The global Antibody Drug Conjugate (ADC) market is rapidly expanding, projected to grow from USD 13.51 billion in 2025 to USD 29.9 billion by 2034, at a CAGR of 9.23%, driven by advancements in targeted cancer therapies, AI integration, and innovative ADC research.

Download this Free Sample Now and Get the Complete Report and Insights of this Market Easily @ https://www.towardshealthcare.com/download-sample/5178

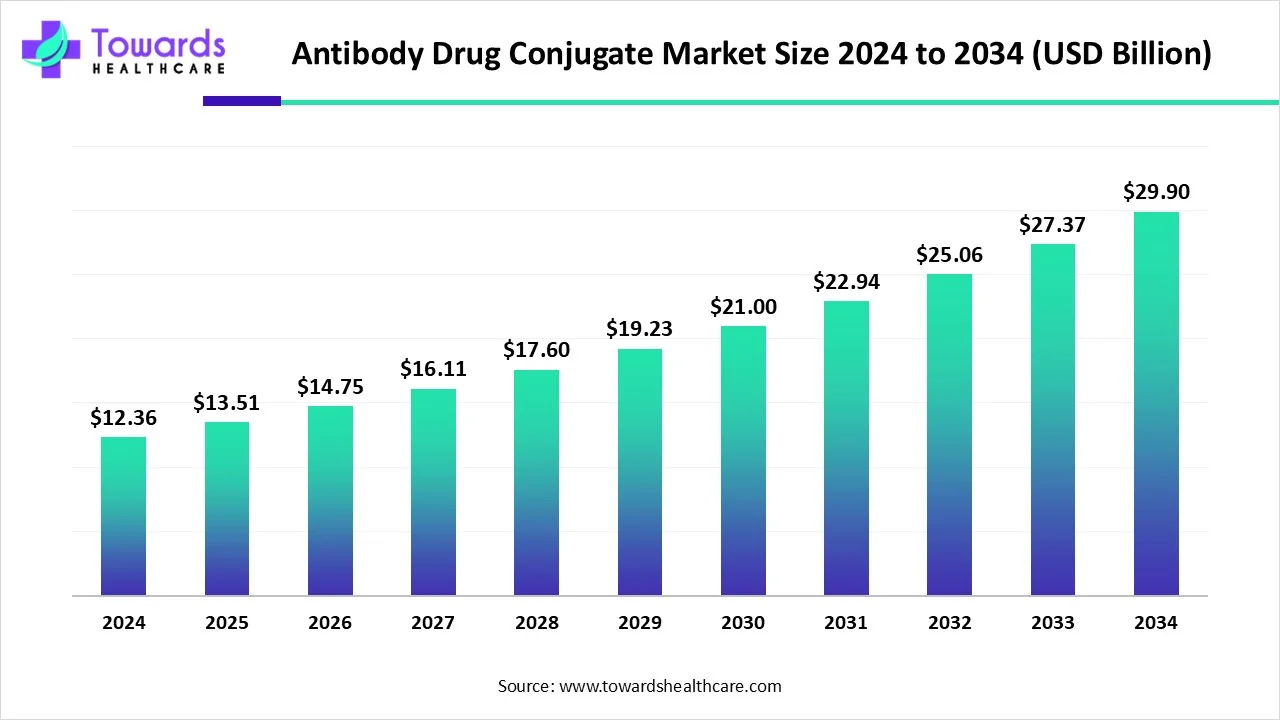

Market Size

Global Market Growth:

●2024: USD 12.36 Billion

●2025: USD 13.51 Billion

●2034 Projection: USD 29.9 Billion

●CAGR (2025-2034): 9.23%

Leading Region:

●North America dominated the market in 2023 with 53% revenue share, driven by FDA approvals, well-funded biotech startups, and high cancer incidence.

Key Market Metrics:

●Segmentations: Product, Target, Technology, Region

●Top Products: Kadcyla, Enhertu, Adcetris, Padcev, Trodelvy, Polivy

●Top Targets: HER2, CD22, CD30

●Technologies: Cleavable linkers dominate with 73% revenue share in 2023.

Market Trends in Antibody Drug Conjugate (ADC) Market

Targeted Cancer Therapy Growth:

●ADCs combine monoclonal antibodies with cytotoxic drugs, allowing highly precise tumor targeting with minimal healthy tissue damage.

R&D Expansion:

●Continuous advancements in antibody design, linker chemistry, and cytotoxic payloads are accelerating ADC innovation.

Breast Cancer Dominance:

●Breast cancer ADCs (like Kadcyla) generated the largest revenue share (49%) in 2023 due to high prevalence (2.3 million women diagnosed globally in 2022).

Emerging Blood Cancer Segment:

●Blood cancer ADCs expected to grow fastest due to easier access to target cells and higher success rates in hematological malignancies.

Product Innovation:

●Enhertu expected to grow fastest (2024–2033) targeting HER2-positive breast and non-small cell lung cancer.

Technological Adoption:

●Cleavable linkers dominate; over 80% of approved ADCs use linkers that release cytotoxins selectively in tumors.

Regulatory Support:

●FDA approvals and accelerated review pathways in North America are driving faster adoption of new ADCs.

Personalized Medicine Opportunity:

●ADCs tailored to individual tumor antigens can replace chemotherapy, enabling “smart chemotherapy” and highly personalized treatment plans.

AI-Driven Discovery:

●Integration of AI into research and development accelerates drug discovery, patient stratification, and manufacturing efficiency.

Global Expansion:

●Emerging regions like Asia Pacific, India, and China show growing adoption due to rising disease incidence, government support, and healthcare investment.

AI Impact on ADC Market

Accelerated Drug Discovery:

●AI analyzes large datasets to identify promising antibody-drug combinations, reducing trial-and-error time.

Precision ADC Design:

●Predicts molecular interactions between antibodies, linkers, and cytotoxins to enhance efficacy and minimize side effects.

Patient Stratification:

●AI predicts patient response to specific ADCs, enabling personalized treatment plans.

Clinical Trial Optimization:

●AI-driven analytics help identify suitable patient cohorts and anticipate adverse reactions.

Manufacturing Efficiency:

●Real-time AI monitoring ensures consistent ADC quality and identifies production issues early.

Literature & Data Mining:

●AI processes biomedical literature to uncover novel targets, linkers, and payload insights.

Toxicity Prediction:

●Predicts potential side effects before clinical trials, lowering the risk of therapy discontinuation.

Cost Reduction:

●Optimizes R&D, clinical trials, and manufacturing, reducing time-to-market and overall costs.

Regulatory Compliance:

●AI models anticipate regulatory requirements and streamline approval submissions.

Future Research Guidance:

●AI identifies emerging ADC trends and innovative therapeutic combinations for continuous market growth.

Regional Insights

North America – Market Leader

●Market Share: Dominated the ADC market with 53% share in 2023.

Key Drivers:

High Cancer Incidence:

●Estimated 2,001,140 new cancer cases in the U.S. in 2024 and 611,720 deaths.

●Increasing prevalence of breast, blood, and lung cancers drives demand for targeted therapies like ADCs.

Regulatory Support (FDA):

●Rapid approvals of ADCs such as Kadcyla and Trodelvy encourage adoption.

●FDA’s review process and clinical trial support reduce time-to-market for novel ADC therapies.

Strong Biotech Ecosystem:

●Presence of numerous startups and established firms specializing in ADCs, like Seagen, Pfizer, and AbbVie.

●Investment in R&D for innovative linkers, payloads, and antibodies.

Healthcare Expenditure:

●High healthcare spend facilitates access to cutting-edge therapies. U.S. national cancer care spend in 2020 was $208.9 billion; expected to increase with rising cases.

Trend Insights:

●Focus on Personalized Medicine: Increasing use of HER2-targeting ADCs (Kadcyla, Enhertu) for tailored treatments.

●Clinical Trials Hub: North America hosts numerous Phase 1–3 trials for novel ADCs, particularly in hematologic malignancies and solid tumors.

Asia Pacific – Fastest Growing Market

Growth Dynamics:

●Rapid adoption of ADC therapies due to rising disease prevalence, healthcare infrastructure development, and government initiatives.

●Growth accelerated by technological integration, including advanced linker-payload combinations and molecular biology techniques.

Key Countries Driving Growth:

China:

●Large population → higher disease burden → greater demand for ADC therapies.

●Strong government support for oncology innovation, clinical trials, and domestic ADC manufacturing.

●Increasing industry-academic collaborations to develop next-gen ADCs targeting HER2, Nectin-4, and TROP2.

India:

●Rising cancer incidence and growing healthcare industry increase demand for effective treatments.

●Adoption of new ADC technologies for faster, higher-quality production.

●Government-led affordability programs improving patient access to ADCs.

Japan:

●Advanced biotech and pharmaceutical research capabilities.

●High adoption rate of novel ADCs for breast and blood cancers.

Singapore:

●AstraZeneca’s $1.5B ADC plant highlights the country as a production and innovation hub in Asia.

Market Drivers:

●Growing middle-class population with access to advanced healthcare.

●Rising prevalence of HER2-positive breast cancer and hematologic malignancies.

●Increased clinical trials and ADC pipeline expansion by global companies in the region.

Trend Insights:

●Government initiatives supporting research and development for ADCs.

●Regional collaborations between pharma companies and academic institutes accelerate innovation.

●Emerging personalized therapy adoption, particularly for breast cancer and blood cancers.

China – Regional Spotlight

●Population Factor: Largest population in APAC → high incidence of cancer cases.

Industry Growth:

●Collaborations between pharma companies and research institutes enhance ADC development.

●Investment in advanced technologies, e.g., cleavable linkers and novel payloads.

●Government Support: Policies to promote innovative cancer treatments and facilitate regulatory approvals.

India – Regional Spotlight

●Healthcare Development: Expansion of hospitals, oncology centers, and cancer research facilities.

●Technological Adoption: Companies adopting faster, quality-focused ADC production technologies.

●Patient Accessibility: Government schemes and subsidy programs make ADC therapies more affordable, increasing uptake.

Market Dynamics

1. Market Drivers – Factors Fueling Growth

Rising Cancer Incidence

●Globally increasing rates of breast, blood, lung, and pancreatic cancers drive the demand for targeted therapies.

Example: North America recorded 2,001,140 new cancer cases in 2024, emphasizing the urgent need for effective ADC therapies.

Impact: Higher patient populations and unmet medical needs accelerate ADC adoption.

Advanced ADC Research & Development

●Innovations in antibody engineering, linker chemistry, and cytotoxic payloads improve therapeutic efficacy and reduce off-target effects.

Example: Site-specific antibody conjugation and genetically engineered antibodies enhance safety and performance.

Impact: Expands pipeline of novel ADCs for both solid tumors and hematologic malignancies.

AI Integration

●Artificial Intelligence accelerates discovery by predicting optimal antibody-drug combinations and simulating molecular interactions.

●Clinical Advantage: AI-driven analytics forecast patient responses, enabling personalized treatment plans.

●Manufacturing Advantage: Real-time monitoring and predictive analytics ensure consistent product quality, reducing errors and wastage.

Regulatory Support

●FDA approvals and expedited review processes in regions like North America streamline ADC market entry.

●Impact: Encourages investment from pharmaceutical companies and shortens time-to-market for innovative ADCs.

2. Market Restraints – Factors Limiting Growth

Severe Toxicity and Adverse Events

●Many ADCs exhibit high systemic toxicity, leading to dose reductions, treatment delays, or therapy withdrawal.

●Example: Even clinically approved ADCs may cause unacceptable side effects in a significant portion of patients.

●Impact: Limits patient adoption and can slow regulatory approvals.

High Clinical Development Failure Rate

●Approximately 12 ADC compounds are in clinical use, but many fail during development due to negative risk-benefit profiles.

●Impact: Increases investment risk for pharmaceutical companies and slows pipeline expansion.

3. Market Opportunities – Areas for Growth

Personalized ADC Therapies

●Future ADCs may be tailored based on a patient’s tumor antigens and molecular profile.

●Impact: “Smart chemotherapy” could replace traditional chemotherapy, providing highly targeted treatment with fewer side effects.

Expansion in Emerging Markets

●Rapid growth expected in Asia Pacific, including China, India, and Singapore, due to rising disease prevalence and government healthcare initiatives.

●Impact: Increased patient access and new revenue streams for ADC developers.

Novel ADC Payloads and Targets

●Development of payloads like topoisomerase inhibitors (Camptothecin) and new targets such as CD22, Nectin-4, TROP2.

●Impact: Expands therapeutic potential for previously difficult-to-treat cancers.

4. Market Challenges – Barriers to Adoption

Costly R&D and Manufacturing

●ADC development involves high costs due to advanced technologies, biologics production, and clinical trials.

●Impact: Limits entry of smaller players and increases therapy pricing for patients.

Complex Regulatory Approvals

●Each ADC must pass rigorous preclinical and clinical trials for safety and efficacy.

●Impact: Long timelines and variable global regulations slow commercialization.

Managing Side Effects

●Even approved ADCs require careful monitoring for toxicity, which can complicate clinical adoption.

●Impact: Demands additional healthcare infrastructure and expertise, potentially restricting market growth in emerging regions.

Top Companies & Strengths

ADC Therapeutics SA

Product Focus: Oncology-focused ADCs.

Overview: Specializes in developing ADCs for various cancer types, leveraging proprietary linkers and payload technologies.

Strength: Strong expertise in precision oncology, robust R&D pipeline, and innovative linker-payload combinations.

AbbVie (Illinois, U.S.)

Product Focus: ADCs targeting SEZ6 and c-Met.

Overview: AbbVie’s ADCs focus on novel protein biomarkers overexpressed in tumors. Delivered via powerful cytotoxic payloads for targeted therapy.

Strength: Strong clinical trial program; expertise in personalized ADC therapies; global research collaborations.

Astellas Pharma, Inc.

Product Focus: Innovative ADCs for multiple cancers.

Overview: Develops ADCs with global regulatory approvals; pipeline includes therapies for solid tumors and hematologic malignancies.

Strength: Regulatory compliance, innovation in antibody design, strong international presence.

GlaxoSmithKline Plc (GSK)

Product Focus: Advanced ADCs with novel antibody technologies and linkers.

Overview: Focuses on optimizing antibody-linker-drug combinations to improve efficacy and safety.

Strength: Expertise in linker chemistry, robust biologics manufacturing capabilities.

Daiichi Sankyo

Product Focus: ADCs for pancreatic, breast, and other cancers.

Overview: Develops targeted ADCs like Enhertu (trastuzumab deruxtecan) with strong clinical data.

Strength: Strong R&D collaborations, global licensing agreements, and expanding clinical pipeline.

Gilead Sciences, Inc.

Product Focus: Trodelvy (ADC for breast and lung cancer).

Overview: Invests heavily in clinical trials, focusing on high-unmet-need cancers.

Strength: Strong financial backing for ADC trials, strategic partnerships, and commercialization expertise.

Pfizer, Inc.

Product Focus: Broad ADC portfolio; acquired Seagen for ADC expertise.

Overview: Plans to develop 8 blockbuster cancer therapies by 2030; integrates Seagen’s ADC technologies.

Strength: Global reach, manufacturing capabilities, and large-scale clinical development infrastructure.

F. Hoffmann-La Roche Ltd. (Roche)

Product Focus: HER2-targeting ADCs (Kadcyla, others).

Overview: Pioneered HER2-directed ADC therapies for breast cancer; global regulatory approvals.

Strength: Strong oncology R&D, proven clinical efficacy, and global market leadership.

AstraZeneca

Product Focus: ADCs for solid tumors; developing large-scale manufacturing.

Overview: Building a $1.5B Singapore ADC plant for end-to-end production.

Strength: Complete vertical integration from R&D to commercial production, strategic investments in global manufacturing.

Seagen, Inc.

Product Focus: Innovative ADCs, FDA-approved therapies.

Overview: Focused entirely on ADC development; acquired by Pfizer for enhanced collaboration.

Strength: Industry leader in ADC innovation, strong FDA approvals, and robust intellectual property portfolio.

Latest Announcements

AbbVie: Presented ADCs targeting SEZ6 & c-Met at ASCO 2024.

AstraZeneca: Announced $1.5B ADC production plant in Singapore, 2024.

Adcytherix SAS: €30M seed capital to develop ADCs for unmet medical needs, 2024.

Daiichi Sankyo Singapore: Expanding ADC access for oncology patients, 2024.

Pfizer: Cancer strategy update post Seagen acquisition, targeting 8 blockbuster ADCs by 2030.

Recent Developments

IPH4502 ADC by Innate Pharma SA – Targets Nectin-4; preclinical data presented at AACR 2025.

Heidelberg Pharma AG ADC for PDAC – Targets TROP2; shows promising efficacy.

Seagen & Kadcyla Clinical Trial – HER2CLIMB-02; progression-free survival endpoint.

Trastuzumab Deruxtecan (Enhertu) – FDA approved for HER2-positive NSCLC and breast cancer.

Galen Breast HER2 AI Tool – Enhances HER2 scoring for personalized therapy.

Segments Covered

By Product

Kadcyla

Market Position: Holds the largest market share in the ADC market (2023).

Targeted Cancer: Specifically targets HER2-positive breast cancer, delivering cytotoxic drugs directly to HER2-expressing cells.

Clinical Impact: Reduces harm to healthy tissue compared to conventional chemotherapy.

Global Reach: Approved in over 100 countries, including the U.S. and EU.

Efficacy Data: Recurrence rates are significantly lower—~13% with Kadcyla vs. 23% in standard treatment.

Recent Trials: HER2CLIMB-02 by Seagen showed progression-free survival improvement when combined with TUKYSA, even in patients with brain metastases.

Enhertu (Trastuzumab Deruxtecan)

Growth Rate: Fastest CAGR in the market (2024–2033).

Indications: HER2-positive breast cancer, HER2-low breast cancer, and non-small cell lung cancer (NSCLC).

FDA Approval: Approved for metastatic/unresectable HER2-positive cases after prior anti-HER2 treatment.

Mechanism: Precisely targets HER2 receptors, delivering a potent cytotoxic payload, allowing “smart chemotherapy.”

Market Trend: Rising adoption due to expanding indications and clinical efficacy.

Adcetris (Brentuximab Vedotin)

Use Case: Primarily for CD30-positive hematologic malignancies like Hodgkin lymphoma.

Technology: Employs a cleavable linker for targeted drug delivery, minimizing systemic toxicity.

Market Share: Strong presence in hematologic ADC segment.

Padcev (Enfortumab Vedotin)

Indications: Urothelial cancer and bladder cancer.

Market Trend: Emerging adoption in oncology with promising trial outcomes.

Trodelvy (Sacituzumab Govitecan)

Focus: Breast and lung cancers.

Investment: Gilead has received up to $210 million for clinical trials, emphasizing lung cancer applications.

Polivy (Polatuzumab Vedotin)

Use Case: Approved for blood cancers, especially B-cell lymphoma.

Targeted Action: Minimizes side effects compared to traditional chemotherapy.

Others:

New ADCs under clinical trials target a range of cancers including pancreatic ductal adenocarcinoma (PDAC), Nectin-4, and TROP2, indicating a robust pipeline for future growth.

By Target

HER2 (Human Epidermal Growth Factor Receptor 2)

Market Share: Largest share of the ADC market.

Clinical Importance: HER2 overexpression drives aggressive breast cancer proliferation.

Therapeutic Impact: ADCs targeting HER2 (Kadcyla, Enhertu) significantly improve overall survival with manageable side effects.

Technology Advancement: Preclinical and clinical research continually enhances antibody-linker-payload design for HER2.

AI Integration: Tools like Galen Breast HER2 improve HER2 scoring, aiding precise patient selection for therapy.

CD22

Growth: Fastest-growing target segment.

Disease Focus: B-cell cancers (like leukemia) and autoimmune diseases (e.g., Sjogren’s, lupus).

Therapeutic Potential: Multiple modalities including monoclonal antibodies, ADCs, CAR-T therapy, and bispecific antibodies.

Clinical Impact: Offers more precise treatment with potentially fewer systemic side effects.

CD30

Indications: Primarily hematologic malignancies (Hodgkin lymphoma).

ADC Example: Adcetris uses CD30 targeting with cleavable linkers.

Impact: Improves patient outcomes in difficult-to-treat lymphomas.

Others:

Emerging targets like Nectin-4 (IPH4502 ADC) and TROP2 (PDAC ADC) indicate market diversification.

Future ADCs are expected to target novel antigens for personalized therapy.

By Technology

Cleavable Linkers

Dominance: 73% of ADCs use cleavable linkers.

Mechanism: Release cytotoxic payload specifically in tumor cells, exploiting tumor microenvironment properties.

Examples: Brentuximab Vedotin, Inotuzumab Ozogamicin.

Advantage: Stability in bloodstream minimizes off-target toxicity.

Non-Cleavable Linkers

Mechanism: Payload remains attached to antibody until internalized in tumor cells.

Use Case: Provides slower, controlled release of cytotoxic drug.

Advantage: Enhanced safety profile for certain tumor types.

Linkerless ADCs

Mechanism: Direct conjugation of cytotoxic drug to antibody.

Potential: Still experimental; may reduce complexity but requires precise targeting.

Payload Technologies:

MMAE (Monomethyl Auristatin E): Highly potent microtubule inhibitor.

MMAF (Monomethyl Auristatin F): Similar to MMAE but less cell-permeable, reducing off-target effects.

DM4: Microtubule inhibitor used in several ADCs for hematologic cancers.

Camptothecin: Topoisomerase I inhibitor; emerging in novel ADCs.

Others: Constant innovation in payload chemistry drives ADC differentiation.

By Region

North America

Dominance: Largest share at 53% in 2023.

Drivers: High cancer incidence, robust biotech startups, strong FDA regulatory framework.

U.S. Cancer Data (2024): 2,001,140 new cases; 611,720 deaths.

Healthcare Spend: $208.9 billion in 2020; projected increase with aging population.

Europe

Mature Market: Strong presence of established ADC manufacturers (Roche, AstraZeneca).

Regulatory Support: EMA approvals streamline ADC adoption.

Asia Pacific

Fastest Growth: Driven by rising disease incidence, government support, and adoption of advanced technology.

China: High population → greater demand; industry-institute collaborations expanding.

India: Rising ADC adoption; government support for affordability and healthcare infrastructure.

Latin America & Middle East/Africa

Emerging Markets: Growing healthcare investment and awareness driving future ADC adoption.

Trend: Focus on cost-effective treatments and increasing access to ADCs.

Top 5 FAQs

1 What is the ADC market size and growth?

●Projected to grow from USD 13.51B in 2025 to USD 29.9B by 2034, CAGR 9.23%.

2 Which region leads ADC adoption?

●North America dominated with 53% share in 2023.

3 Which ADC products dominate the market?

●Kadcyla holds the largest share; Enhertu grows fastest.

4 How is AI impacting the ADC market?

●Enhances drug discovery, trial efficiency, patient personalization, manufacturing, and predictive analytics.

5 What are major market drivers?

●Rising cancer incidence, technological advancements, personalized medicine, AI adoption, and regulatory support.

Access the Dashboard: https://www.towardshealthcare.com/access-dashboard

Immediate Delivery Available | Buy This Premium Research @ https://www.towardshealthcare.com/price/5178

Become a valued research partner with us – https://www.towardshealthcare.com/schedule-meeting

You can place an order or ask any questions, please feel free to contact us at [email protected]

Powering Healthcare Leaders with Real-Time Insights: https://www.towardshealthcare.com/healthcare-intelligence-platform

Europe Region – +44 778 256 0738

North America Region – +1 8044 4193 44

APAC Region: +91 9356 9282 04

Web: https://www.towardshealthcare.com

Find us on social platforms: LinkedIn | Twitter | Instagram | Medium | Pinterest