-first deployments, with North America at 38.5% (2024) and APAC as the fastest riser.

Download this Free Sample Now and Get the Complete Report and Insights of this Market Easily @ https://www.towardshealthcare.com/download-sample/6333

Market Size

●2024 baseline: US$2.57B, commercial traction established across virtual care, EHR, RPM, and cloud workflows.

●2025 checkpoint: US$2.97B, reflecting early AI augmentation of diagnostics and scaled teleconsultation usage.

●2034 outlook: >US$10.88B, >3.6× expansion from 2025 on platformization and hybrid-cloud rollouts.

●Growth velocity: Headline CAGR 15.47% (to 2034); operations/revenue models indicate 15.74% for 2025–2034.

●Revenue mix momentum (2024): Software 49.2% (leader), services fastest (15.5% CAGR), hardware follows via sensor/device refresh.

●Channel gravity: Cloud deployments 63.2% (2024); hybrid models showing the fastest CAGR 27.5% as data governance tightens.

●Solution skew (2024): Telemedicine & teleconsultation 38.6% of revenue; AI/ML solutions are the fastest riser (24.7% CAGR).

●Provider footprint: Hospitals & multi-specialty clinics 35.0% (2024); home healthcare shows the fastest scale-out (21% CAGR).

●Care setting penetration: Primary & outpatient capture 35.1% (2024); specialty lines are the high-growth wedge (19.8% CAGR).

●Regional profile (2024): North America 38.5% lead; APAC outpaces on growth via digital-health scale and policy push.

Market Trends

●Virtual-first front doors: Telemedicine/teleconsultation at 38.6% share (2024); audio/video + asynchronous consults normalize access.

●AI acceleration: AI/ML fastest growth (24.7% CAGR), improving triage, imaging reads, risk scoring, and workflow automation.

●Cloud predominance: 63.2% cloud share; zero-trust, API-first, and multi-tenant analytics unlock cross-site scale.

●Hybrid governance: 27.5% CAGR in hybrid deployments as providers balance PHI locality with cloud elasticity.

●Software center-of-gravity: 49.2% share; interoperability layers unify EHR, RPM, diagnostics, billing, and analytics.

●Service wrap expansion: 15.5% CAGR in consulting, integration, managed AI ops, training, and lifecycle support.

●Outpatient primacy: 35.1% share as clinics shift routine care to digital pathways, reducing wait-times and leakage.

●Home-based care surge: 21% CAGR in home providers, powered by RPM, wearables, and virtual case management.

●Policy tailwinds: U.S. telehealth waiver extensions through Sep 30, 2025; HRSA tech upgrades; Canada & EU grant programs.

●Global rollouts: Dubai’s airport Fakeeh Smart Clinic (Jul 2025); Colombia mobile smart clinic (Sep 2024); Guyana system-wide upgrade (Mar 2025).

10 Deep AI Roles & Impacts

●Autonomous triage & routing: AI symptom checkers prioritize acuity, route to right clinician, cut ED spillover.

●Imaging & diagnostics assist: AI boosts sensitivity/specificity in X-ray/ultrasound; faster reads, lower repeat scans.

●Predictive risk stratification: Early detection of decompensation; targeted outreach reduces readmissions.

●Personalized care plans: ML recommends care pathways, meds titration, and behavioral nudges based on longitudinal EHR + RPM.

●Virtual scribing & coding: Ambient AI reduces documentation time, improves coding accuracy, speeds claim cycles.

●Capacity & scheduling optimization: Forecast no-shows, load-balance provider rosters, minimize idle MRI/CT slots.

●Revenue cycle analytics: Fraud/anomaly detection and denial prediction improve net collections and DSO.

●Quality & safety surveillance: NLP flags gaps in care, drug–drug interactions, and guideline deviations in real time.

●Population health & equity lenses: Geospatial + SDOH models identify underserved cohorts for telehealth outreach.

●Device intelligence: Edge AI on wearables/IoT enables on-device event detection (AFib, hypoxia), lowering alert fatigue.

Regional Insights

North America (leader: 38.5% in 2024)

●Infrastructure maturity: Dense EHR footprint, interoperable APIs, payer acceptance accelerate smart clinic ROI.

●Policy tailwinds: Telehealth flexibilities through Sep 30, 2025; HRSA US$56M (2024) tech upgrades; CMS Rural Health funding (US$50B, 2025) supports access.

●Enterprise consolidation: Health systems scale cloud + hybrid stacks; strong cybersecurity and data-sharing frameworks.

Europe

●Funding scaffolding: EU RRF ~US$16.2B for digital health; EU4Health ~US$939M; Apply AI (~US$1.3B) catalyzes clinical AI.

●National enablers: DVG (Germany), NHS digital programs (U.K.) back EHR, RPM, and AI deployments.

●Focus: Interop, cybersecurity, and cross-border data services for pan-EU care coordination.

Asia Pacific (fastest growth)

●Scale drivers: Large underserved cohorts, mobile penetration, and cost-effective cloud lift adoption.

●Policy thrusts: India’s ABDM (national digital health IDs, telemedicine), startup funding momentum; China’s Internet-plus-Healthcare and EMR unification.

●Use-cases: Virtual primary care, specialist tele-consults, and community RPM hubs.

Latin America

●Access innovation: Colombia (Sep 2024) mobile smart clinic improves reach to rural communities.

●Digital focus: Telemedicine, e-pharmacy links, and AI triage to mitigate clinician shortages.

Middle East & Africa

●Hub projects: Fakeeh Smart Clinic (Dubai, Jul 2025) shows airport/free-zone on-prem + cloud orchestration.

●System transformation: Guyana (Mar 2025) multi-year upgrade bringing world-class access, with tech integration at scale.

Market Dynamics

Drivers:

●Telemedicine ubiquity (38.6% 2024 share), consumer demand for convenience.

●AI/ML momentum (24.7% CAGR), improving outcomes and throughput.

●Cloud dominance (63.2% 2024), enabling real-time multi-site data access.

●Policy & funding (U.S., Canada, EU; India ABDM) accelerating deployment.

Restraints:

●Data privacy/regulatory variance; need for hybrid architectures (fastest CAGR 27.5%) to localize sensitive data.

●Interoperability friction across legacy EHRs, devices, payers.

●Workforce readiness & change management (AI trust, training, scope of practice).

Opportunities:

●Home health expansion (21% CAGR segment) with RPM + virtual nursing.

●Services monetization (15.5% CAGR) via managed AI ops, integration, and analytics.

●Specialty smart lines (cardio/onc/ortho) with high acuity and ROI (19.8% CAGR).

Top 10 Companies

Teladoc Health

●Products: Enterprise telehealth; chronic care; mental health; data & analytics.

●Overview: Global virtual-first care leader integrating EHR and wearables.

●Strengths: Massive visit scale; cross-condition programs; payer/provider network depth.

Amwell

●Products: Virtual care platform; urgent/behavioral; care automation.

●Overview: Connects patients–providers via video/phone/chat with robust SDKs.

●Strengths: Health-system partnerships; white-label capabilities; workflow integration.

Philips Healthcare

●Products: Patient monitoring, imaging, tele-ICU, RPM platforms.

●Overview: Hospital-to-home continuum with interoperable device + software stack.

●Strengths: Clinical hardware + SaaS synergy; remote command centers; AI imaging.

Siemens Healthineers

●Products: Imaging, lab diagnostics, digital health, AI-Rad Companion.

●Overview: Precision medicine and clinical decision support at scale.

●Strengths: Deep imaging portfolio; AI workflow tools; enterprise integration.

GE Healthcare

●Products: Imaging, monitoring, command centers, Edison AI.

●Overview: Data-driven orchestration across radiology, cardiology, peri-op.

●Strengths: Operational AI (bed/OR throughput); broad install base; partner ecosystem.

Oracle (Cerner)

●Products: EHR/EMR, population health, RevCycle, cloud analytics.

●Overview: Core clinical systems with expanding cloud data platform.

●Strengths: EHR footprint; data fabric for apps/AI; payer-provider connectivity.

Medtronic

●Products: Cardiac & diabetes devices, RPM integrations, AI-enabled diagnostics.

●Overview: Device-led pathways plugged into clinic analytics and telehealth.

●Strengths: Evidence-rich devices; longitudinal RPM; procedural depth.

McKesson Corporation

●Products: Distribution, care management software, oncology network solutions.

●Overview: Supply + data capabilities supporting smart clinic logistics.

●Strengths: Scale in distribution; analytics for therapy access; specialty care reach.

Honeywell Life Care Solutions

●Products: Remote patient monitoring kits, device gateways, dashboards.

●Overview: Edge-to-cloud RPM for chronic and post-acute models.

●Strengths: Industrial-grade IoT; interoperability; security pedigree.

TytoCare

●Products: At-home exam kits (otoscope, stethoscope, camera) + telehealth.

●Overview: Clinic-quality remote exams integrated into virtual consults.

●Strengths: High patient usability; provider acceptance; improved diagnostic fidelity.

Latest Announcements & Recent Developments

Dubai (Jul 2025): Fakeeh Smart Clinic @ DAFZ

●AI-powered vitals capture (BP, temp, SpO₂) and smart devices.

●Integrated to Fakeeh University Hospital network for specialist access.

●Serves 23,000+ on-site employees — blueprint for workplace clinics.

Colombia (Sep 2024): Mobile Smart Clinic for Female Migrants

●12-meter coach with advanced equipment for gynecology, psychology, pediatrics.

●Operated with Siemens Healthineers and Red Cross; brings care to remote areas.

●Demonstrates tele-specialty + diagnostics convergence for humanitarian settings.

Guyana (Mar 2025): National Health System Transformation (5-year extension)

●With Mount Sinai & Hess — aiming world-class access by 2030.

●Focus: infrastructure, services quality, and technology integration.

●Sets a national model for smart, inclusive care.

U.S. Policy (2024–2025)

●Medicare telehealth waivers extended to Sep 30, 2025 (virtual breadth incl. audio-only).

●HRSA US$56M (2024) for tech/data modernization in high-need centers.

●CMS US$50B (2025) Rural Health Transformation under tax act enables smart access.

Canada (2024–2025)

●Infoway Connected Care Innovation grants (up to CAD US$40k each to 18 leaders).

●Saskatchewan US$10M fund for team-based clinics.

●Federal US$25M Digital Health Innovation Fund for AI/ML & big data in healthcare.

Europe (multi-year)

●US$16.2B RRF + ~US$939M EU4Health; smartCARE for cancer survivors.

●US$1.3B Apply AI to scale clinical AI in smart clinics/hospitals.

Segments Covered (in-depth with explanation)

Component:

●Hardware: Medical devices, IoT sensors/wearables, robotics, connectivity, servers—foundation for signal capture & bedside automation.

●Software (49.2% share): EHR/EMR, telehealth platforms, AI/analytics, patient ops, RPM—core orchestration and intelligence.

●Services (15.5% CAGR): Integration, upkeep, training, consulting—de-risk adoption and ensure uptime/ROI.

Technology/Solution:

●Telemedicine & Teleconsultation (38.6% 2024): Virtual front-door, asynchronous messaging, specialty access.

●Remote Patient Monitoring: Continuous vitals/behavior data for proactive interventions.

●AI & ML (fastest, 24.7% CAGR): Decision support, automation, personalization.

●IoT-enabled Devices: Edge telemetry into clinic analytics; asset tracking and safety.

●Robotics: Surgical assist/transport; precision, repeatability.

●Big Data & Analytics: Cohort insights, quality metrics, operational visibility.

●Cloud Health IT: Elastic compute/storage; API economy; rapid feature velocity.

End User:

●Hospitals & Multi-specialty (35%): Scale, capex, and IT governance; enterprise architectures.

●Primary/Outpatient Centers: Throughput & access wins; lower total cost of care.

●Diagnostic Centers: Imaging informatics + AI; turnaround speed.

●Home Healthcare (fastest, 21% CAGR): Decentralized care; RPM + virtual nursing.

●Telehealth Platforms: Network effects; payer integration; consumer UX.

Deployment Mode:

●Cloud (63.2% 2024): Multisite access, rapid rollout, centralized analytics.

●On-prem: Data residency, low-latency in OR/ICU, legacy adjacency.

●Hybrid (fastest, 27.5% CAGR): Sensitive data local; AI training/inference flexible in cloud.

●Region: North America (lead), Europe (funded expansion), APAC (fastest growth), Latin America & MEA (access-driven innovation).

Top 5 FAQs

1 How fast is the market growing?

●From US$2.57B (2024) to US$2.97B (2025) and >US$10.88B by 2034, implying ~15.47% CAGR overall (15.74% during 2025–2034).

2 Which components lead?

●Software holds 49.2% (2024); services grow fastest at 15.5% CAGR as clinics seek integration/managed AI.

3 Which solutions dominate?

●Telemedicine & teleconsultation 38.6% (2024); AI/ML solutions rise fastest at 24.7% CAGR.

4 Who leads regionally?

●North America 38.5% (2024); APAC is the fastest-growing on policy + mobile-first adoption.

5 What deployment is preferred?

●Cloud 63.2% (2024); hybrid grows fastest (27.5% CAGR) for security + flexibility.

Latest & Notable Companies (quick snapshot)

●Cleveland Clinic, Mayo Clinic, Johns Hopkins Hospital are exemplars of smart hospital practices with AI, robotics, telemedicine embedded in care pathways (2025 recognition and ongoing deployment).

Access our exclusive, data-rich dashboard dedicated to the healthcare industry – built specifically for decision-makers, strategists, and industry leaders. The dashboard features comprehensive statistical data, segment-wise market breakdowns, regional performance shares, detailed company profiles, annual updates, and much more. From market sizing to competitive intelligence, this powerful tool is one-stop solution to your gateway.

Access the Dashboard: https://www.towardshealthcare.com/access-dashboard

Immediate Delivery Available | Checkout this Premium Research Report @ https://www.towardshealthcare.com/checkout/6333

Become a valued research partner with us – https://www.towardshealthcare.com/schedule-meeting

You can place an order or ask any questions, please feel free to contact us at sales@towardshealthcare.com

Powering Healthcare Leaders with Real-Time Insights: https://www.towardshealthcare.com/healthcare-intelligence-platform

Europe Region – +44 778 256 0738

North America Region – +1 8044 4193 44

APAC Region: +91 9356 9282 04

Web: https://www.towardshealthcare.com

Find us on social platforms: LinkedIn | Twitter | Instagram | Medium | Pinterest