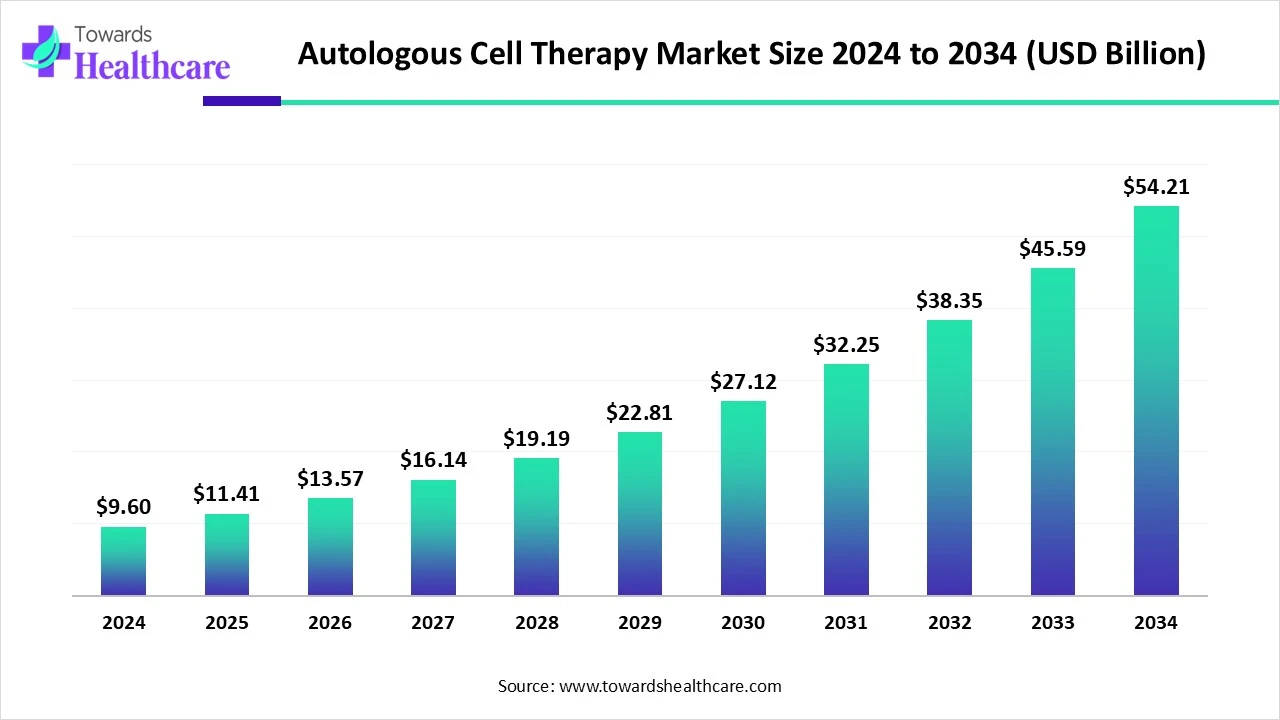

The global autologous cell therapy market—valued at US$ 9.6 billion in 2024 and US$ 11.41 billion in 2025—is projected to expand to approximately US$ 54.21 billion by 2034 (a CAGR of 18.9% from 2025–2034), driven by advances in personalized/regenerative medicine, regulatory support and manufacturing automation while constrained by high per-patient costs.

Download the free sample and get the complete insights and forecasts report on this market @ https://www.towardshealthcare.com/download-sample/6022

Market size

Historical and forecast headline numbers

●2024 market size: US$ 9.6 billion

●2025 market size: US$ 11.41 billion

●2034 projected market size: US$ 54.21 billion

●Forecast period used here: 2025 → 2034 (9 years); reported CAGR: 18.9%.

●Absolute and relative growth (2025→2034)

●Absolute increase: US$ 42.80 billion (54.21 − 11.41).

●Growth multiple: market is expected to become 4.75× larger in revenue by 2034 vs 2025 (54.21 / 11.41 ≈ 4.75).

●The implied effective annual growth rate matches the reported 18.9% CAGR (i.e., 18.90% annualized).

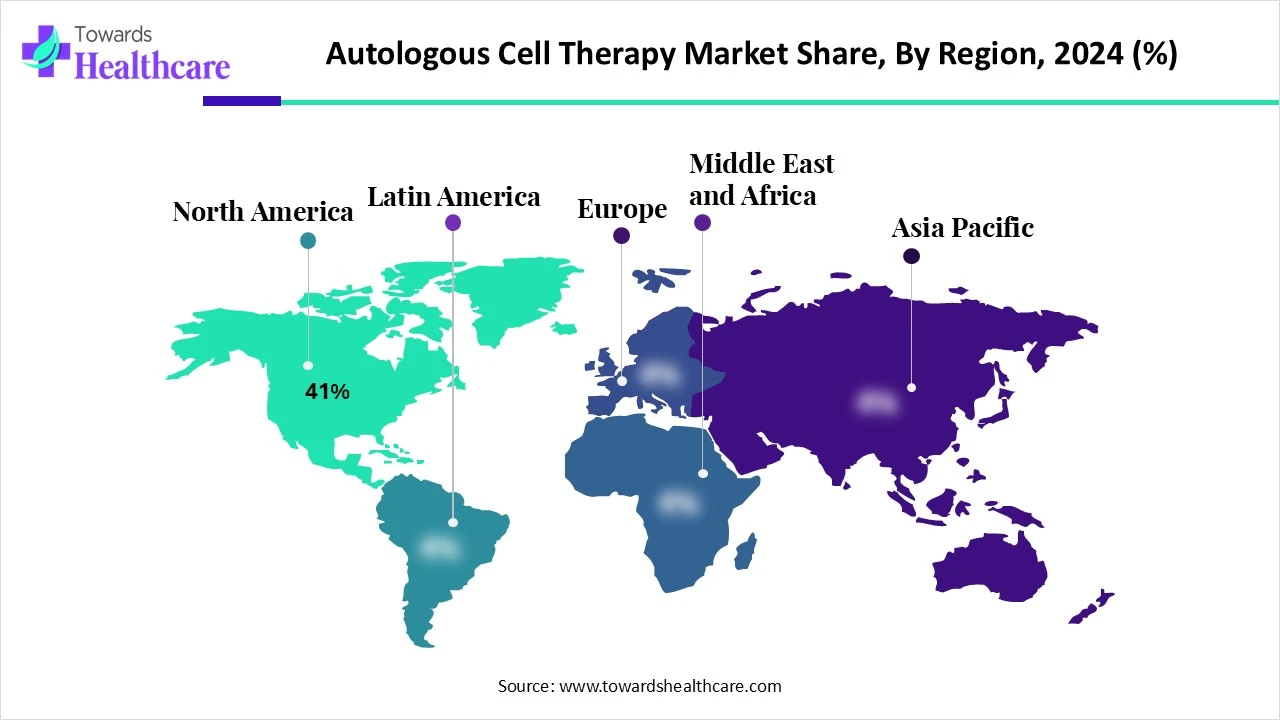

●2024 revenue composition anchors (high-level shares)

●North America dominated in 2024 with 41% share of the global market.

●CAR-T (autologous) accounted for the largest therapy-type share: 32% in 2024.

●By technology, genetic modification techniques held 30% share in 2024.

●Hospitals were the largest end-user channel with 45% share in 2024.

Unit / price context

●Typical treatment price range cited: US$ 300,000 – US$ 500,000 per patient (illustrative of today’s cost challenge).

●Reported automation examples (CiRA) suggest potential to reduce manufacturing cost orders of magnitude in select programs (example given: a reduction from ¥50 million → ¥1 million per patient in an iPSC program using automation — strong proof-of-concept, though not yet universal).

Market structure & concentration

●The market comprises a mix of large pharmas/biotechs with commercial capabilities and numerous specialized biotech companies focused on specific cell modalities (CAR-T, gene-edited stem cells, MSCs, TILs, etc.).

●High regulatory hurdles, specialized manufacturing and hospital delivery logistics concentrate early commercial volumes in well-resourced firms and centers of excellence.

Investment dynamics embedded in size

●The rapid projected growth (4.75×) implies heavy new capacity build, clinical pipelines maturing to commercialization, and payer negotiation activity to accommodate high-cost curative/one-time therapies.

Market Trends

Regulatory approvals enabling new indications (2024–2025)

●April 2025: Abeona’s Zevaskyn (prademagene zamikeracel) — first autologous, cell-based gene therapy for wounds in RDEB — U.S. FDA approval (demonstrates gene-corrected autologous skin cell commercialization).

●31 Jan 2025: NHS approval of exagamglogene autotemcel under a managed access scheme — first CRISPR-based gene-edited stem cell therapy for sickle cell disease (signals regulatory willingness for gene-edited autologous products under managed programs).

EU market expansion via marketing authorizations

●July 2025: Autolus Therapeutics received European Commission marketing authorization for Aucatzyl, an autologous CAR-T therapy for certain B-cell precursor ALL — indicates EU commercialization and geographic expansion of autologous CAR-T access.

Manufacturing automation & platform launches

●7 May 2024: Cellipont Bioservices & Adva Biotechnology launched the ADVA X3 automated AI-driven platform to accelerate CAR-T manufacturing in North America (an example of platform automation moving from R&D to production).

●Kyoto University / CiRA (Jan 2025): automated production of autologous iPS cells in Osaka — claims cost reductions from ¥50M to ¥1M per patient and capacity for ~1,000 patients/year (illustrates scale-up potential for iPSC workflows).

Strategic manufacturing partnerships & capacity expansion

●June 25, 2025: AGC Biologics announced a new facility in Yokohama, Japan to expand cell-therapy process development and clinical manufacturing for autologous and allogeneic programs — reflects regional capacity build for APAC demand.

●June 2025: MaxCyte & Ori Biotech collaboration to integrate closed-loop systems for improved autologous therapy manufacturing efficiency.

AI, digital twins and process intelligence adoption

●AI and predictive analytics are being applied across process control, digital twins, QC monitoring and scale-out strategies to improve consistency and shorten turnaround times — these technologies are already being integrated into production platforms (examples noted above).

Therapy diversification beyond oncology

●The report highlights widening clinical activity and approvals in wound healing, rare genetic disorders, neurodegenerative disease (early trials), ophthalmology and orthopedics — pointing to slower but meaningful adoption outside blood cancers.

Shift to decentralized and point-of-care manufacturing

●Closed-system, point-of-care manufacturing and specialty clinic delivery are flagged as growth vectors — enabling more patient-centric models and relieving hospital capacity constraints over time.

Payer evolution and managed access models

●Examples of managed access (NHS CRISPR approval) and increasing payer interest in long-term cost offsets are beginning to shape formulary pathways for one-time/high-cost therapies.

Clinical evidence continues to drive value capture

●CAR-T’s early clinical successes in hematologic malignancies are the historical catalyst; now, gene-edited stem cells, iPSC-based approaches and improved cell expansion systems are fueling future TAM growth.

Persistent cost & logistics constraint

●Despite all the above, high per-patient cost, complex logistics and manufacturing variability remain key restraints needing systemic solutions (automation, AI, closed systems, partnerships).

Roles / impacts of AI on the autologous cell therapy market

Closed-loop process control & predictive culture optimization

●Mechanism: AI models ingest sensor, imaging and molecular QC data from bioreactors to predict cell growth trajectories and automatically adjust feed/conditions.

●Benefit: Higher batch consistency, reduced failure rates and shorter culture cycles → higher yield per run.

●Implication: Enables smaller footprint facilities to produce more doses reliably; directly lowers per-dose cost when paired with automation (as in ADVA X3 style platforms).

Digital twins for manufacturing scale-out

●Mechanism: Create a virtual replica (digital twin) of a patient-specific manufacturing run to test parameter changes without risking the real batch.

●Benefit: Safe experimentation to shorten process development, faster tech-transfer, mitigated batch risk.

●Implication: Vital for unique autologous batches where every run is single-patient.

Predictive quality control (QC) and release decisioning

●Mechanism: ML models predict potency and safety from upstream signatures (metabolites, cell markers) allowing early go/no-go decisions.

●Benefit: Reduces late-stage batch failures and QC cycle times—critical for time-sensitive autologous therapies.

●Implication: Faster patient treatment timelines and lower waste.

Automated image analysis for cell identity & morphology

●Mechanism: Computer vision classifies cell morphology, confluency, contamination and differentiation states during culture.

●Benefit: Objective, continuous monitoring vs episodic manual inspection; decreased human variability.

●Implication: Supports scaling to 1,000 patient/year claims (CiRA example) by reducing manual QC burden.

AI-driven scheduling & logistics orchestration

●Mechanism: Algorithms coordinate leukapheresis/collection, transport, manufacturing slots and return infusion to optimize turnaround.

●Benefit: Minimized patient wait time and optimized use of constrained manufacturing slots.

●Implication: Increases throughput of existing facilities without physical expansion.

Supply chain risk analytics for critical reagents

●Mechanism: Predictive models flag reagent shortage risks, optimize inventory; suggest alternate vendors.

●Benefit: Reduces batch delays due to raw material shortages.

●Implication: Greater resilience for hospital/regional manufacturing networks.

Adaptive dosing and patient stratification

●Mechanism: Integrate patient-specific clinical/genomic data with historical outcome models to recommend cell dose and preconditioning regimens.

●Benefit: Potential to improve efficacy/safety and reduce need for retreatment.

●Implication: Better health economics and more favorable payer discussions.

Accelerated process development and transfer (AI-guided DoE)

●Mechanism: ML automates design-of-experiments and finds optimal parameter combinations faster than trial-and-error.

●Benefit: Shorter time from bench to clinic, reducing cost of development.

●Implication: Enables smaller companies to industrialize processes more rapidly.

Regulatory intelligence and documentation automation

●Mechanism: NLP tools extract required evidence and auto-generate standardized sections for IND/BLA/market authorization dossiers.

●Benefit: Reduces regulatory submission time and errors, speeds approvals under adaptive pathways.

●Implication: Easier managed access filings (like NHS examples), faster time-to-market.

Post-market real-world evidence (RWE) and safety surveillance

●Mechanism: AI analyses of EHRs, registries and real-world datasets to detect long-term efficacy signals and rare adverse events.

●Benefit: Supports payer value models and post-approval commitments while informing future label expansions.

●Implication: Strengthens payer confidence in high-cost one-time therapies and shapes outcome-based contracts.

Regional insights

A. North America (lead, 41% share in 2024)

Ecosystem strengths

●World-class clinical trial networks, numerous centers of excellence, and leading biotech/pharma players — these translate into fast clinical translation and early commercial uptake.

Regulatory & payer enablers

●Incentives like RMAT (U.S.) and precedent for high-value reimbursements accelerate adoption of life-saving products.

Delivery model dominance

●Hospitals remain primary administration centers due to the ability to manage acute toxicities (e.g., cytokine release syndrome) — explains the 45% hospital end-user share.

Consequence

●Large share, high per-patient spending, and concentrated manufacturing capacity — North America will continue to lead short-term commercialization and capture disproportionate revenues.

B. Europe

Regulatory fragmentation vs centralized pathways

●Centralized EC marketing authorization enables EU-wide access (example: Autolus Aucatzyl). However, national HTA/payer decisions can slow adoption in specific countries.

Managed access & conditional reimbursement

●NHS examples (managed access for CRISPR therapy) show willingness for innovative access mechanisms to balance uncertainty and patient need.

C. Asia-Pacific (fastest growth projection)

Drivers

●Rapid government investment, expanding clinical trial activity, rising healthcare infrastructure and local manufacturing builds (e.g., AGC Biologics in Yokohama).

Country notes

●China: Growing biotech investment, regulatory streamlining and hospital adoption are accelerating local commercialization pathways.

●Japan: Academic centers (CiRA) and tech adoption support advanced programmes (automated iPSC production example).

●India: Emerging talent, regulatory reforms and private investment are building domestic capabilities and potentially lower-cost delivery models.

Consequence

●APAC is a strategic growth corridor for manufacturers building regional CDMOs and commercial partners.

D. Latin America, Middle East & Africa

Current state

●Lower penetration due to constrained infrastructure, limited payer capacity and fewer specialized centers.

Opportunity

●As manufacturing decentralizes (closed systems) and cost per dose falls, targeted partnerships and technology transfer can open these markets for select indications.

Market dynamics

Drivers

●Personalized medicine momentum — autologous therapies match patient biology, lowering immunogenicity and improving durable response rates, especially in oncology.

●Regulatory pathways & designations — accelerated approvals, managed access schemes and RMAT-like frameworks support commercialization.

●Investment & partnerships — venture, strategic and CDMO partnerships scale manufacturing and distribution.

●Technology advances — gene editing, automated bioreactors and AI process control lower variability and cost over time.

Restraints

●High manufacturing & treatment cost — current per-patient costs (US$300k–500k) limit access and strain payers.

●Complex logistics & single-patient runs — bespoke manufacturing precludes classic economies of scale.

●Regulatory/quality complexity — lot-to-lot variability and stringent QC create barriers to commoditization.

Opportunities

●New therapeutic areas — wound healing, neurology, ophthalmology, orthopedics and rare diseases extend TAM beyond oncology.

●Decentralized manufacturing / point-of-care — closed, portable systems and specialty clinics can bring treatment closer to patients and lower hospital bottlenecks.

●AI + automation to reduce costs — CiRA and ADVA X3 show the pathway to large cost reductions and greater throughput.

Value-chain implications (R&D → Patient) — deep

●R&D / Discovery: gene editing and cell engineering drive candidate differentiation (CRISPR, non-viral delivery, antigen design).

●Process development: focus on scale-up/scale-out using microcarriers, automated bioreactors and AI-guided process optimization.

●Clinical manufacturing: the rise of specialized CDMOs and hospital/clinic GMP suites for point-of-care manufacture.

●Distribution & logistics: robust cryo/temperature logistics, same-day/next-day shipment models, and scheduling systems for single-patient runs.

●Delivery & patient management: hospital readiness for infusion, toxicity management, and long-term follow-up infrastructure (RWE registries) for safety and payer outcomes.

Top 10 companies

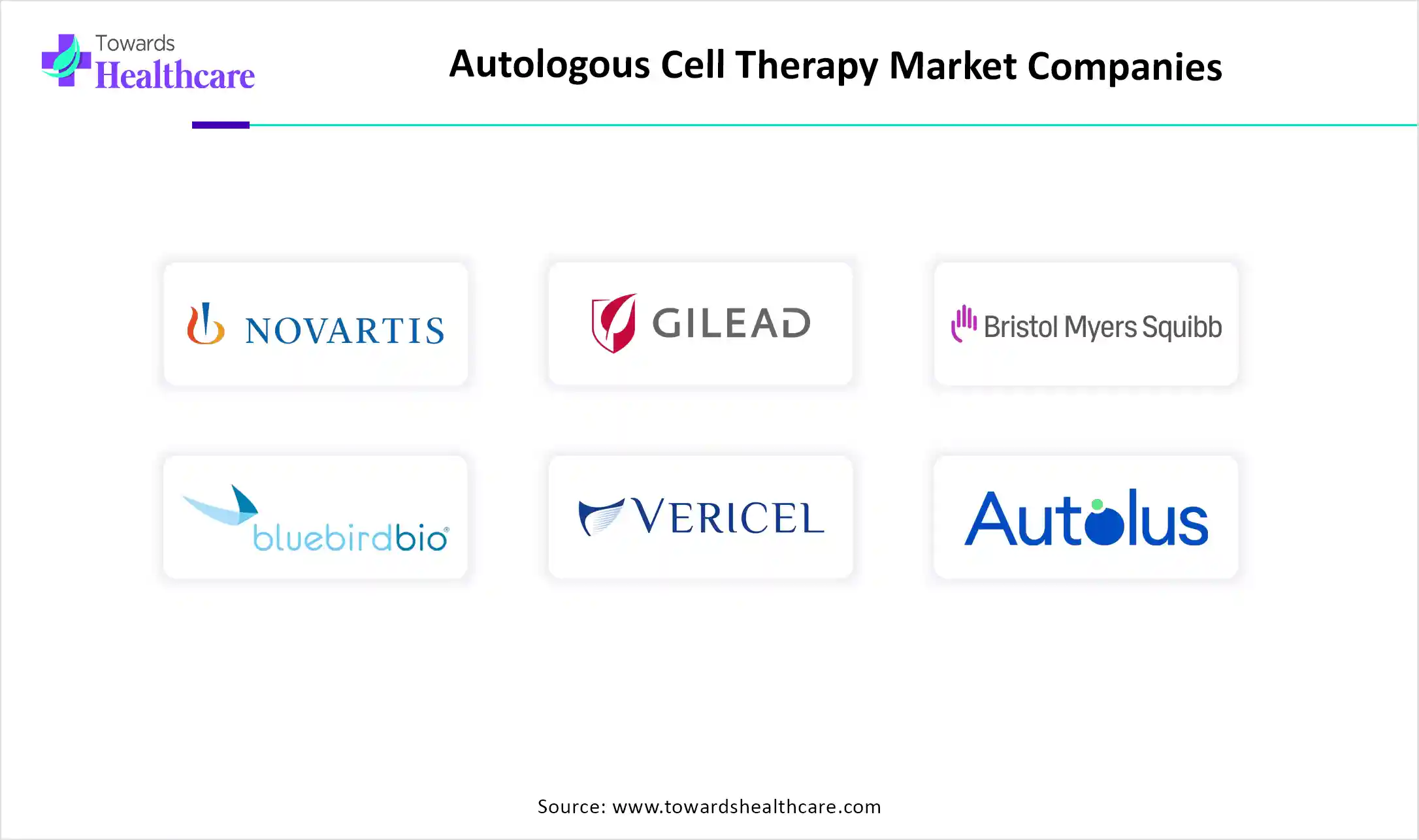

Novartis AG

●Product focus: Advanced autologous cell therapies (CAR-T and gene-modified cell programs).

●Overview: Large global pharma with commercialization, regulatory and global supply chain experience.

●Strengths: Global commercial footprint, robust manufacturing networks, strong payer negotiation experience—critical for scaling autologous launches.

Gilead Sciences, Inc. (Kite Pharma)

●Product focus: Autologous CAR-T / engineered T-cell therapies.

●Overview: Kite operates as a major cell-therapy developer with focus on hematologic oncology.

●Strengths: Deep clinical development expertise in CAR-T, manufacturing know-how, strategic partnerships.

Bristol Myers Squibb

●Product focus: Autologous and gene-modified cell therapy portfolios (immuno-oncology focus).

●Overview: Big pharma investor in cell therapy R&D and commercialization.

●Strengths: Large commercial organization, capacity to integrate complex therapies into clinical practice and payer models.

Bluebird Bio, Inc.

●Product focus: Gene-therapy and gene-modified cell programs (autologous vectors in rare diseases/oncology).

●Overview: Specialist in gene-modified cell approaches.

●Strengths: Deep expertise in vector design and gene correction, with a focus on rare genetic disorders.

Vericel Corporation

●Product focus: Autologous cell therapies for regenerative/repair indications (e.g., skin, cartilage).

●Overview: Focused regenerative medicine company delivering autologous solutions.

●Strengths: Commercial experience in tissue/regenerative products and site-of-care deployment.

Autolus Therapeutics plc

●Product focus: Autologous CAR-T cell therapies (notably EU marketing authorization for Aucatzyl per supplied data).

●Overview: Commercializing autologous CAR-T in major markets.

●Strengths: Clinical experience in CAR-T design and now EU regulatory approval — a proof point for commercialization.

Iovance Biotherapeutics, Inc.

●Product focus: Autologous TIL (tumor-infiltrating lymphocyte) therapies and other personalized T-cell products.

●Overview: Specialist in TIL approaches targeting solid tumors.

●Strengths: Scientific focus on solid tumor T-cell approaches, clinical pipeline experience in TIL manufacturing.

Orchard Therapeutics plc

●Product focus: Ex vivo gene-corrected autologous stem cell therapies for rare genetic disorders.

●Overview: Developer of autologous, gene-modified stem cell therapies.

●Strengths: Experience with ex vivo gene correction workflows and managed access/regulatory negotiations.

Poseida Therapeutics, Inc.

●Product focus: Gene-engineered autologous cell therapies (non-viral methods / CAR-T etc.).

●Overview: Developing autologous advanced cell constructs with proprietary engineering approaches.

●Strengths: Novel engineering platforms aimed at increasing potency and manufacturability.

Adaptimmune Therapeutics plc

●Product focus: T-cell receptor (TCR) engineered autologous therapies.

●Overview: Focus on TCR-based autologous immunotherapies (targets a different antigen class than CAR-T).

●Strengths: TCR expertise for intracellular antigen targeting and potential in solid tumors.

Latest announcements

Abeona Therapeutics — FDA approval of Zevaskyn (Apr 2025)

●What happened: FDA approval for Zevaskyn, the first autologous cell-based gene therapy for wounds in RDEB (uses patient’s skin cells with corrected COL7A1).

●Implications: Demonstrates regulatory acceptance for gene-corrected autologous dermatologic products; opens a commercial precedent for autologous regenerative skin therapies and creates a template for payer discussions regarding durable benefit.

Autolus Therapeutics — EC marketing authorization for Aucatzyl (July 2025)

●What happened: EU marketing authorization for an autologous CAR-T for relapsed/refractory B-cell precursor ALL (adult).

●Implications: Solidifies EU pathway for autologous CAR-T reimbursement & distribution; encourages other CAR-T developers to pursue centralized EU approvals and cross-border commercialization.

CiRA Foundation / Kyoto University — automated autologous iPS production (Jan 2025)

●What happened: Start of automated iPSC production in Osaka, claimed cost reduction from ¥50M → ¥1M per patient and capacity for 1,000 patients/year.

●Implications: Proof that automation + process control can massively lower costs and scale iPSC-based autologous programs—if generalizable, this is transformational for broader autologous cell therapy affordability.

ADVA X3 platform launch (Cellipont & Adva Biotechnology, May 7, 2024)

●What happened: Launch of an AI-driven automated CAR-T manufacturing platform in North America.

●Implications: Example of industry moving from manual, bespoke processes to automated production, which should reduce turnaround time and variability.

NHS approval — exagamglogene autotemcel (31 Jan 2025)

●What happened: Managed-access scheme approval for CRISPR-based gene-edited stem cell therapy for sickle cell disease.

●Implications: Shows public payers will adopt managed access to provide early availability while collecting RWE; favorable for other gene-edited autologous products seeking reimbursement.

AGC Biologics — new Yokohama facility (25 Jun 2025)

●What happened: Facility expansion for process development and clinical manufacturing in Japan.

●Implications: Regional manufacturing capacity build to enable Asia Pacific commercial scale-up.

MaxCyte & Ori Biotech collaboration (Jun 2025)

●What happened: Collaboration to improve manufacturing efficiency and scale via integrated closed-loop systems.

●Implications: Examples of CDMO/platform consolidation to tackle autologous manufacturing bottlenecks.

Regeneration Biomedical — Phase 1 update (May 2025)

●What happened: Presented updated Phase 1 data of an autologous, adipose-derived stem cell therapy in Alzheimer’s showing safety and cognitive improvements.

●Implications: Suggests potential non-oncology expansion of autologous approaches into neurodegeneration; early signal may stimulate further investment in this space.

AstraZeneca — planned acquisition of EsoBiotec (Mar 2025)

●What happened: Announcement of up to US$ 1 billion deal to strengthen in vitro cell therapy capabilities.

●Implications: Indicates big pharma strategic moves to secure cell-therapy process/assay capabilities (in vitro development + manufacturing support).

Industry executive commentary (Hope Biosciences; Autolus CEO comments)

●What happened: Public statements highlighting MSC safety track record and the clinical potency/complexity of CAR-T therapies.

●Implications: Reinforces investor/clinician confidence in certain modalities and acknowledges the need to overcome logistical challenges.

Recent developments

●Proof-points for automation & scaling — CiRA and ADVA X3 examples demonstrate production automation moving from concept to real-world capacity (CiRA’s 1,000 patients/year claim) and AI-driven manufacturing platforms for CAR-T. These are the most concrete levers to materially reduce cost and improve throughput.

●Regulatory milestones unlocking new indications — approvals and managed-access use (Abeona, Autolus, NHS CRISPR) widen the permitted clinical/marketing space for autologous therapies beyond hematologic cancers into wounds and genetic disease.

●Strategic industry consolidation & capacity build — pharma acquisitions (AstraZeneca → EsoBiotec), CDMO expansions (AGC Biologics), and platform partnerships (MaxCyte/Ori) are actively addressing manufacturing and scale barriers.

●Clinical expansion into non-oncology — Phase 1 Alzheimer’s adipose-derived stem cell updates indicate movement toward clinical proof in neurodegenerative disorders — if validated, this extends the market TAM significantly.

●Integrated manufacturing collaborations — collaborations integrating closed-loop systems point to the industry moving toward standardized, interoperable manufacturing ecosystems (reducing bespoke setups).

Segments covered

By Therapy Type (segments + subpoints)

Stem Cell Therapy

●Hematopoietic Stem Cell Therapy (HSCT): historically widespread; autologous HSCT used for hematologic conditions.

●Mesenchymal Stem Cells (MSCs): broad investigational space (safety track record emphasized).

●Neural stem cells / adipose-derived: development for neurology and regenerative indications.

Non-Stem Cell Therapy

●Non-genetically modified T-cells & macrophage therapies: simpler manufacturing, lower regulatory complexity for some indications.

●Fibroblast & other somatic cell therapies: used in dermal/regenerative applications.

Gene-Modified Autologous Cell Therapy

●CAR-T Cell Therapy: largest segment circa 2024 (32% share) — high clinical impact in hematology.

●TCR-T Cell Therapy: targets intracellular antigens; potential for solid tumors.

●Gene-edited stem cells: fastest growing (driven by CRISPR and other editors).

By End-User

●Hospitals — dominant channel (45% share); necessary for complex infusions and toxicity management.

●Specialty Clinics — fastest growing as closed systems and point-of-care manufacturing enable decentralization.

●Academic & Research Institutes — centers for trials and early adoption.

By Technology

●Cell Harvesting & Processing — leukapheresis, tissue harvest; logistics complexity.

●Genetic Modification Techniques — viral vectors, non-viral delivery, gene-editing tools (30% share in 2024).

●Cell Expansion & Culture Systems — fastest growing tech area: bioreactors, microcarrier systems, automation.

●Cryopreservation & Storage — critical for logistics; cryo quality affects product potency.

●Quality Control & Testing — molecular, potency, sterility, release assays — bottleneck for throughput.

By Region (already covered in Regional Insights)

●North America, Europe, Asia Pacific, Latin America, Middle East & Africa — each with the structural drivers and constraints noted earlier.

Top-5 FAQs

Q1 — What is the current market size and growth outlook?

A: The market was US$ 9.6B in 2024, US$ 11.41B in 2025, and is projected to reach US$ 54.21B by 2034, growing at a CAGR of 18.9% from 2025–2034 (a 4.75× revenue increase over that period).

Q2 — Which region leads the market and what is its share?

A: North America dominated in 2024 with a 41% share, driven by strong clinical research, regulatory support, established manufacturing and payer pathways.

Q3 — Which therapy and technology types dominated in 2024?

A: By therapy type, CAR-T cell therapy held the largest share (32%) in 2024. By technology, genetic modification techniques formed the largest technology slice at 30% in 2024.

Q4 — What are the biggest barriers to growth?

A: High per-patient costs (typically US$ 300k–500k), complex bespoke manufacturing, logistical challenges and stringent QC/regulatory requirements remain the primary restraints.

Q5 — How will AI and automation change the economics?

A: AI-driven automation and closed-loop manufacturing (examples: ADVA X3, CiRA automated iPSC production) are expected to improve reproducibility, reduce failure rates and materially lower costs (CiRA reported a reduction ¥50M → ¥1M per patient for an automated iPSC program), unlocking scale and widening access.

Access our exclusive, data-rich dashboard dedicated to the therapeutic area sector – built specifically for decision-makers, strategists, and industry leaders. The dashboard features comprehensive statistical data, segment-wise market breakdowns, regional performance shares, detailed company profiles, annual updates, and much more. From market sizing to competitive intelligence, this powerful tool is one-stop solution to your gateway.

Access the Dashboard: https://www.towardshealthcare.com/access-dashboard

Immediate Delivery Available | Buy This Premium Research @ https://www.towardshealthcare.com/price/6022

Become a valued research partner with us – https://www.towardshealthcare.com/schedule-meeting

You can place an order or ask any questions, please feel free to contact us at [email protected]

Powering Healthcare Leaders with Real-Time Insights: https://www.towardshealthcare.com/healthcare-intelligence-platform

Europe Region – +44 778 256 0738

North America Region – +1 8044 4193 44

APAC Region: +91 9356 9282 04

Web: https://www.towardshealthcare.com

Find us on social platforms: LinkedIn | Twitter | Instagram | Medium | Pinterest