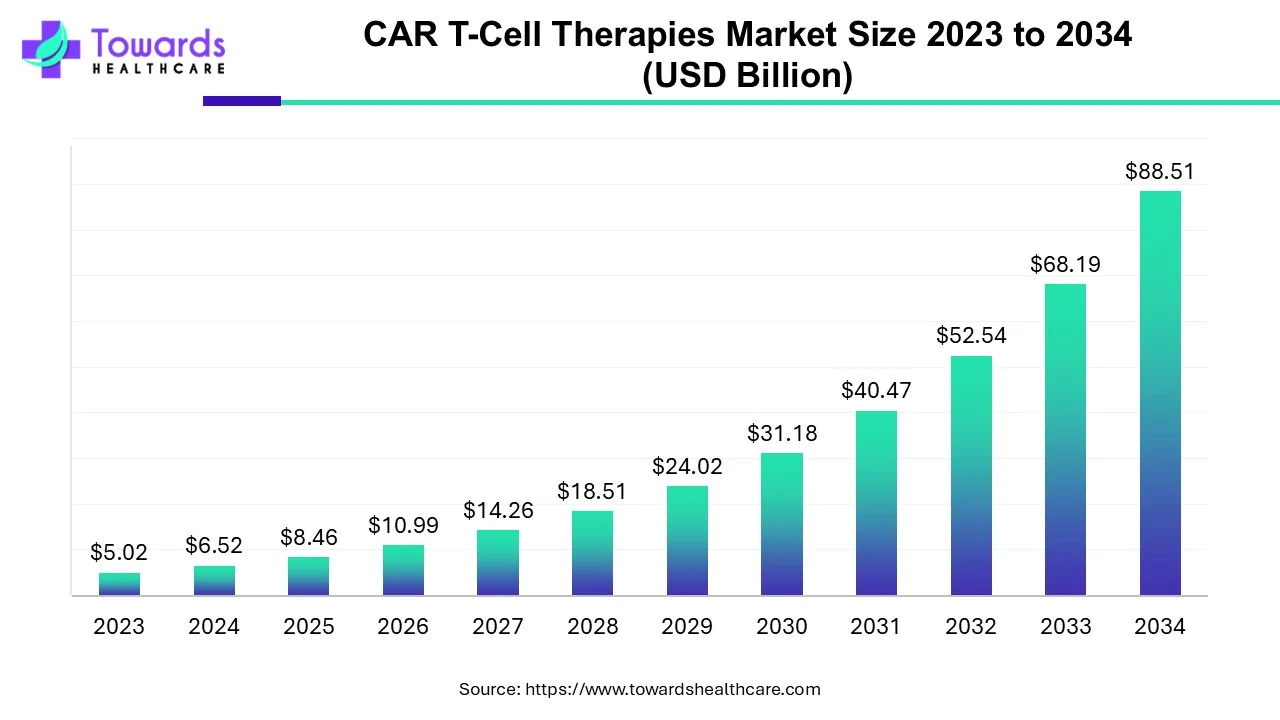

The global CAR T-cell therapies market was valued at USD 6.52 billion in 2024 and — growing at a 29.8% CAGR (2024–2034) — is projected to reach USD 88.51 billion by 2034, driven by accelerating clinical activity, rising cancer incidence and supportive policies.

Download Free Sample of CAR T-Cell Therapies Market Now and Get the Complete Report Easily at: https://www.towardshealthcare.com/download-sample/5028

CAR T-Cell Therapies Market Size

2024 baseline & decade outlook

Market value: USD 6.52B (2024).

Forecast: USD 88.51B by 2034 at 29.8% CAGR (2024–2034) — indicates a highly exponential growth profile typical of emerging, disruptive biotechnologies.

Clinical pipeline scale (demand signal)

1,703 CAR-T trials registered (as of 10 Oct 2025) — enormous pipeline breadth pointing to sustained future product approvals and commercial expansion.

Regulatory approvals as adoption anchors

7 FDA-approved CAR-T products by 2025 — these approved products establish reimbursement pathways, clinical infrastructure needs, and physician/patient awareness that underpin market growth.

Patient population & addressable market

U.S. estimated 187,740 diagnosed with leukemia, lymphoma, and myeloma — a clear immediate addressable population for blood-cancer CAR-T indications.

Australia: 19,400 blood-cancer diagnoses annually — demonstrates that even smaller markets contribute meaningful incremental demand.

Geographic growth asymmetry

North America dominated revenue share in 2024 (infrastructure + approvals).

Asia-Pacific forecasted as fastest-growing region due to policy support, trial growth, and domestic commercialization efforts (e.g., indigenous products).

End-user concentration

Hospitals were the largest end-user in 2024 (availability of infrastructure and reimbursement). Cancer treatment centers are the fastest-growing end-user as they scale specialized delivery capabilities.

Product mix & therapeutic focus

Market led by established CAR-T constructs (e.g., axicabtagene ciloleucel in 2024) with emergent growth from others (e.g., tisagenlecleucel) — an ongoing product mix shift as indications expand.

Economic footprint

High per-patient cost today (hundreds of thousands to millions) — but projected scale, manufacturing innovations, and policy moves are primary levers to improve affordability and expand access, magnifying total market value.

Investment & funding inputs

Government and public-private funding (examples: Canada, Australia, Germany investments listed) are materially increasing R&D and infrastructure spend — a multiplier on long-term market size.

Manufacturing & supply chain constraints

Complex GMP manufacturing and bespoke logistics (autologous workflows, cold chain) act as present capacity limits; solving them (automation, allogeneic approaches) will materially unlock larger portions of the forecasted USD 88B.

Market trends

Rapid pipeline expansion → commercial opportunity

Thousands of trials and multiple late-stage/pre-registration programs signal a multi-product commercial future rather than single-product dominance.

Shift from autologous to off-the-shelf strategies

Industry interest in allogeneic (donor/engineered universal) CAR-T is rising (forecast by experts) to reduce cost, speed delivery and scale capacity.

Geographic leadership shift

China and Asia accelerating clinical trial counts (China surpassed U.S. in trial numbers) — expect faster commercialization and localized manufacturing in APAC.

Diversification of indications

From hematologic malignancies toward solid tumors and non-oncology indications (R&D focus) — the next big value unlock if tumor microenvironment barriers are cracked.

Manufacturing automation & decentralization

Trend toward automated closed systems and cryopreservation to improve reproducibility and expand sites capable of delivering CAR-T.

Value-based pricing & reimbursement evolution

With high therapy costs, payers and providers are experimenting with outcomes-based contracts and new reimbursement models to widen access.

Strategic collaborations & M&A

Partnerships (industry–academic, biotech–big pharma) and licensing deals accelerate capability access (e.g., commercialization partnerships cited), consolidating the ecosystem.

Regulatory maturation

Regulators increasingly provide clearer pathways for cell therapies (approvals and pre-registrations), which reduces time-to-market risk and encourages investment.

Infrastructure build-out (centers of excellence)

More FACT-accredited centers and cancer treatment centers are being established; hospitals lead today but specialized centers are scaling rapidly.

Patient-centric service models

Expansion of patient support, long-term follow up programs, and home-care touchpoints as CAR-T becomes part of chronic survivorship models.

AI impact / role 10 ways AI transforms the CAR T-Cell market

Target discovery & antigen selection

Role: AI models (pattern recognition on multi-omics and clinical data) identify novel, tumor-specific antigens and antigen combinations to improve specificity and avoid off-tumor toxicity.

Impact: Faster target triage reduces wet-lab cycles and focuses clinical candidates with higher predicted safety/efficacy.

Designing improved CAR constructs

Role: Generative and predictive models evaluate CAR domain choices (scFv sequences, co-stimulatory domains) to optimize signaling strength, persistence, and safety.

Impact: Higher success rate in preclinical optimization and fewer failures entering costly clinical stages.

Patient selection & responder prediction

Role: AI integrates genomics, tumor microenvironment markers, prior treatment history, and wearable data to predict which patients will respond and who are at high risk of severe toxicities (e.g., CRS, neurotoxicity).

Impact: Improved clinical trial enrichment, better real-world outcomes, lower SAE rates and more cost-effective therapy allocation.

Adaptive clinical trial design

Role: Machine learning supports adaptive trial arms, real-time safety monitoring and dynamic dose selection using Bayesian and reinforcement learning strategies.

Impact: Trials become faster, smaller and more informative — accelerating approvals and reducing development costs.

Manufacturing automation and process control

Role: AI monitors and controls bioprocess parameters (cell growth, viability metrics) across closed manufacturing systems to ensure batch-to-batch consistency.

Impact: Higher yields, reduced failures, lower cost per dose — directly affecting scalability and price.

Supply-chain & logistics optimization

Role: Predictive scheduling and route optimization for patient leukapheresis, cryo-storage, and dose delivery minimize delays and maintain chain-of-identity.

Impact: Shorter turnaround times, fewer product losses, and better patient experience.

Real-time safety monitoring & early intervention

Role: AI analyses physiologic signals and lab trends (including from wearables) to detect early signs of cytokine release syndrome or neurotoxicity.

Impact: Quicker interventions reduce morbidity, shorten ICU stays and improve survival statistics.

Post-market surveillance & durability prediction

Role: Machine learning models use long-term follow-up data to predict durability of response and late adverse events, informing payer models and clinician counseling.

Impact: Better actuarial models for outcomes-based reimbursement and clearer benefit-risk profiles.

Personalized combination strategies

Role: AI suggests individualized combination regimens (checkpoint inhibitors, targeted agents) based on tumor features and immune profiling to overcome resistance.

Impact: Raises overall durable response rates and expands indications, especially for solid tumors.

Clinical decision support & physician adoption

Role: AI tools synthesize patient eligibility, sequencing of therapies and predicted outcomes into usable dashboards for oncologists and care teams.

Impact: Lowers clinician cognitive load, standardizes care pathways, and accelerates appropriate CAR-T referrals.

Regional insights

North America (dominant in 2024)

Advanced infrastructure & approvals

Presence of major CAR-T manufacturers, manufacturing capacity and 7 FDA approvals by 2025 underpin market leadership.

Clinical adoption network

~311 FACT-accredited U.S. hospitals (example figure) provide distribution scale and patient access.

High per-patient spend & payer frameworks

Reimbursement models evolving; outcomes data from early adopters shape payer contracting globally.

Asia-Pacific (fastest growth forecast)

Trial volume & domestic leadership

China surged in trial counts (surpassed U.S. in clinical trial count) — indicating research concentration and near-term commercialization.

Policy & industrialization

Government initiatives (e.g., Atmanirbhar Bharat / Made in India) and local product launches (India’s indigenously developed CAR-T in Apr 2024) accelerate local manufacturing.

Access & scale tradeoff

Large patient populations provide scale, but uneven infrastructure and reimbursement across APAC require region-specific delivery models (hub-and-spoke, center of excellence networks).

Europe

Innovation with regulatory caution

Europe invests in production/clinical projects (public funding examples) and focuses on safety/regulatory rigor; this supports high-quality evidence generation.

Collaborative research ecosystems

Academic centers and government funding (German BMBF, others) drive translational programs and industry collaborations.

Canada / Australia (notable national investments)

Targeted funding to expand access

Canada: BioCanRx funding for CAR-T & RNA vaccine projects.

Australia: NSW investment (A$20.7M) to improve access to specialized therapies.

Smaller populations but strategic pilots

These investments create models for national reimbursement and center scaling that larger markets can emulate.

Emerging markets (LATAM, MEA)

Long-term potential but near-term barriers

Infrastructure and affordability challenges mean slower adoption initially; donor/allogeneic strategies and cost reductions needed for meaningful penetration.

Market dynamics

Driver — Rising cancer incidence

Growing numbers of hematologic cancers (e.g., 187,740 U.S. cases) directly expand the patient base for approved CAR-T indications.

Driver — Clinical pipeline & approvals

1,703 trials and multiple late-stage/pre-registration programs create near-term launch potential and long-term therapeutic diversity.

Driver — Government funding & policy

National investments (Canada, Australia, Germany, India initiatives) lower translational risk and accelerate infrastructure and access.

Restraint — High cost & access inequality

Therapy cost (hundreds of thousands to millions) restricts uptake; payer models and manufacturing cost reductions are critical to overcome this restraint.

Restraint — Manufacturing complexity

Autologous workflows, GMP needs and bespoke logistics are bottlenecks limiting scale and increasing per-dose cost.

Opportunity — Allogeneic/off-the-shelf platforms

Allogeneic approaches promise lower cost, faster delivery and simpler logistics — a major medium-term market disruptor.

Opportunity — Broadening indications

Expansion from lymphoma/ALL/MM into solid tumors and non-oncology areas would dramatically enlarge the addressable market.

Threat — Safety profile & adverse events

CRS, neurotoxicity and insertional risks require tight monitoring and can hamper adoption if not mitigated.

Enabler — AI & manufacturing automation

AI adoption and closed automated manufacture improve yields, reduce failures and compress timelines, enabling both scale and cost declines.

Competitive dynamic — partnerships & consolidation

Collaborations (e.g., commercial partnerships, R&D alliances) and likely M&A create varied competitive moats — companies with integrated tech/CMC and clinical strengths will lead.

Meet Top 10 innovators in the CAR T-Cell Therapies Market

Novartis

Product(s): Tisagenlecleucel (Kymriah)

Overview: One of the first movers with an approved CAR-T for ALL and some NHL indications.

Strength: Commercialization experience, global footprint, and regulatory precedent-setting; strong manufacturing & distribution capabilities.

Gilead Sciences / Kite (Gilead division)

Product(s): Axicabtagene ciloleucel (Yescarta); KTE-X19 programs

Overview: Major oncology player with multiple CAR-T approvals and broad clinical pipeline.

Strength: Deep clinical development expertise in hematologic malignancies and strong commercial oncology infrastructure.

Bristol-Myers Squibb (BMS)

Product(s): Lisocabtagene maraleucel (Breyanzi)

Overview: Large pharma with CAR-T portfolio and capability to integrate with immuno-oncology assets.

Strength: Financial muscle, global commercial reach and combination therapy potential with other oncology franchises.

Johnson & Johnson Services, Inc.

Product(s): (CAR-T programs / investments)

Overview: Big-pharma investor in next-generation cell therapy approaches.

Strength: Scale in R&D, manufacturing partnerships and ability to fund large multi-center trials.

CARsgen Therapeutics

Product(s): (e.g., partnerships for CT053 / zevor-cel commercialization in China)

Overview: China-based developer with commercialization focus in mainland China.

Strength: Local market knowledge, regulatory navigation in China and partnerships (e.g., Huadong Medicine) for market access.

Gilead / Juno (historical programs listed e.g., JCAR017) / (Poseida, JW Therapeutics)

Product(s): Multiple programs across companies — e.g., JCAR017, Orvacabtagene autoleucel

Overview: These companies represent biotech innovators with late-stage assets and regional commercialization plans.

Strength: Deep translational expertise and focused late-stage assets.

Aurora Biopharma / Cartesian Therapeutics / Miltenyi Biomedicine

Product(s): Descartes-11 (Cartesian); MB-CART2019.1 (Miltenyi)

Overview: Smaller biotech players advancing clinical candidates, often in specialized niches (e.g., MM, NHL).

Strength: Agility in novel biology, niche expertise and ability to collaborate with larger partners.

Lonza

Product(s): (CMO / manufacturing services)

Overview: Contract manufacturing and CMC partner for cell therapies, enabling commercial scale-up.

Strength: Global manufacturing footprint, GMP capabilities and critical role in scaling production.

JW Therapeutics

Product(s): JWCAR029; Juno-origin programs

Overview: China-focused CAR-T developer with pre-registration assets and commercialization plans.

Strength: Local regulatory alignment, rapid clinical progression and domestic partnerships.

Poseida Therapeutics / Bellicum / Curocell

Product(s): P-BCMA-101 (Poseida); BPX-603 (Bellicum); Curocell programs

Overview: Innovators with unique CAR designs, platform technologies and specific indication focuses (e.g., BCMA for myeloma).

Strength: Proprietary engineering platforms, strong IP and differentiated CAR constructs.

Latest announcements

Notable announcements

India — Indigenous CAR-T launch (Apr 2024)

What: President of India launched India’s first indigenously developed CAR T-cell therapy (IIT Bombay + Tata Memorial Center).

Why it matters: Signals national capability to develop and potentially manufacture CAR-T locally — may reduce cost and create a regional hub for other LMICs.

CARsgen & Huadong Medicine collaboration (Jan 2023 / CT053 commercialization)

What: CARsgen licensed zevorcabtagene autoleucel (CT053) to Huadong with a $29.7M initial payment and up to $152.4M in milestones.

Why it matters: Demonstrates sizable upfront investments for China commercialization and a pathway for domestic commercialization.

MGM Medical College — Maharaja Yashwantrao Hospital (Nov 2024)

What: Introduction of CAR-T therapy to treat blood cancer within an Indian medical center.

Why it matters: Expands geographic access and real-world treatment sites beyond a few global centers.

Vyriad & Novartis collaboration (Nov 2024)

What: Partnership to discover and develop in vivo CAR-T therapies using Vyriad’s targeted lentiviral vector and Novartis’ cell therapy expertise.

Why it matters: Moves toward in vivo CAR-T (direct in-patient gene transfer) — a potential shift from ex vivo manufacturing to in-body programming, which could dramatically simplify logistics and cost.

Moffitt Cancer Center & AstraZeneca (Sep 2024)

What: Strategic collaboration to accelerate CAR-T and T-cell receptor therapy development.

Why it matters: Combines academic translational research with pharma drug development strength to push next-gen cell therapies and potential combinations.

Recent development themes

Commercialization partnerships and regional deals (e.g., CARsgen/Huadong) point to rapid market localization.

Academic-industry launches (India, Moffitt) illustrate translation into clinical service delivery and combination R&D.

In vivo approaches (Vyriad/Novartis) represent a technological inflection point that could reshape the value chain.

Segments covered

By Drug Type

Axicabtagene ciloleucel — dominated in 2024 due to established use as second-line for large B-cell lymphoma.

Tisagenlecleucel — projected to grow significantly because of safety profile and use in younger patients (ALL and certain NHL).

Brexucabtagene autoleucel and Others — address niche indications (e.g., mantle cell lymphoma) and emerging constructs; “Others” cover next-gen CARs and platform variants.

By Indication

Lymphoma — largest revenue share in 2024 (high unmet need, limited small molecule options).

Acute lymphocytic leukemia (ALL) — fastest-growing segment due to pediatric/young adult approvals and strong response rates.

Chronic lymphocytic leukemia (CLL), Multiple myeloma (MM), Others — MM driven by BCMA-targeted CARs (Abecma, Carvykti).

By End-User

Hospitals — largest share (infrastructure, reimbursement alignment).

Cancer Treatment Centers — fastest growth due to specialized expertise and protocolized CAR-T delivery pathways.

By Geography

North America — mature market with approvals, infrastructure and payer systems.

Europe — innovation focused, regulatory rigor and growing investments.

Asia-Pacific — fastest growth (trial acceleration, national policy support).

Latin America / Middle East & Africa — nascent adoption; growth tied to affordability and capacity building.

Top 5 FAQs

-

Q: What is the current market size and projected growth for CAR-T therapies?

A: The market was USD 6.52B in 2024 and is projected to grow at 29.8% CAGR to approximately USD 88.51B by 2034. -

Q: How many CAR-T therapies are approved and how many trials are ongoing?

A: As of 2025, 7 CAR-T products had FDA approval; and 1,703 clinical trials for CAR-T interventions were registered on ClinicalTrials.gov (as of 10 Oct 2025). -

Q: Which regions lead and which are growing fastest?

A: North America held the major revenue share in 2024 (advanced infrastructure, approvals). Asia-Pacific is expected to witness the fastest growth, driven by rising trials, government support, and local product initiatives. -

Q: What are the main limitations of CAR-T therapy today?

A: Key limitations include high cost and access barriers, complex manufacturing and logistics, serious side effects (CRS, neurotoxicity), limited approved indications, and durability/relapse risks. Addressing manufacturing and safety are top priorities. -

Q: How will AI and new technologies affect the CAR-T market?

A: AI can accelerate target discovery, optimize CAR design, improve patient selection and monitoring, automate manufacturing, predict outcomes, and support real-time safety detection — collectively improving efficacy, lowering cost and increasing access.

Access our exclusive, data-rich dashboard dedicated to the therapeutics area sector – built specifically for decision-makers, strategists, and industry leaders. The dashboard features comprehensive statistical data, segment-wise market breakdowns, regional performance shares, detailed company profiles, annual updates, and much more. From market sizing to competitive intelligence, this powerful tool is one-stop solution to your gateway.

Access the Dashboard: https://www.towardshealthcare.com/access-dashboard

Checkout CAR T-Cell Therapy Market Report Now at: https://www.towardshealthcare.com/checkout/5028

About Us

Towards Healthcare is a leading global provider of technological solutions, clinical research services, and advanced analytics, with a strong emphasis on life science research. Dedicated to advancing innovation in the life sciences sector, we build strategic partnerships that generate actionable insights and transformative breakthroughs. As a global strategy consulting firm, we empower life science leaders to gain a competitive edge, drive research excellence, and accelerate sustainable growth.

Become a valued research partner with us – https://www.towardshealthcare.com/schedule-meeting

You can place an order or ask any questions, please feel free to contact us at sales@towardshealthcare.com

Powering Healthcare Leaders with Real-Time Insights: https://www.towardshealthcare.com/healthcare-intelligence-platform

Europe Region – +44 778 256 0738

North America Region – +1 8044 4193 44

APAC Region: +91 9356 9282 04

Visit Our Website: https://www.towardshealthcare.com

Find us on social platforms: LinkedIn | Twitter | Instagram | Medium | Pinterest