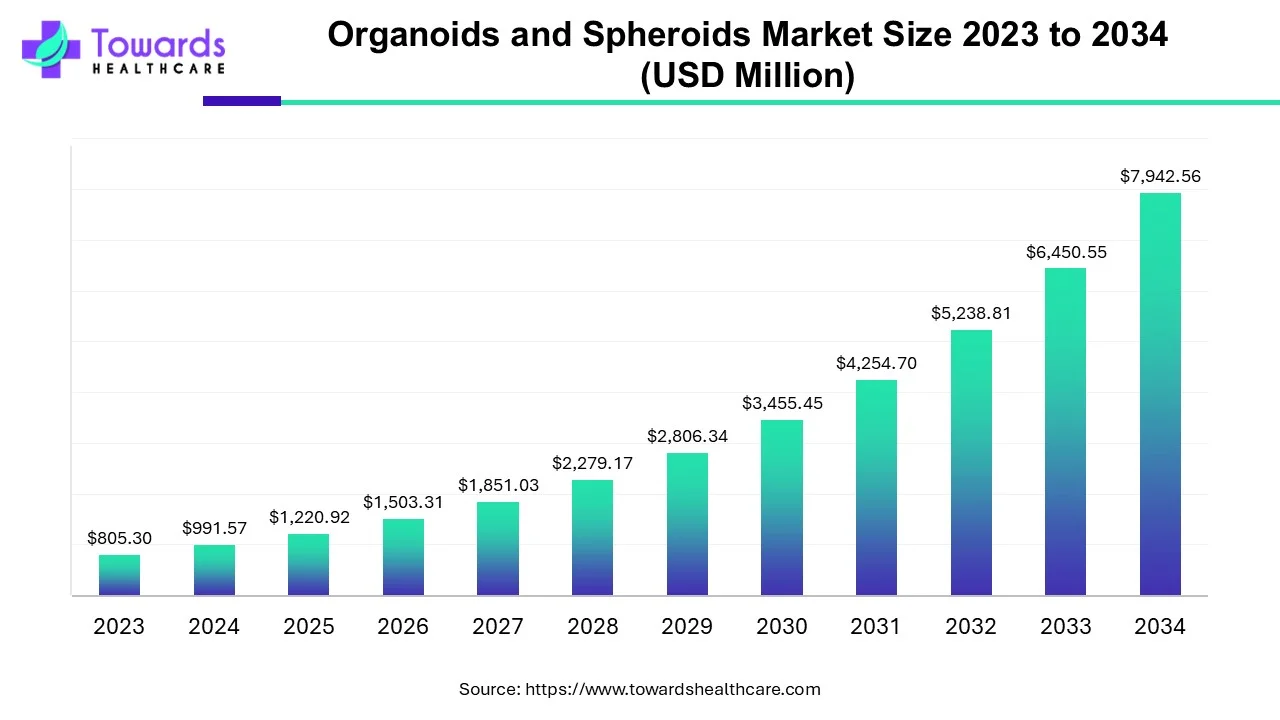

The organoids & spheroids market is projected to grow from USD 1,220.92 million in 2025 to USD 7,942.56 million by 2034 (CAGR 23.13%), driven by rising cancer research, regenerative medicine demand, AI/3D-model advances and commercial productisation.

Download Sample: https://www.towardshealthcare.com/download-sample/5167

Market size

Base and forecast figures

2025 market size: USD 1,220.92M.

2034 market size: USD 7,942.56M.

Implied absolute expansion (2025→2034): USD 6,721.64M.

Compound Annual Growth Rate (CAGR)

23.13% CAGR (2025–2034) — indicates rapid scale-up, adoption and commercialization across R&D, pharma/biotech and translational pipelines.

Revenue concentration (2023 snapshot)

North America held 43% revenue share in 2023 (largest regional share).

Spheroids generated >54% of revenue by type in 2023 (largest single-type share).

Developmental biology had 31% share by application in 2023 (largest application slice).

Growth drivers embedded in size forecast

High unmet needs in oncology and regenerative medicine, increasing replacement of animal models, and investment into high-throughput, AI-enabled organoid platforms underpin the steep CAGR.

Segment-level capacity to capture value

Although spheroids dominated 2023 revenue, organoids are forecasted to grow faster (higher relative growth rate than spheroids) — indicating shifting R&D spend toward more complex, organ-specific 3D models.

Market trends

Shift from 2D to complex 3D models — adoption of spheroids and organoids over monolayer cultures for translational relevance.

Patient-derived models for personalized medicine — organoids used for ex-vivo testing, gene repair and transplant-oriented research.

Integration of microfluidics / organ-on-chip — to reduce necrosis and improve nutrient/oxygen perfusion in larger constructs.

Commercialisation and platformisation — companies offering standardized, scalable organoid platforms (e.g., cardiac, tumor) and licensing agreements.

Robotics and high-throughput automation — Clinical Trial in a Dish and similar scaled workflows for screening multiple candidates.

Space-based experimentation — novel environments (ISS payloads) used to probe organoid behavior under microgravity as proof-of-concept R&D.

3D bioprinting adoption — attempts to solve inner-layer necrosis by spatially arranging vasculature and signaling gradients.

Cross-disciplinary partnerships — tissue engineering, AI, microelectronics and biosensing groups forming startups and spinouts.

Regulatory & ethical focus — pressure to reduce animal testing (NC3Rs activity, lymphoid organoid hubs) and to standardize organoid validation.

Geographic decentralisation of R&D — Asia-Pacific catching up rapidly (China, India, Japan) with academic & industrial investments and indigenous innovations.

10 ways AI impacts / will shape this market

Automated image analysis & phenotyping at scale

AI models analyze high-content microscopy of organoids/spheroids to quantify morphology, growth, necrosis zones, and drug response curves at massively higher throughput than manual scoring.

Benefit: consistent, objective phenotype metrics that improve reproducibility across labs.

Predictive modelling of drug response (in silico → ex vivo loop)

Machine learning models integrate organoid assay outputs with molecular profiles to predict which compounds will translate to clinical response; closes the loop between assay and candidate prioritization.

Benefit: reduces costly false positives in preclinical pipelines.

Optimization of culture protocols

Reinforcement learning and Bayesian optimization tune multi-parameter culture conditions (matrix composition, oxygenation, media feeds, growth factors) to maximize viability and desired differentiation.

Benefit: faster, reproducible protocol development tailored per tissue type.

Spatial transcriptomics & multi-omics interpretation

AI fuses spatial gene expression, proteomics and imaging to map heterogeneity inside organoids — distinguishing viable vs necrotic cores and identifying microenvironmental niches.

Benefit: mechanistic insights for improving organoid design and target identification.

Automated quality control & standardization

Computer vision detects batch effects, contamination, morphological drift and flags failing batches before downstream assays.

Benefit: industrial-grade QC enabling commercialization and regulatory readiness.

Design of microfluidic perfusion systems

AI-assisted fluid dynamics modelling helps design organ-on-chip perfusion patterns to minimize inner necrosis and optimize nutrient gradients.

Benefit: improved long-term viability for larger constructs.

Synthetic biology + AI for engineered organoids

Generative models propose gene circuits or biomaterial compositions to drive desired differentiation trajectories or reporter readouts in organoids.

Benefit: accelerates creation of bespoke disease models.

Virtual clinical trial simulations using organoid data

Aggregate organoid responses from diverse patient-derived samples feed population-level models predicting efficacy and safety distributions.

Benefit: de-risk clinical trial design and patient stratification.

AI-enabled translational matching (drug ↔ patient organoid)

Recommendation systems match investigational drugs to patient-derived organoids most likely to respond based on multi-modal features (genomics, phenotype).

Benefit: speeds precision medicine decisions and companion diagnostic development.

Operational scaling: scheduling, robotics orchestration, and cost optimisation

AI schedules automated robotics, instrument time and reagent usage across multi-site facilities to maximize throughput and minimize cost per assay.

Benefit: makes high-throughput organoid services commercially viable (e.g., “Clinical Trial in a Dish”).

Regional insights

North America (dominant; 43% revenue share in 2023)

Innovation & investment hub

Strong R&D base, high healthcare spend (content notes: U.S. spends $3.8T), and concentration of biotech/pharma buyers.

Commercial ecosystems

Presence of major companies, venture financing, spinouts (e.g., Terasaki Institute startups) accelerates product launches and platform adoption.

Regulatory & telehealth enablers

Growing policy support for translational research and telehealth increases patient sample access and decentralized trials.

Europe (growing, considerable rate)

Policy & funding support

Government & nonprofit funding (e.g., NC3Rs funding for lymphoid organoid hubs) encourages replacement of animal models.

Collaborative conferences & training

Dedicated scientific meetings (e.g., European Organoids & Spheroids Conference 2025) build community and standards.

Asia-Pacific (fastest projected growth)

Rapid research adoption

China, India, Japan pushing organoid research (example: Chinese Medical Journal cancer stats for China 2024; brain-on-chip development from Tianjin University/SUSTech).

Large patient populations & diverse sample pools

Enables biobanking of diverse patient-derived organoids for population-relevant studies.

Cost-competitive manufacturing & scale

Lower costs for reagent production and growing domestic platforms could accelerate commercial scale-up.

Latin America, Middle East & Africa

Emerging markets with targeted pockets of capability

Growth will depend on local investment, collaborations and ability to access global platforms.

Opportunity in neglected disease modelling

Organoids can enable region-specific disease models when resources permit.

Market dynamics

Demand drivers

Rising cancer incidence and need for better translational models (IARC-based 2022: ~20M new cases, 9.7M deaths) drives adoption of tumor spheroids/organoids.

Personalized medicine push (patient-derived organoids) fuels both service and product markets.

Supply / technology push

Advances in 3D culture, microfluidics, 3D bioprinting and AI accelerate product readiness and create multiple commercial offerings (platforms, kits, services).

Value chain evolution

From academic protocol → standardized kits/reagents → automated platforms → contract testing services → therapeutic-decision support (Clinical Trial in a Dish).

Barriers & technical constraints

Necrosis in inner layers (avascular constructs) limits organoid size and maturity; microfluidics/bioprinting are partial mitigations.

Standardization & inter-lab reproducibility remain challenges for regulatory acceptance.

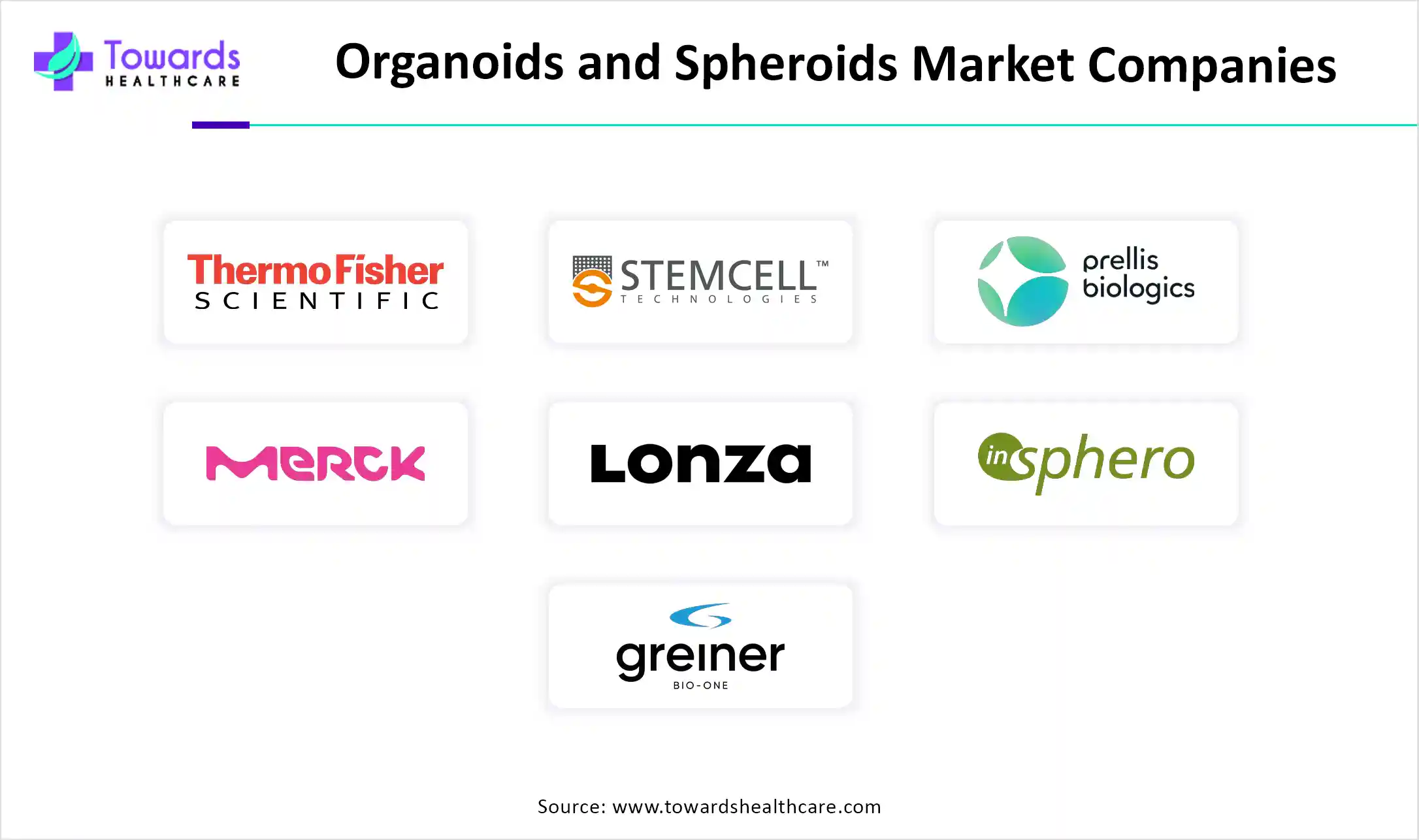

Competitive structure

Mix of large life-science suppliers (Thermo Fisher, Merck, Corning), specialist organoid firms (HUB, InSphero, Prellis) and nimble startups (Digital Immunology spinouts, FinalSpark) — competition across product, platform and service verticals.

Regulatory & ethical influences

Initiatives to reduce animal use (NC3Rs funding, organoid hubs) both create market pull and demand for validated, standardized organoid solutions.

Customer segments & purchasing behaviour

Pharma/biotech for lead selection and translational research; academic labs for method development; contract research organisations (CROs) and hospitals for precision medicine services.

Price / commercialization dynamics

High initial cost for platform adoption but potential to reduce downstream R&D costs by better preclinical predictivity; economies of scale expected as automation matures.

Partnerships & licensing

Strategic commercialisation partnerships (example: InSphero + Genome Biologics cardiac organoid platform) accelerate market reach and expand product portfolios.

Future trajectory

Short-term: platform & service proliferation, validation studies.

Mid-term: AI + organoid ecosystems enable “clinical trial in a dish” workflows.

Long-term: integration into clinical decision making and regenerative therapies (organoid transplantation, organogenesis).

Top 10 companies

Thermo Fisher Scientific, Inc.

Product/Offering: Broad life-science consumables, instrumentation and reagents used in organoid workflows.

Overview: Global leader supplying components for culture, imaging and analytics.

Strength: Scale, distribution, validated reagents and trusted brand across pharma and academia.

STEMCELL Technologies Inc.

Product/Offering: Specialized stem cell media, matrices and kits for organoid and stem-cell based culture.

Overview: Niche leader in reagents needed for organoid differentiation and maintenance.

Strength: Deep product expertise for stem-cell niche support and researcher adoption.

Prellis Biologics

Product/Offering: Advanced 3D bioprinting / vascularization tech (implied by firm type).

Overview: Focus on printing approaches to address vascularization/necrosis limitations.

Strength: Technology aimed at improving physiological relevance and size of constructs.

Merck KGaA

Product/Offering: Life-science reagents, chip/organoid R&D collaborations.

Overview: Large life-science player with R&D investment; exploring organoid-on-chip next-gen products (annual report note).

Strength: R&D budgets and cross-domain resources (life sciences + healthcare + electronics collaboration).

Lonza

Product/Offering: Contract development & manufacturing, cell culture systems and services.

Overview: Well positioned to provide GMP capability and scale for cellular products.

Strength: Manufacturing expertise, regulatory know-how and CRO/CDMO relationships.

InSphero

Product/Offering: Scalable organoid models and commercialization agreements (e.g., 3D Cardiac Organoid Platform via Genome Biologics).

Overview: Specialist in disease-specific organoids and commercial service offerings.

Strength: Focus on disease-specific, scalable organoid platforms and strategic licensing.

Hubrecht Organoid Technology (HUB)

Product/Offering: Organoid tech originating from academic organoid innovators; likely biobanking and protocol licensing.

Overview: Academic spinouts to translate organoid methods into reproducible products.

Strength: Intellectual capital in organoid biology and patient-derived models.

Greiner Bio-One

Product/Offering: Labware, culture plates and consumables for 3D culture (e.g., low attachment plates).

Overview: Essential hardware supplier for spheroid formation and standardized methods.

Strength: Manufacturing of standardized disposables enabling reproducible workflows.

Corning Incorporated

Product/Offering: Specialty cultureware and matrices for 3D culture and organoids.

Overview: Well-established supplier of technical plates and matrices used in spheroid/organoid formation.

Strength: Product reliability and integration into many lab workflows.

Cellesce Ltd. (and other specialist firms: AMS Biotechnology, 3D Biotek, 3D Biomatrix)

Product/Offering: Scale-up platforms, scaffold matrices and service offerings for organoid manufacturing.

Overview: Companies focused on scaling organoid production and customized matrices.

Strength: Niche technical capabilities for commercialization and scaling.

Latest announcements

Space & organoid experiments (May 2024 / March 2024 notes)

What happened: Universities and nonprofits (UC San Diego; National Stem Cell Foundation; other California teams) sent tumor or brain organoids to the International Space Station to study behavior under microgravity. NASA and academic partners invested in these missions.

Implications: These projects validate organoids as robust research platforms in extreme environments, expand fundamental biology knowledge and raise the profile of organoid technologies internationally.

Terasaki Institute spinouts (March 2024)

What happened: TIBI announced four startup firms leveraging institute research in organoids, microneedles, biomaterials and biosensing (Digital Immunology named).

Implications: Signals institutional translation from bench to startup, cross-disciplinary commercialization and new product pathways combining organoids with AI and biosensing.

FinalSpark platform (May 2024)

What happened: FinalSpark released an internet platform giving 24/7 access to 16 human brain organoids for remote experimentation, aimed at building living processors.

Implications: New business model: remotely accessible living organoid resources, democratizing access to specialized organoid assays and opening novel compute/biocomputing research avenues.

Parallel Bio — Clinical Trial in a Dish (May 2024)

What happened: Parallel Bio launched a service using human immune-system models and immunological organoids scaled with robotics to test 20 candidates for five pharma partners.

Implications: Demonstrates commercial viability of organoid services for early safety/efficacy screening and adoption by pharma (including large companies).

InSphero commercialization deal (May 2024)

What happened: InSphero licensed Genome Biologics’ 3D Cardiac Organoid Platform for worldwide commercialization.

Implications: Rapid productization of disease-specific organoid platforms; strategic licensing accelerates market penetration for organ-specific assays.

Merck KGaA R&D (annual report June 2024)

What happened: Merck highlights next-gen organoids on chip being investigated — cross-disciplinary collaboration.

Implications: Big life-science firms are investing in hybrid solutions (chip + organoid) — important for regulatory validation and scalable products.

NC3Rs funding to Oxford (Jan 2025)

What happened: Funding for lymphoid organoid and explant hub at University of Oxford.

Implications: Institutional support for replacing animal models, creating validated organoid hubs for immunology research.

Segments covered

By Type

Organoids — subtypes: neural, hepatic, intestinal, other organoid types.

Explanation: Organoids mimic organ architecture and are central to personalized medicine and transplantation research. Faster growth rate expected.

Spheroids — subtypes: multicellular tumor spheroids (MCTS), neurospheres, mammospheres, hepatospheres, embryoid bodies.

Explanation: Spheroids are simpler cell clusters widely used for tumor biology and initial drug screens; they held >54% revenue in 2023.

By Method

Organoid culture methods: submerged, crypt organoid culture, air-liquid interface (ALI), Lgr5+ clonal organoids, brain & retina protocols.

Explanation: Method choice affects tissue maturation, cell polarity and experimental readouts.

Spheroid formation methods: micropatterned plates, low cell attachment, hanging drop, others.

Explanation: Each method balances throughput, uniformity, and suitability for downstream assays (imaging, HTS).

By Source

Primary tissues — patient biopsy derived.

Explanation: Best for patient-specific models, highest translational relevance, but variable and resource-intensive.

Stem cells / iPSC-derived — pluripotent stem cell derived organoids.

Explanation: Provide reproducible, scalable sources for organoid panels and disease modelling.

Cell lines — easier to scale but lower physiological fidelity.

By Application (listed for context only; user requested not to use by application mainly, but included for clarity)

Developmental biology, personalized medicine, regenerative medicine, disease pathology, drug toxicity & efficacy testing.

Explanation: These are the core use cases driving value capture and funding.

By Region

North America, Europe, Asia Pacific, Latin America, MEA — each with unique drivers (innovation hubs, funding, manufacturing, population diversity).

Top 5 FAQs

-

Q: What is the market size and growth rate for organoids & spheroids?

A: The market is forecast to grow from USD 1,220.92M in 2025 to USD 7,942.56M by 2034, a 23.13% CAGR (2025–2034). -

Q: Which region led the market in 2023?

A: North America led with 43% revenue share in 2023, driven by concentrated R&D investment, healthcare spend and commercialization activity. -

Q: Which product type currently generates the largest revenue?

A: Spheroids generated >54% of revenue in 2023; however organoids are expected to be the faster-growing type going forward. -

Q: What is the main technical limitation slowing organoid/spheroid maturity?

A: Necrosis in inner layers due to avascularity and limited nutrient/oxygen diffusion in larger constructs; mitigations include microfluidics, organ-on-chip and 3D bioprinting approaches. -

Q: How is AI affecting organoid research and commercialization?

A: AI accelerates image analysis, protocol optimisation, QC, multi-omics integration, predictive drug response modelling and orchestration of automated, high-throughput organoid platforms — enabling scalable and more predictive preclinical workflows.

Access our exclusive, data-rich dashboard dedicated to the diagnostics sector – built specifically for decision-makers, strategists, and industry leaders. The dashboard features comprehensive statistical data, segment-wise market breakdowns, regional performance shares, detailed company profiles, annual updates, and much more. From market sizing to competitive intelligence, this powerful tool is one-stop solution to your gateway.

Access the Dashboard: https://www.towardshealthcare.com/access-dashboard

Checkout Organoids and Spheroids Market Report Now at: https://www.towardshealthcare.com/checkout/5167

Become a valued research partner with us – https://www.towardshealthcare.com/schedule-meeting

You can place an order or ask any questions, please feel free to contact us at sales@towardshealthcare.com

Powering Healthcare Leaders with Real-Time Insights: https://www.towardshealthcare.com/healthcare-intelligence-platform

Europe Region – +44 778 256 0738

North America Region – +1 8044 4193 44

APAC Region: +91 9356 9282 04

Visit Our Website: https://www.towardshealthcare.com

Find us on social platforms: LinkedIn | Twitter | Instagram | Medium | Pinterest